近几年乘商分化特征明显。今年市场受政策和春节因素影响,1-8月乘用车增速相对较好。商用车春节后市场才恢复,1-8月走势相对平稳。

近几年乘商分化特征明显。今年市场受政策和春节因素影响,1-8月乘用车增速相对较好。商用车春节后市场才恢复,1-8月走势相对平稳。Cui Dongshu pointed out that due to the increase brought by the non-RDE vehicle treatment in August last year, and this year is the deadline for the tax exemption policy for micro electric vehicles below 200 kilometers at the end of May, so the quality of retail growth in August this year is higher.

The secretary-general of the China Passenger Car Association, Cui Dongshu, released an analysis of the trends in the automotive segment market and the performance of manufacturers in August, pointing out that with the gradual effectiveness of the national "trade-in" policy, the corresponding policy measures and follow-up in various regions, the stimulation of consumption control in Beijing, coupled with the temporary cooling of the price war among new car market, and the boost of the "618" promotion for the second half of the year, the consumption enthusiasm of the previous market observers has been ignited, and the national passenger car market has maintained a relatively good development stage in August. Due to the increase brought by the non-RDE vehicle treatment in August last year, and this year is the deadline for the tax exemption policy for micro electric vehicles below 200 kilometers at the end of May, so the quality of retail growth in August this year is higher.

1. The auto passenger and commercial markets had a good start in 2024.

In recent years, the differentiation of the passenger and commercial markets has become apparent. This year, the market has been relatively good in terms of passenger vehicle growth from January to August, influenced by policies and the Spring Festival. The commercial vehicle market recovered after the Spring Festival and the trend from January to August remained relatively stable.

In recent years, the differentiation of the passenger and commercial markets has become apparent. This year, the market has been relatively good in terms of passenger vehicle growth from January to August, influenced by policies and the Spring Festival. The commercial vehicle market recovered after the Spring Festival and the trend from January to August remained relatively stable.

2. The auto market had a good start in 2024.

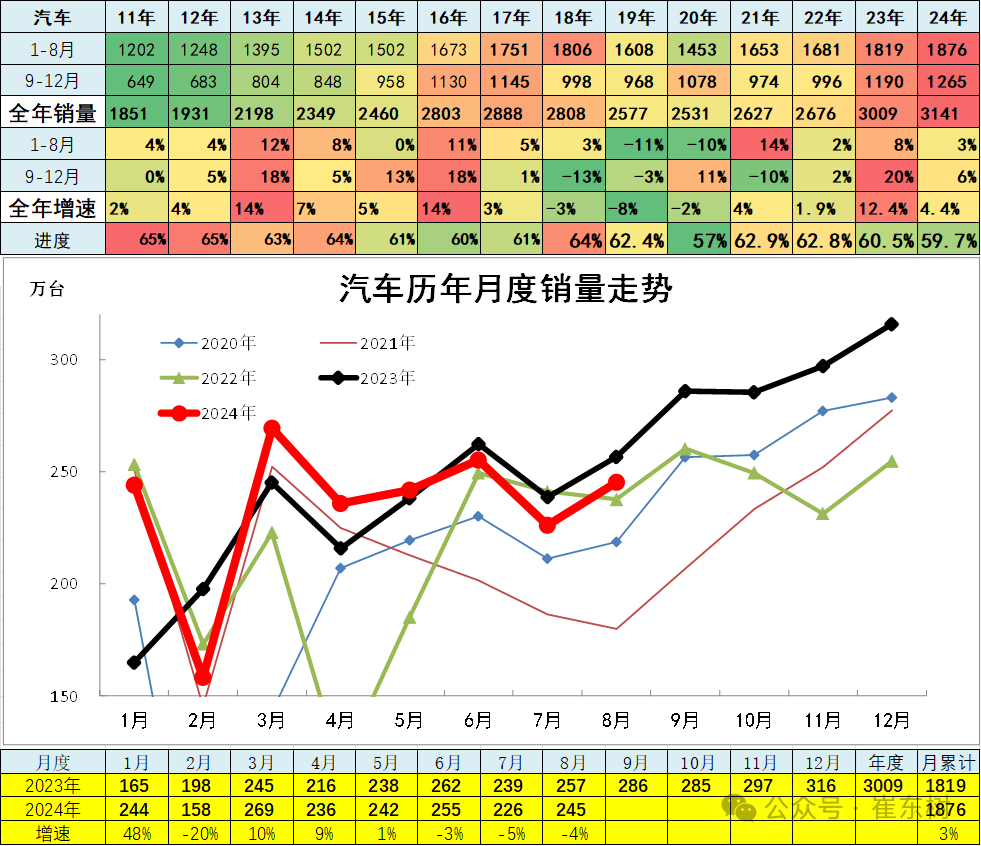

From January to August 2024, the cumulative total sales of automobiles were 18.76 million units, with a cumulative growth rate of 2.8%; in August, the total sales of automobiles were 2.45 million units, a year-on-year decrease of 4%, and a month-on-month increase of 8.7%.

In 2023, the automotive market started with low performance but gradually improved towards the end of the year. The sales volume in February this year showed a significant decline, followed by a significant recovery in August. The market, which was previously sluggish due to price wars, has gradually recovered.

By 2019, total cumulative auto sales were 25.7687 million units, down 8.1%; in 2020, total cumulative auto sales were 25.31 million units, down 1.9%; in 2021, total cumulative auto sales were 26.27 million units, up 3.8%, finally achieving positive growth, higher than the performance in 2019; in 2022, total cumulative auto sales were 26.7557 million units, up 1.9%; in 2023, total cumulative auto sales were 30.09 million units, up 12.4%.

3. There is a significant difference in the performance of major automotive groups.

Compared to the chart for 2021, there was a major differentiation in industry growth in 2022 with some automakers showing strong performance. The outbreak of the epidemic at the beginning of 2022 put pressure on traditional automakers, especially with the added impact of new energy, and state-owned conglomerates showed divergent performance. Geely Auto showed excellent performance, with both its commercial and passenger vehicle segments performing well. There was pressure among companies in the northern region such as FAW, Great Wall and BAIC.

In early 2023, new energy vehicles are pushing the market trend to differentiate. The three central state-owned enterprises have diverged overall, with some state-owned enterprises falling behind. New energy companies such as BYD performed well; Chery and Tesla showed relatively strong performance this year. Second-tier automakers showed differentiation, with serious differentiation and depression among smaller independent brands due to the conversion of old and new energy and continued losses in new energy vehicles.

The lineup of automotive groups in 2024 changed comprehensively, with BYD reducing prices and increasing output. Due to good sales pace and overseas changes in passenger vehicles, FAW, Changan, and Dongfeng performed well, while SAIC remained in sharp decline. New energy vehicles BYD and Tesla experienced differentiation in terms of growth rate.

In August, the auto market showed relative differentiation, with strong consumer demand for new energy vehicles. The market saw structural growth due to scrappage renewal policies, leading to diverging trends among various companies. In August, some major manufacturers experienced a significant rebound compared to the previous month, with BYD showing a strong performance compared to July.

4. Narrow passenger vehicle enterprise production and sales trends

In 2023, the total sales of narrow passenger vehicles reached 25.5323 million units, with a cumulative growth rate of 10.4% for the entire year. In recent years, the technological innovation of new energy vehicles and their competitive strength has continued to grow, while the launch of new models of rbob gasoline vehicles has been weak. The price war in the auto market started early this year, with significant price cuts for certain popular new energy vehicle models, reaching nearly 20%. The extended time from the Chinese New Year in February to the end of April has resulted in a large number of models participating in price reductions, approaching the total number of models that saw price reductions throughout the previous year. This has temporarily led to extreme caution among spring consumers regarding prices, coupled with weak consumption expectations, both of which have temporarily suppressed the launch of the spring auto market. Against the backdrop of differing taxes and rights for electric and gasoline vehicles, the trend of high growth in new energy vehicles and negative growth in rbob gasoline vehicles is becoming increasingly evident.

The extended time span from February, extending until the end of April, has led to a large number of models participating in price reductions, approaching the total number of models that saw price reductions throughout the previous year. As a result, spring consumers have temporarily shown extreme caution regarding prices, and weak consumption expectations have temporarily suppressed the launch of the spring auto market. Against the backdrop of differing taxes and rights for electric and gasoline vehicles, the trend of high growth in new energy vehicles and negative growth in rbob gasoline vehicles is becoming increasingly evident.

With the implementation rules of the national policy of replacing old with new, and the continuous implementation of local new energy subsidy policies, the consumer purchasing power of social savings has been released in May-August, driving the new energy vehicle market to strengthen in the second half of the year, with the new energy vehicles performing better than the expectations of passenger vehicle manufacturers.

From January to August 2024, the cumulative narrow passenger vehicle sales totaled 15.86 million units, with a cumulative growth rate of 3.1%; in August, the cumulative sales of narrow passenger vehicles were 2.1488 million units, a year-on-year decrease of 3.9%, an increase of 9.5% from the previous month.

In August, mainstream vehicle enterprises showed overall strength, with independent brands performing exceptionally well, and joint venture enterprises showing slow improvement. BYD took the lead, Chery maintained the second position in August, and Geely Auto retained the third position. The joint venture FAW-Volkswagen performed relatively strongly.

The main manufacturers of passenger vehicles are quickly dividing, and manufacturers of new energy vehicles have shown strong performance, with particularly obvious differentiation in independent brands.

In the whole of 2023, manufacturers' cumulative retail sales of narrow passenger vehicles totaled 21.7 million units, with a cumulative growth rate of 6%; from January to August 2024, the cumulative sales of narrow passenger vehicles totaled 13.46 million units, a year-on-year increase of 2%, with 1.9 million units sold in August, a year-on-year decrease of 1%.

Trends in production and sales of new energy passenger vehicle enterprises.

In 2022, the sales volume of new energy passenger cars was 6.5 million units, a year-on-year increase of 96%. In 2023, the new energy passenger car market is expected to reach 8.87 million units, showing a steady growth trend.

The sales volume from January to August 2024 increased by 30% to 6.61 million, showing a good trend, driven by scrappage subsidies, manufacturer price reductions, and new vehicle introductions.

6. Trend of production and sales of traditional fuel-powered passenger vehicles

In 2023, the sales volume of traditional narrow-definition fuel-powered passenger vehicles was 16.66 million units, basically flat compared to the same period in 2022; from January to August 2024, the sales volume of traditional narrow-definition passenger vehicles was 9.24 million units, a 10% year-on-year decrease compared to the same period last year, with a 24% decrease in August, marking the largest decline this year.

The continuous decline of conventional passenger cars in the early stage has brought great market pressure. Recently, the trend of traditional cars has rebounded relatively. However, the impact of the dramatic price reduction of new energy will continue to be reflected. It is hoped that traditional cars can also stabilize and recover growth.

The situation of conventional power passenger vehicles dominated by joint venture auto companies is gradually changing, and Chery, Geely, and the three major joint ventures still have relatively strong market positions. FAW-Volkswagen is the absolute leader among joint ventures, while the advantage of domestic brands in fuel vehicles is not obvious compared to joint ventures, and the fuel vehicle technology of joint venture auto companies is still strong.

7. Classification trend of production and sales of commercial vehicle enterprises.

The overall trend of the commercial vehicle market is low, with a year-on-year decrease of 30% in 2022, showing a rare super-low growth rate characteristic in recent years.

In 2023, the total annual sales volume of manufacturers was 4.2977 million units, with a cumulative growth rate of 18.6%; from January to August 2024, the cumulative sales volume of commercial vehicles was 2.7662 million units, with a cumulative growth rate of 1.3%; in August, the sales volume of commercial vehicles was 0.2927 million units, a year-on-year decrease of 11%, and an increase of 3% month-on-month. In 2024, the main reason for the performance in January was the strong base effect, followed by the stable performance in the second quarter under high base effect, and the weak growth of commercial vehicles in July and August.

The main manufacturers of commercial vehicles are SAIC-GM-Wuling, Beiqi Foton, Dongfeng Motor, Changan Automobile, and China National Heavy Duty Truck Group, among which Changan, FAW, and Wuling Motors are relatively strong, and Jiangling has a relatively stable performance. The heavy truck segment performs very well with China FAW and Sinotruk, while some second-tier companies are still under pressure.

8. Classification trend of production and sales of microcar enterprises.

The total sales volume of mini vehicles accumulated by the manufacturer in 2023 is 0.8824 million units, with a cumulative growth rate of 6.3%; From January to August 2024, the cumulative sales volume of mini vehicles is 0.4934 million units, with a cumulative decline of 6.1%; The sales volume of mini vehicles in August is 0.047 million units, a year-on-year decrease of 30%, and a month-on-month growth of 3.3%.

In 2023, Wuling's performance was relatively strong, especially from August to December. After that, there was a sharp adjustment at the beginning of 2024, and it rebounded from March to May. In August 2024, most manufacturers' sales volume increased month-on-month, except for SAIC-GM-Wuling, which had a weaker trend compared to July.

9. Trend of sales and production classification of light-duty truck enterprises

The total sales volume of trucks accumulated by the manufacturer in 2023 is 2.9273 million units, with a cumulative growth rate of 22.8%.

From January to August 2024, the cumulative sales volume of trucks is 1.9527 million units, with a cumulative growth rate of 2.4%; The sales volume of trucks in August is 0.2052 million units, a year-on-year decrease of 7.4%, and a month-on-month growth of 1.4%.

From January to August 2024, the cumulative light truck sales reached 1.2371 million units, with a cumulative growth rate of 1.9%; the sales of light trucks in August were 0.133 million units, a year-on-year decrease of 7.1%, and a month-on-month decrease of 0.3%.

The previous high growth in truck sales was mainly due to the impact of the phasing out of National III diesel vehicles, with powerful measures taken across the country to eliminate National III vehicles and bring about a huge increase in replacement purchases. With the new round of trade-in promotions, there is still potential for market growth.

The major light truck manufacturers in 2024 show a significant differentiation, with Xinyuan Auto experiencing a substantial year-on-year increase in August compared to last year.

Changan Automobile and Xin Yuan Auto have upgraded from strong micro truck companies to strong light truck companies.

10. Trends in the production and sales classifications of medium and heavy-duty truck enterprises

The cumulative sales of medium-duty and heavy-duty trucks in 2019 were 1.3136 million units, a cumulative decrease of 0.9%; the cumulative sales of medium-duty and heavy-duty trucks in 2020 were 1.778 million units, a cumulative growth rate of 35%; the cumulative sales of medium-duty and heavy-duty trucks in 2021 were 1.572 million units, a cumulative decrease of 12%; the sales volume of medium-duty and heavy-duty trucks in 2022 was 0.7675 million units, a cumulative decrease of 51%; the cumulative sales of medium and heavy-duty trucks by manufacturers in 2023 reached 1.0181 million units, with a cumulative growth rate of 32.7%.

From January to August 2024, the cumulative sales of medium and heavy trucks reached 0.7156 million units, with a cumulative growth rate of 3.1%; in August, the sales of medium and heavy trucks reached 0.0722 million units, a year-on-year decrease of 8.1%, and a month-on-month increase of 4.7%.

The high growth of heavy-duty trucks in the early stage was mainly due to the growth of the demand for trucking driven by e-commerce logistics, as well as the rapid growth of financial loans. Under the influence of the epidemic, the consumption of residents has further strengthened the trend of electrification, and it has further stimulated logistics transportation. In addition, comprehensive factors such as the scrapping and renewal of National III and investment promotion have also played a role. Due to the high penetration of automotive finance, problems have gradually emerged, and there is great pressure on the consumption of the automobile market.

In 2024, the main trends of the block orders are diverging, and both Sinotruk and Shaanqi have strong export of heavy-duty trucks to Russia, while FAW and Dongfeng heavy-duty trucks are in a post-holiday adjustment period. This year, Sinotruk and Shaanqi have a strong start, and the block orders of the leading heavy-duty trucks, FAW and Dongfeng, still need to further strengthen product competition and market expansion. The gap between the second-line heavy-duty trucks and the main car companies is still huge.

11. Trends in sales of light commercial vehicles

In 2023, the total sales of passenger vehicles by manufacturers reached 0.4881 million units, with a cumulative growth rate of 19.6%.

From January to August 2024, the cumulative sales of passenger vehicles reached 0.3201 million units, with a cumulative growth rate of 7.5%; in August, the total sales of passenger vehicles reached 0.04 million units, a year-on-year increase of 7.2%, and a month-on-month increase of 11.9%.

From January to August 2024, the cumulative sales of light commercial vehicles reached 0.2525 million units, with a cumulative growth rate of 4.1%. In August, the sales of light commercial vehicles were 0.0309 million units, a year-on-year decrease of 0.3%, and a month-on-month increase of 8.4% compared to the previous month.

In August, Jiangling light commercial vehicles led the market, and other light commercial vehicle companies also performed well. The light commercial vehicle market has been continuously changing recently, and second-tier manufacturers are rising. Changan has been performing exceptionally well in the past two years, followed by SAIC Datong and Jiangling. SAIC Datong has shown strong export performance.

12. Sales trend of large and medium-sized bus companies

In 2023, the total sales volume of large and medium-sized buses reached 0.0917 million units, with a cumulative growth rate of 3.9%. From January to August 2024, the cumulative sales volume of large and medium-sized buses reached 0.0676 million units, with a cumulative growth rate of 22.2%. In August, the sales volume of large and medium-sized buses reached 0.0092 million units, a year-on-year increase of 7%, and a month-on-month increase of 25.5% compared to the previous month.

In the first two years, large and medium-sized buses performed well, with high year-on-year growth rates due to the subsidy market for new energy buses and the promotion by local governments. In the past two years, with the retreat of subsidies, the decline of large and medium-sized buses was significant. However, as local governments currently lack funds, the performance of bus models in 2024 remains generally weak, even though there is growth.

In 2024, the large and medium-sized bus market remains chaotic, mainly based on new energy buses. With the withdrawal of policies, the bus market is showing more signs of overcapacity, and the large and medium-sized bus market will continue to remain low and volatile.