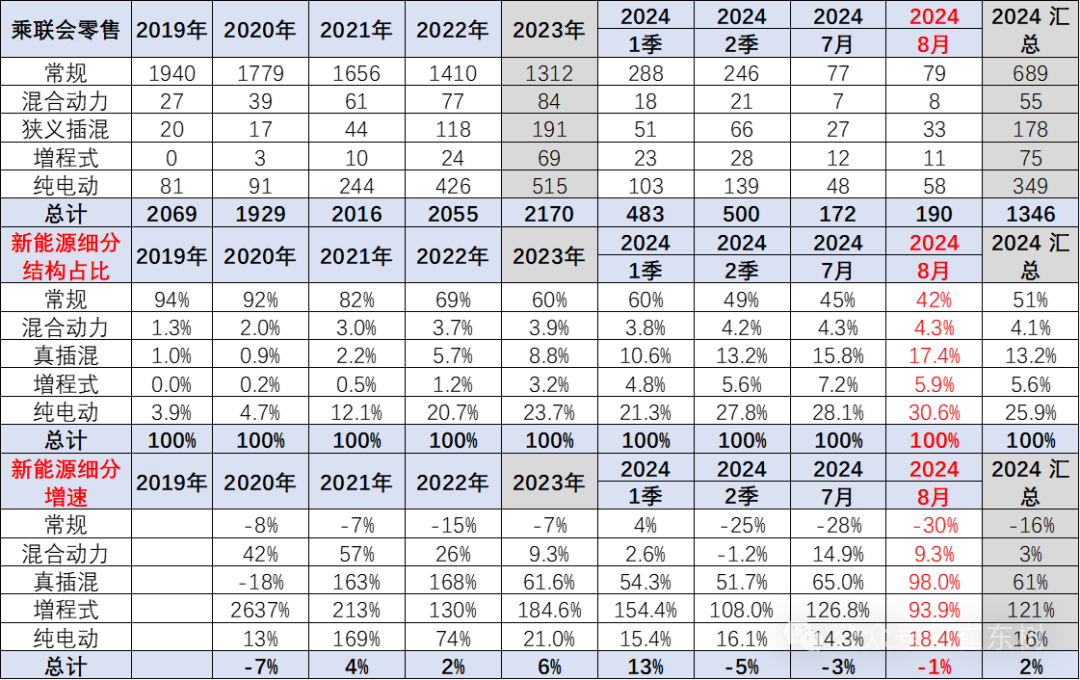

随着7月25日,国家发展改革委、财政部印发《关于加力支持大规模设备更新和消费品以旧换新的若干措施》,提高汽车报废更新补贴标准。此次新补贴标准提高至购买新能源乘用车补2万元、购买2.0升及以下排量燃油乘用车补1.5万元,由于报废更新的新能源较燃油车补贴有多5000元的优势,新能源车市场消费热情进一步被激发,其中入门级纯电动车与狭义插混市场强势增长。

随着7月25日,国家发展改革委、财政部印发《关于加力支持大规模设备更新和消费品以旧换新的若干措施》,提高汽车报废更新补贴标准。此次新补贴标准提高至购买新能源乘用车补2万元、购买2.0升及以下排量燃油乘用车补1.5万元,由于报废更新的新能源较燃油车补贴有多5000元的优势,新能源车市场消费热情进一步被激发,其中入门级纯电动车与狭义插混市场强势增长。According to the China Passenger Car Association data, the sales structure of passenger car market price segment in the country continues to rise, with a significant increase in the proportion of high-end models sales and a decrease in the proportion of mid-to-low-priced models sales.

Zhitong Finance APP learned that Cui Dongshu, Secretary-General of China Passenger Car Association, released an analysis of the price segment market structure of passenger cars in August. According to the data from the China Passenger Car Association, the sales structure of passenger car market price segment in the country continues to rise, with a significant increase in the proportion of high-end models sales and a decrease in the proportion of mid-to-low-priced models sales. This is driven by consumption upgrade and also due to the consumption upgrade of the replacement groups. There will be a further strengthening of the high-end characteristics of the car market consumption structure in 2024. After the Spring Festival in 2024, the passenger car market retail will temporarily decline, and the domestic gasoline car retail from June to August will drop significantly, suppressing the growth of the car market, and there will also be a decline in export contributions.

The above analysis points out that from a structural analysis perspective, the entry level has shrunk, and there are significant problems with the solid consumer base and insufficient purchasing power of mid-to-low-end consumers, and price wars have also erupted. The phenomenon of the upward trend in the price segment of traditional gasoline cars is not a favorable factor for promoting consumption. It is necessary for ordinary consumers to have stronger purchasing power to consume entry-level cars, that is, low-end consumption is very important. Therefore, it is important to improve the purchasing power of ordinary consumers, achieve relatively balanced car market price segments, stimulate entry-level consumption, and achieve consumption entry of first-time buyers.

With the release of the "Measures on Supporting Large-scale Equipment Renewal and the Replacement of Consumer Goods with New Ones" by the National Development and Reform Commission and the Ministry of Finance on July 25, the subsidy standard for the scrapping and renewal of automobiles has been increased. The new subsidy standard for the purchase of new energy passenger cars is now 0.02 million yuan, and for the purchase of 2.0 liters and below displacement fuel passenger cars is now 0.015 million yuan. Due to the 5,000 yuan advantage of the scrapping and renewal of new energy vehicles over fuel vehicles, the enthusiasm for consumption in the new energy vehicle market has been further stimulated, with a strong growth in entry-level pure electric vehicles and narrow-plug-in hybrid vehicles.

With the release of the "Measures on Supporting Large-scale Equipment Renewal and the Replacement of Consumer Goods with New Ones" by the National Development and Reform Commission and the Ministry of Finance on July 25, the subsidy standard for the scrapping and renewal of automobiles has been increased. The new subsidy standard for the purchase of new energy passenger cars is now 0.02 million yuan, and for the purchase of 2.0 liters and below displacement fuel passenger cars is now 0.015 million yuan. Due to the 5,000 yuan advantage of the scrapping and renewal of new energy vehicles over fuel vehicles, the enthusiasm for consumption in the new energy vehicle market has been further stimulated, with a strong growth in entry-level pure electric vehicles and narrow-plug-in hybrid vehicles.

From the monitoring of overseas market retail data exported by domestic brands, the proportion of A0-class electric vehicles was once close to 50%, making them the absolute main force of exports. Domestic brands such as SAIC performed well with small electric vehicles in Europe, which led to relatively targeted tax increase measures. This also reflects that small and micro electric vehicles are the core of the world electric vehicle competition. We urgently need to guide the financial and tax policies for the miniaturization of electric vehicles and encourage the development of small and micro electric vehicles in order to make Chinese electric vehicles sustainable worldwide. As a category of fuel vehicles corresponding to pure electric zero-emission vehicles, plug-in hybrid vehicles have become increasingly prominent in replacing fuel vehicles in overseas markets due to the advantages of low fuel consumption and long range.

1. The price of passenger cars becomes more expensive as the price drops.

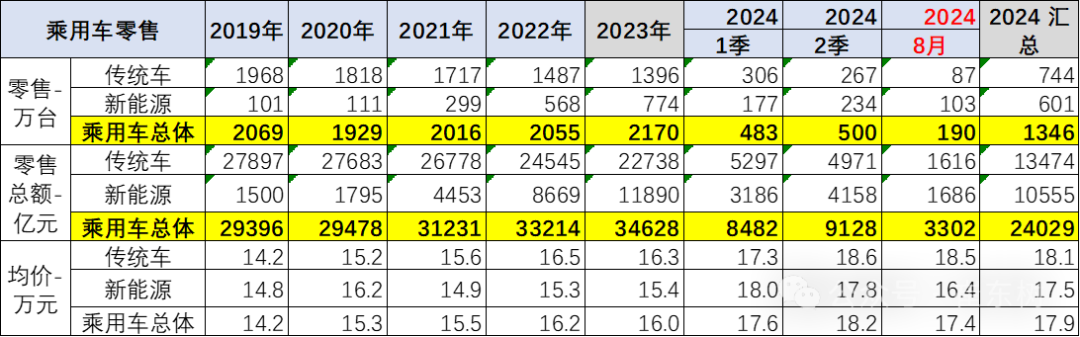

In recent years, the prices of cars have been continuously rising. It was 1.42 million yuan in 2019, 1.53 million yuan in 2020, the average price so far this year is 1.79 million yuan, and it is 1.74 million yuan in August.

The main reason for the rising prices of passenger cars in recent years is the high prices of hybrid and extended-range vehicles, combined with the high-endization of fuel vehicles, which together form a structural driving force. At the same time, the average sales price of existing fuel vehicles has also increased, and the high-endization of fuel vehicles has led to a significant price increase. However, the scrapping and renewal subsidies in August have promoted the increase in the purchase of entry-level cars, leading to an increase in the proportion of sales of entry-level electric vehicles and plug-in hybrids, resulting in a decrease in the average price.

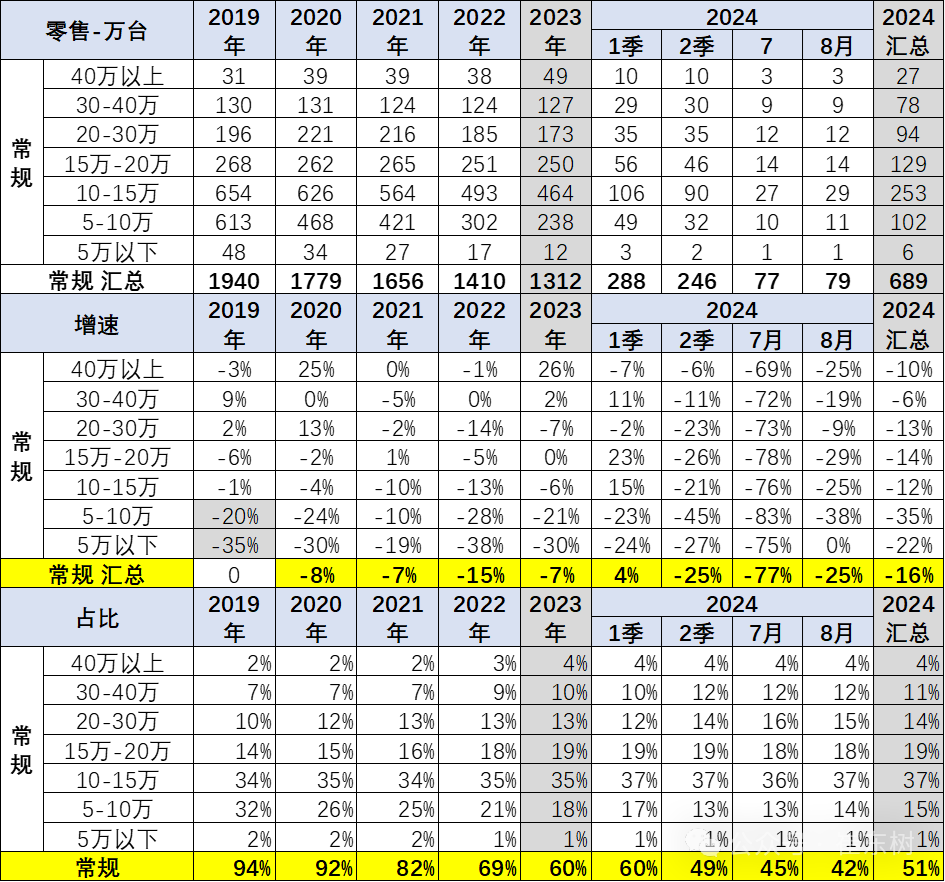

2. Sales structure of passenger vehicle market by price segment.

According to the retail data of the China Passenger Car Association, the trend of the price structure of the national urban market is continuously rising, with a significant increase in the sales of high-end new energy vehicle models and a decrease in the sales of mid-to-low-priced vehicle models.

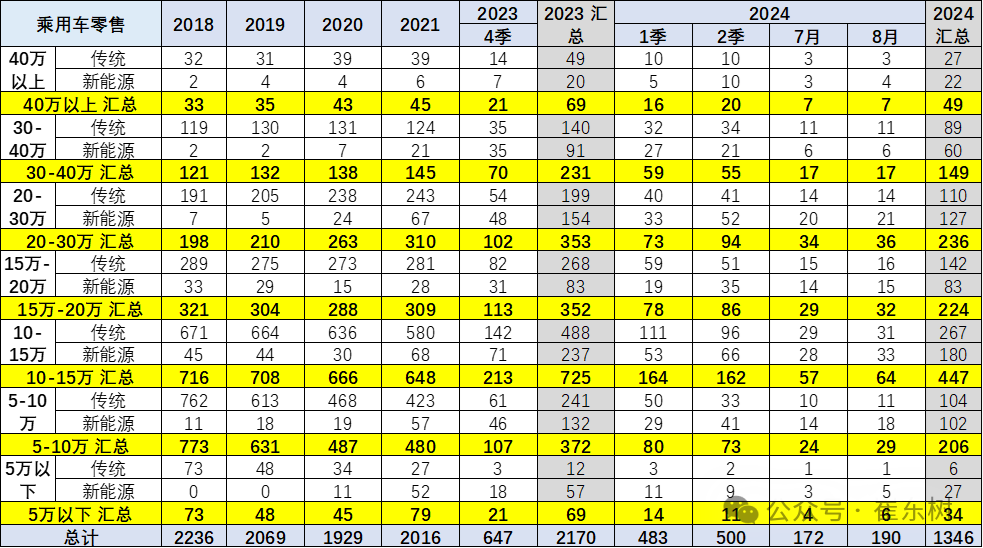

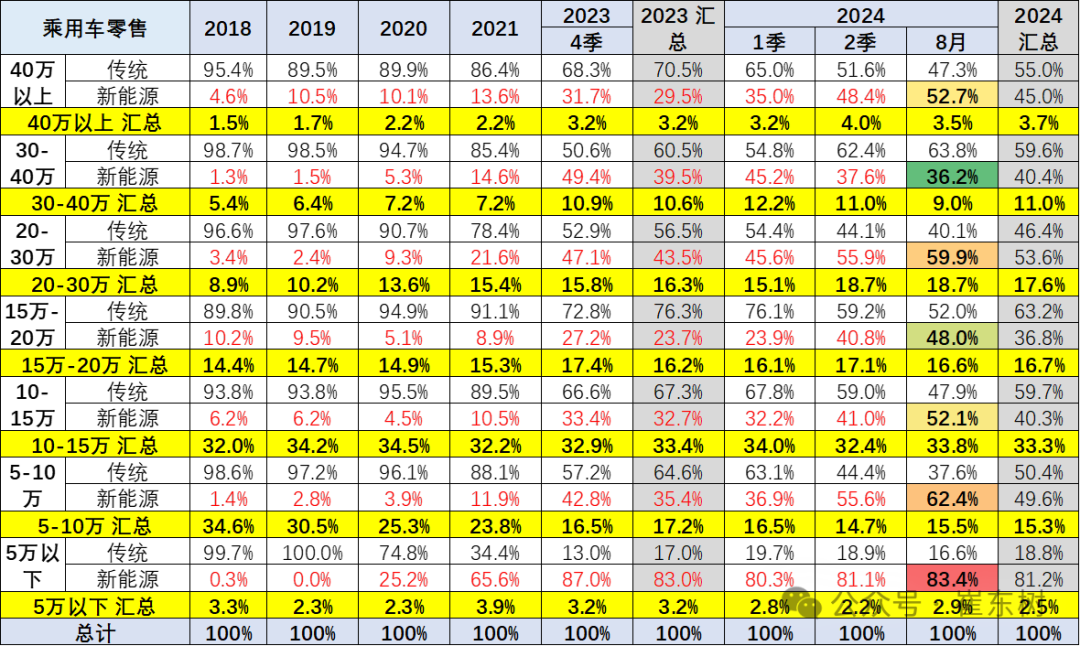

The proportion of models below 0.05 million yuan in 2021-2022 has continued to rise compared to 2020, mainly due to the sales contribution of micro electric vehicles. However, since 2023, it has continued to decline. The sales proportion of models below 0.05 million yuan in 2024 is currently only 2.5%, a decrease of 0.7 percentage points compared to 2023, but it increased to 2.9% in August. After the decline in sales of traditional models between 0.05-0.15 million and the growth of new energy vehicles offset each other, the overall downward trend is still significant.

The market share of models above 0.15 million yuan continues to rise, with rapid growth. The market share of models between 0.2-0.3 million in 2023 domestic retail was 16.3%, and it was 18.7% in August this year. In recent years, the market share of various segments of models above 0.3 million yuan has continued to rise. The retail market share of models between 0.3-0.4 million in 2023 was 10.6%, and in August it was 9%. The domestic retail market share of models above 0.4 million yuan in 2023 was 3.2%, and this year's August was 3.5%. The breakthrough in independent high-end development reflects the obvious trend of high-end development brought by the growth of new energy vehicles in the passenger vehicle market.

3. Sales structure of passenger vehicle market by level.

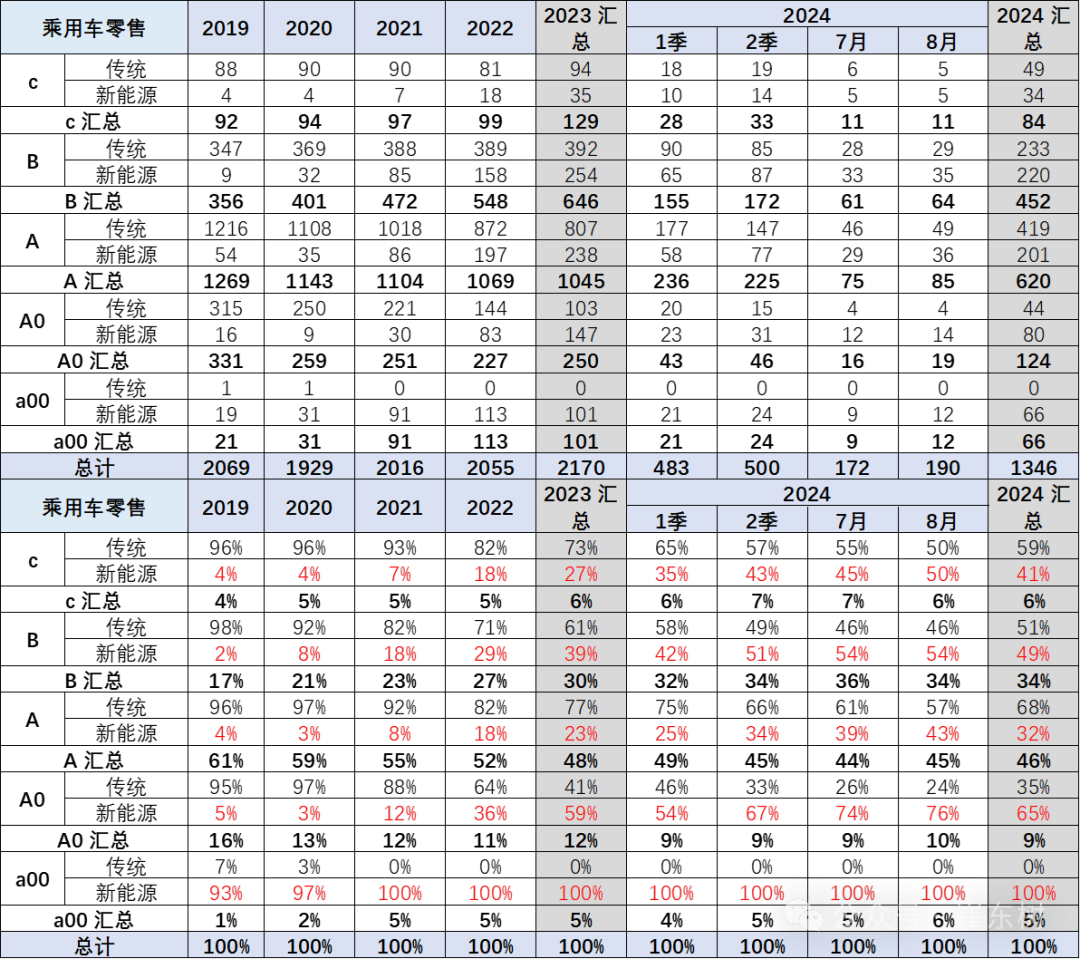

In recent months, small cars have the highest penetration rate of new energy vehicles, with a penetration rate of 100% in August, and A0-level small cars have exceeded 70%. The improvement of new energy vehicles in the A-level segment is rapid.

The penetration rate of B-class and C-class vehicles has increased significantly, reflecting the significant advantages of high-end electrification.

The increase in the penetration rate of new energy in high-end vehicles mainly reflects the trend of autonomous improvement.

4. The structure of new energy vehicles for passenger vehicles

Pure electric new energy vehicles have maintained high retail growth domestically, while plug-in hybrids have performed outstandingly in the past three years with continued slight growth in range. Sales of traditional passenger vehicles have faced continuous downward pressure.

In 2023, the proportion of new energy vehicles reached a strong ratio of 36%, and the penetration rate of new energy vehicles in August 2024 was 54%. The contribution of new energy vehicles in the future will continue to increase slightly.

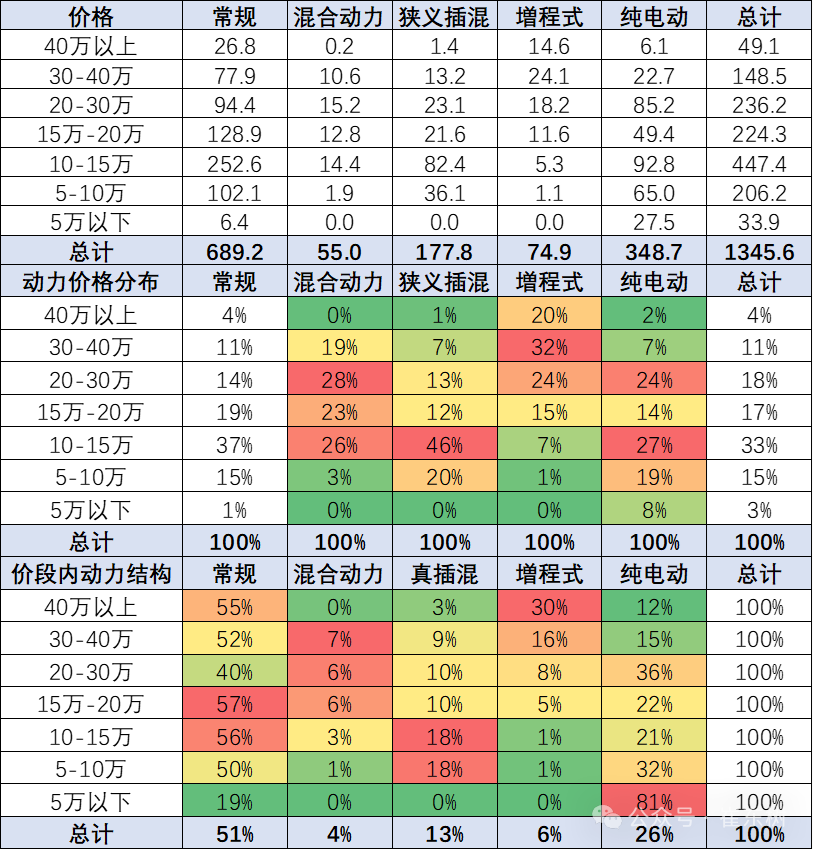

5. Price and sales structure of various types of power in 2024

Currently, the price range of 0.05-0.15 million yuan for passenger vehicles nationwide is a characteristic of the core mainstream market, primarily driven by high proportions of traditional gasoline vehicles. There are significant differences between traditional vehicles and new energy vehicles, while mid-range plug-in hybrids have a relatively concentrated structure.

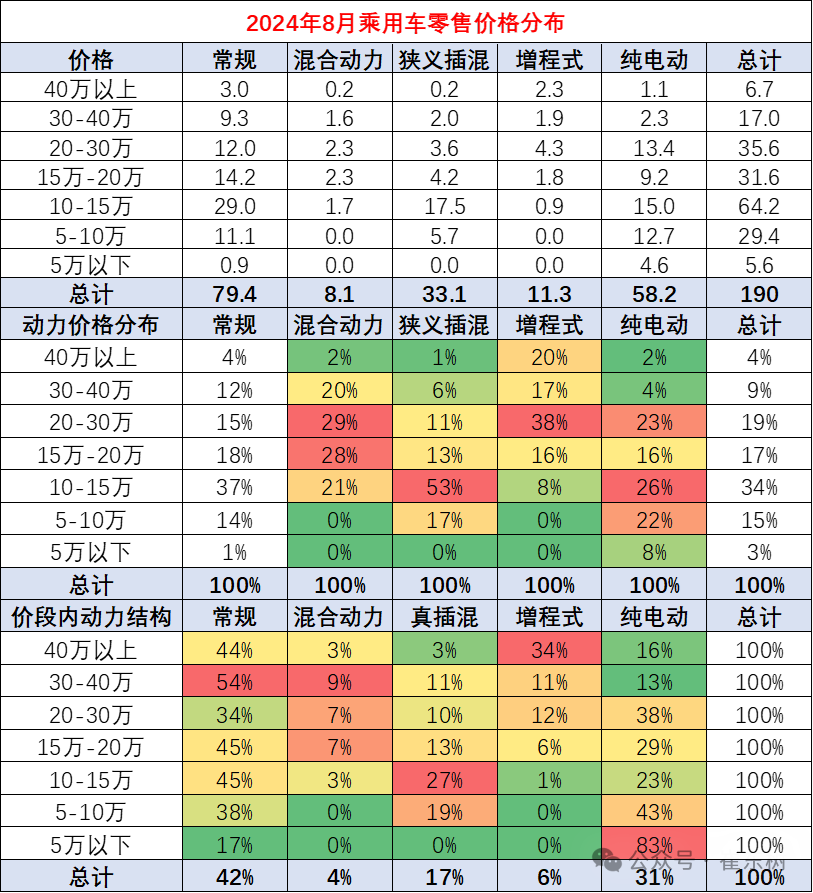

6. Sales structure of internal power for various price segments in August 2024

In the price segment market, power distribution is relatively uneven. Pure electric vehicles perform the strongest in the under-0.05 million yuan market, while extended-range electric vehicles show the strongest distribution pattern in the high-end market price range, and hybrid vehicles have a relatively strong performance in the 0.2-0.3 million yuan range.

Traditional fuel vehicles have shown relatively strong performance in the range of 0.1-0.15 million yuan, forming a differentiated distribution. Especially, the distribution of hybrid vehicles is relatively narrow, with products mainly in the mid-to-high price range. At the beginning of the year, the low-end market contracted severely, which also had a greater impact on the low-end market due to weaker consumption.

7. Conventional fuel passenger vehicle structure.

The high-end trend of traditional fuel vehicle product structure is more obvious, mainly the high growth of models above 0.15 million yuan, which is a direct reflection of consumption upgrade. The decline rate of fuel vehicles below 0.1 million yuan is very fast, and they have formed a feature of sharp decline under the high growth of pure electric vehicles.

8. Changes in the product structure of pure electric vehicles - significant growth in high-end segment.

With the decrease in cost and product improvement, the micro electric vehicles below 0.05 million are growing rapidly, while the electric vehicles priced between 0.15-0.3 million yuan are performing well. Among them, Tesla still ranks above 0.2 million yuan to prevent excessive structural fluctuations.

Currently, the proportion of electric vehicles priced between 0.1-0.15 million yuan is decreasing, and some electric vehicles are used for ride-hailing services. The market trend for A-class electric vehicles in the past two years has not been strong. With the decline in the price of lithium carbonate, there is still great potential for the growth of new energy vehicles priced below 0.1 million yuan.

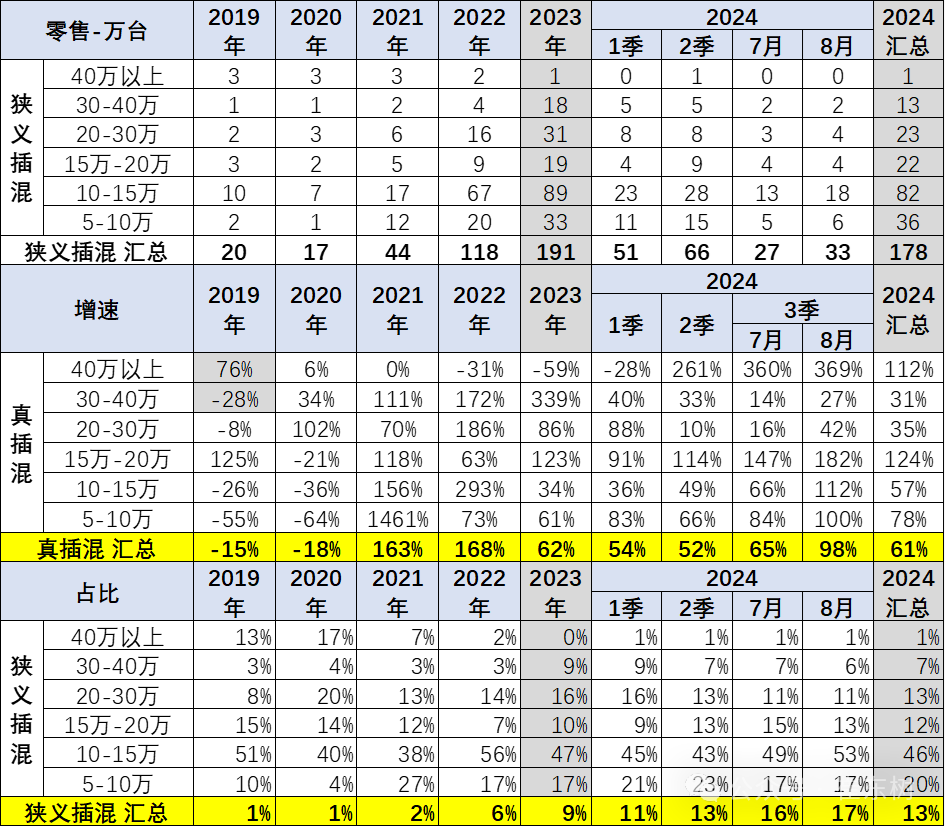

9. Changes in the product structure of plug-in hybrid vehicles - significant increase in the mid-to-high-end segment.

The incremental growth of plug-in hybrid models mainly occurs in the low price range. After the independent plug-in hybrid technology has matured, it has already gained a large market share in the mid-to-low price range.

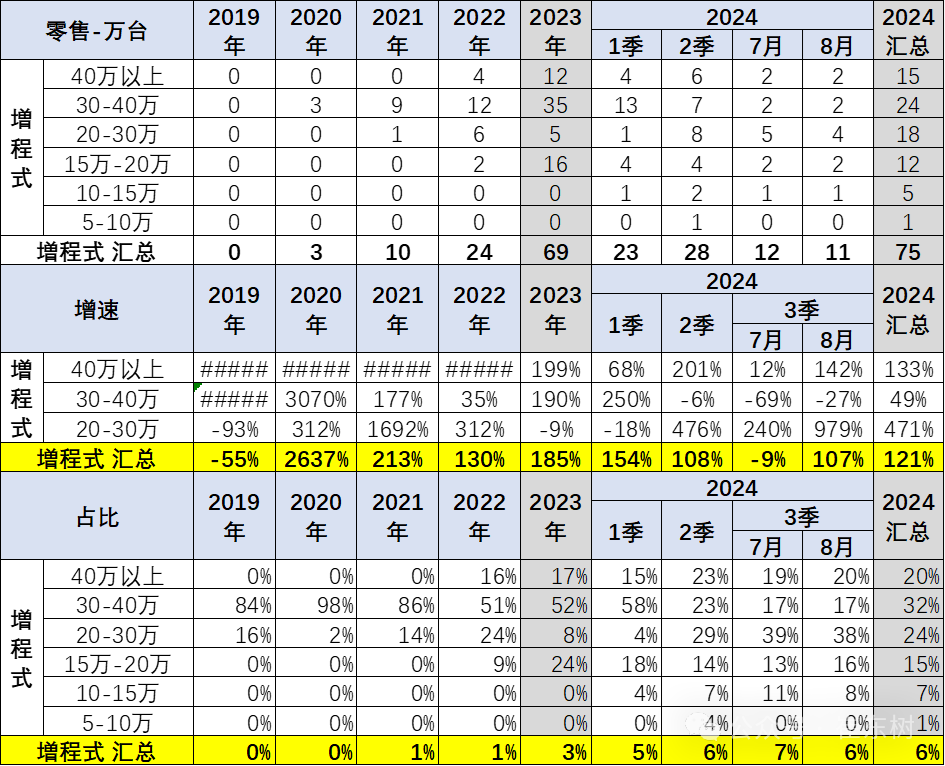

10. Changes in the product structure of extended-range vehicles - strong performance in the high-end segment.

As a branch of pure electric vehicles, extended-range electric vehicles have been included in plug-in hybrids. At present, they continue to show strong performance in the high-end and 150,000-yuan level products.

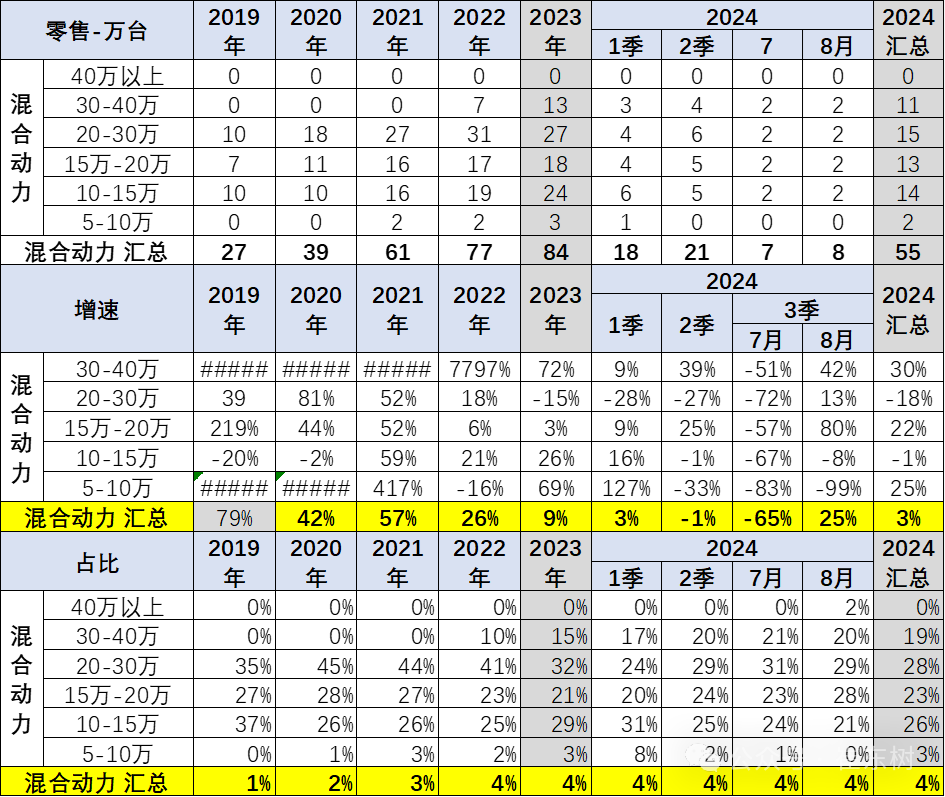

11. Changes in market share of regular hybrid products - high-end segment.

The market share of hybrid vehicles is also continuously increasing. The improvement of supply in 2024 has led to a gradual increase in market share. The market demand under policy drive is shifting towards plug-in hybrids, and the market performance of hybrids is generally average.

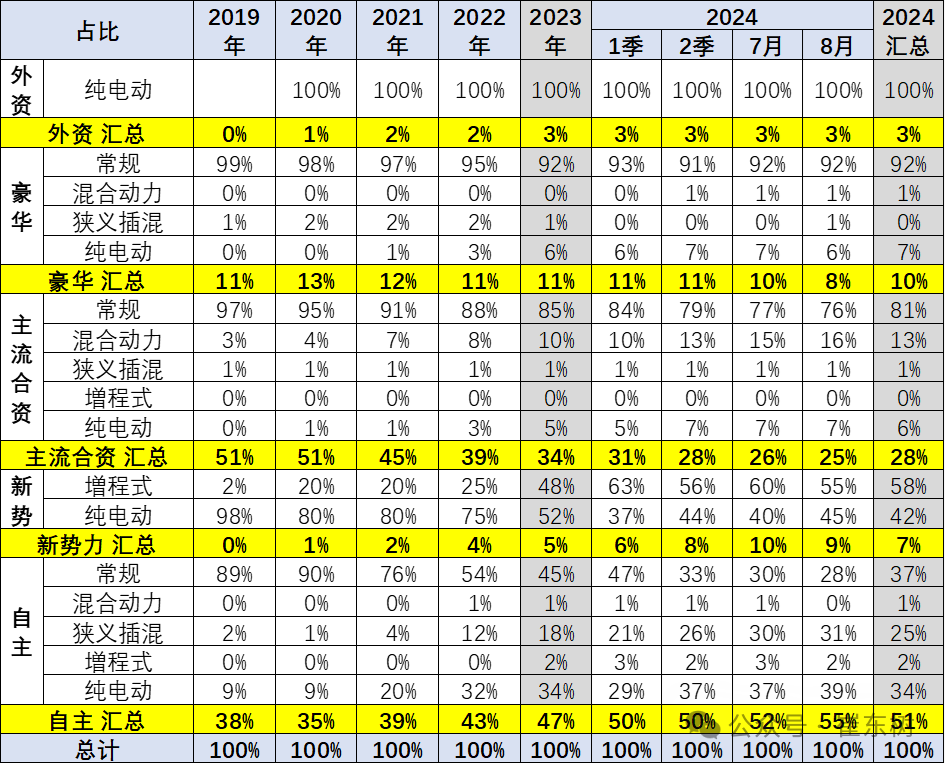

12. Changes in market share of various automakers' products.

In 2024, domestic brands have performed well, and new energy has made comprehensive efforts. Both extended-range and plug-in hybrids have performed well. Overall, the advantages of new energy are more prominent in the high-end oil-electric hybrids brought by independent innovative technology. The structural fluctuation of new forces is greater, and extended-range vehicles perform better.