Source: China International Capital Corporation Author: Liu Gang Zhang Weihan, etc.

Summary

Last week, China and overseas markets showed divergent trends. Influenced by factors such as the expectation of a rate cut by the Federal Reserve, the U.S. stocks rebounded significantly, while conversely, A-shares weakened due to relatively weak domestic economic data and policy expectations. Against this background, the Hong Kong stock market exhibited independent and distinct volatility from A-shares and overseas markets, reflecting its characteristic of 'Chinese assets + foreign capital', aligning with our consistent view that Hong Kong stocks are better than A-shares.

The upcoming Federal Open Market Committee (FOMC) meeting this week is undoubtedly a focus for global investors. For the Chinese market including Hong Kong stocks, the main impact logic of observing the Fed rate cut is how the peripheral easing effect will be transmitted, that is, how domestic policies will respond in this environment. If domestic easing measures are stronger than the Fed's, it will bring greater boost to the market. Conversely, if the magnitude is limited, which is more likely under current real constraints, then the impact of the Fed rate cut on the Chinese market may be marginal and partial. Recent August economic data show that domestic demand remains weak, still requiring more policy support including monetary easing. The Fed rate cut in September is expected to open up policy space for the central bank, but the magnitude may be limited, and expecting 'strong stimulus' is also unrealistic.

Due to sensitivity to external liquidity and the linked exchange rate arrangement, and following the rate cut, Hong Kong stocks have greater flexibility compared to A-shares. At the industry level, rate-sensitive growth stocks (biotechnology, technology hardware, etc.), sectors with high overseas USD financing ratios, local dividend payment in Hong Kong stocks, even real estate may benefit marginally. However, overall, until greater fiscal support is seen, the structural uptrend with wide-ranging volatility remains the main theme.

Main Content: How Does the Rate Cut Affect Hong Kong Stocks?

Market trend review

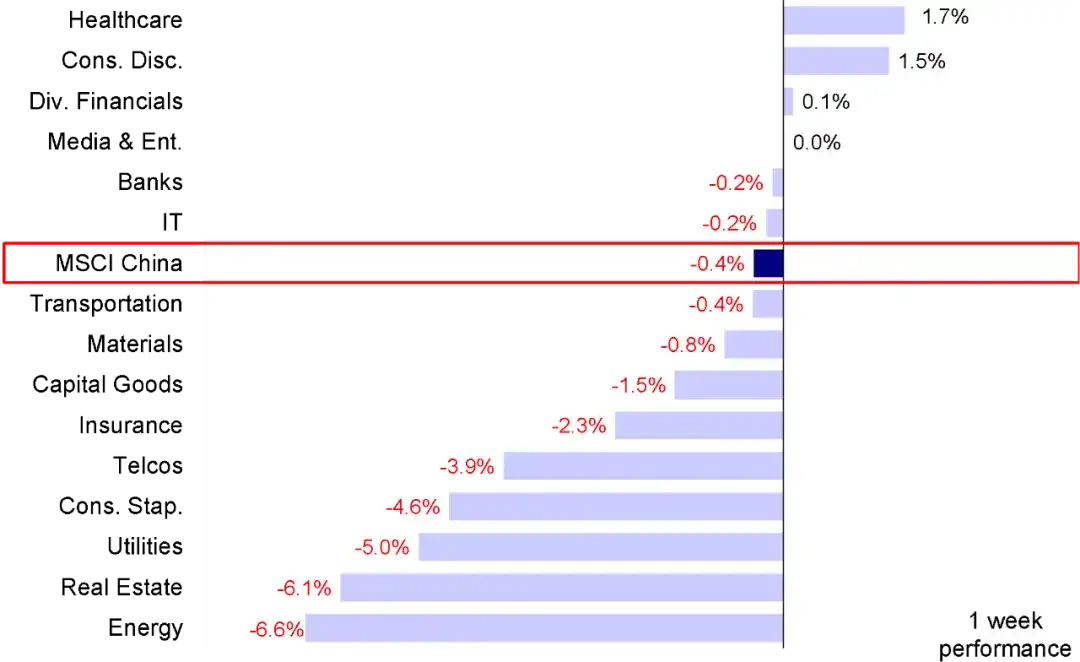

After experiencing a pullback the previous week, the Hong Kong stock market last week overall traded in a volatile range. Among the main indices, the Hang Seng Tech Index slightly declined by 0.2%, the Hang Seng Index fell by 0.4%, and MSCI China and the Hang Seng Enterprises both dropped by 0.4% and 0.6% respectively. In terms of sectors, boosted by the warming expectations of a Fed rate cut, growth sectors such as healthcare (+1.7%) and consumer discretionaries (+1.5%) led the gains, while conversely, energy (-6.6%), real estate (-6.1%), and utilities (-5.0%) performed poorly in the old economy sectors.

Chart: Last week, the MSCI China Index fell slightly, with healthcare and consumer discretionary leading the gains, while energy and real estate lagged behind.

Since the peak at the end of May, the Hong Kong stock market has fallen nearly 10%. Since mid-May, we have been reminding investors that this round of rebound is mainly driven by the funding side and emotions. Therefore, with the market entering the overbought range, investors' divergences and profit-taking are not surprising. Assuming that the risk premium is fully restored to the level of the high point at the beginning of 2023, the corresponding target index level of the first stage of the Hang Seng Index is 19,000-20,000 points (see May 12th "The market is approaching our first stage target" and May 26th "not surprisingly taking profits"). In the past few weeks, overseas funds, especially value-oriented active foreign funds, have flowed out again. The outflow scale this week has increased from USD 93.24 million last week to USD 340 million. This can also provide proof ("Active Foreign Funds Maintain Weakness"). However, with the recent continuous decline of the market, especially A shares falling below 3,000 points again, concerns about the Hong Kong stock market falling to the previous low are also increasing. In this regard, we are not so worried, although we have always believed that further upward momentum needs more catalysts to start, it will not completely give up all the gains, and the Hang Seng Index around 18,000 points can get some support, and looking back at this week's market performance also confirms our previous judgment ("temporary pause or end of rebound"). In addition, compared with A shares, which have returned all gains since March, the Hong Kong stock market has shown obvious resilience, which is consistent with our judgment that the Hong Kong stock market is better than A shares ("The Hong Kong stock market still has a comparative advantage").

Last week, the Chinese and overseas markets showed diverging trends. US stocks rebounded significantly, with the S&P 500 index rising 4% and the Nasdaq surging 6%, due to factors such as expectations of a rate cut by the Federal Reserve. In contrast, A-shares weakened due to relatively weak domestic economic data and policy expectations, with the Shanghai Composite Index falling 2.2% and nearing the 2,700-point level once again. Against this backdrop, the Hong Kong stocks exhibited a volatile trend that was independent of A-shares and differentiated from overseas markets, reflecting its characteristic of "Chinese assets + foreign capital," which is consistent with our view that Hong Kong stocks are better than A-shares.

This situation is particularly evident in sectors. For example, energy and real estate, which are more closely related to domestic fundamentals, lagged behind, while healthcare and consumer discretionary, which are sensitive to interest rates, led the gains. In addition, the market focused on Alibaba, which was formally included in the Hong Kong Stock Connect trading last week. With the favor of southbound investors (who bought 16.4 billion HKD last week), Alibaba's stock rose 3.7% overall. In the long term, based on the holdings ratio of comparable stocks such as Tencent under the current Hong Kong Stock Connect, the inclusion of Alibaba in the Hong Kong Stock Connect is expected to bring about an incremental capital of approximately 150 billion HKD.

The upcoming FOMC meeting of the Federal Reserve this week is undoubtedly the focus of global investors. Although the market has already reached a consensus that the Federal Reserve will start cutting interest rates in September, there is still uncertainty about whether the rate cut will be 25bp or 50bp. The current CME interest rate futures also indicate that the market's probability of expecting a rate cut of 25bp or 50bp is both 50%. The higher-than-expected core CPI released in the United States last week, especially the sharp increase in rent to a new high since January, also adds uncertainty to the magnitude of the rate cut. The fact that different assets such as the Nasdaq, industrial metals, and gold rose together also indicates that besides the clear direction of rate cut trade, there is still "confusion" about growth expectations. Considering that the United States is not in a deep recession and that easing measures have already begun to take effect in some sectors such as real estate, we believe that 25bp is still the benchmark.

For the Chinese market, including Hong Kong stocks, the most important impact of observing the Federal Reserve's rate cut is how the effect of peripheral easing is transmitted, that is, how domestic policies respond in this environment. Considering the constraints of the China-US interest rate differential and exchange rates, a rate cut by the Federal Reserve will provide more room and conditions for domestic easing, which is needed in the current relatively weak growth environment and still relatively high financing costs. Therefore, if the domestic easing is stronger than the Federal Reserve, it will bring greater boost to the market. On the other hand, if the easing is limited, which is also the more likely scenario under the current constraints, then the impact of the Federal Reserve's rate cut on the Chinese market may be marginal and partial.

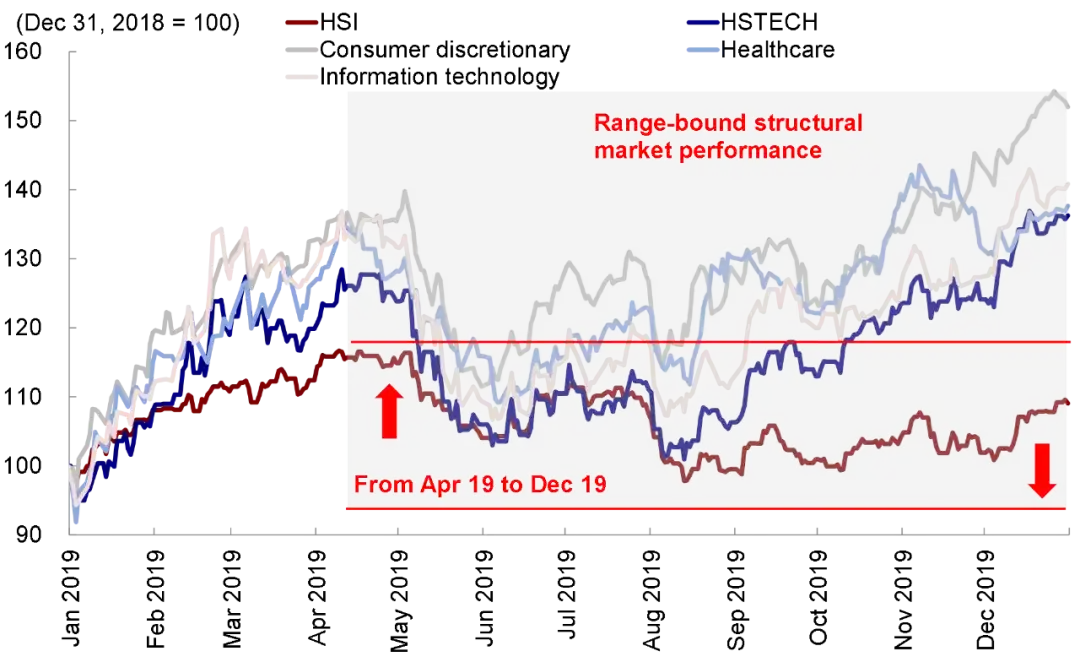

Taking the 2019 rate-cut cycle as an example, the significant rebound of A-shares and H-shares in early 2019 happened precisely when Powell announced a halt to rate hikes from January to March, rather than the formal rate cuts from July to September. The reason behind this is that when Powell announced the halt to rate hikes in early 2019, China also decided to cut the reserve requirement, causing a resonance internally and externally. In contrast, after April, the policy re-emphasized the "total door of monetary policy," which was contrary to the loosening of the Fed. Therefore, even though the Fed officially cut rates in July, A-shares and H-shares overall remained volatile.

Chart: In 2019, the domestic market rebounded significantly due to the loose domestic policy from January to March, but even after the Fed cut interest rates, the market still showed a structural market trend after April.

Chart: The current difference between China's actual interest rates and natural interest rates is significantly higher than that of the USA. If domestic monetary policy exerts greater force, it is expected to boost the market.

►Recently released economic data for August indicates that domestic demand remains weak and requires more policy support, including monetary easing. Apart from the better-than-expected exports in August, various aspects of growth such as prices, credit demand, and consumption investment have all weakened. Social retail sales in August increased by 2.1% year-on-year, a decrease of 0.6 percentage points from July; fixed-asset investment from January to August grew by 3.4% year-on-year, a slowdown from 3.6% from January to July; real estate land acquisition, sales, and investment all remained weak. At the same time, both household and business loan demand fell from the previous month, with long-term loans increasing by 40.2 billion yuan and 154.4 billion yuan year-on-year, respectively; the growth rate of social financing dropped from 8.2% in July to 8.1%, with a decrease of 98.1 billion yuan year-on-year, mainly contributed by government financing, while non-government financing decreased from 7.0% in July to 6.4%, and the household sector's decline was even faster, dropping from 3.8% in July to 3.5%. These all reflect the reality of weak private sector demand and still being in the process of "deleveraging." In addition, the growth rate of M1 decreased from -6.6% in July to -7.3%, also indicating a contraction in corporate operational activities. In this context, increasing leverage and expanding expenditure by the government will be an effective and important supplement. The growth rate of government financing increased from 15.4% in July to 15.8% in August, rising for the fourth consecutive month to the highest point since December 2023. If future spending can continue to expand (July's fiscal support increased by 295.7 billion yuan year-on-year, reaching a new high since December last year), it is expected to provide support for the market and growth.

Chart: The year-on-year growth rate of social financing in August weakened slightly to 8.1%, while the M2 growth rate remained unchanged from July.

Chart: The social financing of the resident sector weakened significantly, while the social financing of the government sector showed clear support.

Chart: From the perspective of the general fiscal deficit, the year-on-year rise in July reached a new high since December of last year.

However, in a recent press conference by the State Council Information Office, the head of the Monetary Policy Department of the People's Bank of China, Zou Lan, explicitly pointed out that the average statutory deposit reserve ratio of financial institutions still has some room for downward adjustment. However, due to factors such as 'deposit migration' and the narrowing of bank net interest margins, short-term interest rate cuts may still face constraints. Therefore, the September rate cut by the Federal Reserve may open up policy space for the central bank, but the extent may be limited, and it is unrealistic to expect 'strong stimulus'. China International Capital Corporation's macro group also believes that the possibility of a general reduction in Loan Prime Rate (LPR) is low.

However, considering how overseas easing is transmitted, the Hong Kong stock market has greater flexibility than the A-share market due to its sensitivity to external liquidity and the arrangement of the linked exchange rate system, which allows Hong Kong to follow interest rate cuts. In addition, Hong Kong stocks have relatively better profitability, and their valuations and positions have been cleared more thoroughly, which also supports the relatively strong performance of Hong Kong stocks. Similarly, at the industry level, growth stocks that are sensitive to interest rates (such as biotechnology, technology hardware, etc.), sectors with a higher proportion of USD financing, local dividends in Hong Kong, and export chains that benefit from the US interest rate cuts driving demand for real estate may also benefit marginally. Although it is not advisable to simply compare the average rules of historical experience, on average, Hong Kong stocks tend to rebound significantly and outperform A shares in the early stages of interest rate cuts, with a higher probability of rising.

Chart: Hong Kong stocks rebound significantly and outperform A shares in the early stages of interest rate cuts, with a higher probability of rising

In terms of investment strategy, as the Federal Reserve's interest rate cut approaches, we still believe that Hong Kong stocks have more flexibility than A shares. If the Federal Reserve's interest rate cut exceeds expectations, especially if the People's Bank of China's interest rate cut exceeds expectations, there will be even greater flexibility. At the industry level, growth sectors that benefit from numerator logic may have higher elasticity in the short term, such as semiconductors, autos (including new energy vehicles), media entertainment, software, and biotechnology. Local dividends and other benefits from Hong Kong's interest rate cuts are also worth noting. However, overall, until we see greater fiscal support, a structural market of wide-range volatility is still the main trend. In summary, the 10-year US Treasury yield has already priced in lower interest rate expectations at 3.6%. If the risk premium returns to mid-2019 levels, the corresponding Hang Seng Index would be around 18,500-19,000. If earnings grow by 10% on this basis, the corresponding Hang Seng Index level would be 21,000. We still maintain our allocation logic for the second half of the year, recommending three directions for structural market conditions: overall downward returns (stable returns from high dividends and high share buybacks, i.e., 'cash cows' with ample cash flow; short-term dividends may see differentiation in local dividends, low volatility dividends, and cyclical dividends), leverage in specific areas (industries with certain business cycles or benefiting from policy support, such as technology growth), and price increases in specific areas (natural monopoly sectors, public utilities, etc.).

Specifically, the main logic that supports our above views and the changes that need to be focused on this week are mainly as follows:

1) In August, China's CPI increased slightly year-on-year, but PPI slowed down significantly. In August, the year-on-year CPI increased from 0.5% to 0.6%, and the year-on-year PPI slowed down from -0.8% to -1.8%, both weaker than market expectations (0.7% and -1.4% respectively). The 0.1 percentage point improvement in year-on-year CPI was mainly driven by the increase in prices of fresh vegetables and fruits, which rose from 3.3% and -4.2% in July to 21.8% and 4.1% respectively, contributing 0.6 percentage points to the year-on-year CPI compared to the previous month. On the other hand, prices of non-food consumer goods and services generally slowed down, and core CPI fell to a new low since April 2021. In contrast, under the backdrop of a global demand slowdown, international commodity prices came under pressure, and domestic efforts to maintain stable growth still have a certain time lag. In August, the year-on-year decline in PPI widened from -0.8% in July to -1.8%.

Chart: In August, CPI increased slightly due to higher food prices, while PPI fell sharply.

2) The growth rate of social financing slightly declined, with a faster decline in non-government sectors. In August, the growth rate of social financing slightly declined from 8.2% in July to 8.1%, mainly relying on the support of government bond financing. The growth rate of government sector financing increased from 15.4% in July to 15.8%, with net financing of government bonds in August reaching 1.61 trillion yuan, an increase of 437.1 billion yuan compared to the same period last year. On the other hand, the growth rate of social financing in non-government sectors decreased from 6.6% in July to 6.4%, while the financing growth rate in the household sector declined even faster from 3.8% in July to 3.5%. The year-on-year decline in M1 broadened to 7.3% in August (vs. -6.6% in July), partly reflecting the need for improvement in corporate profitability.

3) Exports exceeded expectations in their recovery, while imports were lower than market expectations. In August, exports denominated in USD increased by 8.7% year-on-year (vs. +7.0% in July), exceeding expectations. Among them, there was a marginal improvement in exports to the EU and emerging markets, and in terms of specific products, there was a greater improvement in mechanical and electrical products such as mobile phones, automobiles, and ships. Although the global manufacturing PMI continued to contract in August, the better-than-expected export growth in August may be supported by factors such as the concentration of demand released in August after the disruption caused by a typhoon in July, and the anticipation of increased tariffs by the EU prompting companies to accelerate their exports ahead of time. On the other hand, imports in August increased by 0.5% year-on-year (vs. +7.2% in July), lower than market expectations, reflecting signs of weak domestic demand.

Chart: Exports exceeded expectations in their recovery, while imports showed a significant decline in August.

4) The growth rate of social retail sales has fallen, and the growth rate of fixed asset investment has slowed down. In August, the total social retail sales increased by 2.1% year-on-year, a decrease of 0.6 percentage points from July. The retail sales of automobiles decreased by 7.3% year-on-year, reaching a new low for the year. Overall, the policy of "replacing old with new" for consumer goods still needs further implementation. In terms of fixed asset investment, the increase in the decline of the PPI in August has increased the nominal investment growth rate. From January to August, fixed asset investment increased by 3.4% year-on-year (vs. 3.6% from January to July). Real estate development investment remains weak, with a decline on par with the first seven months. However, infrastructure and manufacturing investment still support the overall investment growth rate, but the marginal growth rates have decreased.

Chart: The growth rate of social retail sales in August has fallen, and the growth rate of fixed asset investment has slowed down.

5) This week, southbound funds continue to flow in, while overseas active funds continue to flow out. Specifically, data from EPFR shows that overseas active funds continue to flow out of overseas Chinese stock markets this week, with an outflow scale of approximately 0.25 billion US dollars, which has increased compared to the previous week's 0.21 billion US dollars, and it has been flowing out for 70 consecutive weeks. At the same time, overseas passive funds have turned into an outflow of 0.1 billion US dollars (compared to an inflow of 0.17 billion US dollars in the previous week). Southbound funds continue to flow in this week, with an inflow scale of 12.53 billion Hong Kong dollars, expanding compared to the previous week's 9.27 billion Hong Kong dollars. It is worth mentioning that Alibaba, which has attracted much attention from the market, was officially included in the Hong Kong Stock Connect trading last week and has been favored by southbound investors. Last week, a total of 16.42 billion Hong Kong dollars of southbound funds flowed into Alibaba, ranking first.

Chart: Overseas active funds continue to flow out of overseas Chinese stock markets

Editor/Lambor