Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Shutterstock, Inc. (NYSE:SSTK) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

What Is Shutterstock's Debt?

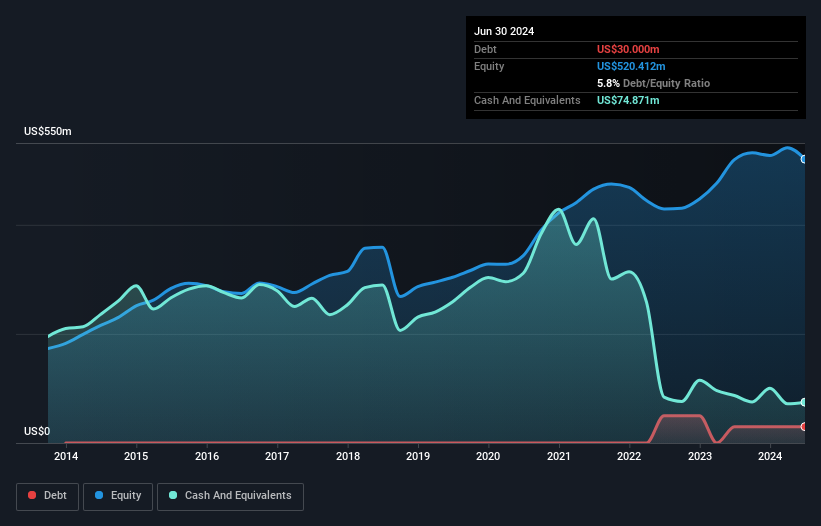

As you can see below, Shutterstock had US$30.0m of debt, at June 2024, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds US$74.9m in cash, so it actually has US$44.9m net cash.

How Healthy Is Shutterstock's Balance Sheet?

The latest balance sheet data shows that Shutterstock had liabilities of US$432.3m due within a year, and liabilities of US$51.1m falling due after that. Offsetting this, it had US$74.9m in cash and US$128.9m in receivables that were due within 12 months. So it has liabilities totalling US$279.6m more than its cash and near-term receivables, combined.

The latest balance sheet data shows that Shutterstock had liabilities of US$432.3m due within a year, and liabilities of US$51.1m falling due after that. Offsetting this, it had US$74.9m in cash and US$128.9m in receivables that were due within 12 months. So it has liabilities totalling US$279.6m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Shutterstock is worth US$1.18b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, Shutterstock also has more cash than debt, so we're pretty confident it can manage its debt safely.

But the bad news is that Shutterstock has seen its EBIT plunge 17% in the last twelve months. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Shutterstock's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Shutterstock has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Shutterstock recorded free cash flow worth a fulsome 82% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Summing Up

Although Shutterstock's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$44.9m. The cherry on top was that in converted 82% of that EBIT to free cash flow, bringing in US$27m. So we don't have any problem with Shutterstock's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 3 warning signs for Shutterstock that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.