穆迪分析公司首席经济学家马克·赞迪表示:“这对美国和全球经济来说都是一大利好。这在很大程度上让美联储不再拖累经济,让经济继续向前发展。这已经起到了帮助作用,股价高于其他情况下的水平。”

穆迪分析公司首席经济学家马克·赞迪表示:“这对美国和全球经济来说都是一大利好。这在很大程度上让美联储不再拖累经济,让经济继续向前发展。这已经起到了帮助作用,股价高于其他情况下的水平。”The Federal Reserve will begin a key shift this week, lowering interest rates for the first time in over four years in pursuit of a rare soft landing for the US economy.

Given that inflation seems to be under control and the US labor market is showing signs of weakness, it is widely expected that officials will lower the benchmark interest rate by at least 25 basis points at the end of the two-day meeting on Wednesday. In the financial markets, some traders—and economists at JPMorgan, the largest bank in the US—are even prepared to bet on a rate cut of half a percentage point.

This is a watershed moment that will begin to free the world's largest economy from the long-held constraints of high borrowing costs. The Fed's move could be accompanied by a signal that it is ready to provide more relief to US businesses and households in the coming months. And this combination is expected to continue driving the repricing of trillions of dollars' worth of global assets that has already begun.

Mark Zandi, Chief Economist at Moody's Analytics, said, "This is a big bullish for the US and global economies. It largely removes the drag on the economy that the Fed has been putting on, and allows the economy to continue to move forward. It has already been helpful to the extent that stock prices are higher than they otherwise would be."

Mark Zandi, Chief Economist at Moody's Analytics, said, "This is a big bullish for the US and global economies. It largely removes the drag on the economy that the Fed has been putting on, and allows the economy to continue to move forward. It has already been helpful to the extent that stock prices are higher than they otherwise would be."

However, policymakers and the future path of the US economy remain uncertain. Many investors and some economists worry that the Fed has waited too long, putting the labor market and economic growth in jeopardy and injecting volatility into financial markets. This was reflected in the US Treasury market on Friday, when traders suddenly resumed betting on a 50-basis point rate cut.

The November presidential election also put the Fed in an awkward position. Republican candidate and former president Donald Trump warned that the Fed should not cut interest rates on the eve of the vote, while Democratic Senator Elizabeth Warren pressured officials to reduce rates by 75 basis points.

Priya Misra, portfolio manager at JPMorgan Asset Management, said, "This is a critical move. A soft landing rate cut is very rare."

JPMorgan is the only major US bank that is sticking to its view of a half-point rate cut. Despite other banks adjusting their rate cut expectations to 25 basis points, Michael Feroli, the bank's chief US economist, reiterated in a client report last Friday that a half-point rate cut is "the right move".

Misra also hopes that the Fed will cut rates by half a percentage point first, but she said that the possibility of a 25 basis point cut is slightly higher because policymakers may still have concerns about inflation. She added that if the Fed truly cuts rates by a quarter of a percentage point, the market reaction will largely depend on how officials "adjust" the extent of the rate cut.

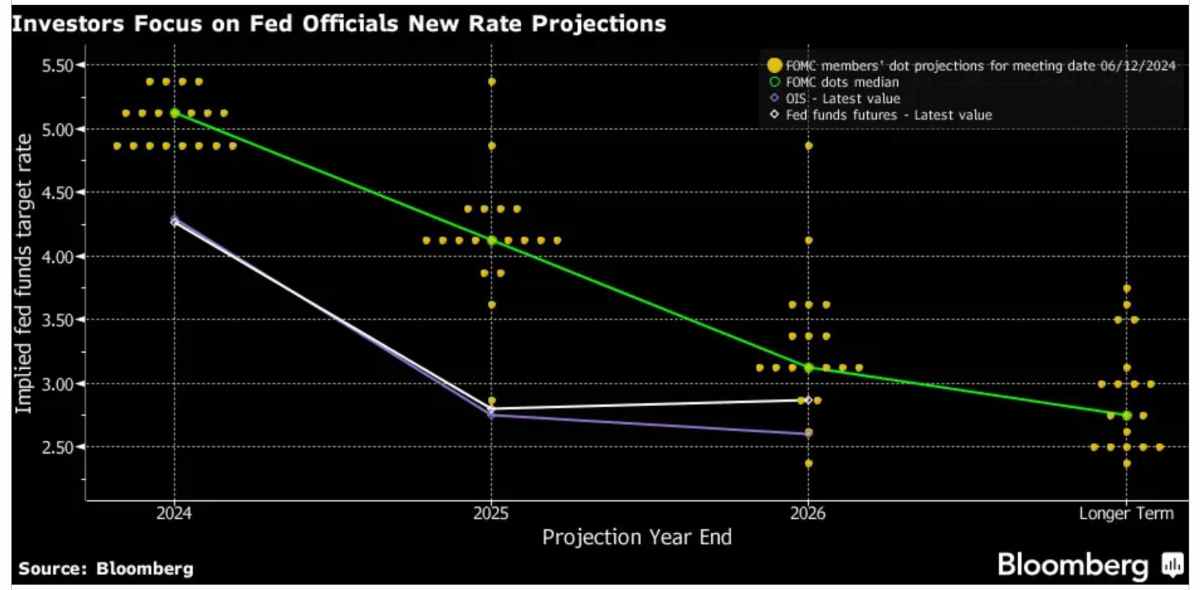

Therefore, after the rate cut confirmation, investors and analysts will focus on two things: the Fed's projection of the benchmark interest rate path (i.e., the dot plot), which will also be released as part of the latest quarterly projections, and the press conference held by Fed Chair Jerome Powell at 2:30 p.m. on the same day.

These projections will provide each policymaker's year-end expectations for each year until 2027. Although anonymous, these projections still include officials' expectations for the extremely short period from now until the end of 2024. Officials rarely provide such explicit disclosures when policy is at a turning point, but the timing of the quarterly projections leaves them no choice.

David Wilcox, former head of the Fed's Research and Statistics Division and current director of Economic Research at Bloomberg, said, "Currently, the year-end dot plot is particularly insightful. Clearly, this is more interesting because they are about to start a rate-cutting cycle."

Specifically, the dot plot will show how many members of the Federal Open Market Committee have already supported further rate cuts in November and December (according to the survey of economists, this number may be in the majority), and how many people expect one of the rate cuts to be half a percentage point. If the latter number represents a fairly large minority, it means that the Federal Open Market Committee is not far from taking more aggressive action.

Regardless of the specific numbers, it will show a huge difference from the forecast in June, when no policy maker expected the number of rate cuts this year to exceed two times.

Traders' forecasts for future interest rate trends are more aggressive. Since the disappointing July employment report, they have been roughly betting on a one percentage point rate cut in 2024. As of last Friday, they expected a rate cut of about 114 basis points by the end of December, including this week's rate cut. By the end of 2025, they expect the benchmark interest rate to drop by 3%.

Next is the standoff between Powell and journalists.

If the committee starts cautiously with a 25-basis-point rate cut, those who believe that labor market dangers are escalating will hope the Fed chair signals that officials are prepared to take more decisive action when necessary. Wilcox said that Powell himself may want to keep the option open for future meetings, regardless of how much they cut rates at the beginning.

"Whether it's announcing a 25-basis-point hike or a 50-basis-point hike, it may be a difficult decision to reach," said Wilcox, who has advised three Fed chairs. "In fact, people can disagree on this."

"Soft landing" is difficult to achieve.

Powell has hinted that he is prepared to react if the unemployment rate rises. In a speech at the Jackson Hole Symposium in Wyoming on August 23, he stated that the Fed "will not seek or welcome a further cooling of labor market conditions".

His colleague, Christopher Waller, a member of the Federal Reserve Board, was even more direct in his statement on September 6th. He not only stated that it is now time to lower interest rates, but also made it clear that further deterioration in the labor market would give the Federal Open Market Committee reason to "act quickly and forcefully".

The consequences of falling behind could be serious. Alan Blinder, former vice chairman of the Federal Reserve, believes that the Federal Reserve has only achieved a noticeable soft landing once in its history, namely in the mid-1990s. At that time, the duration of high interest rates was just enough to suppress inflation without causing the economy to enter into a recession.

More commonly, they have triggered economic recessions. Excluding the 2020 pandemic crisis, the six economic recessions in the past 50 years have pushed the unemployment rate to an average peak of 8.6%. Any such situation would result in millions of people becoming unemployed.

The current unemployment rate is 4.2%, which is significantly higher than the historical lows experienced for most of the past three years. Until April 2023, the rate remained at 3.4%, but has since risen. This summer, it triggered the well-known 'Sam rule', which usually indicates that the economy is in a recession.

Michael Kelly, the Global Head of Diversified Assets at Matsui Securities, is not predicting an economic recession, but he is very concerned and is buying long-term U.S. treasuries to hedge against this outcome.

Kelly said, "What we've seen historically is, once labor markets really collapse, they collapse fast. Once the rocks start rolling down the hill, it's hard to stand in front and stop them."

However, the Federal Reserve is very close to achieving a goal that most economists believe is unlikely to be realized, as the global supply chain weakened due to the pandemic in mid-2021, losing control over prices. The inflation indicator favored by the Federal Reserve has dropped to 2.5% in the year leading up to July, and the unemployment rate remains low.

When the Federal Reserve began its cycle of rate hikes in March 2022 with a moderate 25 basis points increase, few economists predicted that the Federal Reserve would reach this point unscathed. Subsequently, officials accelerated the pace of rate hikes in subsequent meetings, ultimately raising the target range for the benchmark interest rate to 5.25%-5.5%, where it remains today. They have implemented six significant rate hikes, each of 50 or 75 basis points.

BI strategist Ira F. Jersey and Will Hoffman suggest that unless the fed lowers interest rates by 0.25%, the market will be surprised, but clues about the change in interest rate market may be obtained from the median change in economic forecast summary for 2025. If the Fed's interest rate outlook changes, the short-term interest rate market may react reflexively after the Fed announces a rate cut. We expect the theme of 'data dependence' to continue in the post-meeting press conference.

During this process, the US economy has shown remarkable resilience. Unemployment even decreased after spending cuts began. Job vacancies that soared during the pandemic remained high, and price increases remained strong, reaching their highest level in 40 years in the summer of 2022.

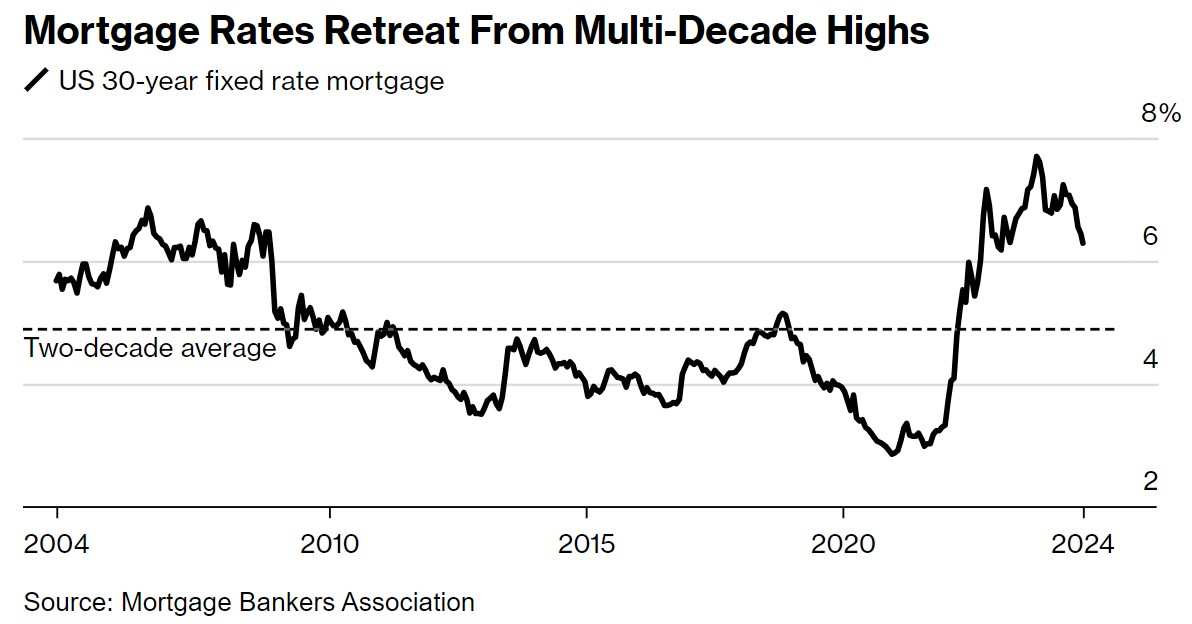

However, the recent US economic growth has slowed down. Although layoffs are still low, recruitment has stagnated, making it harder for the unemployed to find jobs. Job vacancies have dropped to the lowest level since 2021. Meanwhile, rising mortgage rates and soaring house prices have squeezed housing affordability, leading to the lowest annual new home sales in nearly 30 years in 2023.

Fed Chairman and other policymakers insist that the labor market and the overall economy are still similar to pre-pandemic conditions. Many committee members believe that the risks in the labor market are roughly balanced with the risks posed by inflation.

But the committee is not united. A few like Bullard and Chicago Fed President Charles Evans are concerned that the current threat to employment is the most severe. Others like Atlanta Fed President Bostic and Governor Bowman remain concerned about the resurgence of inflation.

This means that Wednesday's events - from the committee's statement to forecasts, to every word from Powell - will be closely watched. Investors in particular hope to be assured that officials will continue to contain inflation while preventing a downturn in the job market.

Seth Carpenter, Chief Global Economist at Morgan Stanley, said, "This will require a greater balancing act between the two aspects of the dual mandate." "For the market, they will scrutinize such matters closely."

Editor/Lambor