The Southeast Asian market has a large population and is still in a period of rapid development. The potential for the development of the home appliance market is huge, and Chinese brands are thriving.

Investment highlights

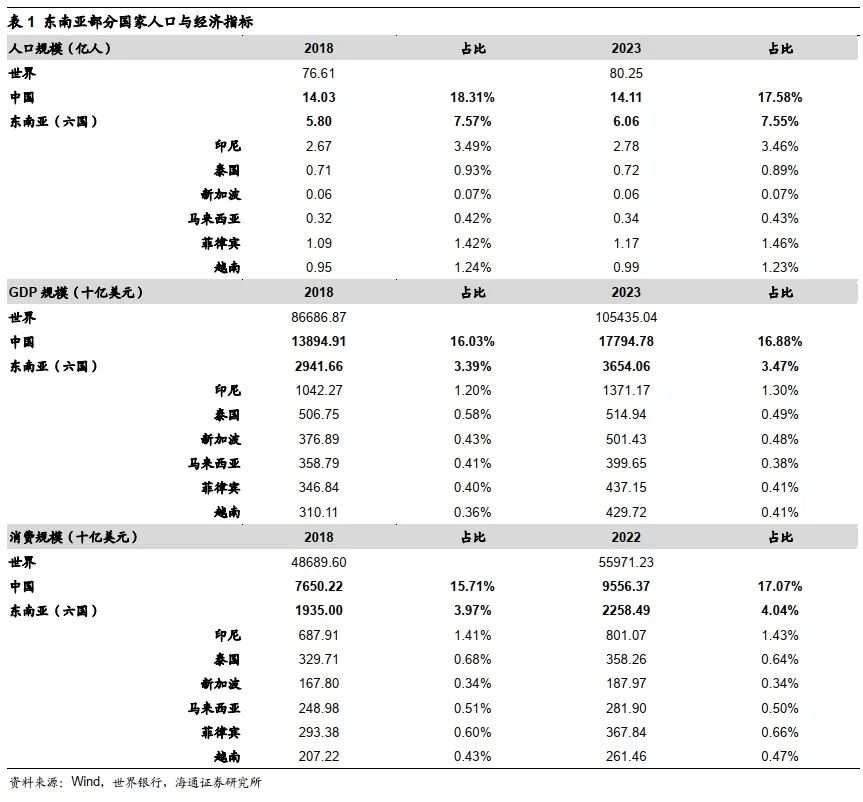

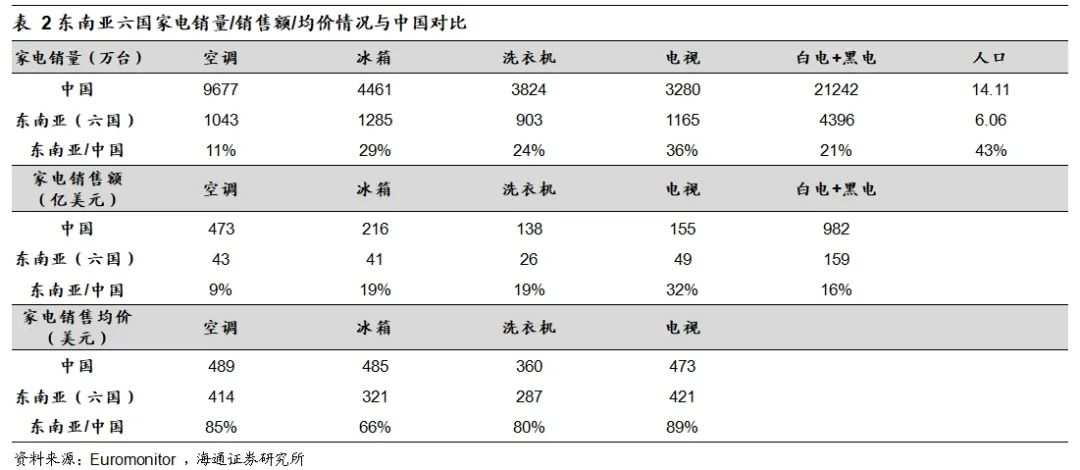

Population is the foundation: The six countries in Southeast Asia account for 7.6% of the global population and 4% of the final consumption expenditure. According to World Bank data, the population of the six countries in Southeast Asia is 0.606 billion people in 2023, accounting for 7.55% of the global total population. The six countries in Southeast Asia achieved a GDP of 3.65 trillion US dollars in 2023, accounting for 3.47% of the global total GDP. Comparing the total volume of household appliances between China and Southeast Asia, the six countries in Southeast Asia account for 43% of China's population. In terms of total sales volume of household appliances, the six countries in Southeast Asia account for 21% of China's white goods and brown goods. Due to factors such as product structure, home appliance prices in Southeast Asia are lower than in China. In terms of total sales of household appliances, the six countries in Southeast Asia account for 16% of China's white goods and brown goods.

With reference to China, the development of Southeast Asia is similar to China around 2010. We predict that their home appliances will achieve high single-digit growth in the future. In terms of per capita GDP and urbanization rate, Singapore's level of development is higher than that of China, while Malaysia is basically on par with China. Indonesia, Thailand, the Philippines, and Vietnam are at a development level similar to that of China in the 2005-2015 period. According to data from the National Bureau of Statistics, during the period of 2005-2015, China stimulated the demand for terminal home appliances through policies such as home appliances going to rural areas and trade-ins, with a compound annual growth rate of 18% for home appliance retail over the course of ten years. Looking at a longer time frame, the compound annual growth rate of home appliance retail from 2005 to 2023 is 10%. After the home appliance policies gradually recede, the industry has entered a new stage of gradual upgrading of product structure. According to Euromonitor data, the compound annual growth rate of the home appliance industry in the six countries in Southeast Asia from 2018 to 2023 is 5%, and the penetration rate is similar to that of China around 2010. Judging from the growth rate and price difference levels compared to domestic levels, we believe that the Southeast Asian home appliance market is expected to achieve growth of around 5%-10%.

With reference to China, the development of Southeast Asia is similar to China around 2010. We predict that their home appliances will achieve high single-digit growth in the future. In terms of per capita GDP and urbanization rate, Singapore's level of development is higher than that of China, while Malaysia is basically on par with China. Indonesia, Thailand, the Philippines, and Vietnam are at a development level similar to that of China in the 2005-2015 period. According to data from the National Bureau of Statistics, during the period of 2005-2015, China stimulated the demand for terminal home appliances through policies such as home appliances going to rural areas and trade-ins, with a compound annual growth rate of 18% for home appliance retail over the course of ten years. Looking at a longer time frame, the compound annual growth rate of home appliance retail from 2005 to 2023 is 10%. After the home appliance policies gradually recede, the industry has entered a new stage of gradual upgrading of product structure. According to Euromonitor data, the compound annual growth rate of the home appliance industry in the six countries in Southeast Asia from 2018 to 2023 is 5%, and the penetration rate is similar to that of China around 2010. Judging from the growth rate and price difference levels compared to domestic levels, we believe that the Southeast Asian home appliance market is expected to achieve growth of around 5%-10%.

Different home appliance categories show differentiation in Southeast Asia, with Korean brands being dominant and Chinese brands gaining more influence. (1) Current situation: In terms of categories, brown goods are generally more popular than white goods in the six countries of Southeast Asia. Among white goods, the popularity of air conditioners is low due to electricity limitations, but electric fans are popular. In terms of competition landscape, Korean brands dominate the Southeast Asian market, Japanese brands have advantages in the air conditioning field, and with Chinese companies gradually acquiring overseas brands (such as Toshiba) and establishing relevant factories in Indonesia, Thailand, and Vietnam, Chinese brands have already gained a certain market position. Due to the increased popularity of televisions in sponsoring global sporting events and the global position of the Chinese air conditioning industry, Chinese brands of televisions and air conditioners have higher acceptance in Southeast Asia and enjoy a higher market share. (2) Changes in the landscape: Compared to 2023, Chinese brands have significantly increased their market share in Southeast Asian countries, competing head-to-head with the thriving Korean brands. Japanese brands have gradually lost market share over the past five years, except in the air conditioning field where they still maintain a relatively leading market position.

China's businesses have laid out their presence in Southeast Asia: cultivating brands and prioritizing manufacturing. The layout of Southeast Asia has formed the effect of industrial agglomeration. For example, Vietnam is a gathering place for the vacuum cleaner, mobile phone, and television industries, while Thailand is primarily focused on the air conditioning and refrigeration appliance industry, making it the largest production base for white goods in Southeast Asia. Taking into account tariffs, shipping costs, local delivery, and after-sales support, Chinese businesses are accelerating their manufacturing layout in the Southeast Asian market. In the short term, factories established in Southeast Asia are primarily exporting to the European and American markets to reduce costs and avoid risks through the transfer of production capacity. In the long term, localization layout will enhance brand awareness and deeply explore the local market.

Investment advice: Pay attention to the increase brought about by going global.

Risk Warning. Fierce competition in the terminal market, slow progress in brand internationalization.

Main text

1. How to view the current situation and development potential of the home appliance market in Southeast Asia

1.1 Southeast Asia (six countries) in the global proportion: population 7.6%, GDP 3.5%, consumption 4.0%

In terms of population, according to World Bank data, the population of the six countries in Southeast Asia will be 0.606 billion people in 2023, accounting for 7.55% of the global population. The GDP of the six countries in Southeast Asia will reach 3.65 trillion US dollars in 2023, accounting for 3.47% of the global GDP. The proportion of GDP in the six countries in Southeast Asia is showing an upward trend. In terms of consumption volume, the final consumption expenditure of the six countries in Southeast Asia accounted for 4.04% of the global proportion in 2022.

Compared with China, the population of China accounts for 17.6% of the global population, GDP accounts for 16.9% of the global GDP, and the final consumption expenditure accounts for 17.07% of the global proportion.

1.2 Total amount of home appliances compared with China: sales volume accounts for 21% of China, and average price has great room for improvement.

Compared to the total amount of household appliances in China and Southeast Asia, the six Southeast Asian countries account for 43% of China's population. In terms of total sales of household appliances, the six Southeast Asian countries account for 21% of China's consumer electronics and small appliances. Due to factors such as product structure, household appliance prices in Southeast Asia are lower than in China. In terms of total sales of household appliances, the six Southeast Asian countries account for 16% of China's consumer electronics and small appliances.

In terms of product prices, the average price of refrigerators and washing machines in the six Southeast Asian countries is only 66% and 80% of that in China, respectively. We believe that this is mainly due to factors such as product structure. Looking at washing machines, the sales volume of fully automatic washing machines in the six Southeast Asian countries accounts for only 62%, while in China, fully automatic washing machines are already fully popularized and account for 95% of total sales. As for refrigerators, the sales revenue of large capacity refrigerators (400L and above) accounts for only 35%, and the sales volume is even smaller. In comparison, in China, the sales revenue of large capacity refrigerators (400L and above) has already exceeded 50%. We believe that as the level of consumption in Southeast Asia increases, optimizing the product structure is expected to drive the overall average price upwards.

In terms of development stage, Southeast Asia is equivalent to the level of China around 2010.

There are significant internal differences in economic development among various countries in Southeast Asia. In terms of per capita GDP, there are significant differences in economic development among Southeast Asian countries. Singapore leads in economic development with a per capita GDP higher than that of China. Malaysia is on par with China, while the other four countries have lower per capita GDP than China.

According to the statistics of the World Bank, China's per capita GDP in 2023 is 0.012 million US dollars, and the urbanization rate is about 64%.

Singapore Malaysia: In 2023, Singapore's per capita GDP is $0.065 million, urbanization rate is 100%, and the level of development is higher than that of China; Malaysia's per capita GDP in 2023 is $0.012 million, urbanization rate is 79%, and the level of development is similar to that of China.

Indonesia, Thailand, Philippines, Vietnam: In 2023, the per capita GDP of Indonesia, Thailand, Philippines, and Vietnam is $4248, $6385, $3668, and $3817, respectively, equivalent to China's levels in 2007, 2012, 2006, and 2006. The urbanization rates of Indonesia, Thailand, Philippines, and Vietnam in 2023 are 59%, 54%, 48%, and 39%, respectively, equivalent to China's levels in 2018, 2014, 2009, and 2003.

Overall, in terms of per capita GDP and urbanization rate, Singapore is more developed than China, Malaysia is roughly equivalent to China, and Indonesia, Thailand, Philippines, and Vietnam are at a development level similar to China's between 2005 and 2015.

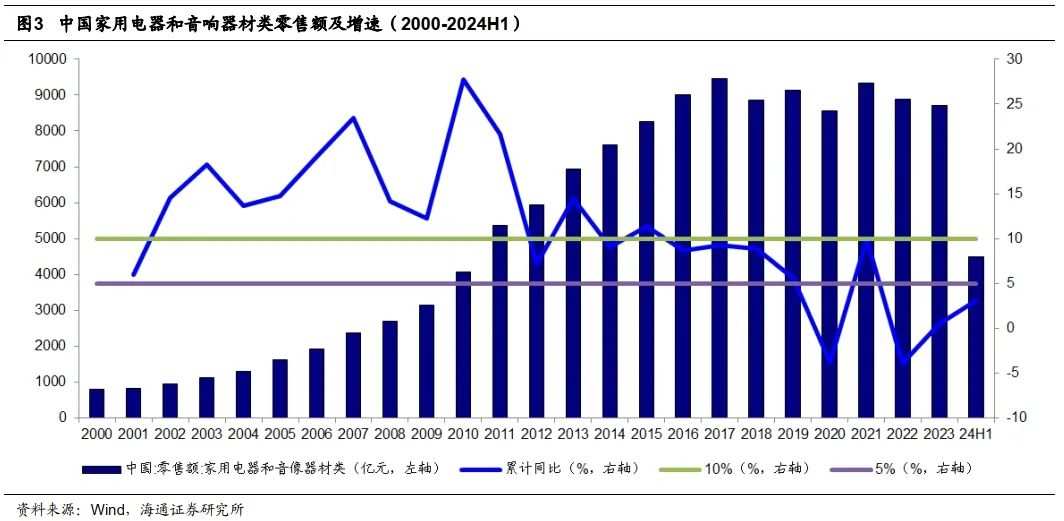

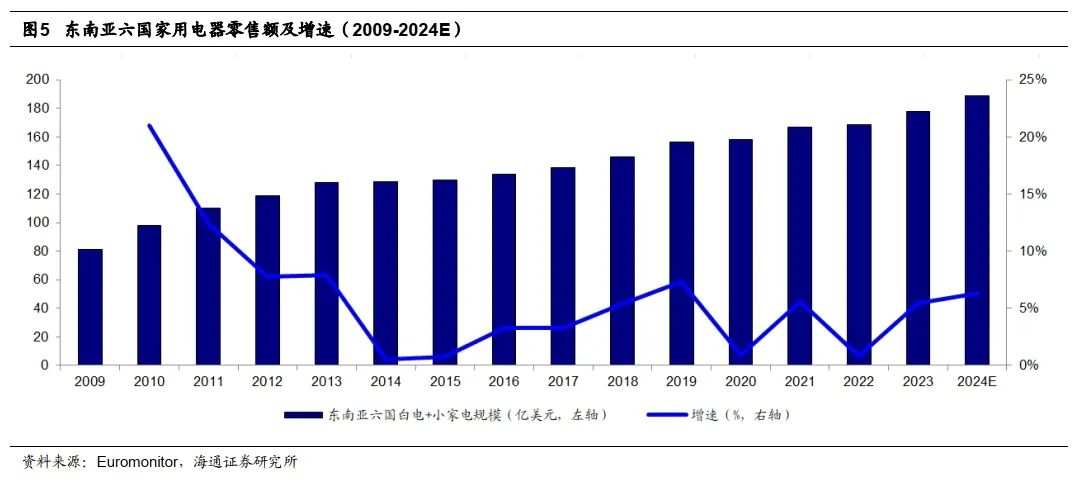

According to data from the National Bureau of Statistics, the retail sales of household appliances and audio equipment in China were 161.3 billion yuan in 2005 and 827 billion yuan in 2015. During this period, China stimulated household appliance demand through policies such as rural home appliances and trade-in programs, with a compound annual growth rate of 18% for the ten years. Looking at a longer time frame, the compound annual growth rate of household appliance retail sales in China from 2005 to 2020 was 12%, and it is expected to be 10% from 2005 to 2023.

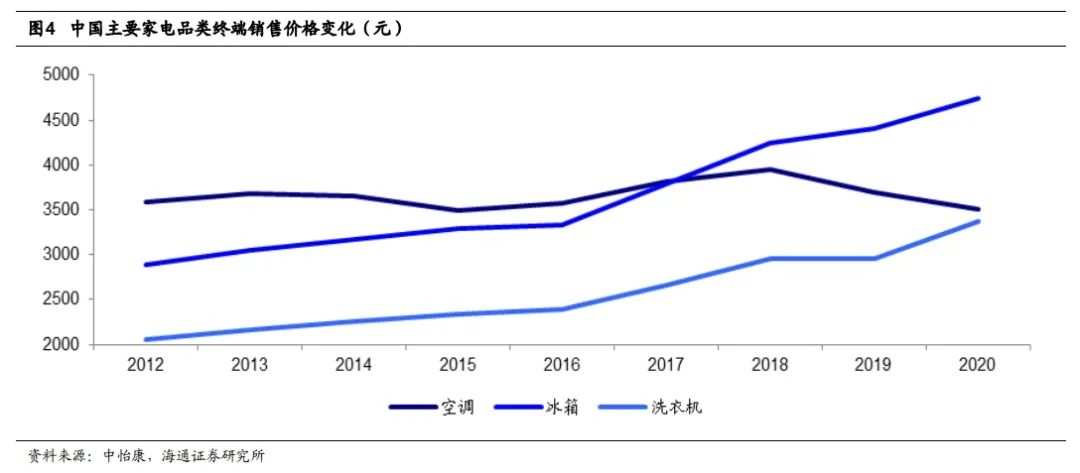

Looking back at the development of the domestic home appliance industry, it experienced a period of rapid growth from 2000 to 2012. After the gradual decline of stimulus policies, the number of household appliances increased significantly. Since 2012, the growth rate of the home appliance industry has slowed down, but the industry has entered a new stage of gradual product structure upgrading. According to price data monitored by CMM, from 2012 to 2020, the average prices of refrigerators and washing machines in the offline market in China have increased from 2891 yuan and 2061 yuan to 4740 yuan and 3375 yuan, an increase of 64% for both.

According to Euromonitor data, the CAGR of the home appliance industry in six Southeast Asian countries from 2018 to 2023 is 5%. Currently, Southeast Asia has reached a similar penetration rate to China around 2010. We believe that the Southeast Asian home appliance market is expected to gradually enter a stage of product structure upgrading, aiming for an industry growth rate of around 5%-10%, benchmarking the growth rate in China after 2010 and the current price difference level with China.

2. The performance of different categories is differentiated, and the Chinese brand's dominance has increased.

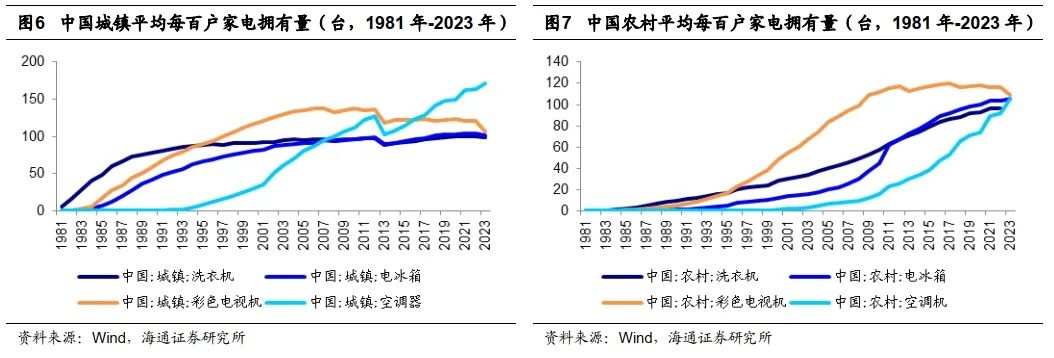

2.1 Category performance: The penetration rate of color TVs and refrigerators in China has reached 80%, while the penetration rate of air conditioners still needs to be improved.

In terms of the pace of penetration of various home appliance categories in China, the categories that have penetrated urban areas in China are washing machines, color TVs, refrigerators, and air conditioners, while the categories that have penetrated rural areas in China are color TVs, washing machines, refrigerators, and air conditioners.

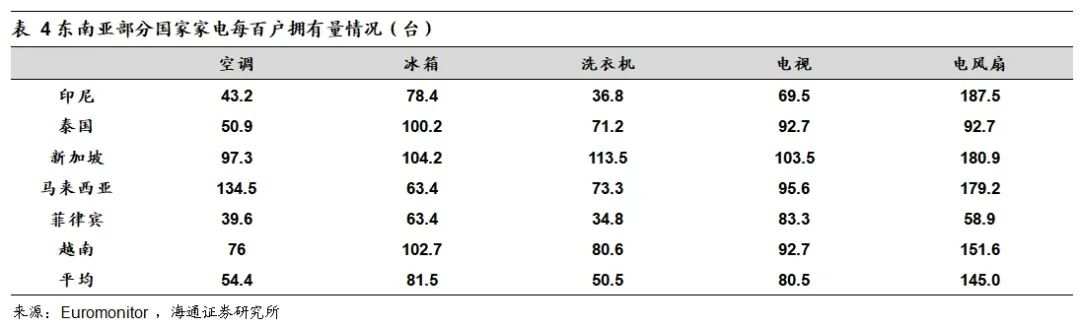

In terms of the pace of penetration of home appliance categories in Southeast Asia, it shows a similar development path to China. Color TVs were popularized earlier, while the penetration of air conditioners came later. Overall, based on population size as a weight, we estimate that by 2023, the six countries in Southeast Asia will have approximately 80 TVs and refrigerators per hundred households, and approximately 50-55 air conditioners and washing machines, and approximately 145 electric fans per hundred households.

2.2 Competitive landscape: Japanese and Korean brands have the advantage, while the dominance of Chinese brands is increasing.

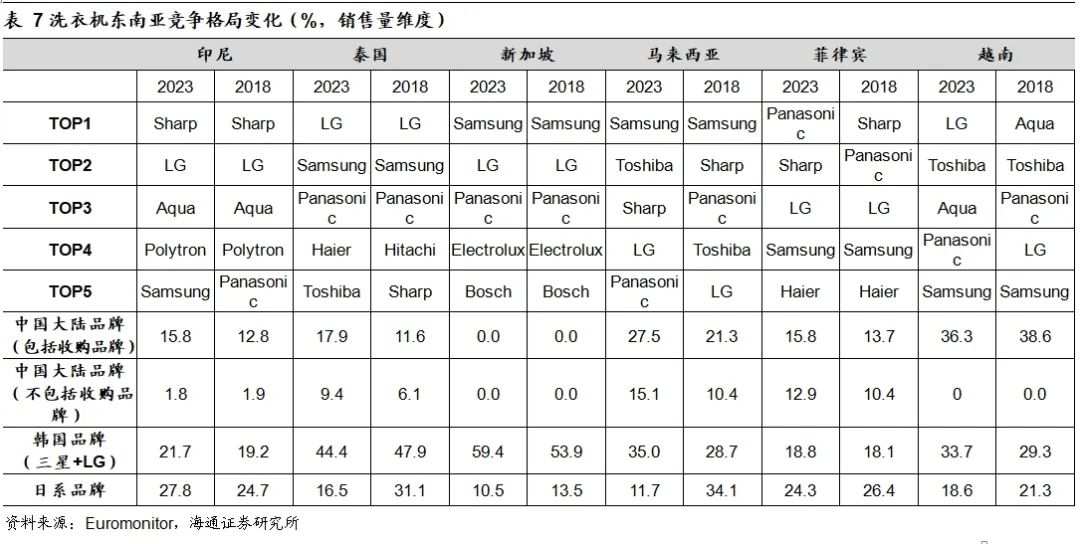

Current situation: From the perspective of the competitive landscape, we found that Korean brands still dominate the Southeast Asian market, followed by Japanese brands. With Chinese companies gradually acquiring overseas brands (such as Toshiba) and establishing related factories in Southeast Asia, Chinese brands are gradually gaining market share in Indonesia, Thailand, Vietnam and other regions.

Apart from developed countries like Singapore, Chinese brands have a relatively low market share in the other five countries of Southeast Asia, but they are accepted more widely. In terms of product categories, Chinese brands (including acquired brands) account for nearly 30% of the market share for televisions in Indonesia and Thailand, and around 10-20% in Malaysia, the Philippines, and Vietnam. For refrigerators and washing machines, Chinese brands (including acquired brands) hold a market share of over 15% in Indonesia, Thailand, Malaysia, and Vietnam, but most of this advantage is achieved through the acquisition of brands (such as Haier Smart Home's acquisition of Aqua and Midea Group's acquisition of Toshiba). The sales share of air conditioners exceeds 20% in Indonesia, Thailand, Malaysia, and Vietnam. Due to the increased awareness through sponsorships of global sports events by television brands and the global dominance of the Chinese air conditioning industry, Chinese brands of televisions and air conditioners are more accepted in Southeast Asia and enjoy a higher market share.

Changes: Compared to 2018, Chinese brands (including acquired brands) have significantly increased their market share in Southeast Asian countries. They are directly competing with the strong Korean brands, while Japanese brands have gradually lost their ground in the Southeast Asian market, with their market share declining throughout the past five years, except in the field of air conditioners where they still maintain a relatively leading market position.

3. The gradual development of Chinese home appliance companies in Southeast Asia

TV companies were the first to enter the Southeast Asian market. Overall, Chinese companies entered the Southeast Asian market in the following order: consumer electronics (black goods), white goods, and small appliances. We believe this is because TV companies started their globalization efforts earlier, and the local TV industry in Southeast Asia was more developed than the white goods and small appliances industries.

The Southeast Asian market has formed an industrial cluster effect due to the layout of Chinese home appliance companies. Currently, Chinese home appliance companies have gradually entered the Association of Southeast Asian Nations (ASEAN) market, leading to the formation of industrial clusters. For example, in Vietnam, the main industries are vacuum cleaners, mobile phones, and TVs. Companies such as Kingclean Electric, Dechang Co., Ltd., and Fu Jia Co., Ltd. have established vacuum cleaner production bases in Vietnam, while companies like BOE Technology Group and Megachips have also entered the display industry in Vietnam. In Thailand, the main industry is refrigeration appliances, such as Haier and Midea, benefiting from the large population in Indonesia and the increasing demand for home appliances. Various companies have begun to enter the Indonesian market in the air conditioning and small appliances sectors.

3.1. Consumer electronics (black goods) sector: leading in layout, prioritizing brands and marketing

TV companies were the first to enter the Southeast Asian market compared to white goods companies. Chinese TV brands were at the forefront of expanding into Southeast Asia's home appliance market. In 1998, Konka established a joint venture in Indonesia, TCL entered the Vietnamese market through the acquisition of a TV factory in 1999, and Changhong built a factory in Indonesia in 2000. The TV industry started expanding into Southeast Asia earlier than the white goods industry.

(1) TCL Electronics: Vietnam as the main battlefield, focusing on local manufacturing

TCL began to enter the Vietnamese market in 1999. In 2019, TCL started the construction of its factory in Vietnam's Pingyang, which serves as a manufacturing base for North American markets in addition to catering to the Vietnamese and ASEAN markets. Currently, TCL's business in Vietnam serves both the local market and the ASEAN market as part of its global supply chain.

According to TCL Electronics' 2023 annual report, TCL Smart TVs ranked first in retail sales in the Philippines and Myanmar in Southeast Asia, and fourth in Vietnam and Thailand. In 2023, TCL's revenue from emerging markets reached 21.3 billion Hong Kong dollars, accounting for 27% of the company's total revenue and 46% of its overseas revenue.

Risk warning: Lower-than-expected demand and intense brand competition

(2) Hisense Visual: Established headquarters in the ASEAN region and made efforts in the Southeast Asian market.

In 2022, Hisense Group established the ASEAN headquarters and made efforts in the Southeast Asian market. Hisense Home Appliances and Hisense Visual jointly invested in establishing a joint venture company in the local area in 2023 to promote business development and brand building in the ASEAN region.

Hisense Visual's brand strategy in the Southeast Asian market is to operate under the dual brands of Hisense and Toshiba. In 2023, the company will continue to enhance its regional management capabilities, significantly increase the number of channels and stores, optimize its network layout and sales touchpoints, and further expand the market space. According to GfK data cited in Hisense Visual's 2023 annual report, Hisense's TV retail market share in Malaysia and Thailand is 11.25% and 14.03% respectively.

In terms of marketing, both TCL and Hisense continue to increase their investment in sports. Hisense maintains continuous marketing activities in world-class events such as the World Cup and the European Championship, while TCL has become the official global sponsor of the Copa America football tournament multiple times, gradually enhancing the brand influence of Chinese brands in the global market.

Risk warning: Demand falls short of expectations, intense brand competition.

3.2 Home Appliance Industry: Progressive development, from production capacity to brand.

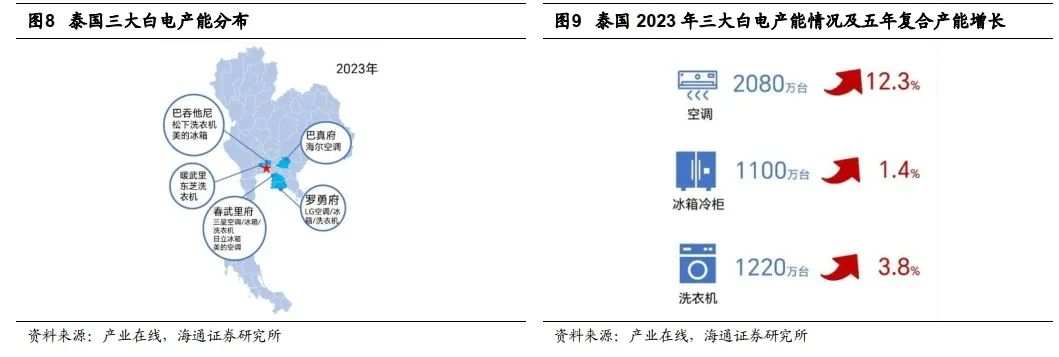

Thailand is the largest home appliance manufacturing country in Southeast Asia. Over the years, major manufacturers from Japan, South Korea, and China have established factories in Thailand. Thailand has become the world's second-largest producer of white goods after China, mainly due to the restructuring of the global home appliance manufacturing industry chain in recent years. Thailand has successfully absorbed the factory production capacity transferred from Japan, South Korea, and China.

Midea Group Co., Ltd.: Global layout, manufacturing overseas, multinational.Merger

Actively deploy factories in Vietnam, Thailand, and Indonesia. Midea Group actively lays out the Southeast Asian market, setting up its first overseas production base in Vietnam as early as 2005. The main product categories produced by Midea's Vietnamese factory are vacuum cleaners, rice cookers, fans, BBQs, etc., with exports as the main focus. The main export destinations include North America, Europe, India, and Southeast Asia. In addition to Vietnam, Midea Group has set up a total of 4 overseas production bases in Thailand, including the Midea compressor and Weiling motor factory in Bangkok, the refrigerator and washing machine factory in Pathum Thani, the refrigerator, microwave, and household appliance factory in Nakhon Ratchasima, and the air conditioner factory in Chonburi, forming a vertical integrated industry chain from upstream core components to downstream home appliances. Furthermore, Midea Group is about to start production at its air conditioning production base in Jakarta, Indonesia.

Acquiring Toshiba's white goods business to expand in the Southeast Asian market. In 2016, Midea Group acquired Toshiba's white goods business in Japan, gradually gaining recognition in the Southeast Asian market with the Toshiba brand.

Risk warning: Demand falls below expectations, intense brand competition.

Haier Smarthome: Independent brand creation, localization strategy.

Independent brand creation. Persisting in the 'independent brand creation' and 'three-in-one' strategy, serving the world with globalization, promoting globalization with localization, and reaching 200 countries and regions. In the Asia-Pacific market, the company leverages Haier Group's acquisition of Sanyo Electric assets, further enhancing Haier's local competitive advantage in Southeast Asia and Japan. Currently, Haier mainly operates under brands such as Haier, AQUA, Candy in the Southeast Asian market. Additionally, the company has established a new air conditioning industrial park in Thailand, continuously improving its global layout to enhance global competitiveness.

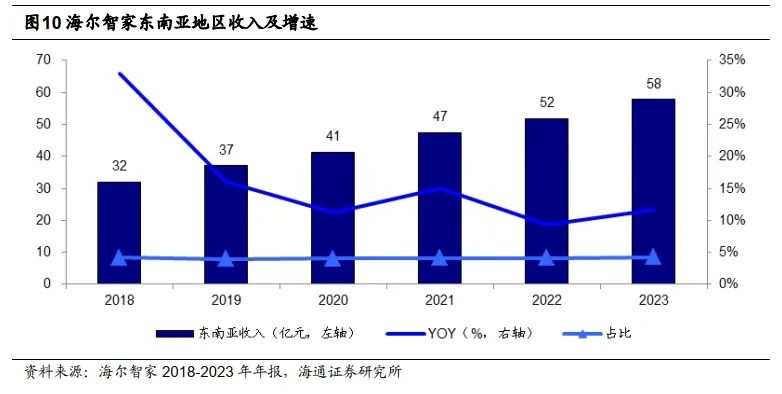

Southeast Asian market has seen double-digit growth for many years, with excellent revenue performance. The company's revenue in Southeast Asia has grown from 3.2 billion yuan in 2018 to 5.8 billion yuan in 2023, accounting for 5% of Haier's overseas revenue.

Risk warning: demand is lower than expected, brand competition is fierce.

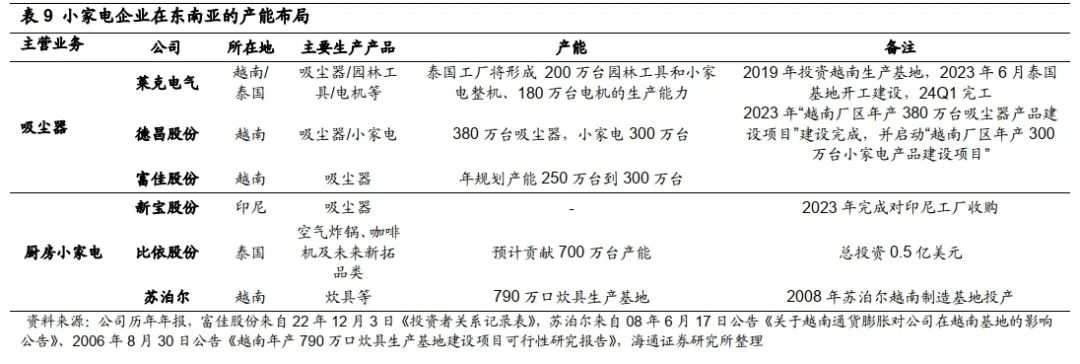

3.3 Small appliance sector: Avoiding the risk of concentrated capacity, brand's tentative investment.

Vietnam is a gathering place for the vacuum cleaner industry, with a leading capacity layout, and the brand is still being cultivated.

Capacity layout: Avoiding tariffs, balancing customer supply chains. Part of the small appliance industry chain has been transferred to Southeast Asia and other regions, mainly due to factors such as trade frictions and the need to balance customer supply chains. Currently, Vietnam has become an overseas gathering place for China's vacuum cleaner industry, with Lek, Fujia, and Dechang all establishing overseas factories in Vietnam, and Biyi Corporation, mainly producing air fryers, is expected to build new capacity in Thailand.

Brand layout: Tentative exploration. Currently, more brand layouts are being conducted in Southeast Asia for new consumer small appliance categories, such as Stone, Zhuimi, and Yunjing in the sweeping robot category, and Laifen in the personal care appliance category. Southeast Asia has a younger population with a higher acceptance of new categories, so many emerging brands are willing to invest certain resources and brands.

3.4 Summary: Be prepared in the short term, brand internationalization in the long run.

As China's economy transitions from rapid growth to high-quality development, Chinese manufacturing companies are increasing their investments in Southeast Asia and showing the characteristics of industrial cluster. For home appliance companies, there are several factors that many consider when transferring production capacity to Southeast Asia, including comprehensive cost, customer requirements, and localization.

First, in the short term, to reduce costs and avoid risks through the transfer of production capacity when targeting the European and American markets.

In the past decade, China's share in the US home appliance import market has been declining, while Mexico's share has increased significantly. At the same time, Southeast Asian countries such as Vietnam have also seen a significant increase in their share in the US home appliance import market. In the short term, Southeast Asia's cost advantages mainly include: (1) Production cost: due to the lower labor costs in Southeast Asia compared to China, if labor efficiency improves in the future, the production costs in Southeast Asia are expected to be lower than in China; (2) Tax incentives: Southeast Asian countries provide additional tax benefits to attract foreign investment and effectively reduce costs; (3) Tariff costs: Chinese companies are accelerating the layout of production capacity in Southeast Asia and other regions to proactively avoid potential future tariffs. In addition, many contract manufacturing companies establish production capacity in Southeast Asia in response to customer requirements in order to stabilize their purchasing share from large customers.

Second, in the long term, to increase brand awareness and explore the local market through deep localization.

Currently, Chinese companies' production capacity in Southeast Asia mostly meets the demands of European and American customers, while the proportion of meeting local demand is relatively small. However, in the long term, Southeast Asia has a large population and great potential for home appliance development. From a competitive perspective, Chinese brand awareness is still generally lower than that of Japanese and Korean brands. But looking at the development trends of the past few years, the recognition of Chinese brands in Southeast Asia is gradually increasing. Combined with the influence of acquired brands in the local market, Chinese companies have gained certain competitive advantages in the Southeast Asian market, and there is still a lot of room for growth. Globally, China's leading home appliance companies are gradually growing into global leaders. Compared to China, domestic brands have become the main force in the domestic home appliance market over the past 30 years due to their stronger product strength, cost-effectiveness, and extensive marketing network. Japanese and Korean brands have gradually faded in the domestic market. In the future, with the advancement of China's localization construction in Southeast Asia, China's brands have the potential to deeply explore the local market by achieving local services, on-site delivery, and aftermarket support.

4. Investment advice

Pay attention to the incremental growth brought by expanding overseas. Southeast Asia has a large population, and its economy is still in a rapid development phase. The potential for home appliance market growth is high, and Chinese brands are thriving, with still a large room for development. As Chinese brands actively expand their overseas production capacity and brand presence, the overseas market will gradually contribute to the overall stable growth of the company.

5. Risk reminders

Intense competition in the terminal market, slow progress in brand internationalization.