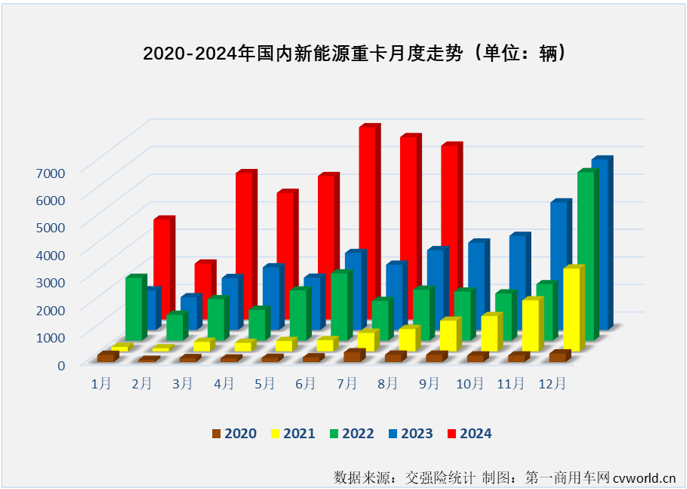

根据第一商用车网掌握的最新数据,2024年8月份,国内新能源重卡共计销售6303辆(注:本文数据来源为交强险实销口径,不含出口和军车,下同),环比7月份下降5%,同比则继续增长,增幅达到117%,新能源重卡市场已连续19个月保持同比增长。从数字上看,8月份新能源重卡市场117%的同比增幅较7月份(+179%)有所缩窄,不过6303辆的销量仍是高水准(史上第三高单月销量,仅低于今年6月份和7月份,如下图),不止如此,新能源重卡市场已连续6个月同比增速破百,今年1-8月平均月增幅高达140%。

根据第一商用车网掌握的最新数据,2024年8月份,国内新能源重卡共计销售6303辆(注:本文数据来源为交强险实销口径,不含出口和军车,下同),环比7月份下降5%,同比则继续增长,增幅达到117%,新能源重卡市场已连续19个月保持同比增长。从数字上看,8月份新能源重卡市场117%的同比增幅较7月份(+179%)有所缩窄,不过6303辆的销量仍是高水准(史上第三高单月销量,仅低于今年6月份和7月份,如下图),不止如此,新能源重卡市场已连续6个月同比增速破百,今年1-8月平均月增幅高达140%。According to the latest data from the first commercial vehicle network, the domestic new energy heavy truck total sales in August 2024 reached 6,303 vehicles, a 5% decrease from July, but a continued year-on-year increase, with a growth rate of 117%. The new energy heavy truck market has maintained year-on-year growth for 19 consecutive months.

According to the latest data from the first commercial vehicle network, the domestic new energy heavy truck total sales in August 2024 reached 6,303 vehicles, a 5% decrease from July, but a continued year-on-year increase, with a growth rate of 117%. In terms of numbers, the 117% year-on-year growth rate of the new energy heavy truck market in August is narrower than in July (+179%). However, the sales volume of 6,303 vehicles is still high (the third highest monthly sales volume in history, second only to June and July this year). Moreover, the new energy heavy truck market has achieved year-on-year growth for 6 consecutive months, with an average monthly growth rate of 140% from January to August this year.

In August, actual sales of 6,303 vehicles surged by 117%, breaking the 6,000-vehicle mark for three consecutive months.

According to the latest data from the first commercial vehicle network, the domestic new energy heavy truck total sales in August 2024 reached 6,303 vehicles (note: the data in this article comes from the actual sales of compulsory insurance and does not include exports and military vehicles), a 5% decrease from July, but a continued year-on-year increase, with a growth rate of 117%. In terms of numbers, the 117% year-on-year growth rate of the new energy heavy truck market in August is narrower than in July (+179%). However, the sales volume of 6,303 vehicles is still high (the third highest monthly sales volume in history, second only to June and July this year, as shown in the figure below). Moreover, the new energy heavy truck market has achieved year-on-year growth for 6 consecutive months, with an average monthly growth rate of 140% from January to August this year.

According to the latest data from the first commercial vehicle network, the domestic new energy heavy truck total sales in August 2024 reached 6,303 vehicles (note: the data in this article comes from the actual sales of compulsory insurance and does not include exports and military vehicles), a 5% decrease from July, but a continued year-on-year increase, with a growth rate of 117%. In terms of numbers, the 117% year-on-year growth rate of the new energy heavy truck market in August is narrower than in July (+179%). However, the sales volume of 6,303 vehicles is still high (the third highest monthly sales volume in history, second only to June and July this year, as shown in the figure below). Moreover, the new energy heavy truck market has achieved year-on-year growth for 6 consecutive months, with an average monthly growth rate of 140% from January to August this year.

As can be seen from the above graph, the red bars representing 2024 have been very "eye-catching", whether looking at the overall or individual months, they are significantly higher than the previous few years. Especially in the past three months, June, July, and August, which happen to be the three months with the highest sales volume in the history of the new energy heavy truck market. As of August 2024, the monthly sales of new energy heavy trucks have exceeded 6,000 vehicles five times, with 3 of them occurring in the recent months of June to August, and the sales volume in the previous months of March to May was also not low (around 5,000 vehicles). From the sales data, it can be seen that the new energy heavy truck industry is currently in its first peak period.

As can also be seen from the above graph, since June 2023, the new energy heavy truck market has consistently maintained a high level. Therefore, it will become increasingly difficult for the new energy heavy truck market to continue to grow at a high rate in the future. However, based on the high level of the recent months, the current round of growth in the new energy heavy truck market will definitely not stop at "19 consecutive increases".

In August 2024, the domestic heavy truck market continued to weaken, with only 0.04 million vehicles sold, a year-on-year decrease of more than 20%. The year-on-year growth rate of new energy heavy trucks in August was 117%, continuing to significantly outperform the overall market. According to the data from the First Commercial Vehicle Network, as of August this year, new energy heavy trucks have continuously outperformed the 'large cap' of the industry for 15 consecutive months. It is worth mentioning that in the first 8 months of this year, new energy heavy trucks have significantly outperformed the 'large cap' of the heavy truck market, with an increase of at least 85 percentage points higher than the overall growth rate of the heavy truck market. The new energy heavy truck market has shown strong resilience in recent months, continuously achieving triple-digit year-on-year growth, and has not been affected by the weakening of terminal demand for heavy trucks. The overall sales of heavy trucks have continued to decline for 5 consecutive months, and August was originally the off-season for heavy truck sales. The recent months have shown the remarkable resilience of the new energy heavy truck market.

In August, the market share of new energy heavy trucks in the terminal sales of the heavy truck market reached 15.7%, an increase from the previous month's 14.2%. The penetration rate of new energy heavy trucks has exceeded 10% for three consecutive months. From January to August this year, the market share of new energy heavy trucks in the terminal sales of the heavy truck market reached 10.48%, a significant increase from the full-year market share of 5.58% in 2023, and a much higher increase compared to the same period last year (which was about 4.05%). Objectively speaking, although the high penetration rate of new energy heavy trucks since 2024 has been a 'boost' for the overall performance of the heavy truck market, the continuous positive development momentum of China's new energy heavy trucks is beyond doubt.

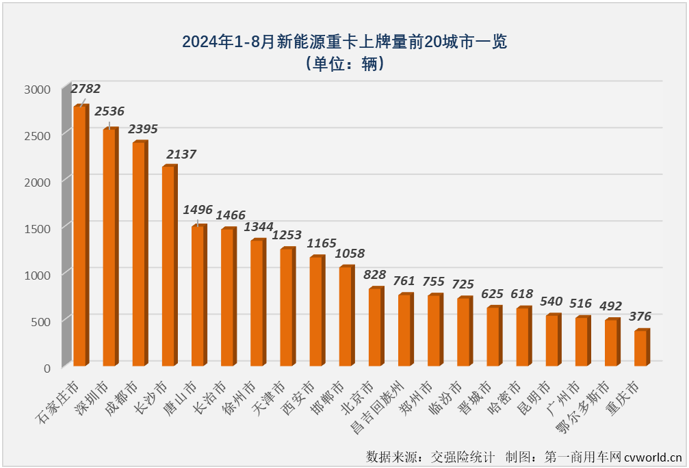

From January to August 2024, new energy heavy trucks were registered and put into operation in all 31 provinces (autonomous regions and municipalities) in the country. In fact, in the first month of 2024, the penetration of new energy heavy trucks had already spread across the country. By August, 13 provinces in China had registered more than 1000 new energy heavy trucks, with Hebei Province registering more than 6000, and Shanxi, Guangdong, Sichuan, Hunan, and other provinces registering more than 3000. Specifically, from January to August 2024, there were 276 cities across the country where new energy heavy trucks were registered, with 39 cities registering more than 200 vehicles, and 26 cities registering more than 300 vehicles. The cities with more than 2000 registered vehicles included Shijiazhuang, Shenzhen, Chengdu, and Changsha.

Xugong/Sany/FAW are competing for the top spot, with Foton skyrocketing into the top four of the monthly rankings.

In August 2024, 11 companies in the new energy heavy truck market sold more than 100 vehicles, with 1 more company exceeding 100 vehicles compared to the previous month. It is worth mentioning that in August, 9 companies sold over 400 new energy heavy trucks, 6 companies sold over 500, and 3 companies sold over 900, continuing the strong market performance of the previous months.

(Note: The above chart shows the sales volume of new energy heavy truck chassis manufacturers, while the sales volume of retrofit manufacturers is not listed separately. In August, JAC sold 89 new energy heavy trucks under the brand DeepWay, and JMC sold 23 units under the joint heavy truck brand ZeroOne, the Strike pure electric tractor.)

In August, XCMG won the championship with a sales volume of 1014 vehicles, winning its 5th new energy heavy truck monthly championship this year; Sany and Jiefang ranked 2nd and 3rd with 996 and 983 vehicles respectively. Jiefang once again refreshed its highest monthly sales volume in the new energy heavy truck market; Foton (600166.SH) ranked 4th with a sales volume of 564 vehicles, creating its highest monthly sales volume and highest monthly ranking this year; Yutong and Shaanxi Auto, ranked 5th and 6th on the monthly list, also exceeded 500 vehicles, reaching 512 and 509 vehicles respectively; FAW (03808), Dongfeng, and Far East ranked 7th to 9th in the August monthly list, with sales volumes all exceeding 400 vehicles, reaching 447, 418, and 401 vehicles respectively; JAC and Hongyan also both exceeded one hundred in August, ranking 10th and 11th on the monthly list.

It can also be seen from the chart that the sales volume of mainstream new energy heavy truck companies in August this year was higher than the same period last year. Among the top 15 companies in monthly sales volume, 8 of them achieved double-digit growth, with Jiefang, Foton, and CAMC achieving explosive growth, with year-on-year increases of 301%, 324%, and 1350% respectively, competing to lead the market. Sany and JAC achieved year-on-year growth rates of 292% and 285% respectively.

In the full year of 2023, there were a total of 20 players with cumulative sales of over 100 units in the new energy heavy truck market, and 9 players with cumulative sales of over 1,000 units. After August 2024, the number of players with sales of over 100 units had reached 20, and those with sales of over 1,000 units had reached 10. It should be noted that after the first quarter, these numbers were 12 and 3 respectively, showing how hot the new energy heavy truck market has been in recent times.

Sales of new energy heavy truck companies from January to August 2024 (unit: vehicles)

As can be seen from the table, from January to August 2024, the cumulative sales of new energy heavy trucks reached 0.0406 million units, a year-on-year increase of 142%, and the cumulative sales growth rate narrowed compared to after July (+148%). Looking specifically at mainstream companies, only one voice is of growth. Among them, FAW, Jiefang, Yutong, Shaanxi Auto, Foton, and JAC have all outpaced the overall growth of the new energy heavy truck market. XCMG and Sany, ranked first and second, achieved year-on-year cumulative sales growth of 135% and 120% from January to August this year. Both companies achieved double-digit growth from the high sales volume in the same period last year, although the growth rates were lower than the overall market growth rate, their growth potential is very high. XCMG and Sany have contributed nearly 4000 and over 3600 units, respectively, to the new energy heavy truck market from January to August this year.

It is worth noting that Jianghuai's new energy heavy truck sales from January to August this year surged by 1151%, leading the industry. First Commercial Vehicle Network noted that over 90% of Jianghuai's sales of new energy heavy trucks this year came from DeepWay pure electric tractors. Since the beginning of the year, DeepWay has repeatedly surged into the top ten of the new energy heavy truck monthly rankings, and now its position in the top ten of the new energy heavy truck industry has become more stable. It should be noted that at the same time last year, Jianghuai was still hovering around the 20th place in the industry.

From the perspective of market share, in the period from January to August 2024, XCMG New Energy Heavy Truck sold a total of 6,901 vehicles, ranking first in the industry with a market share of 16.98%. Sany New Energy Heavy Truck ranked second with a cumulative sales of 6,662 vehicles and a market share of 16.40%. The sales of Qingling New Energy Heavy Truck reached 3,956 vehicles, ranking third with a market share of 9.74%. Qingling's market share has increased by 4.55 percentage points compared to the same period last year, showing the most significant improvement.

Another company with a significant increase in market share is Jiefang, currently ranking fourth in the cumulative sales chart. Jiefang sold a total of 3,786 new energy heavy trucks from January to August this year, with a market share of 9.32%, an increase of 3.82 percentage points compared to the same period last year. Yutong, Shaanxi Auto, and Dongfeng ranked 5th to 7th, with cumulative sales exceeding 3,000 vehicles and market shares of 8.70%, 8.67%, and 7.45% respectively. Yutong and Shaanxi Auto have increased their market shares compared to the same period last year. Foton and YEMA, currently ranked 8th and 9th, have cumulative sales of over 2,000 vehicles from January to August, capturing market shares of 6.28% and 5.97% respectively. Foton's market share has increased by 2.96 percentage points compared to the same period last year.

JAC, currently ranked 10th in the industry, has accumulated sales of 1,051 vehicles from January to August this year, with a market share of 2.59%, an increase of 2.5 percentage points compared to the same period last year. SAIC Hongyan and Beiben have also sold over 500 vehicles, ranking 11th and 12th, with market shares of 1.58% and 1.31% respectively.

Pure electric vehicles accounted for over 90% of the total, while hybrid heavy trucks witnessed a staggering 404% increase from January to August.

First Commercial Vehicle Network has noticed that since 2024, the new energy heavy truck market has continued to focus on pure electric technology. From January to August this year, fuel cell heavy trucks and hybrid heavy trucks accounted for only 6.89% of the entire new energy heavy truck market, with the remaining 93.11% being pure electric vehicle models (this proportion is higher than the same period last year and the whole of 2023, but slightly lower than the proportion in the same period of 2022, as shown in the graph below).

Corresponding to the increase in the proportion of pure electric heavy trucks, the proportion of fuel cell heavy trucks has decreased by 3.6 percentage points compared to the same period last year. From January to August this year, the cumulative sales of fuel cell heavy trucks reached 2,562 vehicles, with a year-on-year growth of 54%. It is the only type among the three major technology routes of new energy heavy trucks that has lagged behind the market 'large cap'.

From January to August this year, 20 'players' have participated in the competition in the fuel cell heavy-duty truck market, with 9 companies having cumulative sales of over 100 vehicles. As shown in the figure, the competition in the fuel cell heavy-duty truck market is very intense at present. The sales of the top 4 companies, Dongfeng, Shaanxi Auto, Foton, and Jiefang, all exceed 350 vehicles, with very small differences between neighboring companies. The differences between Shaanxi Auto, Foton, and Jiefang are all within 5 vehicles, making the ranking competition very intense. In addition, Yutong, Foton Auman, Dayun, Sany, and Long March, among other companies, have also accumulated sales of over 100 vehicles.

Now let's take a look at the increasingly prominent presence of hybrid power heavy-duty trucks (including diesel hybrid, methanol hybrid, and natural gas hybrid). From January to August, 237 hybrid power heavy-duty trucks have been registered across the country, accounting for 0.58% of the market share in the new energy heavy-duty truck market, a 0.3 percentage point increase compared to the same period last year.

From January to August this year, a total of 237 hybrid power heavy-duty trucks were sold, representing a staggering 404% year-on-year increase, significantly outperforming the overall 142% growth of the new energy heavy-duty truck market. As of August, the hybrid power heavy-duty truck market this year has attracted 7 companies, including Yutong, Sany, Beiben, Jiefang, Foton, Changzheng, and Joint Heavy Truck. Among them, the top-ranked Yutong has accumulated sales of over 100, and Sany, Beiben, Jiefang, and Foton have also reached double digits in cumulative sales. The hybrid power heavy-duty trucks of these companies are now being put on the road in multiple cities, mainly in the form of tractors, dump trucks, and concrete mixers.

Conclusion

From June to August, the sales of new energy heavy-duty trucks have maintained a high level of over 6,000 vehicles, achieving continuous doubling growth, completely unaffected by the off-season sales of the heavy-duty truck industry. Recently, all the production companies of new energy heavy-duty trucks are in full swing. In August, 3 companies had sales of over 900 vehicles, 6 companies had sales of over 500 vehicles, and 9 companies had sales of over 400 vehicles. More than half of the companies achieved doubling growth. From the industry to individual companies, the new energy heavy-duty truck market remained highly active in August.