Recently, the hot debate over the delay in retirement policy has prompted widespread public concern about retirement issues. This policy will obviously encourage residents to pay more attention to personal retirement planning and generate greater demand for commercial retirement insurance.

Based on this, Ping An, as a leading insurer with a deep layout in the medical retirement service field, is also facing greater historical opportunities.

Recently, Ping An's premium data for the first eight months has been released, and the premium data shows its steady growth trend. So what signals worth paying attention to are conveyed behind this? How to view the long-term development opportunities facing the company?

1. Analyzing the premium data for the first eight months: Establishing the turning point and unlocking new growth opportunities.

First, let's take a look at the total premium income of Ping An this time.

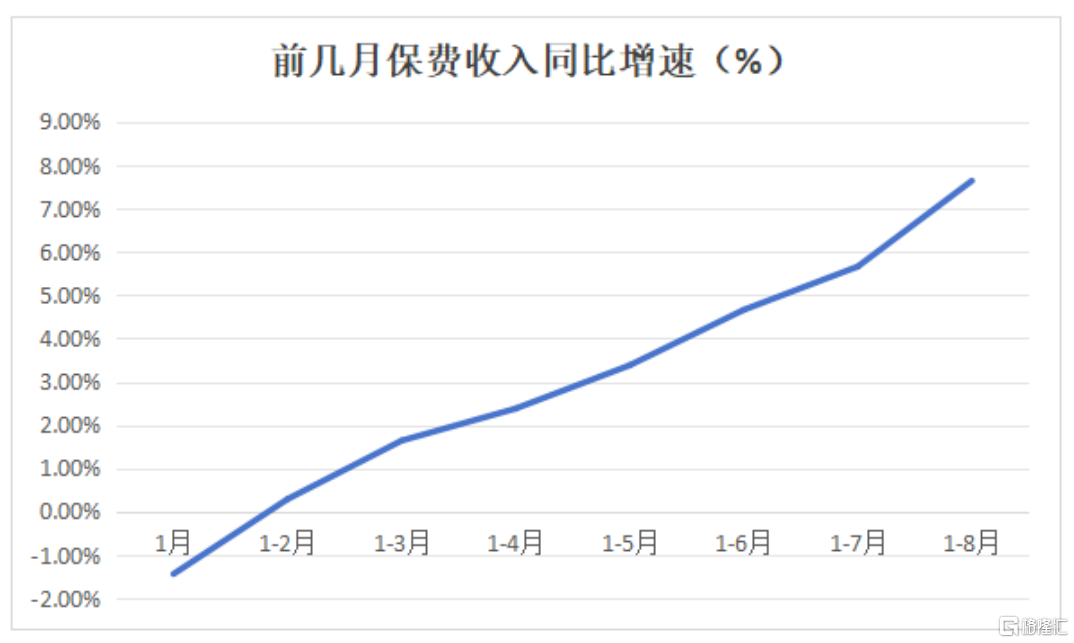

From January to August, Ping An achieved a total premium income of 620.706 billion yuan, a year-on-year increase of 7.64%, reaching a new high for the same period in history.

From the year-on-year growth rate of premium income in the first few months of this year, it is not difficult to find that Ping An has continued to maintain a trend of expansion in growth rate.

Although there was a negative year-on-year growth rate and a decrease in premium income in January, starting from February, the cumulative year-on-year growth rate of premium turned positive and continued to steadily increase. It has expanded from 0.29% in the first two months to 7.64% in the first eight months.

(Data Source: Company Announcement)

It can be seen that Ping An's premium income has shown a positive growth trend, with the growth rate increasing monthly, achieving strong recovery and growth in overall performance.

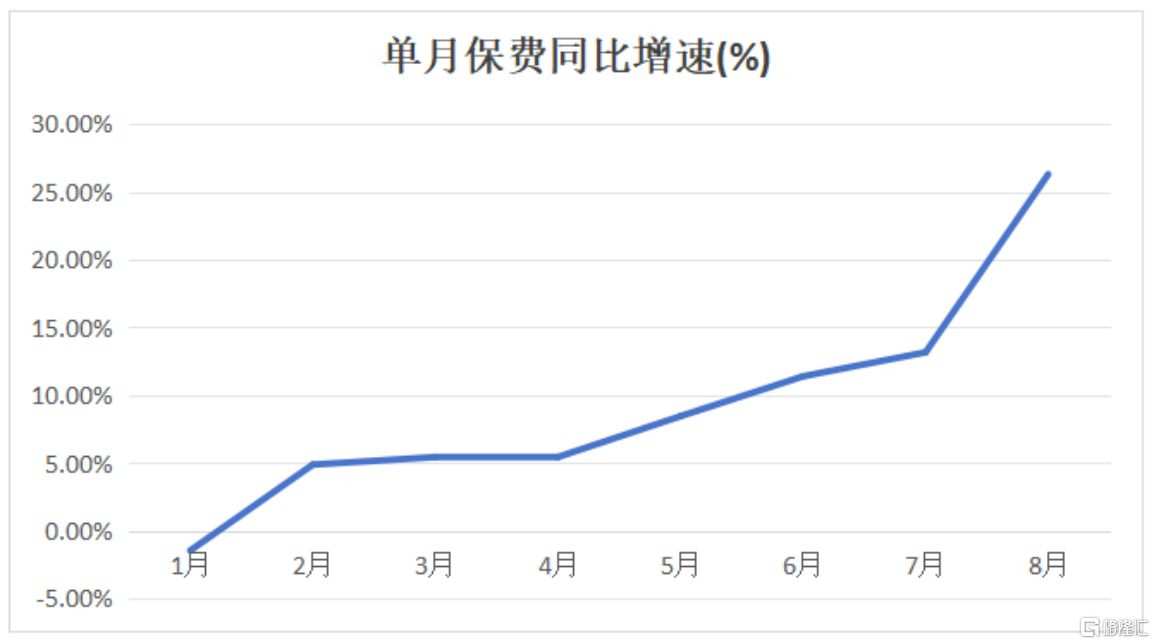

Further look at the monthly data.

So far this year, Ping An's monthly premium income growth rate has also shown a significant acceleration trend, especially in the second half of the year. The month-on-month growth rates in June and July reached 11.40% and 13.17% respectively, while August saw a significant increase to 26.29%, demonstrating strong growth momentum.

(Data Source: Company Announcement)

Further analysis of the income situation of various types of insurance reveals that Ping An's property insurance, life insurance, and health insurance businesses have all shown a positive growth trend, especially with life insurance driving a significant effect on overall premium income.

In the first eight months, the property insurance achieved a premium income of approximately 211 billion yuan, an increase of 5.32% year-on-year; life insurance achieved a premium income of around 384.629 billion yuan, an increase of 9.15% year-on-year; pension insurance achieved a premium income of around 12.812 billion yuan, a decrease of 2.43% year-on-year; and health insurance achieved a premium income of around 12.265 billion yuan, an increase of 13.70% year-on-year.

In terms of monthly data, in August, property insurance increased by 12.48% year-on-year, while life insurance performed most outstandingly with a year-on-year growth of 38.04%. In addition, pension insurance experienced a slight 0.39% year-on-year decrease, while health insurance increased by 14.35% year-on-year.

Overall, the significant increase in premium income in August, especially in life insurance, to some extent, benefited from the market's rush to buy insurance products before the scheduled interest rate adjustment.

It is worth noting that last year, the rush to buy insurance also existed during the 731 period. The overall premium base was at a high level. Looking at the data from June and July this year, even with the high base figure from the past, Ping An still maintained a high level of growth.

In August of this year, the China Banking and Insurance Regulatory Commission issued the 'Notice on Improving the Pricing Mechanism for Life Insurance Products' and the 'Notice on Steadily and Orderly Switching of Life Insurance Products,' effective from September 1, 2024. The upper limit of the scheduled interest rate for newly filed conventional insurance products will be adjusted to 2.5%, while for newly filed dividend-bearing insurance products, the upper limit of the scheduled interest rate will be further adjusted to 2.0% from October 1, 2024.

Therefore, it is not difficult to see that major life insurance companies, including Ping An, presented quite strong performance in premium income in August.

Looking at the overall industry data, the total monthly premium income of the top five life insurance companies, including China Life Insurance, Ping An Life Insurance, Taiping Life Insurance, New China Life Insurance, and People's Insurance Company of China, reached 130.515 billion yuan in August, with a year-on-year growth rate of 48%. In the first eight months, Ping An Life Insurance showed a significantly higher growth rate in premium income, demonstrating stronger momentum in the industry's prosperous phase.

(Data Source: Company Announcement)

Looking ahead, combined with the direction of policies and Ping An's own "alpha", it is reasonable to expect that Ping An's premium income growth rate in September is also likely to continue to remain at a good level, and may even perform better due to the market's response to the upcoming changes in the benchmark interest rate.

Taking a longer-term view, in a low-interest-rate environment, with the entry of bank deposit interest rates into the "1" era, savings-type insurance products are expected to meet the market's demand for stable financial management, and the value of dividend insurance will continue to be highlighted. These factors are expected to drive the demand for insurance products, thus bringing new growth opportunities for Ping An.

Overall, it is highly probable that Ping An will continue to fulfill the steady growth of premium income this year. From the operational performance displayed by the company this year, the turning point of its insurance business has been repeatedly confirmed, indicating that the previous life insurance reform has entered a new stage of releasing momentum after stepping out of the painful period.

From the new business value rate that determines the future profit of the insurance company, it also continues to verify its reform results and subsequent potential.

Earlier interim report data showed that in the first half of this year, the new business value of Ping An's life and health insurance business reached 22.32 billion yuan, an 11.0% year-on-year increase. Among them, the new business value of the agent channel increased by 10.8% year-on-year, and the per capita new business value increased by 36.0% year-on-year.

(Image source: Company overview)

可以说,这些数据充分体现了平安代理人渠道的效率和产能得到了显著提升,反映其在代理人管理和激励机制上的改革取得了喜人的成果,而这些也都为平安未来兑现持续的增长奠定了坚实的基础。

2·“综合金融+医疗养老”战略优势持续释放成长潜能

业务上的持续稳健发展,某种程度也是战略定力与优越性的外延。

平安遵循的“综合金融+医疗养老”双轮驱动模式,可以覆盖客户从年轻到老年的全生命周期,是打造差异化竞争的核心所在。

一方面,依托保险、银行、资产管理、信托、证券等多元化的金融业务,平安打通了传统金融业务之间的界限,让客户的不同金融需求可以得到一站式解决方案。通过这种交叉销售、交叉服务方式,平安的不同金融业务能够实现更低获客成本,以及更高的客户忠诚度。

平安银行、健康险、证券在对内获客的成本,分别仅为对外成本的73%、55%、53%。同时,当客户持有合同数超过4个以上时,留存率将会达到97%以上。

另一方面,平安洞察到我国老龄化趋势带来的庞大医养需求,通过提供“保险+健康管理”和“保险+居家养老”等多层次医疗养老服务,实现业务触角的延伸。

根据2024年中报,截至今年6月,平安寿险的健康管理客户总数超过16 million;居家养老业务已经在全国64个城市落地,共计超0.12 million名客户获得相关服务资格;高品质康养社区项目已在上海、杭州、深圳等5个城市启动,陆续已进入建设阶段,将于2025年起逐步开业。

This is inseparable from the medical and health ecological resources cultivated by Ping An for a long time. As of the first half of 2024, Ping An has achieved 100% cooperation coverage with the top 100 hospitals and tertiary hospitals in China, with approximately 0.05 million internal and external medical teams and 0.233 million cooperating pharmacies.

The significant effectiveness of the huge medical and health resources in empowering the insurance core business.

In the first half of 2024, 28.6% of the new customers came from the medical and retirement ecological circle, and the customers who enjoy the service rights of the medical and retirement ecological circle account for more than 68% of the new business value of life insurance. Among them, the contribution of medical and health equity customers to NBV accounted for 30.4%, an increase of 0.7 percentage points year-on-year; the contribution of retirement equity customers to NBV accounted for 38.3%, an increase of 9.3 percentage points year-on-year.

(Image source: Company overview)

It can be seen that Ping An's unique model has not only improved customer satisfaction and experience, but also brought tangible performance growth to the company. By continuously optimizing services, expanding cooperation, and strengthening technological applications, Ping An, through the dual focus on comprehensive finance and medical retirement, can provide stronger motivation for the company's long-term development, and also provide valuable experience and inspiration for the transformation and upgrading of the entire insurance industry.

3. From macro to micro, examine the three major aspects of Ping An's valuation potential

In addition to the long-term positive development at the business level, the potential for valuation improvement is also a key factor that most long-term funds in the market have a positive attitude towards Ping An.

First of all, the insurance industry itself has obvious cyclical characteristics. With the steady recovery of the macro economy, the demand for insurance products will also increase.

Especially in the context of both supply and demand for savings insurance, even with the high base effect in the first half of 2023, the top listed insurance companies have still achieved rapid growth in the NBV in the first half of this year. According to the research report of Zheshang Securities, starting from September 2024, the target interest rate for traditional insurance will be lowered to 2.5%, but the scarcity of savings-type insurance products with long-term principal and interest guarantees still exists.

Considering the current situation of "asset shortage" in the market, it is difficult to completely reverse in the short term. The scarcity of savings-type insurance will continue to be the preferred choice for embracing certainty in the long run, which is conducive to the top insurance companies achieving double-digit growth in NBV for the whole year.

In addition, the reform of the agency distribution channel is also a key factor in improving the performance of insurance companies. Taking Ping An as an example, in the first half of the year, the new business value of the agency distribution channel was 18.106 billion yuan, with a year-on-year increase of 10.8%, and the per capita new business value increased by 36% year-on-year.

In addition to the expectation of improving liabilities, the repair of assets is also an important catalyst for the valuation improvement of insurance companies.

On the one hand, although long-term interest rates represented by the 10-year treasury bond yield are at a low level, they have stabilized in stages, and the pressure of adding fixed income investments has eased. The new policies such as the new "Ten Measures" explicitly mention the need to guard against interest spread risk of insurance companies, promote the high-quality development of the insurance industry, and lower the targeted interest rate, which helps to alleviate the market's negative expectations for the investment side of insurance companies.

On the other hand, with the introduction of a package of policies to stimulate consumption and stabilize the housing market, market confidence in the repair of assets has been strengthened. According to the research report of GF Securities, the implementation of fiscal policies will promote economic growth and the recovery of asset pricing. With the gradual acceleration of broad fiscal progress and measures to reduce inventory, it is expected that nominal GDP will moderately improve, which is conducive to the recovery of price center and equity market.

The resonance repair of assets and liabilities has created a loose environment for the overall valuation repair of the insurance industry. At the same time, the valuation and positions in the insurance sector are at historically low levels, providing a low base environment for future performance.

Despite the overall good trend of the insurance sector in the first half of the year, it still has significant development potential. According to wind data, the overall P/E and P/B ratios of the insurance sector are at historically low levels.

(Source: Wind)

At the same time, although mutual funds have increased their holdings in the insurance sector due to the high dividend strategy, as of the first half of 2024, the mutual funds' holdings in the insurance sector are still only 0.37%, also at a historically low level.

(Source: Wind, Haitong Securities Research Institute)

Considering the improvement in the fundamentals of the insurance industry, combined with the high dividend feature generally held by insurers, relatively higher certainty is expected to continue to attract long-term funds to increase their allocation to insurance stocks.

Ping An, as the market-recognized leading insurer, will undoubtedly be the core beneficiary of the insurance valuation enhancement. More importantly, its development model of 'integrated finance + medical and retirement' has greatly increased its own development ceiling.

As Sheng Ruisheng, Secretary of the Board of Directors and Brand Director of Ping An, said, Ping An's model is similar to an upgraded version of Wells Fargo & Co and UnitedHealth. Wells Fargo & Co is widely recognized in the industry as a comprehensive financial practitioner, while UnitedHealth is a top-performing company in health insurance and pharmaceutical welfare management. Among them, UnitedHealth's profit is comparable to Ping An as a whole, but its market cap is 4.8 times that of Ping An.

With the support of China's vast market, Ping An has a great opportunity to unleash the enormous growth potential of "comprehensive finance + medical and retirement" by leveraging its own brand, resources, and technological advantages, bringing sustainable growth momentum.

4. Conclusion

From the premium data for the first eight months, it is not difficult to see that the insurance industry is continuing its recovery trend, and at the same time, it can also be seen that companies in the industry are still showing significant differentiation in the life insurance business premium performance. The competition pattern within the insurance industry is undergoing new changes, and different companies' strategies and market positioning are continuously showing different effects.

For Ping An, its steady growth in life insurance business, especially the significant improvement in agent channel and per capita new business value, indicates that the company has made positive progress in improving efficiency and optimizing business structure. It also demonstrates the unique competitive advantage of its "comprehensive finance + medical and retirement" model. Through this forward-looking and differentiated strategic layout, Ping An is continuously advancing its high-quality development and has gained industry recognition.

It is worth mentioning that recently, the "2024 BrandZ Top 100 Most Valuable Chinese Brands" list was released, and Ping An ranked 9th on the list, rising 2 places from the previous year. The brand value increased to $20.514 billion, making it the top brand in the Chinese insurance industry for the tenth time.

It is not difficult to expect that as the company's "comprehensive finance + home-based retirement" strategic layout continues to deepen, Ping An will continue to fulfill its resilience in steady operation and upward growth momentum, continuously driving value creation and upgrading, and occupy a core competitive advantage in future market competition.