Cui Dongshu wrote that after the traditional fuel vehicle market share declined due to the impact of new energy vehicles, the seasonal pace of the NEV market weakened due to the decline in the number of first-time buyers, changes in the number of car buyers, and changes in new energy channels, and the characteristics of “not weak in the off-season” were indeed becoming more and more obvious.

The Zhitong Finance App learned that Cui Dongshu published an article saying that after the traditional fuel vehicle market share declined due to the impact of new energy vehicles, the seasonal pace of the NEV market weakened due to the decline in the number of first-time buyers, changes in the number of car buyers, and changes in new energy channels, and the characteristics of “not weak in the off-season” are indeed becoming more and more obvious.

The retail sprint in July of this year was moderate. There were no excessive overdrafts for August. Coupled with the increase in new energy subsidies for scrap renewal to 0.02 million yuan, the penetration rate of new energy sources reached 54% in August. On July 25, the National Development and Reform Commission and the Ministry of Finance issued “Certain Measures to Strengthen Support for Large-scale Equipment Renewal and Consumer Goods Trade-in” to raise the automobile scrapping and renewal subsidy standards.

This time, the new subsidy standard has been raised to 0.02 million yuan for the purchase of new energy passenger vehicles and 0.015 million yuan for the purchase of fuel fuel passenger vehicles with a displacement of 2.0 liters or less. Due to the advantage of scrapped and renewed NEVs with 5,000 yuan more subsidies than fuel vehicles, consumer enthusiasm in the NEV market has been further stimulated. Among them, entry-level pure electric vehicles and the mixed market in the narrow sense are growing strongly.

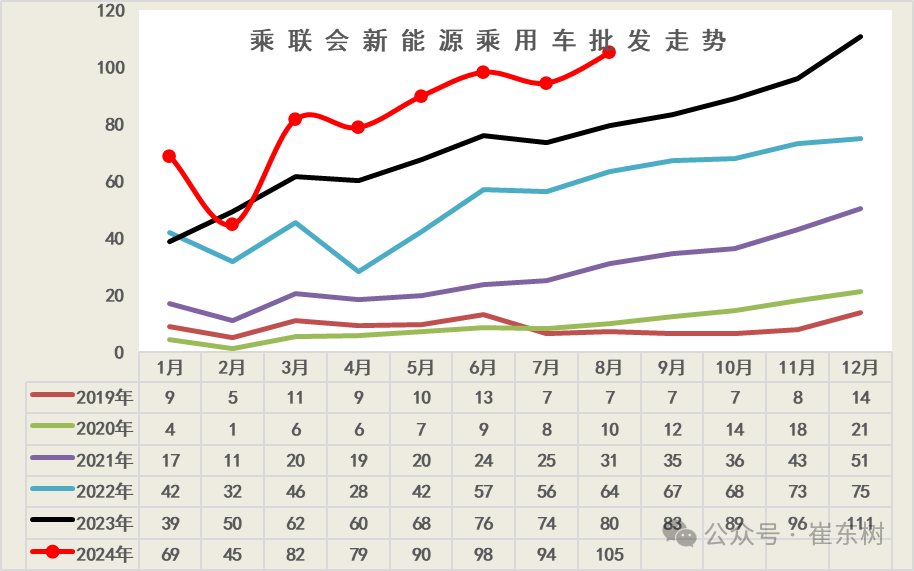

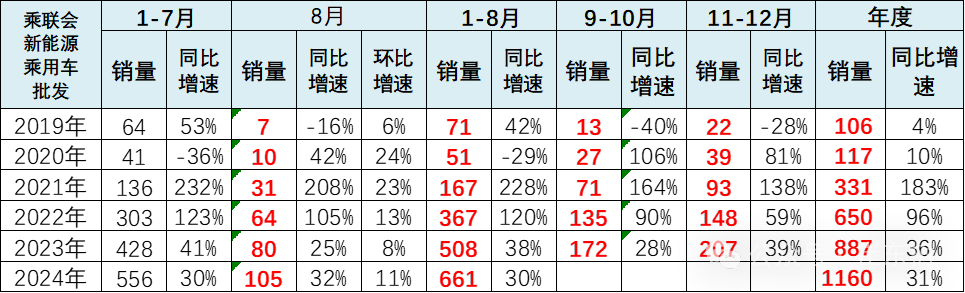

In August 2024, wholesale sales of new energy passenger vehicles reached 1.05 million units, surpassing the highest level in history. Due to the Spring Festival factor and price reduction disruptions, there was a big decline in February. The market gradually resumed growth in March-July, and there was a huge month-on-month increase in August.

Since 2023, there has been a downward trend in power battery prices due to the decline in raw materials such as lithium and nickel. Lower sales in February will help companies cut production at the beginning of the year, remove historical inventory, and achieve a continuous increase in sales of new products.

Wholesale sales of new energy passenger vehicles reached 1.05 million units in August, and the year-on-year growth rate rebounded to 32%. Compared with the 30% growth rate in January-July, this is a strong increase. Overall, the increase was relatively rapid in January-August. Wholesale growth in August was still relatively low compared to retail sales, reflecting the market-driving effect.

In August, the wholesale penetration rate of NEV manufacturers was 48.9%, up 13.3 percentage points from the 35.6% penetration rate in August 2023.

In August, the penetration rate of own-brand NEVs was 63%; the penetration rate of NEVs among luxury cars was 43.2%; while the penetration rate of NEVs of mainstream joint venture brands was only 7.8%.

In August, wholesale sales of traditional car manufacturers fell 24% year on year, while new energy vehicles rose 32% year on year. The growth rate gap was 56 points, and the pressure on fuel vehicles was high.

The NEV market retailed 1.03 million vehicles in August 2024, showing unusual characteristics of August being stronger than July. Overall, retail sales continued to strengthen.

Due to the release in Beijing, the effects of the release of new demand in June-August were obvious, and some wait-and-see groups began to buy cars, and the scrapping renewal increased the enthusiasm for buying.

In 2023, the cumulative retail sales volume was 7.75 million vehicles, up 36% year over year. The 43% growth rate in August of this year was excellent. From January to August 2024, the retail sales of new energy vehicles was 6.01 million units, a relatively strong trend of 35%, close to the 36% growth rate in 2023. This is a very good performance.

In August, the domestic retail penetration rate of new energy vehicles was 54%, up 16.7 percentage points from 37.3% in the same period last year.

In domestic retail sales in August, the penetration rate of new energy vehicles among independent brands was 75.9%; the penetration rate of new energy vehicles among luxury cars was 33.5%; while the penetration rate of new energy vehicles in mainstream joint venture brands was only 8%.

In August, retail sales of traditional vehicles fell 28% year on year, while retail sales of new energy vehicles rose 43% year on year, with a difference of 71 points. The fuel vehicle tax burden was high, and the pressure was high.

Reasons why the new energy penetration rate of domestic passenger vehicles continues to exceed 50%: 1. Empowered by the industrial chain advantages brought by the continuous strength of the Chinese manufacturing industry, batteries, motors, chips, etc. in the equipment manufacturing industry and parts industries have excellent advantages; 2. Driven by new quality productivity, Chinese car companies are making every effort to develop new energy vehicles, driving the transformation of Chinese automobiles from big to strong; 3. The guiding idea of open development of the passenger car industry has promoted the full entry of Internet companies, smart consumer manufacturers, and international NEV companies, etc.; 4. The innovative development of hybrid technology in the Chinese car industry has enabled the innovative development of hybrid technology to achieve Technological breakthroughs in the narrow sense of plug-in hybrid and expansion have enriched the technological lines of the world's new energy development, and obtained a breakthrough advantage of China's plug-in hybrid market with 78% of the world's plug-in hybrid market; in May and August, the country strengthened the passenger car scrapping and renewal policy, which was 0.005 million yuan higher than conventional fuel vehicle subsidies, further helping the development of new energy vehicles; combined measures promoted the penetration rate of new energy vehicles in the off-season car market in July-August to reach a new level; this phenomenon is worth paying attention to.

In August 2024, exports of new energy vehicles amounted to 0.099 million units, which showed a slight month-on-month increase. The slump in exports in January-February should have been affected by factors such as shipping. Autonomous exports increased significantly in March, and exports from some autonomous car companies faced a weakening in demand from Europe in April-August and were actively adjusted.

New energy product brands made in China are increasingly going abroad. Due to the continuous increase in overseas recognition and the improvement of service networks, own-brand pure electric motors are mainly aimed at developed markets. Currently, there is a phenomenon of blocking China's new energy. This is completely wrong, but we also need to face it calmly.

From January to August 2024, a total of 0.78 million units were exported, an increase of 20% over the previous year. Judging from recent retail data monitoring for independent exports to overseas markets, the performance of independent brands in Europe is average. In some overseas regions, in addition to the impressive performance of traditional car exporters, exports from new forces have also been gradually launched recently. Overseas markets have also begun to show data. The export performance of South America and the like is also constantly improving, and exports of autonomous plug-in hybrid models have begun to grow. The high export base in August 2023 had little impact on exports. The impact of tariffs imposed by the EU is gradually fading, and NEV exports are expected to grow at a high rate over the next few months.

In August, retail sales of pure electric vehicles were 0.582 million units, up 18% year on year, up 21% month on month; in August, the narrow range plug-in sales volume was 0.331 million units, up 98% year on year, up 22% month on month; in August extended range retail sales were 0.113 million units, up 94% year on year, down 9% month on month. The year-on-year and month-on-month growth rate was weaker than the pure plug-in hybrid trend.

In the new energy retail structure in August: 57% pure electric, 32% mixed in the narrow sense, and 11% growth rate. In the new energy retail structure in August 2023, 69% is pure electric, 23% is mixed in the narrow sense, and 8% is incremental. In the new energy wholesale structure for the whole of 2023:67% pure electric, 25% mixed in the narrow sense, and 9% increase in range. The range extension effectively compensates for the battery life anxiety of pure electric power, and should belong to the pure electric branch.

Sales of electric vehicles at various levels were divided in August, and the trend of consumption upgrading was very good. Demand for small electric vehicles is weak, and household demand for a second car is average. High-end SUVs represented by Xiaomi are growing strongly.

Due to the end of the tax exemption policy for mini electric vehicles below 200 kilometers at the end of May, it brought about a sharp contraction of more than 20,000 short-range electric vehicles in June-July, leading to a slump in the pure electric market in July, and the pure electric economy market gradually recovered in August, driven by the scrapping and renewal policy. End-of-life renewal subsidies drive the demand for plug-in hybrid models to further divert fuel vehicle demand.

Judging from the monthly domestic retail share, the Pure Electric Autonomous Plus Company performed well in August. The market size of major joint ventures plus traditional luxury cars is far lower than Tesla.

Newcomer car companies such as NIO (09866), Nana, Ideal (02015), and Zero Run (09863) are still generally strong in terms of year-on-year and month-on-month sales performance. In particular, NIO and Ideal have strong performance. This is also an advantage of the market segmentation circuit.

Independent brands have a big advantage in the pure electric market, and Tesla is the main high-end. Recently, mixed autonomy has increasingly taken a dominant advantage, and the growth process has become independent and exclusive to new forces.

In terms of product launch, the market base continues to expand as autonomous vehicle companies combine multiple lines on the new energy route, and the monthly wholesale sales volume of NEV manufacturers has reached 17 manufacturers with monthly wholesale sales exceeding 10,000 vehicles. The number of manufacturers with monthly wholesale sales of NEVs reached 19 (up 4 year-on-year and 2 month-on-month), accounting for 90.7% of total NEV passenger vehicles (89.5% last month and 86.9% in the same period last year).

Independent companies occupy an absolute dominant position, but some car companies are also under continuous pressure to decline in cumulative sales.

The main NEV car companies have not changed much this year from last year. The top two car companies have not changed, but Geely and Tesla are getting closer, and the pure electric performance of the month-on-month trend is strong. Among them, BYD (01211) 37,854, Tesla China 86697, Geely (00175) 75,484, Changan, 49,398, Ideal, 48,122, Chery, 4,074, SAIC-GM-Wuling, 41,514, Celis 35741, GAC Aian 31,772, Zero Sports, 28005, Great Wall Motor 24,769, Dongfeng 23571, NIO 2017, 1403636, SAIC Volkswagen 10135, FAW Hongqi 13,229 vehicles, Volvo Asia Pacific 10,429 vehicles, Jihu 10001 vehicles.

In August, 16 passenger car wholesale sales exceeded 20,000 units (15 last month), ModelY: 56,309 units, BYD Song: 5,3786 units, Seagull: 40949 units, SEAL 06:40015 units, Qin L: 40011 units, BYD Qin: 30446 units, MODEL3:30388 units, BYD Yuan: 30061 units, Lavida: 26186 units, Ruihu 8:25821 units, Boyue: 25622 units, .Ideal L6:24897 units, Song 700 L: 2300 Taiwan, Xingyue: 22,376 units, Sagitar : 21251 units, Tiggo 7:21005 units Among them, NEV ranked in the top 8 overall passenger car sales (top 10 last month), and the domestic performance of major fuel vehicle models such as the Lavida improved.

In recent years, the pure electric passenger car market is still dominated by BYD, Tesla (TSLA.US), and traditional independent brands, but recent joint venture performance has improved markedly. In August 2024, the NEV passenger vehicle market diversified and the NEV performance of large groups was divided. The strong performers of pure electric vehicle companies in August 2024 include BYD, Tesla, Geely, Wuling, and Changan. Joint venture electric vehicle companies are weak.

The overall trend of the new forces is divided. Zero Run, etc. are strong, while the overall performance of some of the new pure electric forces is average.

The relatively strong performance of pure electric models in August 2024 was products such as Tesla MODELY, Seagull, MODEL3, and BYD Yuan.

The BYD Seagull micro electric vehicle is extremely powerful and also meets entry requirements. Although the trend of the Wuling Hongguang Mini was weak in the early stages, the Hongguang Mini has improved markedly recently, and new products such as the mini electric car Seagull have performed well.

The plug-in hybrid market trend was divided in August 2024. The main manufacturer was BYD in the absolute lead. Due to high sales volume, BYD followed up with BYD's development mix with Geely Automobile, Great Wall Motor, Changan Automobile, SAIC-GM-Wuling, etc., and BYD actively followed suit after the price reduction. Recently, Geely and Great Wall's new hybrid products are very competitive.

The mixed market performance of joint ventures is relatively weak. Due to differences in the industrial chain, some joint ventures for plug-in hybrid models performed relatively well. Recently, European mixers have been weak, and luxury car mixes are not strong.

Plug-in hybrid models reflect the characteristics of traditional domestic enterprises. Recently, sales of BYD Song, BYD Qin, and Destroyer 05 have been good. BYD's product matrix is rich, and the trend coverage is relatively large. European and American companies don't pay enough attention to the luxury mix market, and the sales trend is relatively stable. Recently, pure electric and plug-in hybrid export models have performed well in the European market. There are many exports such as the BYD Seal, etc., which has given a slight boost to the European new energy market in China.

Extended range NEV companies have performed very well recently, and some car companies such as Ideal and Celis have shown phased explosive growth characteristics. This year's ideal growth performance was very good, but August was temporarily weak. Range extension products such as Changan Automobile and Zero Run continued to grow rapidly.

Gincon Celis's strong growth performance has recently become a dark horse. Ideal cars drive increased range growth, and actual users' demand is still a pure electric model.

Ideal L6, the main model in August 2024, continues to be the leading model, and the M9 is also trending very well. Competition in the main model market is gradually intensifying. Models with monthly sales of more than 10,000 units already have full competition, and the Changan series is growing very well.

The extended range electric vehicle Ideal L6 became the leading model. The performance of the Ideal L9 gradually slowed down, and the sales structure shifted to the L7. It shows that consumers still have good acceptance of the low-end growth range, and the cost performance advantage of the extension is still very important. Recently, Changan Deep Blue's range has been extended, and Qiyuan's pure electric power has also begun to be launched, forming different characteristics.