Source: Barron's Chinese

Author: Nicholas Jaskinski

Evan Greenberg, CEO of Chubb Ltd, has a highly influential fan - Warren Buffet, CEO of Berkshire Hathaway. Berkshire Hathaway disclosed last month that it held 6% of the shares in Chubb, one of the world's largest insurance companies, by the end of 2023. Berkshire itself is a major participant in the insurance industry, but it is not the only buyer. In the past year, Chubb's stock return, including dividends, was about 40%, surpassing the S&P 500 index's total return of 25%, and making the company's market capitalization reach $110 billion. This increase in market capitalization reflects Chubb's outstanding performance, which is attributed to its prudent underwriting practices and conservative management of its investment portfolio of about $140 billion. The company's earnings per share increased by 48% in 2023 and its book value per share increased by 21%.

Greenberg is the son of Maurice "Hank" Greenberg, the former CEO of American International Group (AIG). Greenberg worked at AIG for 25 years, rising through the ranks. He left the insurance company in 2000 and took over Ace Limited in 2004. The company merged with Chubb in 2016, the largest M&A in the property and casualty insurance industry at the time.

Today, Chubb is the largest commercial insurance provider in the United States, and the company is also known for its high-end homeowner insurance for the wealthy. However, about half of the company's premiums last year came from outside the United States. Asia has always been a growth area where the company is bullish: Although Asia accounts for 40% of global GDP, the insurance industry accounts for only 26% of the global insurance market share. This gap is expected to narrow over time. Greenberg sits on the board of several nonprofits that focus on international and Asian affairs. Barron's recently interviewed Greenberg about his underwriting philosophy, the challenges of dealing with increasingly frequent climate disasters, and US-China relations. Following are the edited excerpts of the conversation.

Author: Ghatam Baird

Read more history and make fewer predictions.

Introduction:

I encountered Charlie Munger in an investment class at the University of Southern California Graduate School and had the privilege of asking him an important question: "What should I do to become a better investment professional?" His answer was: "Read history! Read history! Read history!" This is one of the best advice I have ever received.

Fear is more able to grasp human behavior than the most impressive historical evidence.

Warren Buffett once said, "The words of market forecasters will fill your ears, but they will never fill your wallet."

Think about since 2009, how much damage your wallet would have suffered if you had believed in those so-called market experts highly praised by the business media.

1. Forecasting is a compulsive desire.

Have you ever wondered why TV hosts and market experts make so many predictions day after day, even though they are wrong most of the time and never doubted? Why are they so eager to make these predictions?

Jason Zweig explains the impulse for constant prediction in his book "Your Money and Your Brain": "Just as nature abhors a vacuum, people abhor randomness. The impulse to predict the unpredictable stems from the dopamine centers in the brain. I call this human tendency 'prediction addiction'."

This trend is driven by a pleasurable chemical called dopamine in our brain, which releases a natural impulse to make the next prediction, and then another one after that.

As Zweig explains, prediction addiction is a compulsive desire to find meaning in everything in the world, including things that cannot be predicted, like future stock prices. (When asked what the market will do, the legendary figure J.P. Morgan said, "It will fluctuate.") None of us can predict our own future. Nevertheless, we are still deceived by the illusion of control and try to predict macroeconomics, markets, currencies, and commodity prices.

Investment writer Dan Solin discussed prediction addiction in an article he wrote for The Huffington Post: "This addiction is particularly severe. Our brains not only naturally believe we can predict the future and find patterns in random behavior, but our brains also reward us for such behavior. The brains of people engaged in this activity experience pleasure similar to that of gamblers entering a casino."

For investors, prediction addicts are like gamblers in a casino.

Try this interesting exercise: search the internet and look at the predictions and results of market experts on a macro theme during a randomly chosen time period in the past few years. You will never take these people seriously again. Predictions only attract attention, and they can't do anything else.

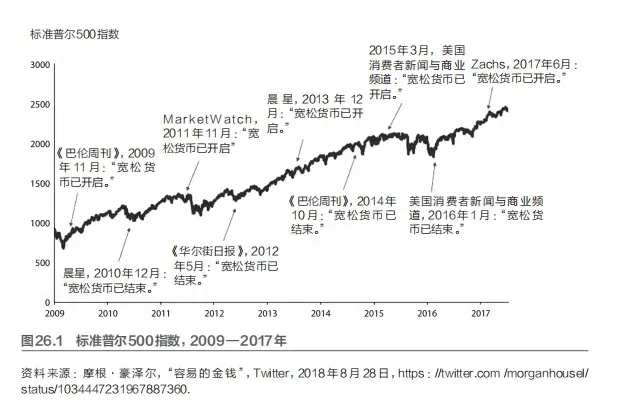

As the saying goes, a bull market builds a wall of worry. Since March 2009, countless worrisome headlines have driven many investors to sell stocks and completely exit the market out of fear.

The speed at which bad news spreads is ten times faster than good news, which is one of the biggest reasons why capturing market returns is so difficult. You might think it's simple to buy an index fund and then ignore it. The reason is simple, but it's certainly not that simple, because bad news will amplify your face, while good news just plays quietly in the background.

Except for a few exceptions, most human miracles are long-term, man-made events. Progress is made step by step. The silent miracle of human progress is that step by step, year after year, the world is progressing. Not according to one indicator per year, but there is always progress. Despite facing immense challenges, we have made great progress. This is a fact-based worldview. In the past 20 years, we have halved the global population living in extreme poverty, but the phrase 'poverty rates are on the rise' has never dominated the headlines. When a trend gradually improves over time and experiences periodic sharp declines, people are more likely to notice the decline rather than overall improvement. News media tend to focus on vivid events - dramatic, tragic events - rather than the daily progress and daily virtues in the world. News channels compete to attract our attention with vivid stories and dramatic narratives. They tend to focus on the unusual rather than the common, the new or temporary rather than slow-changing patterns. Although fundamental improvements are world-changing events, it is difficult for them to be considered news if progress is too slow, too scattered, or too small. The fastest spreading stories often have elements of fear or anger, gradually instilling a sense of helplessness. Open any news channel or go on social media. You may have heard or read about political instability, market turmoil, natural disasters, murders, suicides, disease outbreaks, geopolitical tensions, and a long list of bad news. People often refer to the present era as the 'worst in history', but these people have obviously never read a history book. The combination of negative bias and availability bias leads to a universal pessimism about the world. However, in reality, we live in one of the most hopeful times in human history. In almost all long-term time frames that you observe, the world has made incredible progress in many important parameters. It's just that bad news is an event or headline, while good news is a process or statistical data. And bad news, compared to statistical data, can be a more vivid and attention-grabbing story.

Second, pessimists are correct, optimists make money.

Remember, pessimists may sound smart, but optimists are the ones who make money. Business is the foundation of civilization. When we invest in stocks, we participate in business and support its continued development. Those who focus on the big picture will succeed in the long run. Others who only focus on crises will become neurotic at the worst times and miss out on hopeful opportunities for wealth creation.

Investors should learn from Warren Buffett's investment philosophy, which emphasizes the importance of focusing on individual companies and ignoring the noise about interest rate hikes, surging inflation, stock market crashes, oil shocks, government collapses, recessions, depressions, and even total wars.

In his 1994 letter to shareholders, he wrote:

We will continue to ignore political and economic forecasts because they will distract investors and businessmen, and the cost is high. 30 years ago, no one could foresee the outbreak of the Vietnam War, wage and price controls, two oil price shocks, and no one could predict the resignation of the president, the disintegration of the Soviet Union, nor did anyone know that the Dow Jones would drop 508 points in a single day, or that bond yields would fluctuate in the range of 2.8% to 17.4%.

Surprisingly, these sensational global events did not affect Benjamin Graham's investment principles, nor did they affect investors buying quality assets at reasonable prices.

Imagine if we were overcome by unknown fears, delaying or changing capital allocations, how much we would pay. In fact, we often find the best deals when panic reaches its peak due to major events. Panic is the enemy of fanatics and the friend of those who adhere to market fundamentals.

Over the next 30 years, there will definitely be a series of different major shocks. We will neither try to predict these, nor profit from them. If we can identify businesses similar to those we have acquired in the past, external surprises will have little impact on our long-term performance.

In his letter in 2012:

A thought for my CEO partners: undoubtedly, the immediate future is always full of uncertainty. The United States has faced various uncertainties since 1776. Sometimes people are very concerned about countless, persistent uncertainties, while at other times, they ignore uncertainty (usually because everything is going smoothly).

The business prospects in the United States are bright. Stocks will also perform well because their fate is closely linked to the performance of companies. Periodic difficulties are inevitable, but investors and managers are in a game influenced by their preferences. (The Dow Jones Industrial Index rose from 66 to 11497 in the 20th century, despite four devastating wars, one great depression, and multiple recessions, eventually still soaring 17320%. And don't forget, investors also received a fair amount of dividends.)

Because this game is so tempting, Charlie and I believe that trying to follow the arrangement of Tarot cards, 'expert' predictions, or the ins and outs of the business cycle is a huge mistake. The risk of missing out on this game is much greater than staying in it.

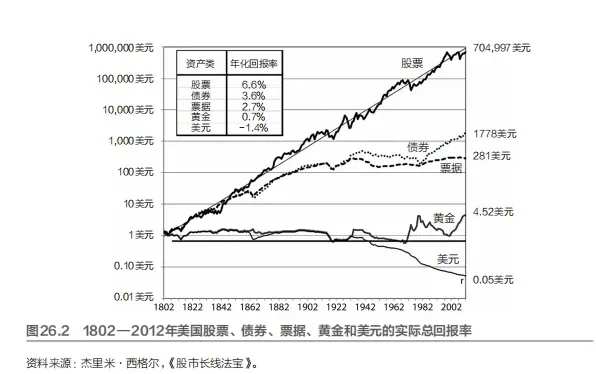

Why does Buffett always emphasize that the game investors participate in is "very advantageous for them"? Please refer to Figure 26.2. If data from more than two centuries cannot convince you that what Buffett said is true, then there may be nothing that can convince you.

Please refer to Figure 26.2, and we can clearly understand why Buffett warns not to consider holding cash equivalents and currency-denominated financial instruments as risk-free assets, because holding them for the long term actually carries significant risks. Buffett believes that risk is the loss of purchasing power. Bonds, which are widely touted as offering zero-risk returns, now also offer zero-return risks.

Whenever the media causes me to doubt, despair, or fear the current trend, I focus on the bigger trend. If you want to maintain long-term confidence in the stock market, you also need to pay more attention to this long-term trend.

A more macro situation tells us that over the past two centuries, despite various major and minor disasters, and despite people constantly giving various reasons to explain that the end of the world may be imminent, stocks have delivered an average annual real return of over 6.5% to their owners, far surpassing U.S. Treasury bonds, bonds, gold, and global reserve currencies. History clearly shows that stocks offer the highest long-term real returns. Their advantage over other categories of assets is completely overwhelming. Taking action based on this information in the long run is much more advantageous than reacting to the opinions and advice of commentators and consulting services who constantly predict an impending depression.

In a memorandum to Oak Capital clients in February 1993, Howard Marks wrote, "From 1926 to 1987, the average annual return on stocks was 9.44%. But if you went to redeem and missed the best 50 months out of these 744 months, you missed all the returns. This tells me that trying to time the market is a source of risk, not protection."

In response to significant market downturns, market experts often say things like, "The short-term outlook is uncertain...There are many global uncertainties...Stock prices may fall further, so wait for some time until more factors become clear...Wait until liquidity conditions improve...Wait until the election is over...The current political situation is full of uncertainty."

In other words, "wait and see." This particular advice can be costly for investors who want to enjoy the euphoria of rising stock prices in a bull market and avoid the pain of falling stock prices in a bear market. Higher stock market returns do not accumulate in a uniform manner. Instead, they often trace back to the sudden bursts of power that occur during several periods. Additionally, no one can accurately predict the timing and duration of these periods. A large portion of bull market gains often occur at the initial stage of market recovery. If investors do not participate in the market at that time, they are likely to miss out on a significant portion of the returns.

A study by SageOne Investment Advisors reveals that although the Indian stock index (Sensex) has risen 251 times from 1979 to 2017 (an annualized return of 15.5%), if you miss the 7% increase during the best few months or the 1% increase during the best few days, your return will be zero. As the cost of obtaining high returns from stocks, investors need to endure periodic downturns. The length of time in the market is important, rather than timing the market. It is important that you have the ability to invest consistently over time, regardless of market fluctuations, without worrying about the market trend tomorrow, next week, or next month. It's that simple.

It's simple, but not easy to achieve.

Three, read history! Read history! Read history!

Emotions cannot be tested in reverse; that's why, in hindsight, all the previous bear markets and the accompanying generally low stock valuations were opportunities there for the taking. From its listing in 1980 to 2012, Apple's market cap reached $22.5 billion. An investment of $0.01 million turned into $2.25 million. But if an investor experienced two consecutive drops of over 80% and multiple drops of over 40%, they would definitely not be able to handle it. Even outstanding companies like Fairfax Financial, which has delivered a ROI of 18% (a compound annual growth rate of 33% over 33 years) as of September 2019, saw its stock price fall nearly 80% between 1999 and 2002, with negative ROI each year during those four years. How many investors do you think can hold on during a continuous 80% decline in the stock market? People have different tolerance levels for downward volatility, whether it is perceived as a large-scale decline or the actual market decline. [All investors should read Morgan Housel's article "The Agony of High Returns" on Motley Fool.] The stock market is the only market where people run out of stores when things go on sale. When the market is in turmoil and panic, don't pay attention to the terrifying predictions and constant urging of authoritative figures and experts telling you to cash out as soon as possible, especially when you have a large amount of unrealized gains (when the temptation for profits and cashing out is at its peak).

Jargon is the preferred method in the financial world because it makes people sound smarter. For example, Wall Street has a saying, "Don't fight the Fed" (meaning don't go long if the Fed is tightening policy, and don't go short if the Fed is cutting rates). It sounds intuitive and logical, right? Now, please refer to the following:

1. January 3, 2001: Fed cuts rates by 50 basis points,$S&P 500 Index (.SPX.US)$and it closed at 1347. From that time to the lowest point in October 2002, it fell by 43%, while the Fed continued to cut rates.

2. September 18, 2007: Fed cuts rates by 50 basis points, and the S&P 500 index closed at 1519. From that time to the lowest point in March 2009, it fell by 56%, while the Fed continued to lower interest rates.

On June 30, 2004: The Federal Reserve raised interest rates by 25 basis points, and the S&P 500 index closed at 1140 points. From that time until September 2007, with rate cuts, interest rates increased by 33%, and the Federal Reserve raised rates more than 16 times.

On December 16, 2015: The Federal Reserve raised interest rates by 25 basis points, and the S&P 500 index closed at 2073 points. From that time until July 2019, with rate cuts, interest rates increased by 45%, and the Federal Reserve raised rates more than 8 times.

Now, let's take a look at common comments in the business media:

"Due to rising interest rates, the market is weakening."

"Historically, the stock market performs well during periods of rising interest rates."

You can choose the narrative style you prefer (which may be influenced by your personal experiences). During periods when rising interest rates lead to a sharp market decline, most of the seemingly smart voices in the media are likely to choose the first option. Unless the market is completely indifferent, news of rate hikes will not appear in the headlines. In fact, during this time, some experts may use historical charts or tables to illustrate that the rising interest rate environment in the past bull market proves the second choice is correct. The market moves first. Here are relevant reasonable explanations. Always has been.

The harsh reality is that the stock market does as it pleases. Investors should not get caught up in high-frequency macro indicators. Just focus on individual companies and their industry development. That's the best way. That's all. Always stay humble and honest.

Investors often replay in their minds over and over again the moments in the market when they were recently hit hard, and these memories will ultimately determine the future behavior of these investors. The examples in this chapter clearly illustrate why a solid historical foundation is crucial for cultivating the steel-like nerves required to navigate the cyclical dislocations in financial markets.

I encountered Charlie Munger in an investment class at the University of Southern California Graduate School and had the privilege of asking him an important question: "What should I do to become a better investment professional?" His answer was: "Read history! Read history! Read history!" This is one of the best advice I have ever received.

The purpose of studying history is to make us aware of possibilities that we would not have considered otherwise. Often, we are surprised by events that have not happened in our lifetime, even though similar unprecedented events may have occurred multiple times throughout history. Rather than futilely attempting to predict the future, we should strive to learn as many lessons as possible from the past. Studying history and obtaining relevant benchmarks, such as historical data of statistically significant groups over a longer time frame, helps to avoid the proximity bias and vividness bias, because a notable characteristic of the present world is that despite economic cycles being ubiquitous, people's financial memories are extremely short-term.

Considering problems from a historical perspective enables investors to surpass their emotions and remain rational. This is also the only way to succeed in investments.

Editor/Lambor