In 2024, China's automotive market retail achieved the expected strong start, followed by a dramatic divergence between new energy vehicles and fuel vehicles. From January to August 2024, the retail sales of new energy vehicles reached 6.01 million units, showing a relatively strong trend with a 35% increase, close to the 36% growth rate in 2023.

According to the Securities Times app, Cui Dongshu, the secretary-general of the China Passenger Car Association, stated that in 2024, China's automotive market retail achieved the expected strong start, followed by a dramatic divergence between new energy vehicles and fuel vehicles. From January to August 2024, the retail sales of new energy vehicles reached 6.01 million units, showing a relatively strong trend with a 35% increase, close to the 36% growth rate in 2023. With the introduction of the national scrappage renewal policy and a doubling of subsidies in July, new energy vehicles accelerated high growth. In August, traditional vehicle retail sales decreased by 28% to 0.87 million units year-on-year, while new energy vehicle retail sales increased by 43% year-on-year, a difference of 71 percentage points. Fuel vehicles faced heavy tax burdens, subsidies encouraged the purchase of new energy vehicles, and fuel vehicle companies faced greater collapse pressure.

Rural residents are more sensitive to prices, and a considerable number of people tend to purchase pure electric vehicles priced below 0.07 million yuan. Currently, A00-level vehicles are not tax-exempt for distances under 200 kilometers, making them relatively disadvantaged compared to low-speed electric vehicles. Therefore, policy support for economically efficient electric vehicles is still needed for new energy vehicles to enter rural areas. The inadequate construction of charging infrastructure in county and township markets hinders promotion. Thus, promoting the coordinated development of photovoltaic energy storage electric vehicles is also a good way to promote the penetration of new energy vehicles in rural areas.

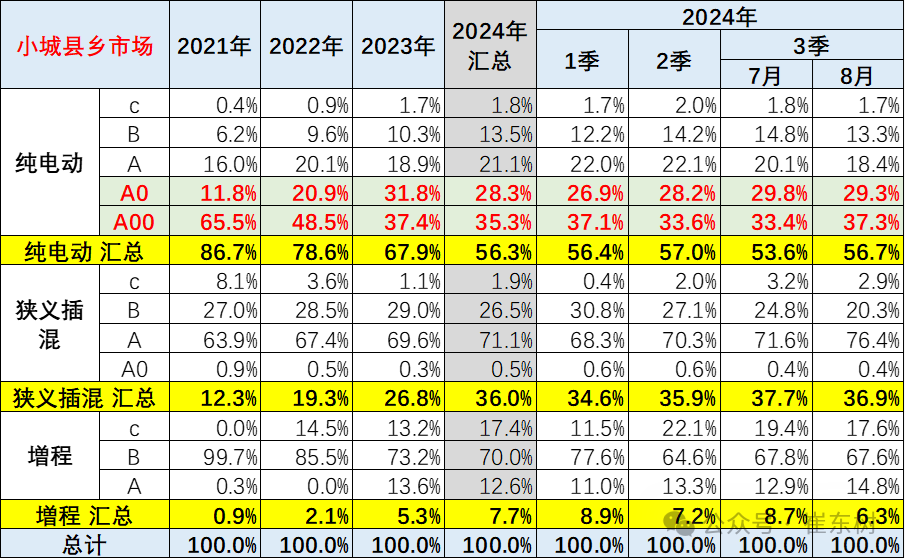

In small town and county markets, the sales structure of new energy vehicles has shifted from 87% being pure electric vehicles in 2021 to 56% being pure electric vehicles in 2024, gradually resembling the situation in large cities.

Promoting the sales of new energy vehicles in small town and county markets should focus on strengthening rather than suppressing. The sales structure of pure electric vehicles in small town and county markets has decreased significantly, from 66% for A00-level vehicles in 2020 to 35% in 2024. While the scrappage renewal policy has had some driving force for A00-level electric vehicles, the level of support is far from enough. Supporting new energy vehicles entering rural areas should involve lifting the purchase tax exemption for electric vehicles below 200 kilometers, which would benefit the practical lower spending power of the elderly in rural areas, rather than pushing them to buy low-speed electric vehicles.

1. Strong wholesale of new energy vehicles in August 2024

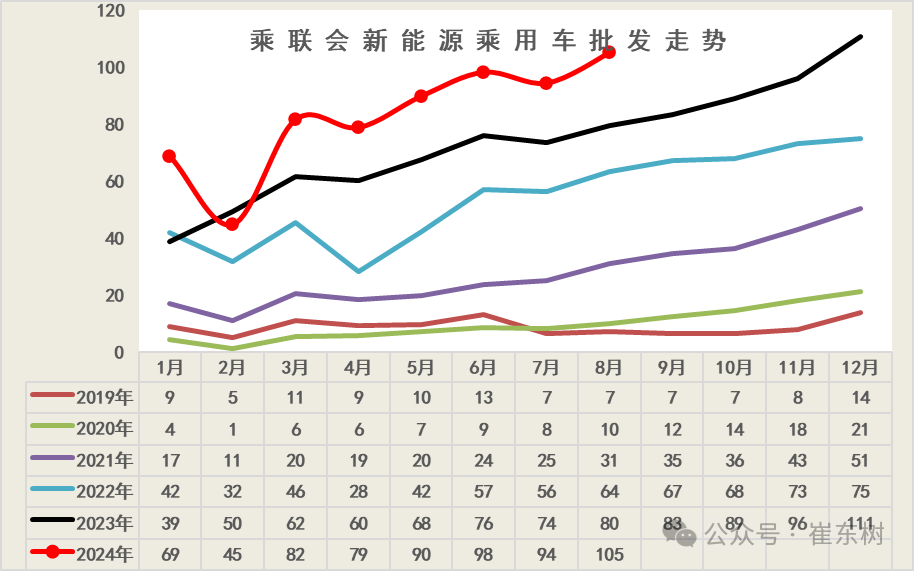

In August 2024, the wholesale sales of new energy passenger vehicles reached 1.05 million units, surpassing the historical highest level. Due to the impact of the Spring Festival and price reductions, there was a significant decline in February, but the market gradually recovered and grew from March to July, with a huge month-on-month growth in August.

Since 2023, the prices of power batteries such as lithium and nickel have been falling, so there is a downward trend in power battery prices. The low sales in February is beneficial for the company to reduce production at the beginning of the year, clear inventory, and achieve continuous growth in new product sales.

In August, the wholesale sales of new energy passenger vehicles reached 1.05 million units, with a year-on-year growth rebound of 32%, which performed well. This growth rate is significantly higher than the 30% growth rate in the period from January to July, showing strong growth overall from January to August. The wholesale growth in August is still relatively low compared to retail, reflecting the effect of market stimulation.

2. The national penetration rate of new energy vehicles - wholesale

In August, the wholesale penetration rate of new energy vehicle manufacturers was 48.9%, an increase of 13.3 percentage points compared to the 35.6% penetration rate in August 2023.

In August, the penetration rate of new energy vehicles in independent brands was 63%; the penetration rate of new energy vehicles in luxury cars was 43.2%; while the penetration rate of new energy vehicles in mainstream joint venture brands was only 7.8%.

In August, the wholesale volume of traditional automakers decreased by 24% year-on-year, while the retail volume of new energy vehicles increased by 32% year-on-year, with a growth difference of 56 percentage points, putting pressure on fuel vehicles.

3. In August 2024, the retail growth rate of new energy vehicles is strong.

In August 2024, the new energy vehicle market retail sales reached 1.03 million units, showing unusually strong performance in August compared to July, and overall maintaining a strong retail trend.

Due to the issuance of licenses in Beijing, the effect of releasing new demand from June to August is significant, and some price-waiting groups have started to purchase cars, which has increased the enthusiasm for purchases released by scrapping and updating.

By 2023, cumulative retail sales will reach 7.75 million units, a year-on-year increase of 36%. The strong performance in August, with a growth rate of 43%, showed a relatively strong trend of 6.01 million units in retail sales of new energy vehicles from January to August 2024, a 35% increase, close to the 36% growth rate in 2023, which is very impressive.

4. National new energy penetration rate - retail

In August, the domestic retail penetration rate of new energy vehicles was 54%, an increase of 16.7 percentage points from the 37.3% penetration rate in the same period last year.

In domestic retail sales in August, the penetration rate of new energy vehicles in independent brands was 75.9%; in luxury cars, it was 33.5%; while in mainstream joint venture brands, it was only 8%.

In August, traditional car retail sales decreased by 28% YoY to 0.87 million units, while new energy vehicle retail sales increased by 43% YoY, a difference of 71 percentage points. The heavy tax burden on fuel cars puts pressure on them.

The continuous breakthrough of the domestic passenger vehicle new energy penetration rate exceeding 50% is due to the following reasons: 1. The empowerment of the industrial chain advantages brought by the continuous strengthening of China's manufacturing industry, with strong advantages in battery, electric machine, chip, and other equipment manufacturing industries and parts industries; 2. Under the promotion of new production forces, Chinese automakers are fully developing new energy vehicles, driving the transformation of China's automobile industry from big to strong; 3. The guiding ideology of the open development of the passenger vehicle industry has promoted the comprehensive entry of internet companies, intelligent consumer manufacturing companies, international new energy vehicle companies, and activated industry competition and innovation capabilities; 4. The innovative development of Chinese automakers in plug-in hybrid technology, achieving breakthroughs in narrow-sense plug-in hybrid and extended-range technology, enriching the technical route of global new energy development, and achieving a breakthrough advantage of 78% market share in China's plug-in hybrid market; 5. In August, the government intensified its policy of scrappage and renewal of passenger vehicles, with subsidies for pure electric and plug-in hybrid vehicles being 0.005 million yuan higher than that for conventional fuel vehicles, further boosting the development of new energy vehicles; The above measures have pushed the penetration rate of new energy vehicles in the weak season of the car market in July and August to exceed 50% consecutively, helping to push the popularization of new energy vehicles to a new level. This phenomenon deserves attention.

5. Analysis of the new energy vehicle market in urban and rural areas.

According to the regulations that divide urban and rural areas (Guohang [2008] No. 60), "Based on China's administrative division, the residents' committees and village committees confirmed by the civil affairs department are the dividing objects on the basis of actual construction, and China's territory is divided into urban and rural areas. "Cities and towns include urban and town areas. Urban areas refer to residents' committees and other areas actually connected to the construction of the municipal districts and districts in municipalities, districts, and municipal government office locations. Town areas are those outside urban areas, including county government office locations and other towns, whose construction is actually connected to residents' committees and other areas. "Rural areas refer to areas outside the cities and towns specified in these provisions."

Since insurance data is national data managed by the China Banking and Insurance Regulatory Commission, its classification is not as detailed as that of the National Bureau of Statistics. Therefore, we cannot see the corresponding distribution of urban and rural areas from the insurance data of the China Banking and Insurance Regulatory Commission. We can only use the classification of this prefecture-level city as the basis for analysis and make approximate reference analysis.

According to the differences between the China Banking and Insurance Regulatory Commission and the National Bureau of Statistics, insurance data is the official data of the CBIRC. From this data, we can see that the analysis is based on the proportion differences of large cities, medium-sized cities, small cities, and county markets. Therefore, we collectively refer to the county and small city market as the small county and city market.

In the analysis of the small county and city market, the sales volume of new energy pure electric vehicles is constantly increasing. In 2020, the sales volume of new energy vehicles in the small county and city market accounted for 0.5%. By 2024, the proportion of new energy vehicles in the small county and city market will reach 5.3% of the national passenger vehicle sales volume, showing a continuous upward trend.

The improvement of the small county and city market is mainly due to the growth of plug-in hybrid electric vehicles and pure electric vehicles. The small county and city market has also shown strong growth due to the adoption of plug-in hybrid and pure electric vehicle models as substitutes for fuel vehicles.

From the distribution of new energy sales in small towns and counties markets, the growth rate of pure electric vehicles in Northeast, North China, Northwest, and Central regions is relatively fast. Recently, the performance in the Northwest and Northeast is good, and the performance in North China is relatively strong. The overall performance in South China and East China, on the other hand, is relatively average.

Looking at the vehicle structure, the sales volume of A00-level pure electric vehicles in small towns and counties markets in August has increased significantly. A00-level vehicles have continued to grow substantially in various regions, with a month-on-month increase of more than 50% in the Northeast, North China, and Northwest regions.

The pressure on small and micro electric vehicles in the early stages has increased due to the cancellation of vehicle purchase tax incentives. Currently, micro electric vehicles are facing relatively high pressure in competition with low-speed electric vehicles. On the other hand, the proportion of A0-level mid-to-high-priced electric vehicles has also grown in small cities. Therefore, in the small towns and counties markets, the demand for A00-level electric vehicles that are suitable for farmers' needs has not been effectively released in the early stages, but there has been a significant growth in August.

The differences in vehicle models between large and medium-sized cities and small towns and counties markets in China are extremely significant. In major cities, Tesla's MODEL 3, MODEL Y, and Xiaomi's SU7 perform relatively well. In large cities, MODEL Y and MODEL 3 also perform relatively well. However, in small towns and counties markets, vehicles such as Haigu perform relatively well. At the same time, there is a strong demand for economic electric vehicles such as Wuling Hongguang Mini, Wuling Hongguang Bingguo, Changan Lumin, BYD Yuan, Panda Mini, and Yuanup. Therefore, it can be seen that in the small towns and counties markets, the first eight vehicle models are mainly dominated by economic electric vehicles.

In the plug-in hybrid market, the top models are mainly BYD Qin L, Li Xiang L6, and others with relatively strong performance. When it comes to the rural market, the performance of BYD Qin, Qin L, and Song, which are generally low-priced models, is relatively good. In the rural market, there is generally weaker demand for mid-to-large-sized cars, but Qin, Qin L, and Song have gained relatively strong market competitiveness at low prices, resulting in stronger demand growth in the rural market.

6. Characteristics of new energy passenger vehicle usage

The proportion of rental and leasing of new energy passenger vehicles gradually increased from 2018 to 2019, but then began to decline in 2020. In 2024, the proportion of rental and leasing was 7.9%, with a rental proportion of 6.2% in August, driven by stronger private consumption.

Recently, the market share of plug-in hybrids in the private market has continued to increase, while the demand for rental and leasing of plug-in hybrids has continued to shrink, with pure electric vehicles remaining the best choice for rental. The proportion of pure electric vehicle rentals significantly rebounded in August compared to before the Spring Festival.

7. The performance of the regional market is gradually improving

In the past few years, the main demand for new energy passenger vehicles has been strong in heavily restricted cities, but it has been declining recently. Excluding the restrictions in heavily restricted cities, the proportion of pure electric new energy passenger vehicles in total sales volume in August 2024 has dropped to 17.4%. This also indicates that the growth rate of the new energy vehicle market in heavily restricted cities is gradually slowing down, and the overall vehicle and population size have constraints on demand. Due to the large population base and poor public transportation, there is a strong demand for the mid-sized city market in recent months, and the new energy market in county and rural areas is gradually starting up.

8. The performance of the new energy market in urban areas is gradually improving.

The main reason for the decline in new energy vehicle sales in August is cities like Xi'an with high previous sales volume, which has a relatively small overall impact. The main driver of month-on-month growth in August is cities like Shanghai, Zhengzhou, Chongqing, and Suzhou, while markets like Changchun and Zhuhai have declined.

Compared to the same period in 2023, the new energy market in 2024 is still growing rapidly, with Beijing, Xi'an, Hangzhou, Chengdu, and other cities experiencing relatively rapid growth, forming the core driving forces for incremental growth.

9. There are regional differences in demand for pure electric vehicles.

The gradual start of the pure electric private household market is driving the industry's development. Although the demand in large cities with purchase restrictions has been strong in the past two years, its proportion has gradually decreased. The market share in large and medium-sized cities with driving restrictions has continued to rise, while the private consumption market in small cities and rural areas has shown slower recovery. The leasing market for pure electric vehicles has shown slight improvement, with rental leases accounting for the peak of pure electric vehicle sales volume in 2020. Subsequently, the proportion of rental leases declined in 2021, falling to around 15% from 2021 to 2023, and further dropping to 10% in August 2024, with a significant decline in the market share of medium-sized cities.

From the performance of the main vehicle models, it is also evident that the demand for main vehicle models is sluggish in large and medium-sized cities, with average performance in extra-large cities. Particularly, the increase in August is mainly driven by significant improvements in small cities and rural markets. The main vehicle models are still in an outward development trend, with a broader reach in the middle and small city markets in August compared to the same period, while the growth of the pure electric market in extra-large cities is relatively sluggish.

10. Regional demand for plug-in hybrid passenger vehicles

The incremental potential of plug-in hybrid vehicle models in the private consumption market is significant. Although there has been a reduction in Shanghai, there is good demand in middle and small city markets. Personal plug-in hybrid demand in rural and township markets is growing rapidly, with strong month-on-month performance in August. The proportion of unit and rental plug-in hybrid vehicles has continued to decrease. The main demand for plug-in hybrid rental models is in extra-large and large city markets, with a significant decline in rental of plug-in hybrids in extra-large cities this year.

In August, plug-in hybrids showed strength, with large and medium-sized non-restricted cities still being the main force, while the demand proportion in restricted cities decreased. Plug-in hybrids have formed good momentum in rural areas and rural markets.

In recent years, the proportion of plug-in hybrid vehicles in non-restricted cities has gradually increased, with BYD and Geely relatively strong. The Qin and Dolphin performed very well in the county and township markets in August, surpassing some of the old star models.

BYD Qin and Song and other low-priced plug-in hybrids perform well in small and medium-sized cities.

11. Increased demand for passenger vehicles in the region

The main users of extended-range passenger vehicles are individual and corporate owners, with the latter accounting for a much higher proportion than plug-in hybrid users, reflecting that extended-range models are more suitable for corporate owners than plug-in hybrids.

The main market for extended-range vehicles is still large and medium-sized cities, but with the growth of Wanjie and Deep Blue, small cities and county markets are gradually rising.

12. Regional penetration rate of pure electric passenger vehicles- August

Currently, the proportion of pure electric vehicles in restricted cities has remained stable, rising from 20% in August 2021 to 37% in 2024.

In non-restricted cities, the sales proportion of large, medium, and small cities for pure electric vehicles is basically the same. In August this year, the proportion in medium-sized cities increased to 29%, and the penetration rate in county and rural markets rose to 25%.

The penetration rate of plug-in hybrids continues to increase in markets across the country, especially in mega-cities. In August this year, the market share of plug-in hybrids reached 23% in mega-cities. In smaller cities, the market share of plug-in hybrids also continues to rise, and the gap in penetration rate among different cities has relatively narrowed.

Due to the promotion of the plug-in hybrid license policy, Shanghai saw an increase in the plug-in hybrid market share to 11% in August, up 7%.

13. There is significant differentiation among regional markets.

The performance of the rental markets in various regions varies greatly. The strong performers in the rental market in August this year are Guangdong, Jiangsu, Zhejiang, and Sichuan. The performance of various manufacturers in the rental markets in different regions also varies greatly, and the market share of some local products in local rental markets may not be very high.

The private market has been strong recently in Zhejiang, Shandong, Jiangsu, and Henan. The characteristics of the private pure electric vehicle market are relatively distinct, with a very clear trend towards high-end. BYD has performed well, and developed regions such as Jiangsu and Guangdong are mostly in the first place. Wuling has performed very well in Shandong, Henan, and Hebei.

Both Nio Inc and Xiaomi's performance in the new energy fund market have been very good, while traditional passenger vehicle manufacturers have also performed outstandingly in the private electric vehicle market.

BYD and Li Auto Inc have shown strong performance in the private plug-in hybrid vehicle market, especially in the leading main cities for BYD (01211) and Li Auto (02015) ranking second overall, with Chongqing Changan Automobile (000625.SZ) in third place. Chongqing Sokon Industry Group Stock, Geely, and Great Wall Motors also have relatively strong trends.

As the private plug-in hybrid vehicle market, other than BYD, is mainly plug-in hybrid electric vehicles, the performance of private plug-in hybrids of joint-venture car companies is relatively weak. Therefore, the gradual breakthrough of Great Wall Motors and Geely in plug-in hybrids is very significant.

14. The market trend in Beijing

The market trend of new energy vehicles in Beijing in 2024 is relatively stable. The sales volume in August 2024 reached 0.03 million units, which is at a high level compared to the same period in previous years, and the license plate indicators have been fully absorbed.

Since the relatively tight new energy vehicle indicators in 2018, the Beijing new energy vehicle market has shown a contrasting trend with the national trend in 2022. The current growth rate is relatively low, and some users who purchased cars in 2018 should consider replacing them. However, the overall market volume is still not high, which is a result of the impact of the pace of indicator issuance suppressing consumption.

The sales volume of new energy vehicles in Beijing in the second half of last year was good, considering the lack of indicators and the limited supply of Tesla vehicles. The performance in August in Beijing was also relatively strong. The overall level of new energy vehicles in Beijing is practical, which also reflects the good demand for household use.

15. Shanghai new energy market trend

The trend of new policy in the Shanghai market is significantly different from that of the Beijing market, and the trend from 2019 to 2021 is extremely stable. Starting from December 2022, there was a rush to buy at the end of the year, resulting in a low start to the year, and a significant drop in sales volume at the beginning of 2024.

In August 2024, the sales volume of new energy vehicles in Shanghai reached 0.029 million units, a decrease of 5% compared to August last year's 0.031 million units. The impact of policy adjustments on Shanghai's new energy vehicles last year is gradually recovering, and the impact of the rush to buy due to the tightening of license plate policies has a greater impact on the early Shanghai auto market.

16. The market trends of new energy passenger vehicles in cities with vehicle restrictions.

New energy vehicles performed relatively well in cities with vehicle restrictions, reaching a level of 0.244 million units in August 2024, with a year-on-year growth rate of 44%.

The cumulative sales of new energy vehicles reached a level of 1.5 million units in 2024, reflecting the continuous growth in demand for new energy vehicles in cities with vehicle restrictions.

17. The market trends of new energy passenger vehicles in areas without purchase or driving restrictions.

Non-restricted cities, which refer to areas where conventional vehicles are not subject to purchase or driving restrictions. Due to the lack of restrictions for traditional vehicles, the demand for new energy vehicles in these cities is a true market demand. Currently, non-restricted cities are also experiencing rapid growth, and these cities are relatively widespread across the country. The sales of new energy vehicles in these areas are also at a relatively high level.

In 2022, the cumulative sales of new energy vehicles in non-restricted cities reached a level of 2.73 million units, with a year-on-year growth rate of 96%, showing a strong growth characteristic. In 2023, new energy vehicle sales in non-restricted cities performed extremely well, reaching 4.06 million units. From January to August 2024, sales reached 3.44 million units, with a growth rate of 50%, indicating a strong performance.