Source: China International Capital Corporation Strategy. Author: Wang Hanfeng, Liu Gang et al. After a significant sell-off in the early part of last week, overseas Chinese capital stocks rebounded strongly in the middle of the week. At the beginning of the week, investors' sentiment deteriorated further due to multiple domestic and international factors. Under the pressure of external fund outflows, there was an impact on liquidity in the market and the market performance plummeted. Fortunately, this liquidity shock eased somewhat after policy stabilization signals on Wednesday, and the market subsequently showed an almost linear upward trend. After the roller coaster market last week, we tend to believe that the panic-style rapid sale in the early stage may be temporarily over, and the market may gradually enter a consolidation and bottoming period. However, the recovery of emotions still needs some time, mainly due to: 1) The outflow of overseas funds, especially the reduction of large-scale sovereign funds, is difficult to see a significant reversal in the short term; 2) The short selling ratio in the market is still high; 3) The geopolitical tensions, Sino-US relations, epidemic, domestic policies, and uncertainties in regulation have not yet completely weakened. Therefore, looking ahead, whether the market rebound can continue depends on: 1) Whether positive policy signals can be specifically implemented; 2) Whether external uncertainties will be alleviated.

Authors: Liu Gang, Wu Wei, etc.

The current market has entered a key window for internal and external factors. Internally, the recent market has paid extensive attention to changes in domestic policies, especially measures regarding existing housing loans and mortgage conversions. According to calculations by China International Capital Corporation, if the average interest rate of existing mortgages is reduced by about 54-60 basis points, taking a 30-year RMB loan of 1 million yuan as an example, under the calculation of equal principal and interest payments, the amount that needs to be repaid each month is expected to decrease by about 500 yuan. However, even if this is implemented, existing housing loans only partially address early repayment and expenditure pressures, and do not provide much help in boosting housing demand. Of course, the Federal Reserve's interest rate cut is about to begin, which can further open up space for domestic interest rate cuts, but the extent of the cut may still be limited.

Externally, the September US election and the opening of the interest rate cut window are approaching. The non-farm payrolls released on Friday night did not completely calm the market's recession concerns, nor did it provide a clear signal of the extent of interest rate cuts. In addition, with the second debate of the US election on September 10th, there have been more changes in overseas markets recently, and short-term uncertainties will have an impact on the market.

On the fundamental level, the current economic growth momentum is still weak. From the perspective of micro-enterprise profits, in the first half of the year, the profits of overseas Chinese-funded stocks increased slightly by 2.3% year-on-year, which is faster than the 0.2% growth in 2023. However, this is more driven by costs, while demand has declined. In addition, companies generally adopt a contraction strategy, so the increase in return on equity (ROE) is mainly due to increased profit margins driven by costs. The current market consensus expects a nearly 20% year-on-year growth in the second half of the year, which we believe may be overly optimistic. However, it is worth noting that Hong Kong stock profits are still better than A-shares, with a difference of -3%. This is mainly because the profit structure of Hong Kong stocks is more advantageous: 1) The proportion of new economy in the industry structure is high; 2) The contribution effect of top companies is more pronounced. This once again supports our previous view that the flexibility of Hong Kong stocks is still greater than A-shares, and structural factors continue to be the main theme.

In summary, the short-term uncertainty in the domestic and international environment may continue to bring volatility, and we still believe that the flexibility of Hong Kong stocks is greater than A-shares. In terms of allocation, the growth sectors that benefit from interest rate cuts in the short term may have higher flexibility, but in the medium term, the main theme is still a structural market with range fluctuations, corresponding to dividends + technology growth.

Market trend review

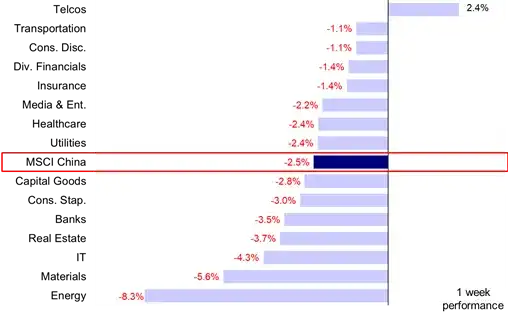

The Hong Kong stock market experienced a correction this week, with all major indices falling. Among them, the Hang Seng China Enterprises Index fell 3.6%, the Hang Seng Index fell 3.0%, the MSCI China Index fell 2.5%, and the Hang Seng Tech Index fell 2.0%. In terms of sectors, only the telecommunications sector (+2.4%) led the gains, while all other sectors declined. Among them, the energy (-8.3%), raw materials (-5.6%), and information technology (-4.3%) sectors were the biggest losers.

Chart: Only the telecommunications sector rose, while the energy and raw materials sectors fell.

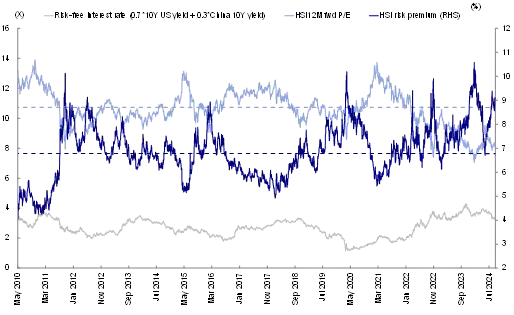

Since the peak at the end of May, the Hong Kong stock market has fallen nearly 10%. Since mid-May, we have been reminding investors that this round of rebound is mainly driven by the funding side and emotions. Therefore, with the market entering the overbought range, investors' divergences and profit-taking are not surprising. Assuming that the risk premium is fully restored to the level of the high point at the beginning of 2023, the corresponding target index level of the first stage of the Hang Seng Index is 19,000-20,000 points (see May 12th "The market is approaching our first stage target" and May 26th "not surprisingly taking profits"). In the past few weeks, overseas funds, especially value-oriented active foreign funds, have flowed out again. The outflow scale this week has increased from USD 93.24 million last week to USD 340 million. This can also provide proof ("Active Foreign Funds Maintain Weakness"). However, with the recent continuous decline of the market, especially A shares falling below 3,000 points again, concerns about the Hong Kong stock market falling to the previous low are also increasing. In this regard, we are not so worried, although we have always believed that further upward momentum needs more catalysts to start, it will not completely give up all the gains, and the Hang Seng Index around 18,000 points can get some support, and looking back at this week's market performance also confirms our previous judgment ("temporary pause or end of rebound"). In addition, compared with A shares, which have returned all gains since March, the Hong Kong stock market has shown obvious resilience, which is consistent with our judgment that the Hong Kong stock market is better than A shares ("The Hong Kong stock market still has a comparative advantage").

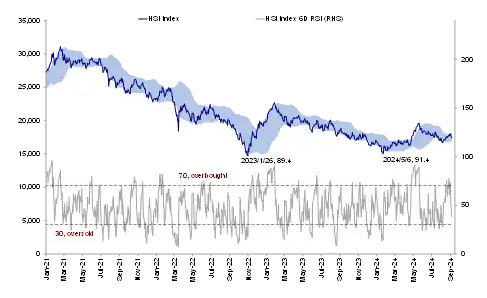

The Hong Kong stock market has fallen for four consecutive trading days this week, ending the independent trend of four consecutive weeks of gains since August and outperforming the A-share market. Against the backdrop of several technical indicators that have clearly rebounded or even overbought (short selling accounted for a fall to 16%, and the RSI also indicates that the market has reached overbought levels), a certain amount of correction was not unexpected. Under the influence of escalating concerns about overseas recession and uncertain domestic policy expectations, the risk premium has once again risen to a high point of 9.1% since early August. In terms of sector performance, sectors represented by energy, materials, and banks have continued to decline in dividends, while the previous week's market led by insurance, essential consumption, and real estate did not continue.

Chart: The risk premium of the Hang Seng Index quickly rebounded from 8.6% last week to 9.1%.

Chart: Relative Strength Indicator (RSI) shows that Hong Kong stocks are approaching overbought levels.

The current market is entering a key window period for internal and external factors. Internally, the recent market has been widely concerned about changes in domestic policies, especially the measures regarding existing mortgage loans and conversion to mortgages. The significant interest rate difference (about 60bp) between existing mortgage loans (about 4%) and new mortgage loans (new mortgage loan interest rate as of June is 3.45%) has led to a high prepayment rate (14%). Opening up the conversion to mortgages would help to alleviate the repayment pressure on residents to a certain extent, ease deleveraging on the household side, and partially boost consumption.

According to the calculation of China International Capital Corporation, under two scenarios of whether to re-open the conversion to mortgages and the scope of conversion to mortgages, if the average interest rate on existing mortgages is lowered by about 54-60bp, the borrowers' interest expenses will be reduced by about 200-240 billion yuan per year, corresponding to 0.4%-0.5% of urban residents' disposable income in 2023 and the total retail sales of social consumer goods in 2023. Taking an individual with a 30-year RMB loan of 1 million yuan as an example, under equal monthly installment payments, the amount to be repaid each month is expected to decrease by around 500 yuan. However, even if realized, the existing mortgage loans will only partially solve the early repayment and expenditure pressure, and will not provide significant help to boost housing demand, mainly due to the fact that the current new mortgage loan interest rate (3.45%) is still significantly higher than rental yield (mostly below 2%) in major cities.

Of course, the imminent rate cut by the Federal Reserve can further open up room for domestic rate cuts, but the magnitude of the rate cut may still be limited, considering the following factors: 1) Last week, the head of the Monetary Policy Department of the central bank, Zou Lan, stated that the further downward movement of loan and deposit rates is still subject to certain constraints due to factors such as the narrowing net interest margin of banks. 2) The constraint of the renminbi exchange rate on rate cuts still exists, which is also the reason why we previously emphasized that the impact of the Federal Reserve's rate cuts may be smaller than the US presidential election.

Externally, the US presidential election and the window for interest rate cuts in September are about to open. On Friday night, the last data on non-farm payrolls before the September FOMC meeting was released in the US, but the overall results disclosed were more moderate, not completely alleviating market concerns about a recession, and did not provide a clear signal of the magnitude of interest rate cuts. The market is still caught between greater recessionary pressures and insufficient rate cuts. In addition, the second debate of the US presidential election on September 10th and recent uncertainties in overseas markets have led to more variables. Considering that the Hong Kong stock market is more sensitive to external disturbances compared to the A-share market, this will have an impact on the market in the short term.

Chart: If the risk premium returns to the level of mid-year last year, the corresponding Hang Seng Index is around 19,000; if the profit growth is 10%, the corresponding point is 21,000.

Fundamentally, the current economic growth momentum remains weak. In terms of prices, in the first week of September, consumer prices for vegetables and fresh meat, as well as industrial metal prices including coking coal, rebar steel, and copper and aluminum, all weakened compared to the previous week; In terms of production, blast furnace capacity utilization and other indicators showed a slight recovery from the previous week; In terms of exports, the crude oil transportation index and the export container index have shown a third consecutive week of contraction compared to the previous week.

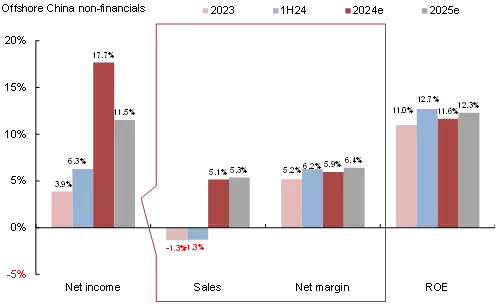

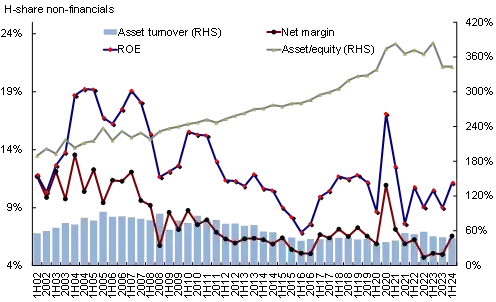

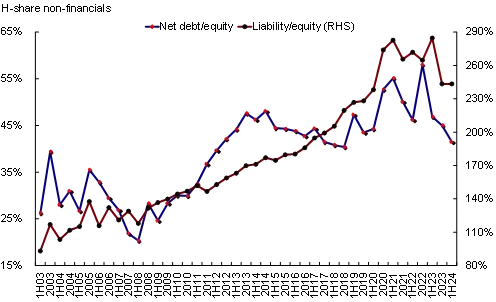

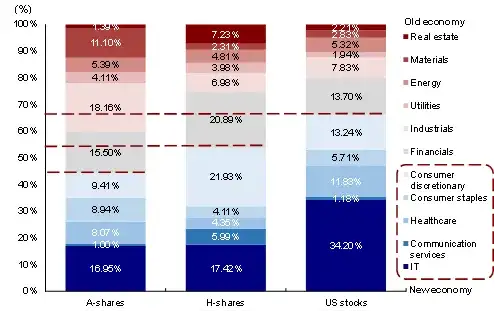

From the perspective of micro-enterprise profits, overseas Chinese-funded stocks have basically completed the disclosure of their 2024 interim performance. In the first half of the year, non-financial industry income declined by 1.3% compared to the same period last year, remaining weak, and profits increased by a slight 2.3% compared to 0.2% in 2023, indicating a slight acceleration. However, this is mainly driven by cost, while demand has actually declined. In addition, companies have generally adopted a contraction strategy, with capital expenditures and net debt ratio declining year-on-year in the first half of the year, so the increase in return on equity (ROE) is more due to cost-driven profit margins. The current market consensus expects a 10% growth in full-year overseas Chinese-funded stocks, implying a nearly 20% year-on-year growth in the second half, which we believe may be overly optimistic. However, it is worth noting that Hong Kong's profits are still better than A shares' -3%, mainly because Hong Kong's profit structure is more advantageous: 1) In terms of industry structure, Hong Kong has a higher proportion of new economic stocks and a lower proportion of midstream manufacturing; 2) In terms of concentration, the contribution effect of leading companies is more significant. This once again supports our previous view that Hong Kong stocks still have greater resilience than A shares, and structural trends remain the main theme.

Chart: Declining income drags down the growth rate of the first half of the year

Chart: The increase in net profit margin is the main reason for the slight growth in profits

Chart: Leverage remains stable in the first half of this year...

Chart:...Debt-to-equity ratio decreases, proportion of company's cash holdings increases, and the company's financial structure becomes more conservative.

Chart: Hong Kong stocks have the advantage in terms of profit and earnings structure compared to A shares.

Overall, the short-term uncertainty in the domestic and international environment may continue to bring volatility, and we still believe that Hong Kong stocks have greater flexibility than A shares. In terms of allocation, growth sectors that benefit from interest rate cuts in the short term may have higher flexibility, such as semiconductors, automobiles (including new energy), media and entertainment, software, and biotechnology. However, in the medium term, the structural trend of range-bound volatility remains the main theme. The current 10-year US Treasury bond yield of 3.7% has already fully priced in rate cuts. If the risk premium returns to the level of last year, the corresponding Hang Seng Index level would be around 19,000. If earnings grow by 10% on this basis, the corresponding Hang Seng Index level would be 21,000. In the medium term, dividends and technology growth are the main themes: 1) Overall returns are declining, corresponding to stable returns from high dividends and share buybacks, namely "cash cows" with ample cash flow, from cyclical dividends to banking dividends, and then to defensive low volatility dividends; 2) Local leverage, such as technology growth driven by industry growth (internet, gaming, education) or policy support (technology hardware and semiconductors).

Specifically, the main logic that supports our above views and the changes that need to be focused on this week are mainly as follows:

1) The US ISM Manufacturing PMI for August was lower than expected for the fifth consecutive month, but showed a rebound from the previous month. The August US ISM Manufacturing PMI rose to 47.2, lower than the market expectation of 47.5, but higher than July's 46.8. In terms of sub-indices, the forward-looking new orders sub-index declined to 44.6, indicating a slowdown in demand. The supply delivery and output sub-indices declined, reflecting ongoing production constraints.

2) Non-farm payroll data for August in the US fell slightly below expectations, but wages showed a small increase compared to the previous month. The US added 0.142 million new jobs in August, lower than the expected 0.165 million, but higher than the previous value of 0.114 million. Among them, temporary unemployment decreased by 0.19 million, household survey-based new jobs increased by 0.168 million. As a result, the unemployment rate dropped from 4.3% last month to 4.2%, and wages showed a small increase compared to the previous month (rising from 0.2% to 0.4% on a monthly basis, and from 3.6% to 3.8% on a yearly basis).

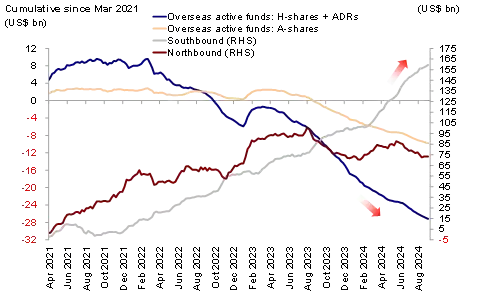

3) This week saw inflows of southbound funds and continued outflows of overseas active funds. Specifically, data from EPFR shows that overseas active funds continued to flow out of overseas Chinese equities markets this week, with a net outflow of approximately 0.21 billion USD, narrowing from 0.24 billion USD in the previous week. This marks the 69th consecutive week of outflows. At the same time, overseas passive funds continued to flow in with a net inflow of 0.17 billion USD (remaining flat compared to the previous week's outflow of 0.17 billion USD). Southbound funds continued to flow in this week, with an accumulated inflow of 9.27 billion HKD, expanding from the previous week's inflow of 5.05 billion HKD.

Chart: Overseas active funds continue to flow out of overseas Chinese stock markets

Key events to watch

On September 9th, China's CPI and PPI for August will be released; on September 10th, China's import and export data for August will be released; on September 11th, financial data will be released.

Editor/Jeffy