According to Qunzhi Consulting's monitoring, China's independent display market shipped about 10.5 million units in the first half of 2024, with steady year-on-year performance.

The Zhitong Finance App learned that in 2024, China's independent display market showed a complex and dynamic trend in many aspects. Judging from the situation in the first half of the year, factors such as the growth of e-sports displays, the upgrade of office monitors, and the brand's low price strategy have all contributed to the development of the market. According to Qunzhi Consulting's monitoring, China's independent display market shipped about 10.5 million units in the first half of 2024, with steady year-on-year performance.

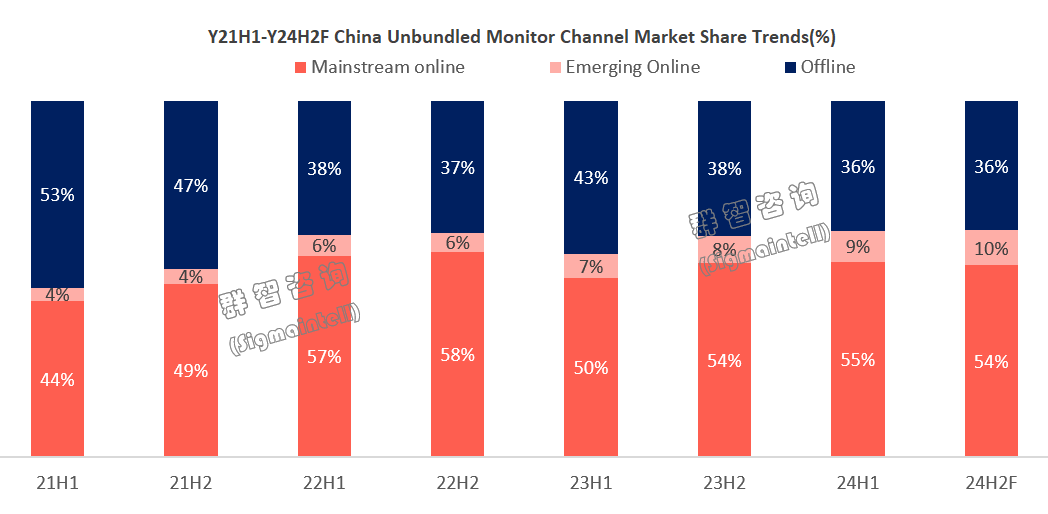

As demand in the independent display market in China has stabilized, channel abundance and brand vitality have continued to grow.

The share of offline channels in the standalone display market has declined, but they still occupy a mainstream position. Compared with the rapid development of online channels, offline channel shipments have shrunk slightly. According to Qunzhi Consulting's monitoring, offline channel shipments accounted for about 36% of total shipments in the first half of 2024, down 7 percentage points from the same period last year.

Online channels have maintained steady development, and mainstream e-commerce and emerging e-commerce complement each other, jointly promoting the development of online channels.

Mainstream online e-commerce relies on mature logistics distribution systems, perfect after-sales service, and extensive brand coverage to provide consumers with reliable shopping guarantees. Online mainstream e-commerce sales accounted for about 55% of total shipments in the first half of 2024, an increase of 5 percentage points over the same period last year.

Emerging online e-commerce businesses can more intuitively display product features and usage effects through influencer recommendations, live streaming, etc., to attract the attention of young consumers. Online emerging e-commerce sales accounted for about 9% of total shipments in the first half of 2024, an increase of 2 percentage points over the same period last year.

Currently, among the three major channels, brands have a relatively balanced layout in offline channels and mainstream e-commerce channels. Offline channels require high brand operation and management capabilities, so traditional brands with perfect offline channels are still the main ones. In the past, brands that were mainly offline made up for weak channels last year. However, looking at emerging e-commerce platforms, the leading brands are currently dominated by relatively flexible local brands. Among them, AOC, HKC (HKC), and Titanarmy (Titanarmy) quickly gained a place among them due to their good domestic reputation and sensitivity to the market.

Taking the first half of 2024 as an example, AOC's emerging e-commerce channel, which ranked number one, accounted for 7% of its shipments, which is relatively low, yet it accounts for 19% of emerging channels (15% in mainstream e-commerce). Huike's second-largest e-commerce channel accounts for 10% of its shipments, and it accounts for 14% of emerging channels (9% for mainstream e-commerce). In third place is Titan Legion. Emerging e-commerce channels account for 24% of its shipments, and 12% in emerging channels (4% in mainstream e-commerce).

Overall, the three channels have different characteristics. Offline channels and mainstream e-commerce channels need to be continuously stabilized as a guarantee of scale. In particular, mainstream e-commerce platforms are affected by the “catfish effect” of emerging e-commerce platforms, and brands cannot relax; while emerging e-commerce platforms provide new growth opportunities for brands, and brands can increase their investment in emerging e-commerce channels to seize market growth opportunities.

The competitive landscape of brands in the standalone display market continues to change. Traditional leading brands have further consolidated their dominant position in the market through active expansion of product lines and price strategies; international brands continue to make efforts in cost control and product innovation, and competition between international brands and local brands will become more intense. At the same time, with the development of the market, emerging brands occupy a place in the market with unique product characteristics and market positioning.

Office display market — traditional brands maintain competitive advantage:

AOC's overall market shipment volume was 1.605 million units, with a market share of 24%, and shipments fell 6% year on year. The online sales volume was 0.404 million units, the online market share was 12%, and sales volume decreased by 5% year on year. AOC has always occupied an important position in the office display market, has a high market share, and its market performance is stable.

The overall shipment volume of Lenovo (00992) was 1.102 million units, with a market share of 16%. The online sales volume was 0.096 million units, the online market share was 3%, and sales increased 91% year over year. Lenovo's online market has grown, and results have been achieved in expanding online channels and adjusting marketing strategies, further optimizing online sales channels, and consolidating and expanding its online market share.

The overall shipment volume of Philips (PHG.US) was 0.889 million units, with a market share of 13%. Shipments fell 9% year on year. The online sales volume was 0.146 million units, the online market share was 4%, and sales volume decreased by 18% year on year. Philips' performance in the overall market and online market was poor. This is mainly due to the lack of price advantages of its products compared to competitors and increased market competition.

Huike's overall shipment volume was 0.707 million units, with a market share of 11%, and shipments increased 4% year on year. The online sales volume was 0.175 million units, the online market share was 5%, and sales increased 3% year over year. Huike has maintained a steady growth trend in both the overall market and the online market. This is due to its cost-effective product strategy and constantly expanding sales channels.

Dell (Dell) shipped 0.589 million units overall, with a market share of 9%, and shipments increased 17% year over year. The online sales volume was 0.131 million units, the online market share was 4%, and sales volume decreased by 31% year on year. Dell's performance bottomed out and rebounded. Driven by active channel policies, it achieved a good recovery in the overall market, but the online market experienced setbacks. The online market is more price sensitive. Dell's product positioning and price strategy are mainly in the middle and middle end, and are more significantly affected by the downward price trend.

The overall shipment volume of Samsung (Samsung) was 0.331 million units, with a market share of 5%. Shipments fell 28% year on year. Online sales volume was 0.119 million units, online market share was 3%, and sales volume decreased 35% year over year. Driven by a profit-oriented strategy, Samsung changed from its original overall development strategy to a mid-to-high-end positioning strategy, so shrinking its market size became an inevitable trend. However, at the same time, Samsung still maintains a certain level of competitiveness in China's middle and high-end markets.

E-sports display market - local brands stir up the market:

AOC's overall shipment volume was 0.857 million units, with an overall market share of 23%, and shipments increased 22% year on year. The online sales volume was 0.421 million units, the online market share was 18%, and sales increased 21% year over year. AOC's overall shipping volume and online sales are high, and showing a clear growth trend. The rich price range and performance combination of its products can meet the dual needs of office user upgrades and e-sports players.

Huike's overall shipment volume was 0.581 million units, with an overall market share of 15%, and shipments increased 19% year over year. The online sales volume was 0.351 million units, the online market share was 15%, and sales increased 7% year over year. Huike's overall market share is stable, and shipments and online sales are growing steadily. Expand in the e-sports display market with a cost-effective product strategy. Pay attention to the balance between product performance and price, and provide competitive prices by optimizing the supply chain and production cost control.

Titan Legion's overall shipment volume was 0.45 million units, with an overall market share of 12%, and shipments increased 198% year over year. The online sales volume was 0.23 million units, the online market share was 10%, and sales increased 28% year over year. As a traditional e-sports professional brand, Titan Legion has achieved explosive growth, and its market share has increased rapidly. It accurately grasped the development opportunities of the e-sports market, focused on the field of e-sports displays. Product specifications and sales channels closely followed market trends, while cooperating with e-sports teams, game anchors, etc., enhancing the brand's influence in the e-sports industry.

The overall shipment volume of Asus (Asus) was 0.326 million units, with an overall market share of 9%, and shipments increased 62% year on year. The online sales volume was 0.138 million units, the online market share was 6%, and sales increased 31% year over year. The dual brand strategy has obtained good market feedback in terms of high quality and high performance positioning. The market share is relatively stable, and there has been a certain increase in shipments and online sales. As a well-known computer hardware brand, it has gained advantages in technology accumulation and brand reputation through category integration. In terms of brand building, Asus also focuses on cooperation with e-sports tournaments and events, enhancing the brand's popularity and reputation in the e-sports field.

Kangguan (KTC) shipped 0.35 million units, with an overall market share of 3%, and shipments increased 107% year on year. The online sales volume was 0.246 million units, the online market share was 11%, and sales increased 132% year over year. Overall shipments and online sales grew rapidly, and the performance was outstanding. Kang Guan is positioned as being friendly to the people and has a high cost performance ratio. In addition, it actively expands e-commerce channels and cooperates with e-commerce platforms to carry out promotional activities, increasing product visibility and sales.

The overall shipment volume of SANC (SANC) was 0.26 million units, with an overall market share of 2%, and shipments increased 219% year on year. The online sales volume was 0.226 million units, the online market share was 10%, and sales increased 454% year over year. Shengze rapidly emerged with aggressive market strategies. In terms of products, we continue to launch competitive new products, focusing on high cost performance and differentiated layout. Attract consumer attention by providing high-configuration and low-price promotional positioning.

Overall, in the 2024 office display market, traditional brands such as AOC and Lenovo still occupy a certain market position, but they are facing challenges from Chinese brands such as Huike. In the e-sports display market, local brands such as AOC, Huike, and Asus are facing challenges from emerging brands such as Titan Legion, Kanguan, and Shengse. Fierce market competition has prompted brands to continuously adjust their strategies to meet consumer needs and market changes.

In summary, the 2024 Chinese display market showed a complex and dynamic trend in many aspects. Judging from the situation in the first half of the year, factors such as the e-sports boom, low price strategy, and brand competition have all boosted the development of the market. In the forecast for the second half of the year, market demand trends, technology development direction, and changes in the competitive landscape also brought opportunities and challenges to the market.

In terms of channel layout, we recommend continuing to stabilize offline and mainstream e-commerce channels while increasing investment in emerging e-commerce channels; on the product side, focusing on cost performance balance and adjusting price strategies in a timely manner according to market demand; enhance e-sports promotion in homogenized competition, strengthen cooperation with e-sports teams, etc., and enhance the brand's influence in the e-sports field.