Ahead of the upcoming September FOMC meeting, the market is closely watching the latest nonfarm data, as it will have a decisive impact on future recession risks and the extent of Fed rate cuts.

The market is discussing whether the Fed will cut rates by 25 basis points or 50 basis points, especially after Powell reiterated the importance of the labor market in policy decisions at the Jackson Hole meeting. The possibility of a rate cut is being closely watched. However, the market's reaction has not formed a unified trend, and the performance of various asset classes is also different.

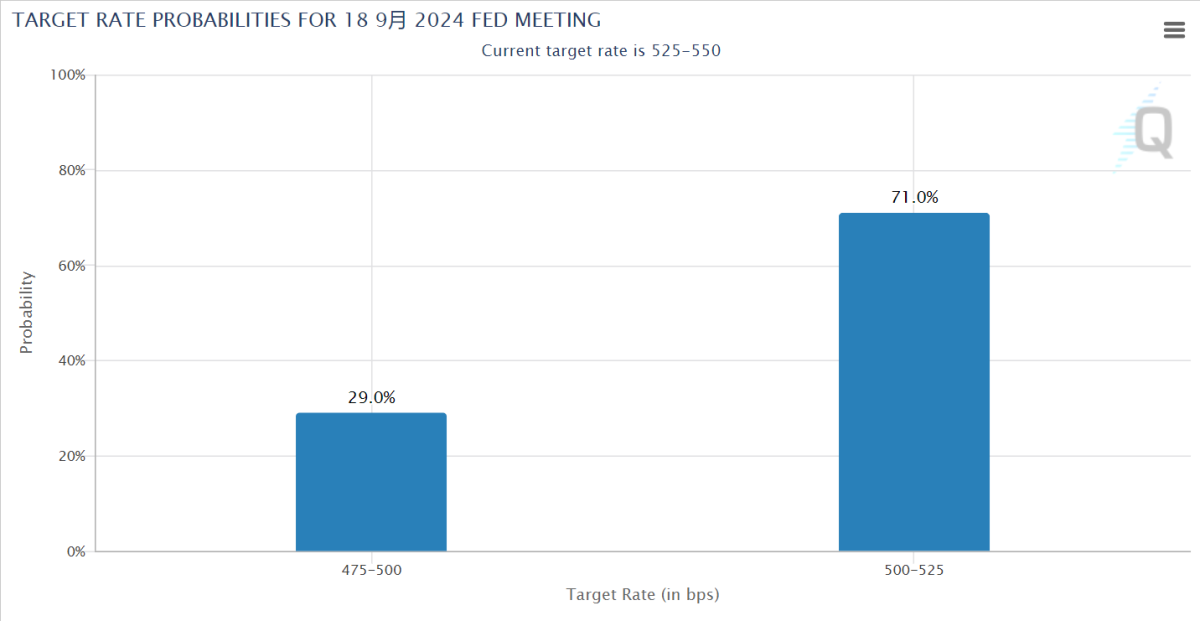

As of now, the probability of a 25 basis point rate cut reflected by CME interest rate futures has risen to 71%, while the expectation of a 50 basis point rate cut has fallen to 29%. Meanwhile, the 10-year US Treasury yield remains at 3.7%, gold has fallen after significant volatility, US stocks have declined again, and the US dollar index has seen a slight increase.

This indicates a significant divergence in the market's views on economic prospects and the extent of rate cuts. Investors are not only concerned about recession pressure, but also discussing whether a 25 basis point rate cut is enough to address the pressure of economic slowdown.

Nonfarm data and rate cut expectations

The latest nonfarm data did not provide a clear economic signal, making it difficult for the market to form a consensus. However, when it comes to employment or unemployment rates, the answer of whether it will be a 25 basis point cut or a 50 basis point cut seems to be completely opposite.

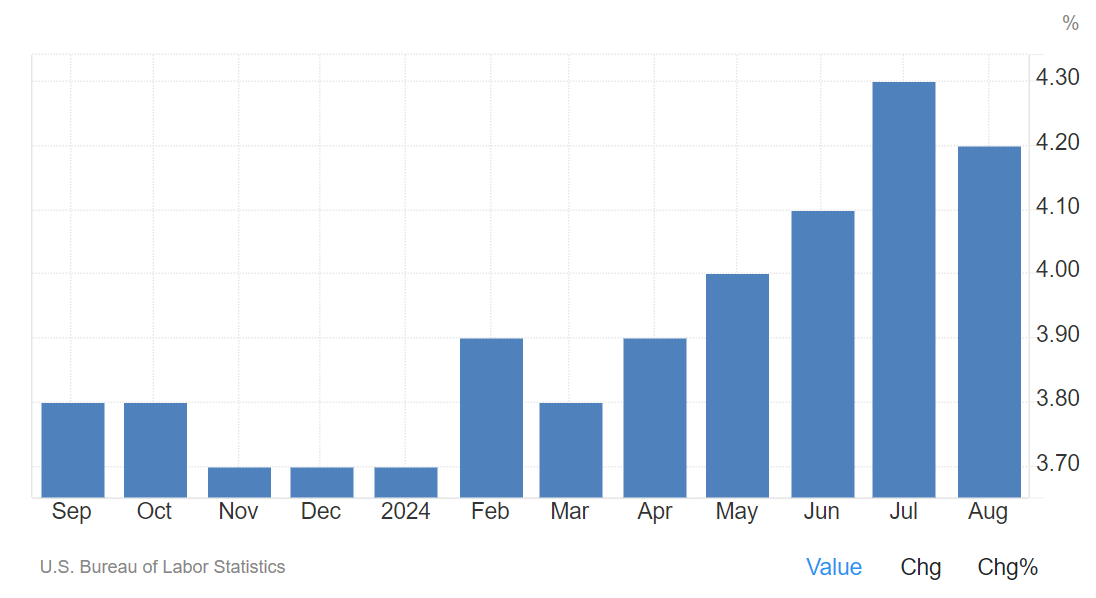

The unemployment rate rose to 4.3% in July, triggering the "Sam rule" and making the market more sensitive to the scale of subsequent rate cuts.

Although the nonfarm data fell short of expectations, it was not completely negative. The number of new jobs added was only 0.142 million, lower than the expected 0.165 million, and the data for the previous month was also revised down significantly to 0.089 million.

In August, the unemployment rate slightly decreased by 1 percentage point to 4.2% from 4.3%, and the number of temporarily unemployed decreased by 0.19 million, partially offsetting the previous employment losses due to weather conditions.

The weekly initial jobless claims number remains low, and layoffs are currently at a historical low. The layoff and dismissal rate in July slightly increased to 1.1%, still lower than the pre-pandemic level.

This means that although the job market is slowing down, it is not enough to indicate the severity of an economic recession. The market generally expects the data recovery this month to alleviate recession concerns and potentially dispel expectations of a 50 basis point interest rate cut. However, the degree of data recovery falls short of expectations, reinforcing the view that the job market is slowing down but not fully recessionary.

The frequency of interest rate cuts has become a current market focus.

When discussing the magnitude of interest rate cuts, there is significant disagreement in the market. A 25 basis point interest rate cut is still the benchmark expectation, mainly because there are no signs of deep recession at present.

Although a 25 basis point interest rate cut may not completely alleviate the market's recession concerns, the risk of a 50 basis point interest rate cut is that it could trigger greater economic panic.

Meanwhile, although the Federal Reserve has not officially started cutting interest rates, the market has already begun to feel the effects of loose monetary policy, especially in the real estate market and financing conditions.

Specifically, as the 10-year Treasury yield declines, 30-year mortgage rates have fallen to 6.4%, below the average rental yield of 7%. This has driven a recovery in existing home sales and new home sales saw a 10% month-on-month increase in July.

In addition, the demand for refinancing has also rebounded as mortgage rates have declined. In terms of direct financing, the credit spreads of high-yield bonds and investment-grade bonds are at historically low levels, and the decrease in financing costs has led to a substantial increase in the issuance of credit bonds, with a year-on-year growth of 20.6% from May to August in the USA.

How much is the asset included in the interest rate cut expectations?

Currently, different assets in the market have different responses to the expectations of interest rate cuts.

According to estimates, the US interest rate futures have factored in a 225 basis point interest rate cut expectation, with gold factoring in 83 basis points, copper at 77 basis points, and US bonds and stocks at 75 basis points and 29 basis points respectively. $SPDR Gold ETF (GLD)$ $S&P 500 (.SPX)$ $U.S. 10-Year Treasury Notes Yield (US10Y.BOND)$ $U.S. 2-Year Treasury Notes Yield (US2Y.BOND)$ $U.S. 20-Year Treasury Bonds Yield (US20Y.BOND)$ $U.S. 30-Year Treasury Bonds Yield (US30Y.BOND)$ $NASDAQ 100 ETF (QQQ)$

This means that unless new recessionary pressures emerge, the market's inclusion of interest rate cut expectations is already quite sufficient. As interest rate cut expectations are realized, the market will gradually shift from safe assets such as gold and US bonds to risk assets such as stocks and industrial metals.

Looking back at the interest rate cut cycle of 2019, similar situations have also occurred.

Prior to the first interest rate cut by the Federal Reserve in July 2019, the 10-year US bond yield had dropped from the high point of 3.2% to 1.5%. Despite experiencing multiple pullbacks in risk assets during this period, with the improvement in economic expectations and the bottoming out of long-term bond yields, gold gradually peaked, while US stocks and copper prices began to rebound. Similarly, in the current cycle, with the realization of interest rate cuts, market expectations for asset rotation are expected to undergo similar changes.

Summary

Overall, there is still significant uncertainty in the market about the interest rate cut at the September FOMC meeting. While a 25 basis point rate cut is widely seen as the base case, expectations for a 50 basis point rate cut have not completely faded.

As economic data is gradually revealed and market expectations are continuously adjusted, asset prices may experience volatility. However, overall, the market has already partially priced in the expectations of an interest rate cut. Future investment opportunities may be more focused on assets that could benefit from the rate cut, such as stocks and industrial metals.