Invesco Asia Pacific market strategist Zhao Yaoting said that in this round of interest rate cuts, he leans towards a defensive stance and over-allocates to fixed income rather than stocks.

Zhao Yaoting, Invesco Asia Pacific market strategist, said that in this round of interest rate cuts, he leans towards a defensive stance and over-allocates to fixed income rather than stocks. He stated that through observing previous interest rate cut cycles, he is researching other assets that may perform well during the Fed's interest rate cut cycle. In terms of stocks, value and defensive assets, such as medical care and consumer essentials, may perform well, similar to previous interest rate cut cycles. He believes that the bear market for technology stocks may continue until further evidence proves the productivity gains brought by artificial intelligence.

Recent economic data from the USA and China indicates that both economies are heading towards weakness - therefore, a defensive approach should be taken, and cyclical assets should be reduced. Despite the weak growth of the world's largest economy, which may offset the benefits of loose policies, it seems that emerging markets and international assets tend to benefit from the Fed's interest rate cut cycle. In other words, in terms of stocks, Zhao Yaoting believes that, similar to previous interest rate cut cycles, value stocks and defensive stocks such as healthcare and consumer essentials are likely to perform well.

The bear market in technology is likely to continue until there is further clear evidence that artificial intelligence can improve productivity.

Recent economic data from the USA and China indicates that both economies are moving towards a more weakened state - it is reasonable to increase defensiveness and underweight cyclical stocks. Emerging markets and international assets often benefit from the Fed's interest rate cut cycle, however, the weak growth of the world's largest economy may offset the benefits of loose policies.

The Fed's struggle against persistent inflation is coming to an end, but authorities are facing a new challenge to prevent the economy from entering a recession. The recent July JOLTS (job openings and labor turnover survey) employment data, August ADP employment population, and monthly non-farm employment population from the U.S. Bureau of Labor Statistics were lower than expected, which is thought-provoking. After 3 years of strong performance, the labor market has shown signs of recession, as has the U.S. stock market, with the S&P 500 index falling by over 4% last week, and the yield on the U.S. 10-year Treasury bonds falling by 19 basis points to 3.72%, reaching the lowest level since June 2023.

Recent market volatility reflects investors' concerns about whether the Fed's first interest rate cut is too small to prevent an economic recession and whether it is too late. Although it is believed that the Fed will cut the benchmark interest rate next week, the deteriorating labor market data may give the Fed the opportunity to cut rates by more than 25 basis points next week. Nonetheless, he believes that the possibility of a rate cut by more than 25 basis points next week is slim, because a substantial rate cut at the current time and during the U.S. election period would lead market participants to accuse the Fed of attempting to influence the election results, and that the Fed should have cut rates earlier.

Zhao Yaoting believes that despite undergoing a period of aggressive tightening, the United States will be able to avoid an economic recession.

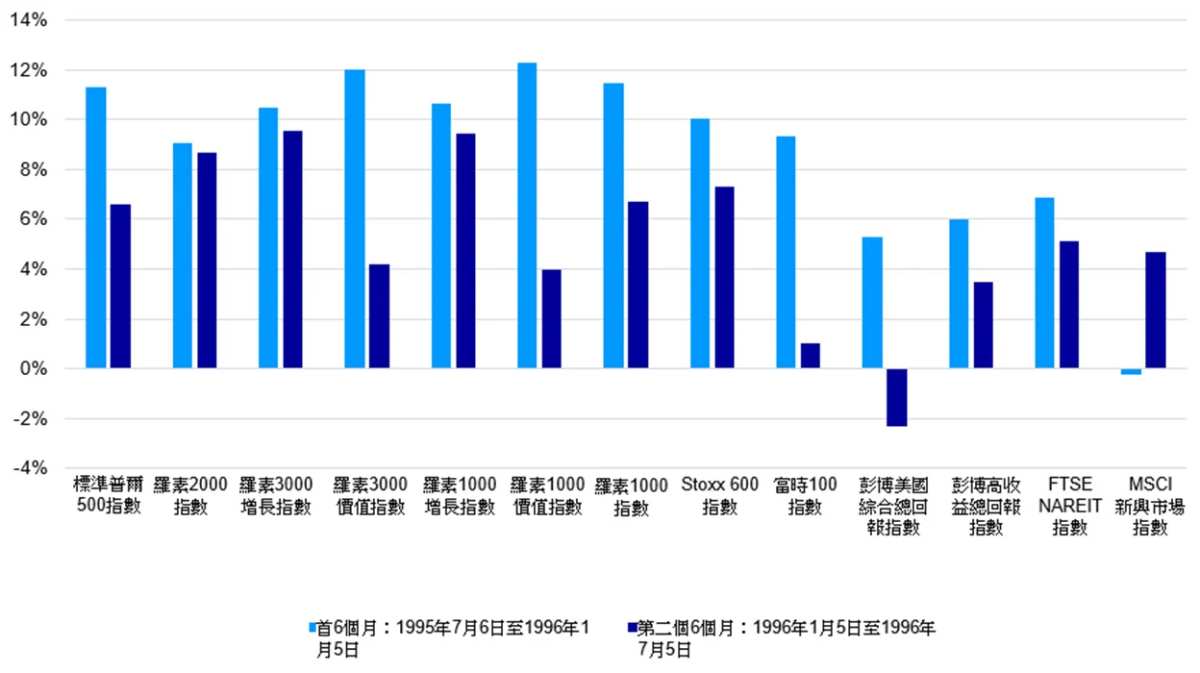

Refer to the interest rate reduction cycle from 1995 to 1996.

The last time the Federal Reserve was able to raise interest rates and avoid an economic recession was during the tightening cycle in 1995. Although history does not usually repeat itself, it often rhymes, so lessons can be learned by studying what happened in the market when the Fed reduced interest rates in 1996.

Six months after the Federal Reserve began cutting interest rates on July 6, 1995, the S&P 500 index rose 11.32% (chart). Value stocks outperformed growth stocks slightly. The healthcare industry performed the best. In the six months after the Fed started cutting interest rates, international stock markets performed slightly worse than the US stock market, while bonds recorded steady gains.

Overall, the returns during the subsequent six-month period were more moderate. This may be attributed to the fact that the easing cycle was very short-lived, with a small decrease in interest rates of only 75 basis points.

Asset class performance in the first and second six-month periods after the Federal Reserve began its accommodative policy from 1995 to 1996.

Source: Bloomberg, as of September 3, 2024.

Currently, the trading price of the US stock market is higher than its historical average valuation level, perhaps digesting the upcoming interest rate reduction cycle, so he believes that the stock market will not experience a sharp rise similar to the interest rate reduction cycle in 1996.

For stock investors, it is also wise to adopt a more defensive stock deployment. Similar to the 1995 cycle, in this round of loose cycle, defensive stocks such as healthcare and value stocks are expected to outperform growth stocks.

Although the strong profits made by the largest artificial intelligence chip manufacturer did not boost the market, the artificial intelligence frenzy seems to have stalled. The market is likely to take a wait-and-see attitude towards artificial intelligence, especially in terms of whether it can achieve productivity breakthroughs.

Although the Federal Reserve's policy rate cut helps alleviate market tension, it should boost local currencies and risk assets in emerging markets, the positive effects may be offset by soft economic growth in China and the US. Overall, while maintaining an optimistic view, it is expected that the US economy will slow down in the coming quarters. Despite the US economic slowdown, other major economies have not taken up the growth baton.

The upcoming interest rate reduction cycle in the US is likely to be interrupted due to anti-inflationary forces and weak growth. Continuous rate cuts, moderate energy prices, and a softening dollar should prevent the US economy from entering a recession. However, policy uncertainty may intensify, especially before the US presidential election, which could mean companies delaying capital expenditure and investment.

In this environment, he continues to believe that adopting a defensive deployment is a wise move.