由于业务繁忙,贷款经纪人表示系统负荷已经接近极限,促使贷款机构、交易部门、风险管理人员和信用评级机构尝试增派新员工。Cushman & Wakefield商业地产经纪公司高级经济学家兼投资者洞察负责人Abby Corbett表示:“今年夏天CMBS的发行非常活跃。”

由于业务繁忙,贷款经纪人表示系统负荷已经接近极限,促使贷款机构、交易部门、风险管理人员和信用评级机构尝试增派新员工。Cushman & Wakefield商业地产经纪公司高级经济学家兼投资者洞察负责人Abby Corbett表示:“今年夏天CMBS的发行非常活跃。”The Wall Street commercial real estate loan system has been operating at a high speed since the beginning of this summer

The Zhitong Finance App learned that since the beginning of this summer, the Wall Street commercial real estate loan system has been operating at a high speed, which helps ease the pain caused by the debt burden created ten years ago.

According to S&P Global, lower interest rates due to falling US Treasury yields have given borrowers more room to deal with nearly 1 trillion dollars of mortgage debt due this year and the next four years each. Despite rising loan delinquency rates, strong demand for new mortgages on Wall Street has driven a significant increase in commercial mortgage-backed securities (CMBS) bond transactions.

Due to busy business, loan brokers said the system load was close to its limit, prompting lenders, trading departments, risk managers, and credit rating agencies to try adding new employees. Abby Corbett, senior economist and head of investor insight at Cushman & Wakefield Commercial Realtors, said, “The CMBS launch was very active this summer.”

Due to busy business, loan brokers said the system load was close to its limit, prompting lenders, trading departments, risk managers, and credit rating agencies to try adding new employees. Abby Corbett, senior economist and head of investor insight at Cushman & Wakefield Commercial Realtors, said, “The CMBS launch was very active this summer.”

Many banks and insurance companies keep real estate loans on their books, while Wall Street usually packages new mortgages — covering commercial properties such as hotels, retail, homes, and office buildings — into CMBS bonds and sells them to investors.

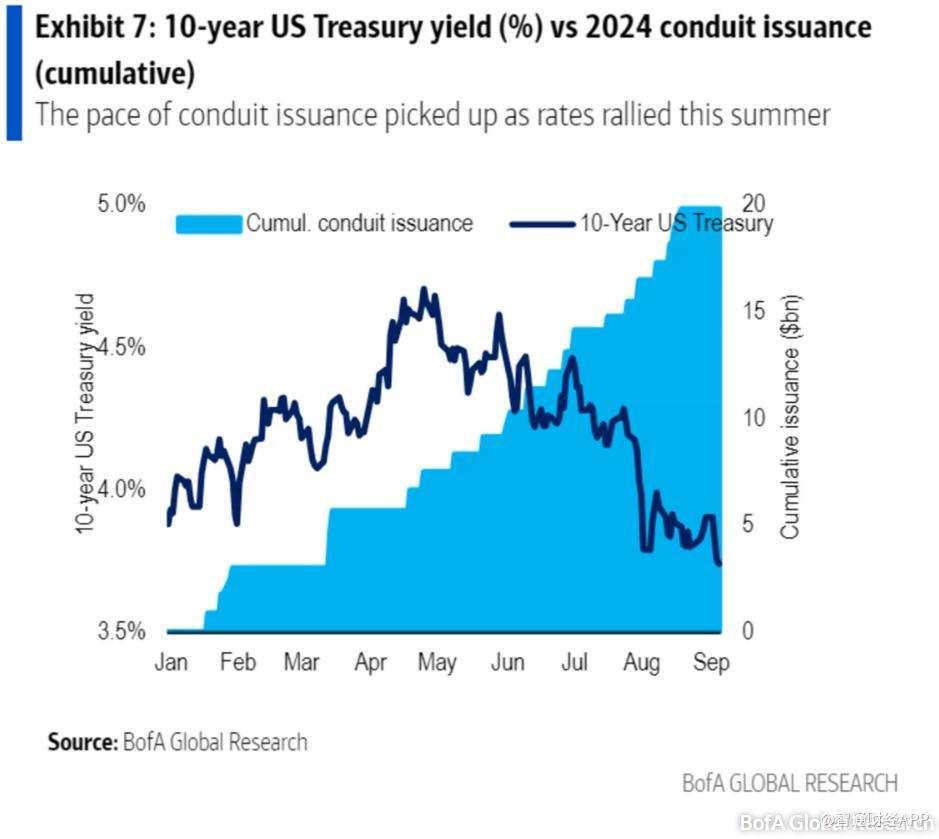

According to Bank of America Global data, the volume of new issuance in 2024 is close to 70 billion US dollars, more than double that of the same period last year. Bank of America strategists pointed out that the 10-year US Treasury yield fell below 4% from the summer, which is one of the main reasons driving the surge in bond issuance.

Although the commercial real estate background is still difficult, especially in the office real estate sector, the financing boom continues unabated. However, investors and regulators are still wary of buildings located outside of high-demand properties located in core areas that are fully equipped.

According to Trepp LLC, the delinquency rate for office real estate loans rose to 7.97% in August, while the overall delinquency rate including hotels, shopping malls, and other property types rose to 5.44%. By contrast, the peak of the delinquency rate after the global financial crisis in July 2012 reached 10.34%.

The recovery in the commercial real estate loan market is still in its early stages. Over the past two years, rising interest rates have led to a sharp drop in transaction volume and triggered industry-wide layoffs.

Lisa Pendergast, executive director of CRE Finance Council (CRE Finance Council), said that although the market environment is full of uncertainty, the increase in Wall Street and regional bank loans is a positive sign for commercial real estate. It is expected that upcoming interest rate cuts will also help stabilize the market and help determine real estate valuations. She also pointed out that despite the uncertain environment, the need for staff expansion in the loan and investment sector is still growing.

Wall Street's influence in the estimated $4.7 trillion commercial real estate debt market is expanding, according to the Association of Mortgage Bankers.

Corbett pointed out that CMBS has accounted for about 15% of the loan market so far this year, which is higher than the pre-COVID-19 average of about 13%. Compared to other lenders, CMBS generally offers higher leverage and looser terms for borrowers, such as interest-only loans.

The potential risk is that the economy may fall into a “hard landing” situation even though the Federal Reserve is expected to cut interest rates in September. Lower interest rates are beneficial to the performance of collateral assets, but Barclays's credit research team pointed out in a recent client report that for some assets, interest rate cuts may come too late. In particular, for old bond transactions where office buildings account for a relatively high share, the risk of credit rating downgrades is expected to remain high.

Market fluctuations in August and early September are also a potential risk. Corbett said that although there have been some “orange alerts” in recent economic data and the labor market, Wall Street doesn't seem to be paying enough attention. She stressed that interest rates are not everything; real estate valuations and whether the property can generate enough revenue to cover the cost of debt are just as important.

As of Wednesday, the 10-year US Treasury yield was 3.66%, as August inflation data lowered expectations that the Federal Reserve would cut interest rates sharply next week. Meanwhile, the Dow Jones Industrial Average, the S&P 500, and the Nasdaq Composite Index rebounded after falling in early trading.

For investors who include bonds in their portfolios, they may have already been exposed to the CMBS market. Other investors can gain market exposure to CMBS through exchange-traded funds. As of Wednesday, the iShares CMBS ETF is up 4.1% this year.