在动辄成千上万道芯片制造工序中,有30%都在重复一件事情,那就是给娇嫩且患有严重洁癖的芯片用大量的水和化学溶剂洗澡,去除上一道工序的残留,为下一步做准备。

在动辄成千上万道芯片制造工序中,有30%都在重复一件事情,那就是给娇嫩且患有严重洁癖的芯片用大量的水和化学溶剂洗澡,去除上一道工序的残留,为下一步做准备。Source: Yaya Hong Kong Stock Circle

Author: Kyle

In the first half of this year, statistics show that at least 180 Hong Kong stock companies have implemented share buybacks, with a total amount of HKD 121 billion, setting a new high in the same period of history. Especially in the Internet companies, almost every shareholder return program has been significantly improved, which can be said to have opened a new era of Internet shareholder returns.

Among these companies, Tencent, the "North Star" of Hong Kong stocks, is undoubtedly the most prominent. In the first half of this year, it contributed more than 40% of the repurchase volume of the Hong Kong stock market, firmly occupying the seat of the "repurchase king" of the Hong Kong stock market. In the second quarter, Tencent's single-quarter repurchase amount reached HKD 37.5 billion, which doubled from the first quarter's HKD 14.8 billion. The repurchase average price increased from HKD 290.6 to HKD 361.8, an increase of nearly 25%. It is worth mentioning that Tencent's repurchase amount this year will exceed HKD 100 billion, doubling from last year's HKD 49 billion. What is the concept of a one trillion repurchase plan? This amount is the sum of Tencent's total repurchase amount in the past ten years, which proves the management's confidence in future development and attaches importance to the demands of investors. Through various means such as repurchase cancellation, dividends, and physical distribution, Tencent has truly given back to shareholders in the capital market while achieving performance growth.

One, the significance of a trillion repurchases is actively emerging.

Looking back at the past two years, since Tencent's major shareholder Prosus began to reduce its holdings, the stock price has been somewhat suppressed. In particular, there have been regular trading behaviors in the market when Hong Kong stocks perform poorly. For example, Hong Kong-listed companies have a "silent period for repurchase" in the month before the financial report is released, during which repurchase is not allowed. This caused great upward pressure on the stock price whenever Tencent entered the repurchase silent period before last year.

As can be seen from the following data, of the five silent periods before the end of 2023, only Tencent's stock price in October-November 2022 rose, and in other times it fell. However, since the end of last year, Tencent's stock price has risen during two consecutive silent periods. Especially after the launch of the trillion-dollar repurchase plan this year, the repurchase volume has far exceeded the number of shares sold by major shareholders. Therefore, whether it is on normal trading days that can be repurchased, or during silent periods, the impact brought by the sale of major shareholders can be ignored, and this point is being formed by market consensus. For example, during the repurchase silent period from January to March this year, which happened to be the worst half-year Hong Kong stock market, the Hang Seng Index fell to 14,800 points. Tencent's performance during this period was significantly better than before. Even though the short selling ratio once reached 20%, the stock price did not fall, and the final interval increase was 6%. After the release of the better-than-expected 2023 annual report and the restart of the repurchase at the end of March, Tencent's stock price performed even better in the second quarter, with an increase of nearly 25%. During the same period, the Hang Seng Index and the Shanghai and Shenzhen Composite Indexes fell significantly, with gains of only 8% and 4%, respectively, while Tencent significantly outperformed the Hong Kong stock market with a gain of 25%.

Behind this phenomenon, there is no doubt that the trillion-dollar repurchase plan, which has doubled from last year's amount, has played an important role.

More importantly, after the repurchased shares are cancelled, Tencent's share capital has been declining for three consecutive years. Since 2021, Tencent's total share capital has decreased from 9.608 billion shares to 9.355 billion shares. In the first quarter of this year, Tencent issued ordinary shares decreased by 1.1% compared to the previous quarter, and the repurchased shares have also been gradually cancelled since this year. This trend will continue to increase earnings per share and further enhance shareholder value. (Caption) Starting in 2022, Tencent has increased its repurchase efforts. With the repurchase cancellation, the company's total share capital has gradually decreased.

Author: Joshua

The semiconductor manufacturing industry is a thirsty industry.

Before, $Taiwan Semiconductor (TSM.US)$ it used 0.2 million tons of water for chip cleaning, which is equivalent to the daily water consumption of the entire Taiwan province, and Intel uses 34 million tons of water in a year, which is equivalent to drying up 2.5 West Lakes in Hangzhou.

In the thousands of chip manufacturing processes, 30% of them are devoted to one thing, which is to bathe the delicate and germaphobic chips with a large amount of water and chemical solvents, to remove residues from the previous process and prepare for the next step.

But if you think that these water resources can be provided by Nongfu Spring, the natural water carrier, then you are wrong. Every link in the chip manufacturing process requires professional equipment and materials to support production. Even 'water' has a high barrier to entry. Currently, most of the semiconductor materials and equipment are supplied by Japanese companies that have accumulated rich experience in the industry.

But if you think that these water resources can be provided by Nongfu Spring, the natural water carrier, then you are wrong. Every link in the chip manufacturing process requires professional equipment and materials to support production. Even 'water' has a high barrier to entry. Currently, most of the semiconductor materials and equipment are supplied by Japanese companies that have accumulated rich experience in the industry.

The reason why Japan's stock market has outperformed the US, China Taiwan, and South Korea in the global capital inflows into semiconductor-related stocks is because most of their semiconductor companies have never left the table, and their accumulated experience can be put into action at any time, greatly reducing the time and cost of trial and error that downstream customers value the most, thus winning market favor.

1. Not everyone is equal in the face of opportunities.

The water used to wash chips is called ultrapure water. In addition to H2O, it is required that there are almost no impurities in this water. Ultrapure water is essential for miniaturization and stacking of semiconductor circuit linewidths, and the more advanced the chip, the more process steps it has, and the greater the amount of water consumed.

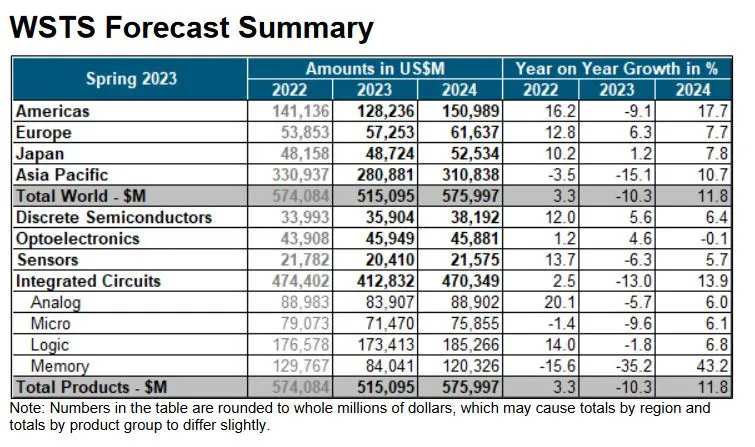

Therefore, when the global semiconductor market is expected to reach a historical high of $576 billion, the demand for ultrapure water also expands.

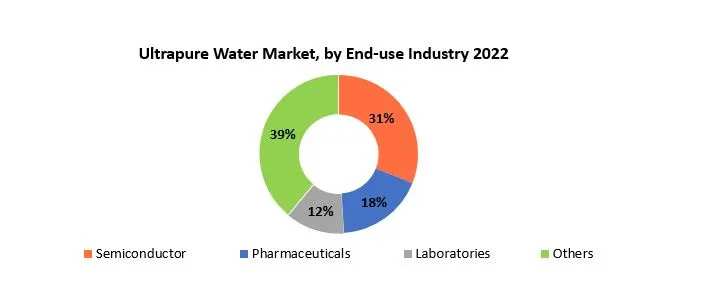

The global market for ultrapure water for semiconductors is estimated to be approximately $1.692 billion in 2023 and is expected to reach $2.711 billion by 2030, with a CAGR of 7.9% from 2024 to 2030. In terms of downstream, wafer manufacturing is the largest application market, accounting for about 82% of the market share.

In terms of market demand, it seems that semiconductor-related companies worldwide have equal opportunities in this potential market. However, in the "seniority-based" semiconductor industry, the reality is not so.

Because the semiconductor equipment industry is a B2B business, the core of industry competition lies in the level of technological advancement and certification issues for entering the customer supply chain. In such a high threshold and lengthy certification process, in order to reduce trial-and-error costs, downstream customers rarely accept new faces. As a result, the industry has become an insider's game, collectively exclusive between upstream and downstream.

As early as the 1980s, Japan had become the world's largest semiconductor industry, with a well-established independent semiconductor industry system. This also makes Japan the second economy after the United States capable of riding the wave of the semiconductor industry's resurgence. The semiconductor companies in Japan are also the ones that benefit the most from the AI boom and have seen the largest increase in stock prices in line with the U.S. stock market.

Nowadays, under the monopoly of TSMC, Samsung Electronics, and Intel, the investment scale of semiconductor equipment is becoming larger, requiring ultra-pure water treatment facilities of the size equivalent to a football field. There are only a few manufacturers in the world that can design and deliver such large-scale equipment in a short period of time, with the experience and tricks to quickly respond to malfunctions in after-sales service.

Of course, it doesn't mean that new entrants have no opportunities. However, in order to ensure that the company always stays at the forefront of technology, NVIDIA's new semiconductor technology roadmap is updated every year. From ChatGPT to Midjourney, from Sora to Kimi, AIGC needs to maintain the frequency of historic breakthroughs every month to keep consumers' interest fresh.

From the production of computing power to the application of programs, the entire industry is in a tense competition akin to military preparation. Time is money, and nobody wants to wait for a new entrant to grow. Japanese companies that already have skilled workers, technical expertise, equipment, and scale advantages in the semiconductor industry naturally become the first group of people to stand at the forefront.

Second, two worlds in mutual admiration

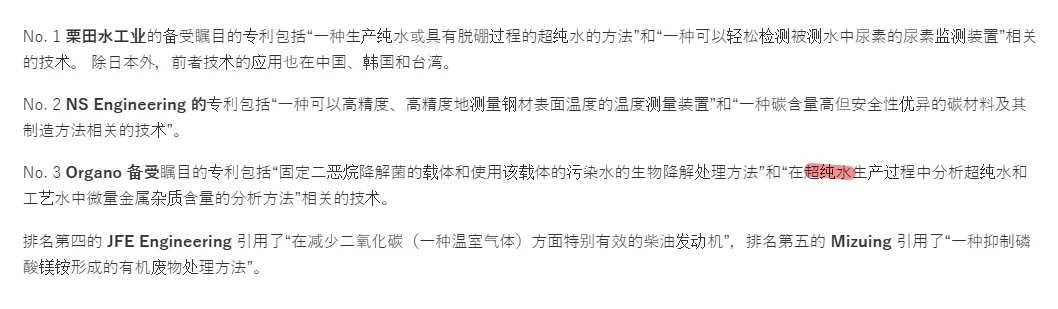

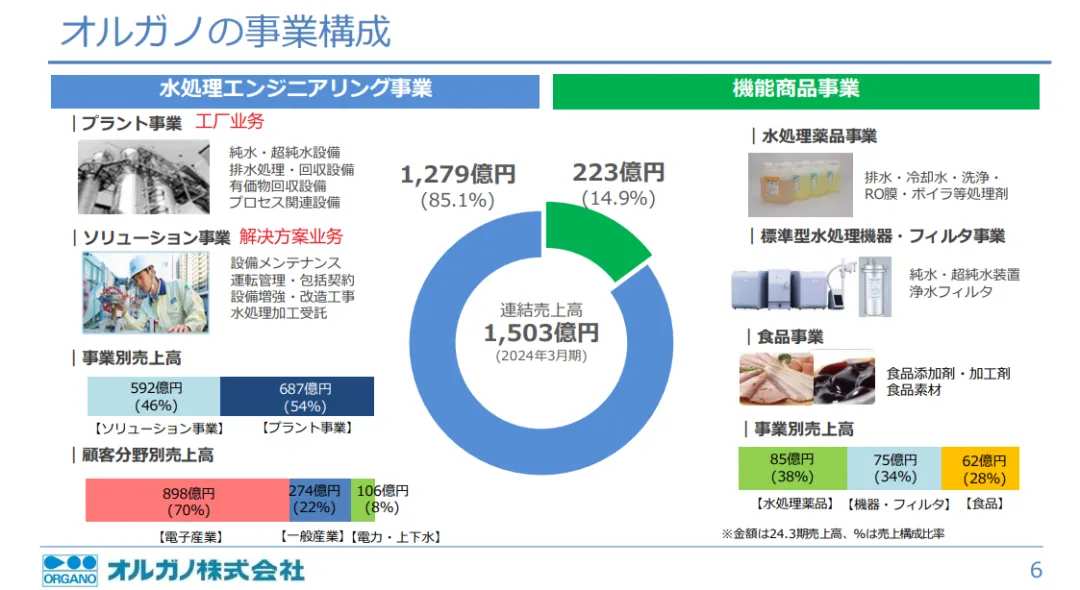

Almost every material involved in semiconductor manufacturing has been monopolized by Japanese companies for a long time, and ultra-pure water is no exception. The global market for ultra-pure water used in semiconductors is estimated to be around $1.692 billion in 2023. As a major participant in this market, $Kurita Water Industries (6370.JP)$Please use your Futubull account to access the feature.$Organo (6368.JP)$Please use your Futubull account to access the feature.$Nomura Micro Science (6254.JP)$ The market share of the top three Japanese companies alone accounts for 86% of the global market.

Organo Water Treatment is a comprehensive water treatment company with a history of more than 70 years, with a market share as high as 30% in the global semiconductor equipment water treatment field. In comparison with the other two companies, Organo also has the biggest advantage of deep cooperation with Taiwan Semiconductor.

In the year 2000, Ognuo Water Treatment became a supplier to Taiwan Semiconductor and established a subsidiary in Taiwan, China in 2005. Today, Ognuo Water Treatment is also producing ultrapure water for Taiwan Semiconductor's Japanese wafer fab. After Taiwan Semiconductor entered the US market, Ognuo Water Treatment also established a subsidiary in the United States.

Organo Water Treatment, which can accompany Taiwan Semiconductor wherever it goes, has its first competitive factor in its technological strength.

Organo Water Treatment was the world's first company to produce a 10nm particle measuring device. Its patent advantages in ultrapure water field also exceed those of its industry competitors. This technological strength has not only been favored by Taiwan Semiconductor, but also won the company the new factory project order in Hokkaido for Rapidus, a local outsourcing factory in Japan, in 2023.

In the semiconductor industry chain, the close relationship between Ognio Water Treatment and Taiwan Semiconductor has jointly promoted the research and development and production of key materials. Faced with the advance strategic deployment for the future AI trend, examples of strong collaboration in the semiconductor industry are not uncommon, essentially aiming to spread industrial value beyond the speed of other individual semiconductor companies, allowing them to lead in new technology and repeatedly win industry and historical positions.

The advantage of industry chain integration makes Ognio Water Treatment more resilient in the face of market fluctuations, maintaining a difficult-to-break position of ultra-pure water. This clear industry monopoly advantage and continuous technical strength that win the favor of major customers have caused Ognio Water Treatment's stock price to increase tenfold in 5 years.

However, the essence of the stock price increase still relies on performance. Taiwan Semiconductor, as a foundry factory, has seen its stock price rise more than many AI technology stocks, mainly due to hitting new highs in both performance and profits. Even with a partnership with NVIDIA, if it had the performance like Intel, its future would still be at risk.

Therefore, for Ognio Water Treatment, the relationship with Taiwan Semiconductor is not the only binding factor. More importantly, this relationship and its own business model have created high-profit certainty for the company. The tenfold increase in five years is based on solid value growth.

3. High Certainty of Equipment Companies

As an upstream supplier of semiconductor equipment and materials, Ognio Water Treatment has relatively lower overall operational risks. Being a water seller, as long as there are more gold diggers downstream, ultra-pure water will continue to be in high demand.

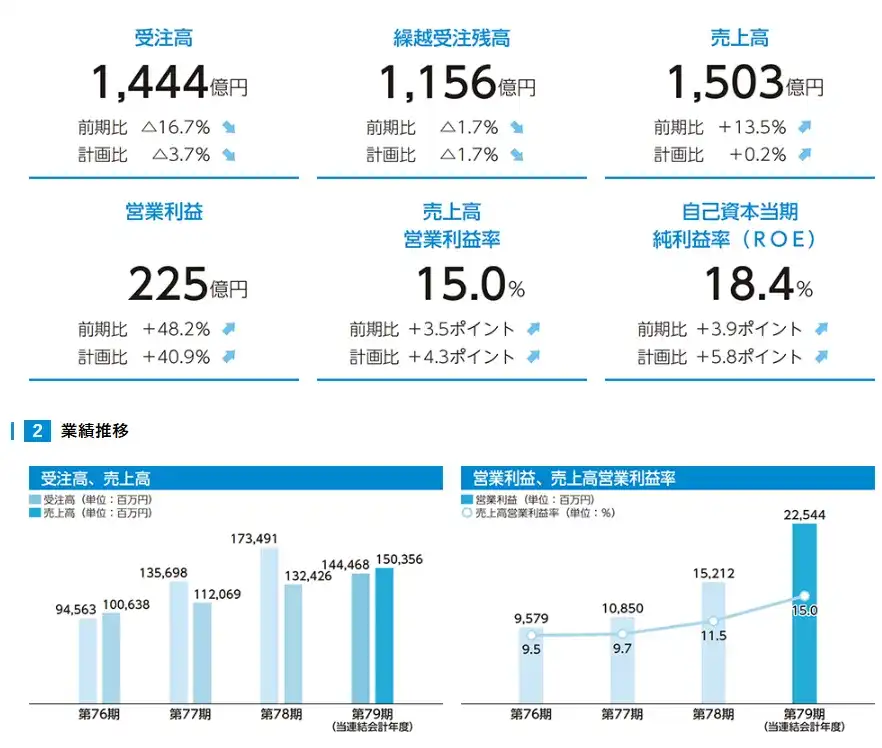

As the market related to generative AI expands, and new data center infrastructure emerges along with the recovery of the memory market, semiconductor-related capital expenditure and factory utilization rates remain high both domestically and internationally. Benefiting from this, Ognio Water Treatment's performance continues to shine. As of the first quarter of the 2025 fiscal year (April 1, 2024, to June 30, 2024), both sales, operating income, and quarterly profit have all achieved double-digit year-on-year growth.

In terms of segmentation, the water treatment engineering business is the largest source of revenue for Aqua Know. In terms of industries, 70% of the revenue in this business comes from the electronics industry (mainly semiconductors, which accounts for about 60% of the revenue from the semiconductor industry). In terms of service types, although the solution in the water treatment engineering business does not have the highest proportion, it has relatively higher profit contribution.

Because solutions belong to customized services and are often formulated in conjunction with the construction of new factories, Aqua Know's revenue from solution businesses has also seen a significant increase when major projects such as Taiwan Semiconductor's Japan factory have broken ground, leading to the company achieving historically high profit margins.

What is more critical is that Aqua Know's high-profit level in water treatment is sustainable.

The performance of equipment and material suppliers is closely related to order confirmation, and future performance and competitiveness can be roughly analyzed through existing orders. Aqua Know's current backlog of orders is 139.269 billion yen, although it has decreased, it is still sufficient as the sales foundation for the next fiscal year, supporting performance growth.

In addition, Taiwan Semiconductor's second Kumamoto factory is about to start construction, and Rapidus' 2nm pilot wafer factory is also planned to break ground in 2025. As the main supplier of ultra-pure water materials and equipment, Aqua Know still has the opportunity to continue receiving orders, and the company's historically high level of profitability can still be maintained.

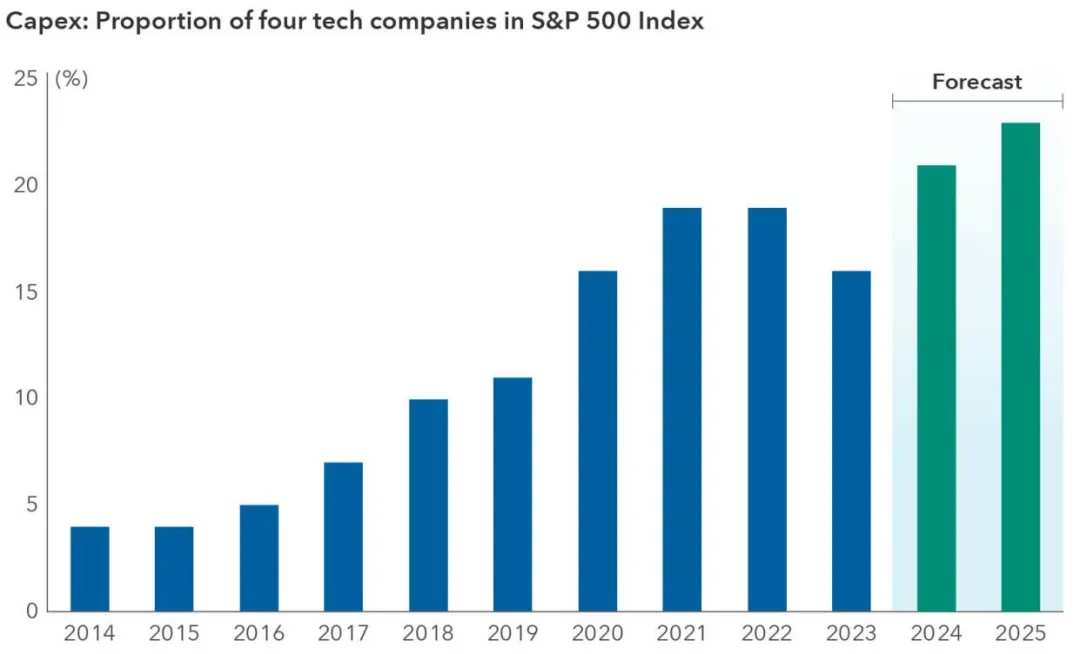

From a global perspective, the capital expenditure boom of downstream large technology companies has long overshadowed the cyclical nature of the semiconductor industry in the AI era. This also provides Aqua Know, which has already achieved international layout, with ample room for performance imagination.

Source: FactSet (As of May 1, 2024, data from Alphabet, Amazon, Meta, and Microsoft, as well as 2024 and 2025 forecast data based on analyst consensus)

Despite the negative factors such as Nvidia's revenue growth not meeting buyer expectations and the current commercialization of the AI industry being concentrated on infrastructure rather than consumer terminals, which has raised concerns about the sustainable development of the industry. But as mentioned at the beginning, equipment companies have higher certainty. Even if they are not profitable now, in the face of the fomo (Fear of missing out) sentiment, large technology companies still need to continuously increase capital expenditures, which further strengthens the demand for upstream equipment, and Aqua Know's water is still in high demand.

Conclusion

From demand, following the 'buddy' taiwan semiconductor, Aogano water treatment has seized the largest share in the growing ultra-pure water market; in terms of supply, the patent technology barriers established by Aogano water treatment have outperformed peers and expanded its customer base; and in terms of certainty, the hand orders, establishment of large-scale projects, and continuous expansion of capital expenditures by global tech giants have given Aogano water treatment, as an upstream 'water seller', high performance growth certainty.

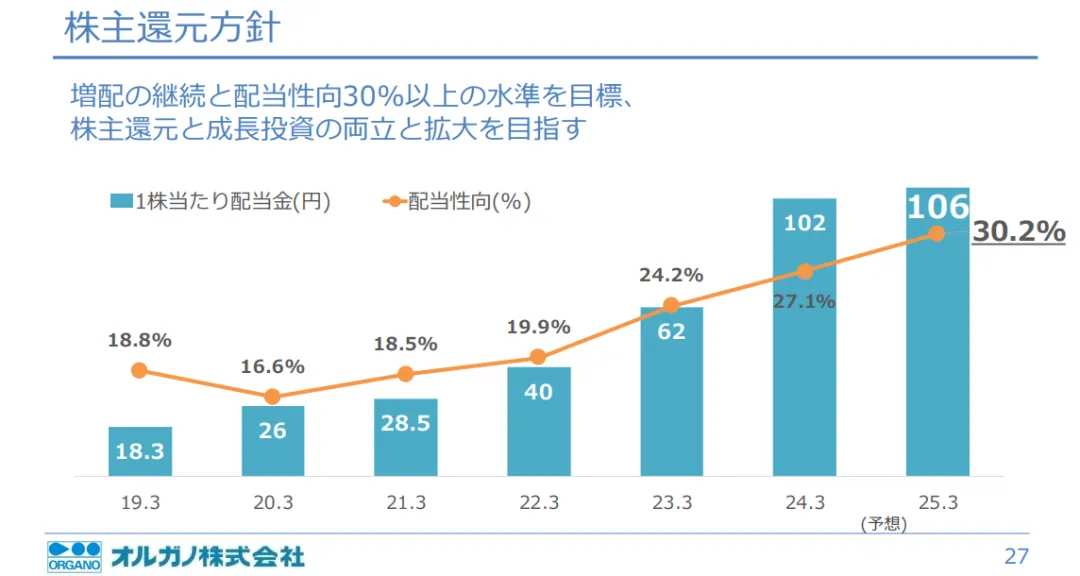

More importantly, this is a growth stock that cares about rewarding shareholders. On the basis of certain growth potential, the company is also constantly increasing its dividend payout ratio to enhance shareholder returns.

Aogano water treatment currently has a market cap of approximately $2 billion and is one of the components of the JPX-Nikkei mid-small cap index, an enterprise that has not been covered in a timely manner by analysts. Inflation stimulating economic growth will provide investors with higher alpha returns from these under-researched Japanese companies with profit growth potential.

Editor/Somer