China Real Estate Research Institute stated in a document that the inventory liquidation cycle is dynamic, influenced by both the inventory scale and market sales speed. With a significant reduction in land supply, the market is entering a phase of spontaneous inventory reduction. However, the current real estate sales still face adjustment pressure, and relying solely on market forces to reduce inventory is relatively slow, requiring further support policies.

According to the Futubull Finance APP, the China Real Estate Research Institute stated in a document that the inventory liquidation cycle is dynamic, influenced by both the inventory scale and market sales speed. With a significant reduction in land supply, the market is entering a phase of spontaneous inventory reduction. However, the current real estate sales still face adjustment pressure, and relying solely on market forces to reduce inventory is relatively slow, requiring further support policies. At present, state-owned enterprise inventory acquisition and land activation policies have room for improvement. If policy adjustments can be accelerated, it will help inventory liquidation and also have a positive impact on the improvement of the cash flow of real estate companies and the expectations of residents.

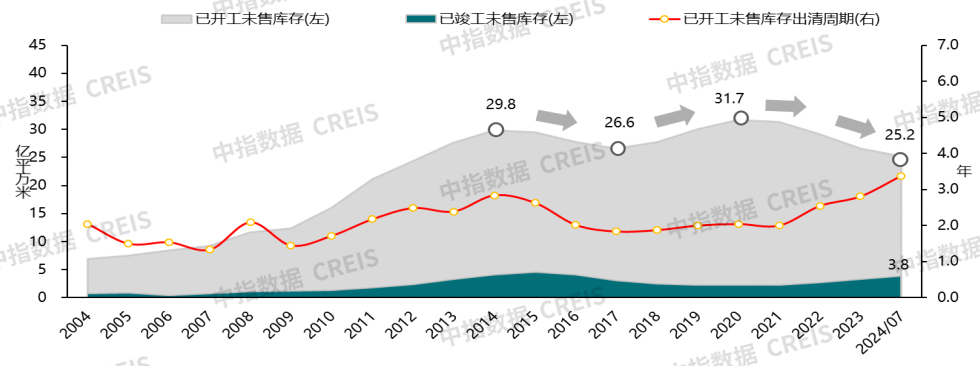

As the new construction area rapidly declines, the 'started but unsold inventory' has decreased significantly. By the end of July, the national 'started but unsold inventory' of residential properties was about 2.5 billion square meters, a 5.2% decrease from the end of last year. The contraction in supply is the main reason for the current inventory reduction. However, in terms of the liquidation cycle, the liquidation cycle of the 'started but unsold inventory' is about 3.4 years, 0.6 years longer than the end of last year.

In response to the 'completed but unsold inventory,' the May 17th policy put forward the 'state-owned enterprise inventory acquisition' plan. Currently, many places have issued public notices for collection, but the policy is still in an exploratory phase, and policy optimization is still needed to enhance the enthusiasm of all parties. Regarding the 'land sold but not yet started construction,' Yuexiu Guangzhou recently succeeded in returning the land and compensating with bills, and the funds from the returned land will continue to be used to purchase land in Guangzhou. This approach provides a reference for other cities and may have more cities following suit in the future, improving the inventory structure and relieving enterprise inventory pressure.

The national new home 'started but unsold inventory' is about 2.5 billion square meters, the reduction in supply has led to a decrease in the inventory scale, but it still faces certain pressure for liquidation.

Figure: Different scales of residential property inventory nationwide

Note: The 'started but unsold inventory' = cumulative new construction area of commodity residences - cumulative sales area of commodity residences. The accumulated liquidation cycle of 'started but unsold inventory' since 1998 = 'started but unsold inventory' / annual sales area of commodity residences. The sales area of commodity residences in 2024 is estimated on a year-on-year basis.

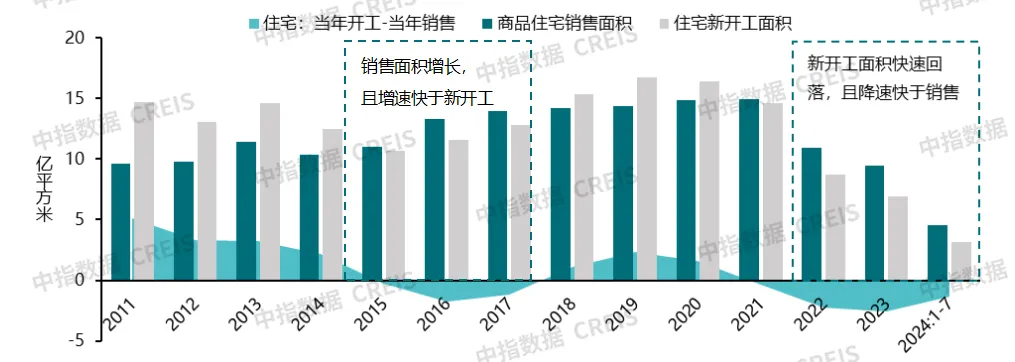

Figure: Comparison of national residential new construction and sales area

According to the China Index Research Institute's calculations, as of July 2024, the national residence "under construction and unsold inventory" is 2.52 billion square meters, of which the "completed and unsold inventory" is 0.38 billion square meters. In terms of clearance period, the current clearance period of "under construction and unsold inventory" is about 3.4 years, indicating significant pressure to clear inventory.

Looking at the trend of inventory changes in the past decade, it can be roughly divided into three phases:

Phase 1 (2015-2017) - Driven by the monetization of shantytown renovation, inventory declined: After experiencing a real estate boom in the previous years, some cities faced issues of inventory backlog, with the "under construction and unsold inventory" reaching 2.95 billion square meters in 2015. In order to alleviate the inventory issue in the market, the government at that time implemented the policy of "monetized relocation of shantytown residents", demolishing old houses to release new housing demand. The market inventory scale decreased slightly in 2016-2017, but due to the increase in market demand, the enthusiasm of real estate companies for land acquisition quickly recovered, resulting in only a small decrease in market inventory.

Phase 2 (2018-2021) - "Three Highs" model driving inventory growth: In recent years, the real estate market has entered a period of stable development, and compared to 2016-2017, market demand has slightly declined. During this period, local governments continued to increase land supply, and under the promotion of the "Three Highs" model by real estate companies, the market inventory scale gradually increased.

Phase 3 (after 2022) - Decrease in supply leads to inventory decline: Since 2022, the real estate market has cooled down significantly, and the national "under construction and unsold inventory" has decreased. However, unlike in 2016-2017, the current market sales have not shown a clear recovery, and the decrease in inventory is mainly due to a significant decrease in land transaction volume and new construction (the land transaction and new construction scale in 2023 decreased by about 60% compared to 2020, and the scale continued to decline in 2024). This difference is also reflected in the trend of the clearance period in the two phases. In 2016-2017, as market sales increased and inventory levels decreased, the clearance period shortened and the market inventory pressure eased. Currently, although market inventory levels are decreasing, sales continue to be sluggish, resulting in a lengthening clearance period and increasing market inventory pressure.

In addition, in contrast to the decreasing scale of "under construction and unsold inventory", the scale of "completed and unsold inventory" has continued to grow since 2020, which is also an indication of the sustained weak market sales. As of July 2024, the national scale of "completed and unsold inventory" is approximately 0.38 billion square meters, a growth of 70.9% compared to 2020.

State-owned enterprise (SOE) acquisitions and stock-piling are direct means to clear inventory, but the pace of implementation still needs to be accelerated, and there is room for improvement in the acquisition and stock-piling policies.

Local SOE acquisitions and stock-piling should have the most direct impact, but the pace of implementation is still slow due to factors such as purchase prices, funding costs, and mismatched housing supply. After the policy of providing CNY 300 billion in refinancing for indemnificatory housing loans was introduced on May 17, various regions started promoting the relevant work of SOE acquisitions and stock-piling for the purpose of affordable housing. According to monitoring by the China Index Research Institute, as of the end of August 2024, about 30 cities have issued announcements soliciting commercial housing for use as affordable housing. According to data disclosed by the central bank, as of the end of June 2024, the balance of refinancing for affordable housing loans was CNY 12.1 billion.

Table: Announcement of "State-Owned Enterprises Receiving Unsold New Houses" issued by some cities.

Data Source: Comprehensive compilation by China Real Estate Index Research Institute.

From the current policies of state-owned enterprises in receiving unsold houses, there may be various challenges in their implementation:

(1) Difficulty in matching acquisition prices: Based on the current announced collection notices, the acquisition price is usually set as the upper limit, taking the reset price of affordable housing in the same location as a reference (including land transfer costs, construction costs, and profits not exceeding 5%). This price may be difficult to reach the level that developers are willing to accept.

(2) Supply and demand mismatch: From the perspective of city distribution, in cities where real estate developers have large inventory pressures and strong willingness to sell, the demand for affordable housing is relatively limited, making it more difficult to achieve profitability balance. On the other hand, in core cities with strong demand for affordable housing, market inventory pressure may be smaller, and real estate developers may have a relatively lower willingness to sell commodity housing at a discount. In terms of unit size, affordable housing should mainly consist of small units. Under strict restrictions on unit size, there are few existing commodity housing projects that meet the requirements. Although the maximum acquisition unit size has been relaxed to 120 square meters or less in some cities, it may still require secondary renovation in the future to meet the requirements of affordable housing. In terms of building requirements, most cities currently require priority selection of entire buildings or entire units that are unsold and can be managed under a closed system. However, the number of projects that meet these conditions in the market is relatively limited.

(3) High cost of funds: Although there is currently a 300 billion yuan re-loan support for affordable housing provided by the central bank, the longest loan term does not exceed 5 years, and the annual interest rate for re-loans is 1.75%. If the loan interest rates of commercial banks are taken into account, the funding cost of state-owned enterprises in acquiring unsold houses is approximately around 3%. If additional costs such as renovation and operation are considered, the actual costs may be even higher. Therefore, in the process of converting unsold housing into rental housing, financial subsidies and other measures are needed to achieve a balance of profitability. However, local governments are currently facing substantial financial pressures, and their fiscal support for acquisition and storage may be limited.

Table: Recent progress in state-owned enterprises' acquisition and storage in some cities.

Data Source: Comprehensive compilation by China Real Estate Index Research Institute.

In terms of the progress of urban acquisition and storage, on August 17th, the first project in Wuhan officially landed, providing more than 500 units of affordable rental housing for the whole city. On August 26th, the signing ceremony of the second batch of acquisition of existing commercial housing for use as affordable housing was held in Chongqing. After the transformation of 7 projects, more than 2,600 units of affordable housing can be provided. Zhengzhou Chengfa Anju Group has been negotiating the acquisition of some existing projects since the second half of 2021. As of June 2024, Zhengzhou Chengfa Anju Group has cumulatively acquired more than 111,000 units of housing. Fuzhou is also one of the 8 pilot cities for the rental housing loan support program. As of July 2024, Fuzhou Anzhu Development Co., Ltd. has cumulatively acquired about 5,000 units of existing housing, and the first batch of 149 units of renovated rental housing will be allocated in September this year.

In addition, Zhuhai State-owned Assets has also initiated the acquisition of existing houses. On July 31, 2024, Huafa Group announced that it would transfer all the existing properties under its subsidiary Huaben Company to Zhuhai Anju Group for a price of 266 million yuan. On August 8th, Huafa Group, Zhuhai Anju, and Guangdong Branch of China Construction Bank signed a strategic cooperation agreement in Zhuhai. According to the agreement, Guangdong Branch of China Construction Bank will provide Zhuhai Anju with comprehensive bank credit support with a total amount not exceeding 20 billion yuan. The three parties will carry out in-depth cooperation in the construction of Anju projects and other aspects. On August 9th, Huafa Group issued another announcement that it intends to conduct transactions of existing commercial housing and supporting parking spaces (including housing sources that meet the pre-sale conditions) with the company's controlling shareholder, Zhuhai Huafa Group Co., Ltd. or its subsidiary, with a total transaction amount not exceeding 12 billion yuan.

To speed up the pace of state-owned enterprise acquisition and storage, related policies still need to be further optimized. Possible directions include:

(1) Expand the scope of use of acquired existing houses. After acquisition and storage, they can be prioritized as resettlement houses and it is suggested to allow them to be rented before being sold in order to solve the problem of fund balance. That is, maintain the nature of the acquired existing commercial houses unchanged, use them as rental housing after renovation during the deep adjustment stage of the real estate market, and after being approved by the local city government when the real estate market stabilizes, they can be sold again as commercial houses.

(2) Expand the scope of acquisition targets. On the one hand, the current state-owned enterprise acquisition and storage focuses on completed unsold inventory, but there is no targeted policy for unfinished inventory under construction. In the future, the state-owned enterprise acquisition and storage policy may further expand the scope to include eligible unfinished inventory (the use of acquisition and storage funds is strictly supervised to ensure the normal completion of projects). On the other hand, it is possible to consider incorporating the acquisition of commercial housing into the solution of operating difficulties faced by construction enterprises and decoration companies, and include the already incurred work-to-house transactions into the scope of acquisition of completed existing commercial housing, thereby relieving the difficulties of upstream and downstream industry chain enterprises.

(3) Further increase financial support, such as extending the maximum duration of refinancing for affordable housing to meet the capital needs of renovation and operation of rental housing. In addition, if state-owned enterprise acquisition and storage can be included in the scope of local government special debt funds, it will also help to alleviate the financial pressure on local governments and accelerate the pace of acquisition and storage of existing houses.

Recently, Yuexiu obtained 12 billion yuan in compensation for land withdrawal in Guangzhou, which will be used for subsequent land acquisition in Guangzhou. This model provides a new approach to solving the problem of land inventory.

In addition to the above-mentioned unsold completed inventory and unsold completed inventory, the broad definition of real estate inventory also includes land sold but not yet started. This part of the scale is also quite large, and in recent years, affected by the market downturn and debt pressure, real estate companies have a lower willingness to start construction on the land they have. In view of land inventory, the Ministry of Natural Resources has previously proposed policy ideas and measures to support enterprises in optimizing development, promoting market circulation and transfer of land, and supporting local governments in taking back land at reasonable prices.

Recently, some real estate companies have been improving their land inventory structure through land withdrawal. In July 2024, the Hongshan Town Government in Gulou District, Fuzhou, announced that China Resources Fuzhou Duchilu plot had submitted an application for land withdrawal. In August 2024, the Yuhua Sub-bureau of the Changsha Natural Resources and Planning Bureau stated that the Zhongxin Chutian Lanting project is undergoing land reclamation procedures due to the developer's financial problems. The government plans to reclaim the land and then re-list it for sale.

In addition, controlling the supply of land is also an important means of regulating market inventory. On April 30th this year, the Central Political Bureau meeting proposed "to coordinate the research on digesting the stock of real estate and optimizing the policy measures of incremental housing". On the same day, the Ministry of Natural Resources issued a document requiring cities with large inventory levels to suspend the sale of residential land, and clearly stating that future land supply will be closely related to the revitalization of stock land.

Summary & Outlook

Currently, China's real estate sales still face adjustment pressure, and the market is still in the bottoming stage. If the "inventory digestion" policy accelerates its implementation in the next few months, it will have a positive impact on the improvement of cash flow for real estate companies and the expectations of residents. On the housing side, state-owned enterprises acquiring and storing inventory is the most direct way to reduce inventory, but the policy details still need to be optimized and the implementation needs to be accelerated. On the land side, revitalizing stock land and optimizing land supply are the main policy directions, among which land withdrawal and replacement may become an effective way to improve the land inventory structure. Overall, with a significant reduction in supply, the market has entered a stage of spontaneous inventory reduction, and with the addition of policy support and stabilization of sales, it is expected that market inventory will continue to improve.