我们认为,这份通胀数据基本锁定美联储在9月降息25个基点,但不支持大幅宽松。我们的基准情形仍是美国经济软着陆,只不过这次伴随通胀粘性,可能导致美联储降息“走走停停”。这也意味着当前市场对于大幅降息的定价可能过度激进,未来存在调整风险。

我们认为,这份通胀数据基本锁定美联储在9月降息25个基点,但不支持大幅宽松。我们的基准情形仍是美国经济软着陆,只不过这次伴随通胀粘性,可能导致美联储降息“走走停停”。这也意味着当前市场对于大幅降息的定价可能过度激进,未来存在调整风险。Source: CICC Commentary Author: Zhang Jundong, Fan Li, Zhang Wenlang With the expectation of a basic stable market and interest rate cuts in September [1], trading style has changed. After the June CPI and retail sales data were released, large-cap growth stocks led by AI concepts have clearly pulled back, while gold, small-cap stocks, and real estate, consumer, manufacturing, and bank-related stocks in the Dow have performed relatively well. The trading main line behind seems uncertain, and there has been a large discrepancy in the market's judgment on whether the US economy will have a "soft landing" or a "hard landing" after interest rate cuts. Is the market currently experiencing a short-term cut in style or a long-term change in style? We believe that with the basic expectation of interest rate cuts being largely fulfilled, the space for interest rate cut trading ("buying on expectations") may be significantly squeezed, while the "cyclical trading" after interest rate cuts is gaining momentum (see "All kinds of interest rate cut trading are the same, but the trading logic after interest rate cuts is different"). Unlike interest rate cut trading, cyclical trading mainly prices the recovery of terminal demand and the restart of the economic cycle after interest rate cutting. Its supporting logic is the resilience of US household demand, large fiscal and re-industrialization, and more deeply, the "realization from empty to real" of the total scale and structural resilience of the US economy. Under the support of total-scale resilience of the economy, the interest rate cut may be relatively limited (that is, a "shallow" interest rate cut), which is more beneficial to the real economy, especially profitable-supporting enterprises, and has a relatively limited boost to valuation. In terms of pace, Trump Trade 2.0 may accelerate the arrival of cyclical trading, given the increasing probability of Trump's recent election victory, stronger fiscal dominance (monetary coordination), industrial return, and potential weak US dollar in his policy ideology. At the same time, we also remind that due to the uncertainty caused by the election results, US stocks may enter a relatively high volatility period in the July-October of each election year; and after the uncertainty of the election dissipates, US stocks and bond rates often rise, and on average, value stocks perform better than growth stocks after the election (see "Major asset classes in US election years: seeking certainty in uncertainty").

Today's weather is good Today's weather is good

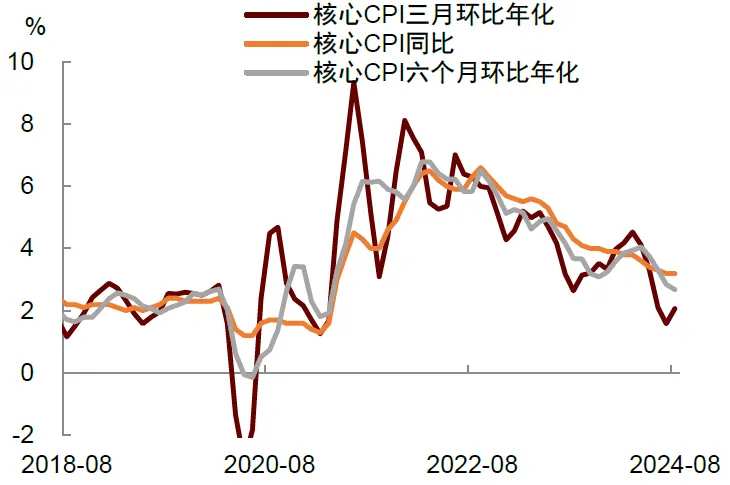

In August, the total CPI in the United States rose by 0.2% on a seasonally adjusted basis (previous value of 0.2%), and the year-on-year growth rate fell to 2.5% (previous value of 2.9%), which is lower than market expectations. The core CPI rose by 0.3% on a monthly basis (previous value of 0.2%), with a year-on-year growth rate of 3.2%, which is in line with market expectations. Although the total CPI continues to slow down, the core CPI has rebounded for the second consecutive month, especially the inflation in rent and core services (supercore), which has attracted market attention.

We believe that this inflation data essentially locks the Federal Reserve into a 25 basis point rate cut in September, but does not support a significant easing. Our base scenario is still a soft landing for the US economy, but this time with inflation inertia, which may cause the Federal Reserve to cut interest rates 'stop and go'. This also means that the current market pricing for a significant rate cut may be overly aggressive, with potential adjustment risks in the future.

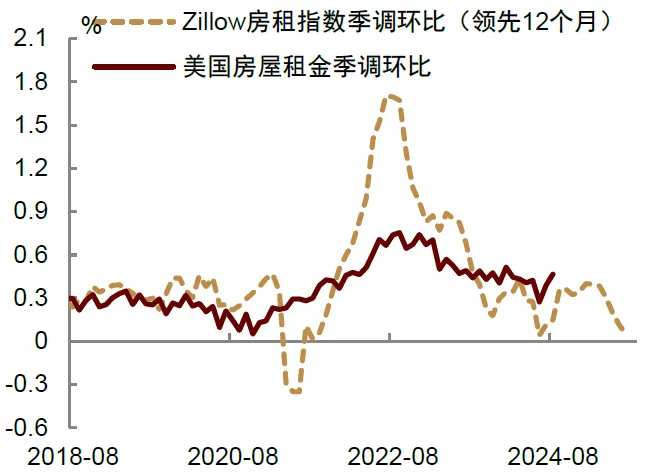

In August, the overall CPI in the United States slowed, but the core CPI rebounded for the second consecutive month, indicating that the inflation stickiness still exists. In terms of specific items, the main sources of inflation stickiness in August are two-fold. First, the rental item saw an increase from 0.3% the previous month to 0.5%. Within this category, the seasonally adjusted rent for primary residence increased by 0.4% (previously 0.5%), equivalent rent for landlords increased by 0.5% (previously 0.4%), and hotel prices rebounded significantly from a previous increase of 0.2% to 2.0%. The stickiness of rental inflation is in line with predictions, indicating that based on the Zillow Rental Index trend, it may be difficult for the CPI rental inflation to remain below 0.2% in the next 6 months. This suggests that the anti-inflation effect resulting from the slowdown in rents may be relatively limited.

Another source is the non-rental core service inflation (supercore) that the Federal Reserve is most concerned about. The month-on-month growth rate of this indicator expanded from 0.2% the previous month to 0.3%. Among them, after a significant continuous drop, airfare prices rebounded strongly in August, with a month-on-month growth rate of 3.9%, driving the overall month-on-month growth rate of transportation services from 0.4% the previous month to 0.9%. Medical service prices fell by 0.1% month-on-month, with hospital and related services increasing by 0.4%, but dental medical services (-0.6%), ophthalmic medical services (-0.5%), and home elderly care services (-0.2%) all declined month-on-month.

Another source is the non-rental core service inflation (supercore) that the Federal Reserve is most concerned about. The month-on-month growth rate of this indicator expanded from 0.2% the previous month to 0.3%. Among them, after a significant continuous drop, airfare prices rebounded strongly in August, with a month-on-month growth rate of 3.9%, driving the overall month-on-month growth rate of transportation services from 0.4% the previous month to 0.9%. Medical service prices fell by 0.1% month-on-month, with hospital and related services increasing by 0.4%, but dental medical services (-0.6%), ophthalmic medical services (-0.5%), and home elderly care services (-0.2%) all declined month-on-month.

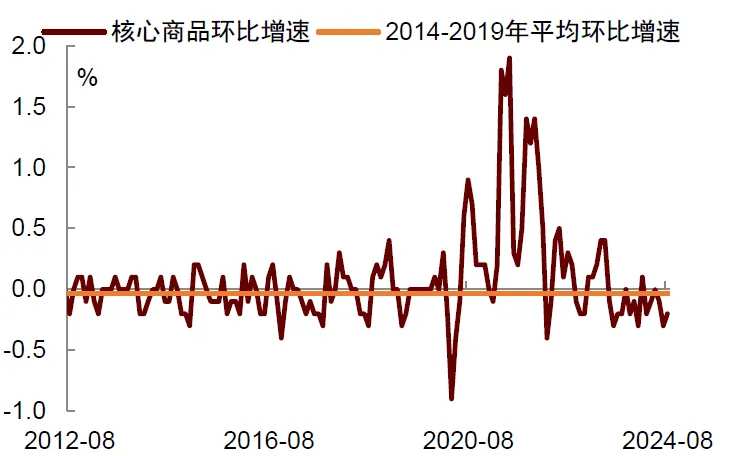

The good news is that the core commodity inflation remains sluggish, declining by 0.2% month-on-month, although the decline narrowed from 0.3% the previous month. Supply chain repairs and China's cheap exports to the United States have put pressure on US commodity inflation, offering hope for a soft landing. Furthermore, the prices of televisions (-2.8%), smartphones (-1.4%), computers (-0.4%), furniture and bedding (-1.0%), and medical instruments (-0.6%) have all continued their downward trend, many of which are China's advantage export products or benefit from China's abundant supply capabilities. The price of used cars fell by 1%, narrowing from the 2.3% decline the previous month. The price of new cars rose by 0.1%, rebounding from the 0.3% decline the previous month. After experiencing software malfunctions in auto sales in June, there has been some pressure on the inventory of used and new cars, which may lead to a slight price increase in the coming months.

Chart 1: The core inflation in the USA continues to show a slowing trend; Source: Haver, CICC Research Department

Editor/Rocky