Source: US Stock Research Institute

Strong performance and a sharp drop in stock prices. What is the market worried about?

Major chip vendors for tech companies $Broadcom (AVGO.US)$ Announced its third-quarter earnings report for fiscal year 2024, which showed that the San Jose, California-based chip vendor surpassed expectations in both revenue and profit.

The company's AI-based revenue accelerated and continued to grow in the third quarter. However, as sales continued to weaken, Broadcom's non-artificial intelligence revenue continued to drag down its earnings performance. Despite this, Broadcom CEO Hock Tan announced on a conference call that the sales slowdown in its non-AI revenue has bottomed out.

However, his remarks did not give much of a boost to Broadcom's stock price, which fell 10% the day after the release of the third-quarter earnings report.

Strong performance, plummeting stock prices, what is the market worried about?

According to Gangtice Investment Research, Broadcom (AVGO.US) had strong results in the third quarter of 2024, with total revenue of 13.1 billion US dollars, an increase of 47% over the previous year. The AI business continues to grow, VMware orders accelerate, and revenue from non-AI semiconductors is stable.

VMware software revenue grew 200%, mainly driven by VMware's business model transformation. AI network revenue increased 43% year over year, driven by strong demand for AI network products from hyperscale cloud customers. Non-AI network revenue increased 17% month-on-month and is expected to continue to grow in the fourth quarter. Storage revenue increased 5% month-on-month and is expected to achieve medium to high single-digit growth in the fourth quarter. Wireless revenue increased 1% year over year and is expected to grow by more than 20% month-on-month in the fourth quarter. Broadband revenue fell 49% year over year and is expected to continue to decline in the fourth quarter. Industrial and other revenues fell 31% year over year and are expected to grow month-on-month in the fourth quarter. Broadcom expects total revenue for the fourth quarter to be around $14 billion, up about 64% year over year.

In fact, Broadcom's overall performance was excellent. Revenue increased 47% year over year to 13.072 billion US dollars, and Non GAAP diluted EPS increased 18% year over year to 1.24 US dollars, exceeding market expectations. However, after the announcement of the company's results, the stock price fell more than 8% after the market. The main reason was that the semiconductor solutions revenue growth rate for the current quarter slowed beyond expectations and fell short of expectations. At the same time, the company's performance guidance for the fourth fiscal quarter also fell short of expectations, causing market concerns.

At the same time, looking at semiconductor companies' stock price performance in this earnings season after the announcement, it was found that the vast majority of semiconductor companies' post-performance stock price performance was not optimistic. Take a look at it specifically:

(1) Nvidia announced a strong second-quarter report. Both revenue and net profit greatly exceeded market expectations, but the stock price plummeted by nearly 7% after the day's market and closed down 6.38% the next day.

(2) TSMC announced a strong second-quarter report. Both performance and guidance were very optimistic, but the stock price closed down 1.38% after the results.

(3) Asmack's second-quarter report strongly exceeded market expectations, but revenue guidance for the third quarter fell short of expectations, and the stock price closed down 12.74% after the results.

(4) AMD's performance growth in the second quarter was strong. The third quarter guidance was in line with expectations. After the results, the stock price increase narrowed to 4.36%, and the stock price fell 8.26% the next day. Additionally, we can also find that the Philadelphia Semiconductor Index has dropped nearly 20% since its July high.

So why is the stock price performance of semiconductor companies still not optimistic, even if their performance is excellent? The reasons are as follows:

(1) Market expectations are too high. After a huge increase in the previous period, driven by the AI wave, the market continues to raise performance expectations for semiconductor companies, especially expectations for future performance growth. Once the semiconductor company's performance guidelines do not meet the highest expectations and cannot absorb overvaluation, then there will be a clear correction in the company's stock price.

(2) AI input and output are poor or affect downstream demand. The current semiconductor market explosion is mainly due to the rise of the AI wave. The increase in semiconductor companies' performance comes from the increase in demand for AI chips from downstream customers. However, the investment and output ratio of major semiconductor customers in AI is not optimistic. As can be found in the second-quarter reports issued by major technology internet companies, huge AI capital expenses did not bring corresponding returns; on the contrary, they lowered profit margins. Therefore, in this context, if downstream customers cannot continue to increase capital expenses, semiconductor companies will face the problem of declining order growth and slowing performance growth.

(3) The high base led to an inevitable slowdown in performance growth. Semiconductors are a cyclical industry. 2023 and 2024 are explosive growth cycles for the industry. After 2025, as chip supply continues to increase and industry demand cools down, compounded by high base issues, the semiconductor industry's revenue growth rate will inevitably slow down.

Therefore, we can judge that the semiconductor industry is nearing the top of the industry cycle. As the company's performance growth slows after 25 years, the company's pricing needs to return to a reasonable level.

Strong AI revenue, smooth integration of VMware's business, and Broadcom is still able to compete

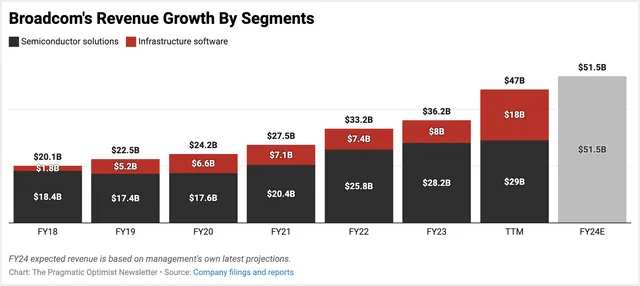

Judging from expectations, Broadcom's business growth will also return to a reasonable level. Currently, Broadcom's revenue sources are mainly divided into two major parts: semiconductor solutions and infrastructure software businesses. Among them, semiconductor solutions account for a relatively large share of revenue, over 50%, and the infrastructure software business has rapidly expanded since the acquisition of VMware.

The company's revenue increased 47% in the quarter, mainly benefiting from a 200% increase in the infrastructure software business and the acquisition of VMware. The impact of the acquisition is expected to continue into the next quarter, and then return to normal growth levels. Meanwhile, semiconductor solution revenue growth slowed to 5% this quarter, mainly due to weak growth in non-AI businesses, which led to a 49% decline in broadband revenue and a 41% decline in non-AI network revenue, offsetting the strong performance of the AI sector. Performance guidelines that fell short of expectations were also hampered by non-AI businesses.

In the long run, Broadcom's performance growth is still driven by the increase in demand for AI chips.

Broadcom's custom AI chips and network chips are essential components for building data center vendors to build AI systems, so Broadcom is unquestionably one of the core targets benefiting from the surge in AI demand. This quarter, the company raised its sales forecast in the AI sector again. It is expected that sales of AI components and custom chips will reach 12 billion US dollars in FY24, an increase of 9.1%. This is the second time that the company has raised expectations, and demand for AI is still very optimistic.

The company's management revealed that in the next 3-5 years, the potential market for the company's AI business is expected to reach 30 billion US dollars to 50 billion US dollars every year. Judging from the revenue of 12 billion US dollars in FY24, there is still room for double growth in the future, effectively driving the company's performance growth.

Meanwhile, Seeking Alpha analyst Uttam Day said that Broadcom continues to maintain its dominant position in the customized AI chip market, which has boosted the company's prospects due to the promotion of AI.

“In my previous notes, I highlighted the company's predictions relating specifically to sales related to artificial intelligence, which is expected to generate at least $11 billion in revenue from sales of the company's chips, networking products, and other components.

In the third-quarter earnings report released late last week, Broadcom's Tan announced that they currently expect sales in the artificial intelligence sector to be around $12 billion, higher than management's previous forecast for the 2024 fiscal year, and higher than the market's forecast of $11.8 billion. One reason for this increase is that the company is seeing benefits from VMware integration.

Although Broadcom's third-quarter consolidated revenue increased 34% year over year to $12 billion, in reality, the company's infrastructure solutions division took on most of the heavy responsibility. Broadcom's infrastructure solutions division's revenue was almost four times the reported revenue for the same period last year, reaching $5.8 billion. The integration of VMware solutions is the main reason for this segment's growth, accounting for $3.8 billion, or 66% of the $5.8 billion sales in the infrastructure solutions segment.

In a conference call discussing third-quarter earnings, Tan mentioned that VMware has booked millions of VCF (VMware Cloud Foundation) CPU computing costs. VCF is the latest version of VMware's full-stack server virtualization software, with annual subscriptions reaching $2.5 billion, an increase of 32% over the previous quarter. Tan also pointed to VMware's progress in integrating EBITDA. A thorough reform of VMware operations is still ongoing to bring it closer to Broadcom's overall software operating framework, which still keeps VMware on track to achieve its goals:

At the same time, we continue to reduce VMware costs. We cut VMware spending from $1.6 million in the second quarter to $1.3 million in the third quarter. When we acquired VMware, our goal was to achieve an adjusted EBITDA of $8.5 billion within three years of the acquisition. We are successfully meeting and even surpassing our FY25 EBITDA target in the next fiscal year.

Unlike the growing infrastructure solutions division, growth declined again after Broadcom's semiconductor solutions division first showed signs of re-acceleration in the second quarter.

Semiconductor solutions revenue declined 4.8% year over year to $7.3 billion in the third quarter. Strong demand from hyperscale enterprises for artificial intelligence networks and Broadcom's customized AI chip products drove a 43% year-on-year increase in the network products division of Broadcom's semiconductor solutions.

This advantage was offset by weak demand from enterprise customers in the semiconductor solutions sector, and weakness in other product areas unrelated to artificial intelligence. Revenue from non-artificial intelligence networks, server storage, and wireless and Broadcom products is either flat or severely losing money, and will continue to be at these levels in the next quarter, according to management's outlook.

However, Tan has repeatedly reiterated during the conference call that he believes the deceleration in non-artificial intelligence revenue has bottomed out:

In summary, here are the trends we're seeing in the semiconductor sector. Overall, our non-AI market has bottomed out, and we expect a recovery in the fourth quarter. Demand for artificial intelligence remains strong, and we expect AI revenue to increase 10% month-on-month in the fourth quarter to reach more than $3.5 billion. That would mean AI revenue in FY24 will reach $12 billion, higher than our previous expectations of over $11 billion.

Combining all of this with software, here's our prediction for the fourth quarter. We expect semiconductor revenue for the fourth quarter to be around $8 billion, up 9% year over year. For infrastructure software, we expect revenue of around $6 billion. As a result, we expect consolidated revenue for the fourth quarter to be approximately $14 billion, up 51% year over year.”

Analysts are adamant that Broadcom's valuation is far more than that

In the current market environment, we need to pay particular attention to semiconductor companies' performance growth prospects.

1. About Broadcom's trading strategy

From Broadcom's perspective, it is expected that AI customized chips will be the driving force for the company's performance growth, and the EPS growth rate will maintain double-digit growth in FY24 and FY25. In terms of shareholder returns, the company's dividend rate (TTM) is around 1.33%. No share repurchase plans have been announced, and shareholder returns are unattractive. The company's current market value is 711.359 billion US dollars, and the price-earnings ratio (TTM) is 131.97. Based on the profit expectations for FY24 and FY25, PE (forward) is 32x and 25x, respectively. The valuation is relatively reasonable, and there is limited room for stock price growth.

Investors with underlying shares are advised to use CoverCall's investment strategy to sell high-priced bullish options; investors who do not hold underlying shares can wait for a further correction in stock prices before taking the opportunity to buy.

2. Trading strategies for the semiconductor industry

Currently, the semiconductor boom is at the top, and the industry's valuation is high. It is recommended to pay close attention to changes in the US macroeconomic environment and the progress of AI technology. US macroeconomic data changes frequently, and the latest manufacturing data is not very optimistic. The non-farm payrolls data to be released tonight will have a major impact on the market.

The semiconductor industry is expected to fluctuate greatly in the short term and face the risk of a pullback. Currently, the most well-known leveraged ETF that shorts semiconductors is SOXS, but multi-leveraged ETFs lose a lot. Long-term holding is not recommended. Trend trading can be carried out, and short-term profits can be made to sell.

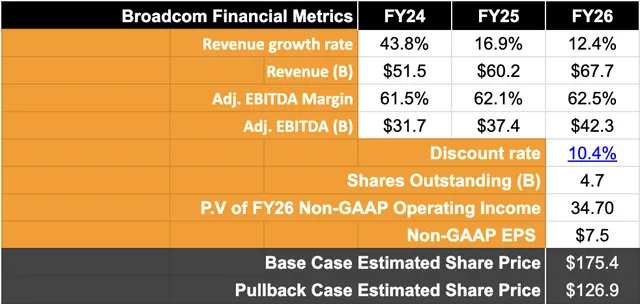

Taking into account management's upward forecast for the fourth quarter, the company's revenue is expected to grow by around 44% this year to around $52 billion. According to the third-quarter earnings report, my expectations for revenue growth of more than 20% for the 2026 fiscal year have not changed.

However, in terms of profit, I believe Broadcom has more room to grow. EBITDA profit margin after strong performance this quarter. I believe profit margins can be increased by at least 100 basis points by fiscal year 2026, which means profit margins will increase by 22% by fiscal year 2026. This profit increase should guarantee a profit multiplier greater than 35 times.

But considering the $4 billion annual interest expense I mentioned earlier, I think the expected price-earnings ratio of 23-24 times is reasonable. Taking into account the 10.4% discount rate and the 4.7 billion tradable share base, this represents a 29% increase from current levels.

The upside of the above model does not include potential dividends. At the time of writing, Broadcom's yield was 1.5%, and the consensus forecast is that the yield will grow to 2% in the 2026 fiscal year.

VMware integration risks and other factors to consider

One risk I would like to point out is that the market enters the usual seasonal pattern of the September depression, which will temporarily reduce the valuation multiples. In this case, I think the market will price Broadcom at a lower price-earnings ratio, close to the long-term price-earnings ratio of about 17-18 times the S&P 500, as questions about revenue growth and subsequent EBITDA profit margins have surged due to seasonal pessimism. This means that the target price is around $125-128, as shown in Chart D in the previous section.

One reason for the increase in revenue was its VMware integration, and people questioned Broadcom's imposition of its own software operating model on VMware. This has led some customers to switch from VMware to their peers, such as Nutanix (NTNX), reporting that any consequences of VMware integration have brought benefits. In this moment of doubt, I would alert investors to Hock Tan's acquisition-led growth strategy, which focuses entirely on acquiring companies, reallocating resources, and providing customized solutions, then marketing them to large enterprises and hyperscale enterprises.

This played a good role in Broadcom's numerous acquisitions, enabling Tan's team to price based on value and maintain their profit expansion strategy along the way. One commenter on the public forum, who appears to be a former VMware reseller, said they might have to “recommend that our customers do the same because most of them are small to medium businesses,” which reinforces Tan's right to eliminate SMEs and other small customers that are not Broadcom's focus.

Despite this, such media reports about unstable VMware integration may temporarily put some resistance to Broadcom's sentiment, leading to a correction in stock prices. This pullback will only create buying opportunities.

Edit/rice