By adjusting the gap between deposit facility interest rates and loan interest rates, policymakers aim to ensure that the ECB maintains control over market conditions while shrinking its balance sheet.

The Zhitong Finance App learned that the ECB will announce the latest interest rate decision on September 12 (Thursday). At that time, the ECB may cut interest rates for the second time since this year, and this rate cut will take quite a technical turn.

Although the market currently generally expects the ECB to cut interest rates by 25 basis points on Thursday, the potential rate cut of 60 basis points on major refinancing interest rates is far less conventional. The purpose of the ECB's move is to provide “lubricant” for the operation of the financial system when large-scale bond holdings and long-term loans are lifted. By adjusting the gap between deposit facility interest rates and loan interest rates, policymakers aim to ensure that the ECB maintains control over market conditions while shrinking its balance sheet.

1. What is the situation now?

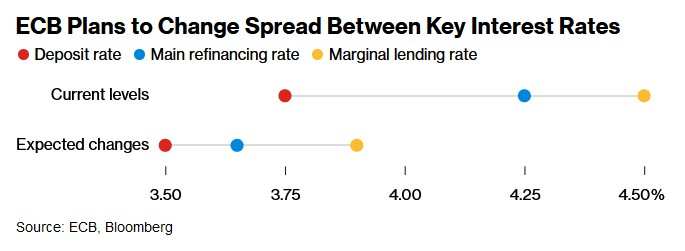

Currently, the ECB deposit mechanism interest rate is 3.75%, the main refinancing rate is 4.25%, and the marginal loan interest rate is 4.5%. The asymmetric spread between these three interest rates is a legacy of the ECB's negative interest rate era. Previously, in order to combat deflation and stimulate the economy, the ECB drastically cut deposit mechanism interest rates below zero, but they were unable to take the same measures for the other two interest rates.

2. What will change?

The ECB is about to close the gap between deposit facility interest rates and major refinancing rates — from 50 basis points to 15 basis points, and the spread between the main refinancing rate and the marginal loan interest rate will remain unchanged at 25 basis points. If the results of the interest rate cut meet the general expectations of market observers, the deposit mechanism interest rate will drop to 3.50%, the main refinancing rate will drop to 3.65%, and the marginal loan interest rate will drop to 3.9%.

Adjustments to major refinancing interest rates and marginal loan interest rates of more than 25 basis points are considered technical adjustments needed to deal with changes in the financial system and monetary policy in recent years. They are the result of a 15-month review of the ECB's operating framework and announced in March of this year.

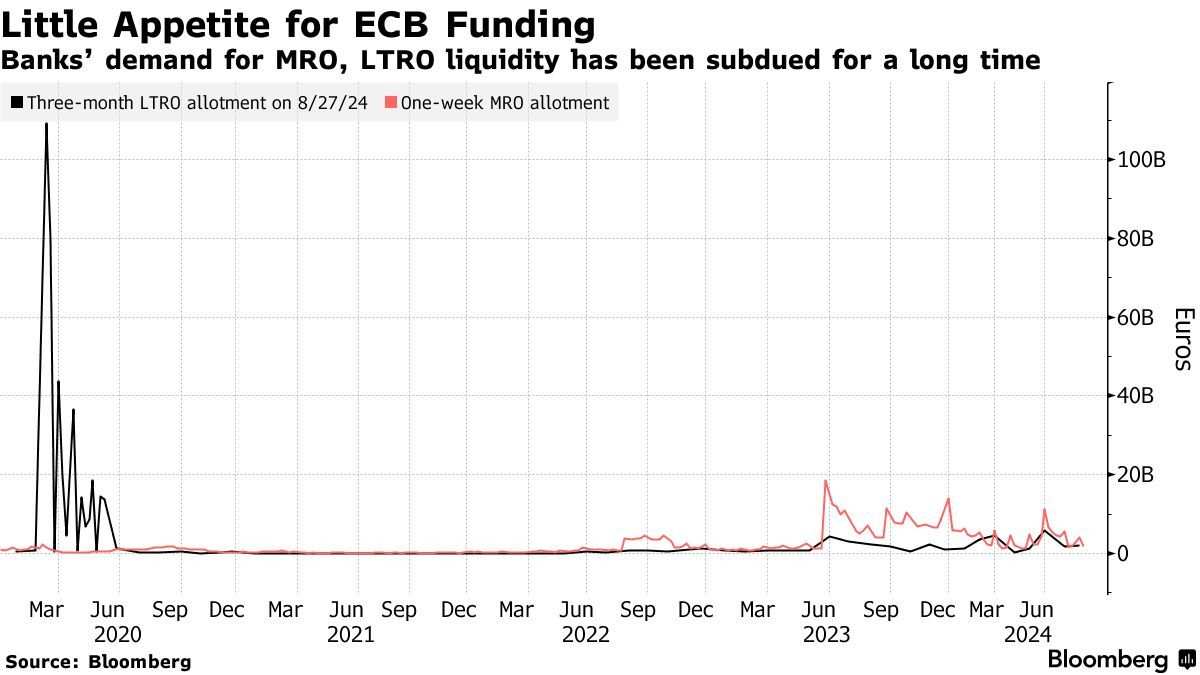

Bank borrowing by the ECB has been low in recent years, so the impact of this move on the overall financing situation will be minimal. The current weekly financing amount is around 2 billion euros, while the total amount of outstanding three-month loans is around 10 billion euros.

3. Why should the ECB do this?

Since the ECB began large-scale bond purchases in 2015, there has been excess liquidity, and overnight market interest rates have followed deposit mechanism interest rates. But for some time now, policymakers haven't reinvested the proceeds from all maturing bonds, and long-term loans are maturing, so the balance sheet has been shrinking rapidly.

This process will continue as policymakers continue to push forward crisis-era stimulus measures. There will come a day when liquidity will no longer be sufficient. In the absence of a new asset purchase plan, banks will need to start borrowing again. This could cause market fluctuations as a side effect.

The main goal of policy makers is to keep such market fluctuations to a minimum. Narrowing the gap between interest rates for banks borrowing from the ECB and interest rates for storing funds at the ECB has also narrowed interest spreads where overnight market interest rates may change.

4. Is this the end result of how future policies operate?

Probably not. Before the ECB announced its upcoming reforms, policymakers had a heated debate about whether they wanted to continue to operate in a system where bank liquidity exceeded technical requirements, or whether they wanted to return to the austerity monetary system before the Great Financial Crisis — a system where capital needed to be managed painstakingly.

Opinions among policy makers are very divided. The final answer is that policymakers decided to temporarily keep the current system, that is, excess liquidity makes market interest rates close to deposit mechanism interest rates. As balance sheets shrink in the future, banks will have more responsibility to decide how much liquidity they need to operate.

5. Is it possible for banks to change their behavior?

Borrowing from the ECB will become relatively cheap, which may provide an incentive for banks to participate in regular lending operations. The narrowing of the spread between the deposit mechanism interest rate and the other two interest rates also means a reduction in the cost of prudent action, that is, requiring slightly more capital than strictly required, and depositing the remaining funds back to the central bank. At the same time, banks also have room for interaction in order to save a little interest when borrowing money.

6. What impact will it have on the market?

The impact on the market in the short term is likely to be limited, in part because the change was already evident earlier this year. Most importantly, the level of excess liquidity is still high, over 3 trillion euros (around 1.7 trillion euros before the pandemic), which limits the need for other sources of funding.

As the battle for liquidity heats up, the key market to focus on will be the buyback market. In the repurchase market, banks can use extremely secure collateral as collateral in exchange for cash from peers. According to Chicago Mercantile Exchange Group (CME Group)'s RepoFunds Rates Benchmark data, the single-day repurchase rate for liquidity guaranteed by a set of German bonds is currently slightly below 3.75%, which is the current level of deposit interest rates.