① What are Meituan's second-quarter results? ② How does the agency view Meituan's subsequent performance?

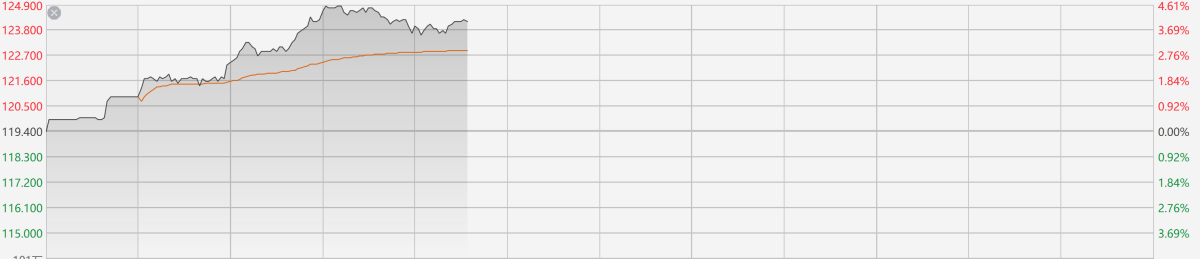

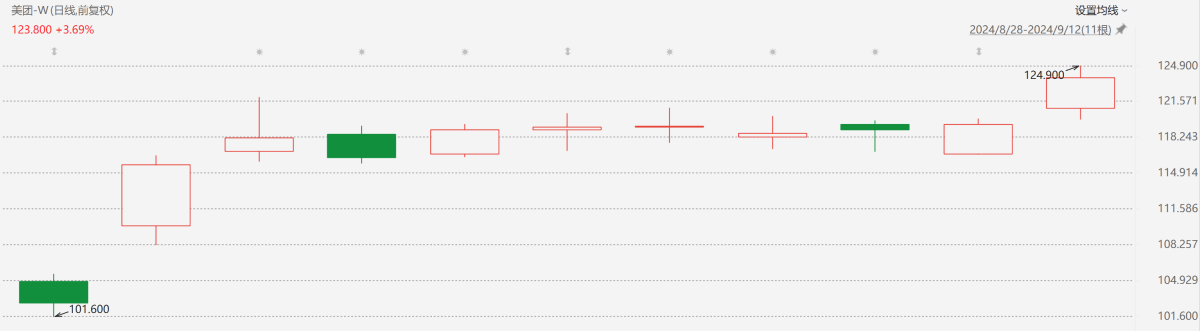

Financial Services Association, September 12 (Editor Hu Jiarong) Meituan-W (03690.HK) has continued to strengthen recently. Since announcing the second-quarter results on August 28, the company's stock price has increased by more than 16% cumulatively. As of press release, it rose 4.10% to HK$124.3.

Note: Meituan's performance

In terms of news, Meituan announced its results for the second quarter of this year on August 28, with revenue of 82.3 billion yuan, an increase of 21% over the previous year; quarterly revenue of core local businesses reached 60.7 billion yuan; the number of annual active users and merchants reached a record high, and the number of orders delivered instantly reached 6.2 billion yuan.

Notably, after Meituan released its second-quarter results, its stock price fluctuated and strengthened. The cumulative increase was 12.43% from September 29th to September 11th. If current performance is taken into account, this increase increased to 16.53%.

Note: Meituan's performance since August 29th

The agency is optimistic about Meituan's subsequent performance

According to Fitch's rating report, Meituan's long-term issuer default rating was raised from “BBB-” to “BBB,” and the outlook is “positive”. This rating adjustment reflects significant improvements in Meituan's profitability and strong free cash flow (FCF). This is due to the company's successful strategy implementation and mitigation of in-store business competition. It is expected that the scalability of the Meituan platform, the increase in the penetration rate of core local commercial businesses, and the strategic shift from subsidy-driven investment to reward-driven investment will support the steady growth of EBITDA and the generation of FCF in the short to medium term.

J.P. Morgan predicts Meituan's adjusted earnings per share growth of 119 percent and 95 percent for the third and fourth quarters, respectively, faster than 78% in the second quarter. J.P. Morgan also pointed out that Meituan has significantly accelerated returns to shareholders, repurchased shares by more than 3% of tradable shares, and increased the size of the repurchase plan to 1 billion US dollars.

Citi also pointed out that looking ahead to Meituan's third and fourth quarter results, profit growth is likely to outpace the increase in revenue and total daily transactions due to product innovation, subsidies and cost improvements. As repurchases speed up, it is better to increase earnings per share than adjust earnings.