Futures Morning Peak - Audio Version

Macro News

According to the data from the Shanghai Shipping Exchange, as of September 6, 2024, the Shanghai Export Container Freight Index (Composite Index) was 2726.58 points, a decrease of 236.80 points compared to the previous period. The China Export Container Freight Composite Index was 1912.46 points, a decrease of 3.1% compared to the previous period.

China has requested consultations with Canada at the World Trade Organization regarding the additional tariffs imposed on Canadian electric vehicles, steel, and aluminum products. Canada has ignored the WTO rules, seriously undermining the rules-based multilateral trading system, disrupting the global supply chain of electric vehicles, steel, aluminum, and other industries. China firmly opposes this and urges Canada to comply with WTO rules and immediately correct its wrongdoings.

Citigroup traders are betting on the Federal Reserve cutting interest rates by 50 basis points three times this year, which exceeds market expectations and the bank's economists' predictions. Citigroup's short-term interest rate trading department stated that if the Fed sees weakness in the labor market, it will actively ease its policies.

The "Special Long-Term National Bond Fund Supports the Implementation Plan for the Trade-in of Consumer Goods" has been released in Shenzhen. It supports the trade-in of personal passenger vehicles, new energy buses, household appliances, home improvement, and other eight major areas. The goal is to achieve approximately 0.07 million vehicles replaced through the trade-in program by the end of 2024, approximately 1 million units of sales for household appliances, approximately 0.051 million households transformed and upgraded through home improvement, approximately 0.25 million electric bikes updated, and approximately 1,300 operating trucks and city buses updated.

According to the U.S. Bureau of Labor Statistics, the nonfarm payroll employment increased by 0.142 million people in August, accelerating compared to July, but lower than the market expectation of 0.16 million people. The June nonfarm payroll employment was revised down from 0.179 million people to 0.118 million people, and the July nonfarm payroll employment was revised down from 0.114 million people to 0.089 million people. After the revision, the total nonfarm payroll employment for June and July was lower by 0.086 million people compared to the previous estimate.

According to Dalian Commodity Exchange, the trading schedule for the Mid-Autumn Festival in 2024 is as follows: The market will be closed from September 15th (Sunday) to September 17th (Tuesday), and will resume normal trading on September 18th (Wednesday). September 14th (Saturday) is a weekend holiday. There will be no night trading on the evening of September 13th (Friday). The call auction for all contracts on September 18th (Wednesday) will be from 08:55 to 09:00 in the morning. Night trading will resume on the evening of September 18th (Wednesday).

Global futures market dynamics

1. Domestic commodity futures night trading closed generally down, energy and chemical products performed weakly, soda ash fell 3.83%, low-sulfur fuel oil fell 3.4%, crude oil fell 3.05%, RBOB gasoline fell 2.65%, glass fell 1.96%, PTA fell 1.75%, LPG fell 1.66%. Black series fell across the board, with coking coal down 3.47%, coke down 3.05%, iron ore down 2.35%, hot rolled coil down 1.86%, and rebar down 1.83%. Most agricultural products fell, with cotton down 1.66%, cotton yarn down 1.64%, palm oil down 1.16%, and soybean oil down nearly 1%. Basic metals fell across the board, with lead in Shanghai down 1.39%, stainless steel down 1.26%, nickel in Shanghai down 1.08%, copper in Shanghai down 1.07%, aluminum in Shanghai down 0.91%, tin in Shanghai down 0.29%, and zinc in Shanghai down 0.22%. Gold in Shanghai fell 0.63%, and silver in Shanghai fell 3.2%.

2. International precious metal futures fell across the board, with COMEX gold futures down 0.64% at $2,526.8 per ounce, a weekly decline of 0.03%, and COMEX silver futures down 2.85% at $28.27 per ounce, a weekly decline of 3%.

3. International oil prices fell across the board, with U.S. oil October contract down 1.43% at $68.16 per barrel, a weekly decline of 7.33%; Brent crude November contract down 1.68% at $71.47 per barrel, a weekly decline of 7.1%.

4. Most London base metals fell, with LME copper futures down 1.52% at $8,954 per tonne, a weekly decline of 3.04%; LME zinc futures down 1.19% at $2,705 per tonne, a weekly decline of 6.63%; LME nickel futures down 1.36% at $15,860 per tonne, a weekly decline of 5.4%; LME aluminum futures down 1.56% at $2,341.5 per tonne, a weekly decline of 4.31%; LME tin futures up 0.22% at $30,840 per tonne, a weekly decline of 4.66%; LME lead futures down 1.25% at $1,970 per tonne, a weekly decline of 4.04%.

5. Chicago Board of Trade (CBOT) agricultural futures main contracts fell across the board, with soybean futures down 1.86% at 1004.5 cents per bushel, a weekly increase of 0.45%; corn futures down 1.1% at 406.25 cents per bushel, a weekly increase of 1.31%; wheat futures down 1.35% at 567 cents per bushel, a weekly increase of 2.81%.

Black series Hot News

1. According to Mysteel statistics, the total import iron ore inventory at 45 ports nationwide was 154.0895 million tons, an increase of 0.3657 million tons compared to the previous period, with an average daily port clearance volume of 3.0274 million tons at 45 ports, an increase of 0.0275 million tons compared to the previous period. The total import iron ore inventory at 47 ports nationwide was 160.7895 million tons, an increase of 0.4657 million tons compared to the previous period, with an average daily port clearance volume of 3.1794 million tons, an increase of 0.0195 million tons compared to the previous period.

According to Mysteel's survey, the blast furnace operating rate of 247 steel mills was 77.63%, an increase of 1.22 percentage points compared to the previous week and a decrease of 6.76 percentage points compared to the same period last year. The average daily output of pig iron was 2.2261 million tons, an increase of 0.0172 million tons compared to the previous week and a decrease of 0.2563 million tons compared to the same period last year.

Minister Huang Runqiu of the Ministry of Ecology and Environment stated that by the end of this year, the national carbon emissions trading market will include key emitting industries such as steel, cement, and aluminum smelting in addition to the existing power industry. Further improve the carbon pricing mechanism and accelerate the establishment of a carbon footprint management system.

According to Steel and Silver E-commerce, the total inventory of steel in urban areas this week was 9.4018 million tons, a decrease of 0.4897 million tons compared to the previous week (-4.95%). It includes 40 cities and a total of 142 warehouses.

Shenzhen Agricultural Products Group News

According to Wind data, as of the week ending September 6, the profit of self-bred and self-raised pig farming was 559.36 yuan per head, and on August 30, it was 542.76 yuan per head; the profit of imported pig farming was 359.80 yuan per head, and on August 30, it was 342.02 yuan per head.

According to the China Sugar Association, the national sugar production in the 2023/2024 sugar season is expected to reach 9.9632 million tons, an increase of 0.99 million tons compared to the previous year, with a growth rate of 11.03%. As of the end of August, the cumulative sales of sugar nationwide reached 8.861 million tons, an increase of 0.7747 million tons compared to the same period last year, with a growth rate of 9.58%; the cumulative sugar sales rate was 88.94%, a decrease of 1.2 percentage points compared to the previous year.

India plans to extend its sugar export ban for the second consecutive year to cope with the prospect of declining sugarcane production. According to government sources, India also plans to raise the price of ethanol purchased by oil companies from sugar mills by more than 5% starting from November to promote biofuel production. It is expected that sugar production in the next 2024-25 season may decrease from 34 million tons this year to 32 million tons.

The latest forecast by the Food and Agriculture Organization of the United Nations for global grain production in 2024 has been revised down by 2.8 million tons from July, mainly due to the downward revision of prospects for coarse grain crops. Currently, the global grain production in 2024 is expected to be 2.851 billion tons, which is basically the same as the level in 2023.

5. Zhengzhou Commodity Exchange issued a risk alert letter. There are many uncertain factors affecting the rapeseed meal, vegetable oil market recently, and the prices fluctuate greatly. All member units should strengthen investor education and risk prevention work, and remind investors to participate rationally and trade legally.

6. The Southern Peninsular Palm Oil Millers' Association (SPPOMA) data shows that from September 1st to 5th, 2024, the palm oil yield in Malaysia increased by 7.38% and the oil extraction rate decreased by 0.36%, resulting in a 5.37% increase in production.

7. According to the U.S. Department of Agriculture, the net soybean sales for the 2023/2024 marketing year were -0.228 million tons, compared to -0.144 million tons the previous week. The net sales for the 2024/2025 marketing year were 1.659 million tons, down from 2.616 million tons the previous week. The net soybean sales to China for the 2023/2024 marketing year were -0.102 million tons, compared to 0.063 million tons the previous week. The net sales to China for the 2024/2025 marketing year were 1.002 million tons, down from 0.87 million tons the previous week.

8. According to data released by the Malaysian Palm Oil Association (MPOA), the estimated palm oil production in Malaysia from August 1st to 31st increased by 4.52%. The production increase was 3.74% in the Malay Peninsula, 6.03% in the East Coast, 7.33% in Sabah, and 3.66% in Sarawak.

Energy and Chemicals News

1. According to Zhuo Zong Information, the latest data shows that as of the week ending September 5th, the overall production of styrene in China was 0.3051 million tons, an increase of 0.0073 million tons or 2.45% from the previous week. The factory utilization rate was 70.06%, an increase of 1.69% from the previous week.

2. According to Wind data, as of September 5th, the methanol inventory at East China ports was 0.6081 million tons, which increased by 0.0273 million tons compared to the same period last week.

3. The Ministry of Energy of Kazakhstan stated that during the planned maintenance period in October, compensatory oil production cuts will be made to offset the OPEC+ production reduction measures.

Metal Hotspot News

According to Mysteel's research, on September 6th, the first production line of the KPS nickel-iron project in Indonesia (12 RKEF production lines) was successfully fired and the iron is expected to be produced in early October, with an additional nickel metal output of 1,200 tons per month for each production line after smooth production.

According to data from the Shanghai Futures Exchange, copper inventories decreased by 26,371 tons last week, aluminum inventories decreased by 3,973 tons, zinc inventories decreased by 78 tons, lead inventories increased by 4,674 tons, nickel inventories decreased by 169 tons, and tin inventories decreased by 1,017 tons.

According to Fubao Information, the decline in lithium carbonate prices does not seem to stop the enthusiasm for project construction, and there are still many new projects to be put into production in China in 2024. Overall, the capacity waiting to come online in 2024 includes: 0.11 million tons of lithium carbonate, 0.035 million tons of lithium hydroxide, 0.03 million tons of lithium salt, and 0.78 million tons of lithium concentrate.

According to a report from Bank of America, the fundamentals of tin remain solid, with an expected average price of $37,000 per ton by 2026, compared to the previous forecast of $32,500 per ton.

Praising "Periods" - Revealing the Trading Logic of Commodity Trading!

When will the black series rebound from the fall?

One German Futures analysis suggests that the next two weeks are critical as we transition from the slow to busy season in September. After the price drop, speculative demand has almost disappeared, but attention can still be paid to exports, construction starts, and improvements in funding. To stabilize and rebound, it is necessary to see verification of production cuts or continuous destocking. Rebar is about to face a challenge to support at the key level of 3,000 yuan, and if the bearish part takes profits along with a temporary easing of supply and demand contradictions, a strong basis may bring a rapid oversold rebound. However, looking at the medium term, the total demand increment is insufficient, and the complete resolution of industry contradictions will inevitably face the clearance of some production capacity. Whether in the upstream, midstream, or downstream, there will be a long period of profit pressure. Therefore, the suggested strategy is still to mainly build short positions in the medium term and be certain of shorting commodities. There is a large space for shorting iron ore.

With a combination of bullish factors, is it time to bottom out soybean meal?

China Securities Futures Analysis pointed out that improved export of soybeans, low water level in the Mississippi River, hot and dry weather in Brazil, and short covering by managed funds have collectively driven the rebound of CBOT soybeans this week, with CNF prices also rising. As new soybean harvest approaches, we expect valuation upside for soybean products to be somewhat limited in the short term. Subsequently, the market focus will shift to new soybean exports and weather conditions in South America. On the domestic front, the timing of valuation-based soybean meal destocking is approaching, coupled with the impact of the stronger soybean cost transmission and the anti-dumping incident on rapeseed meal. We believe that in the short term, given the high soybean inventory and the lack of incentive for oil plants to reduce production, the weak position of soybean meal on the supply side is expected to persist for some time.

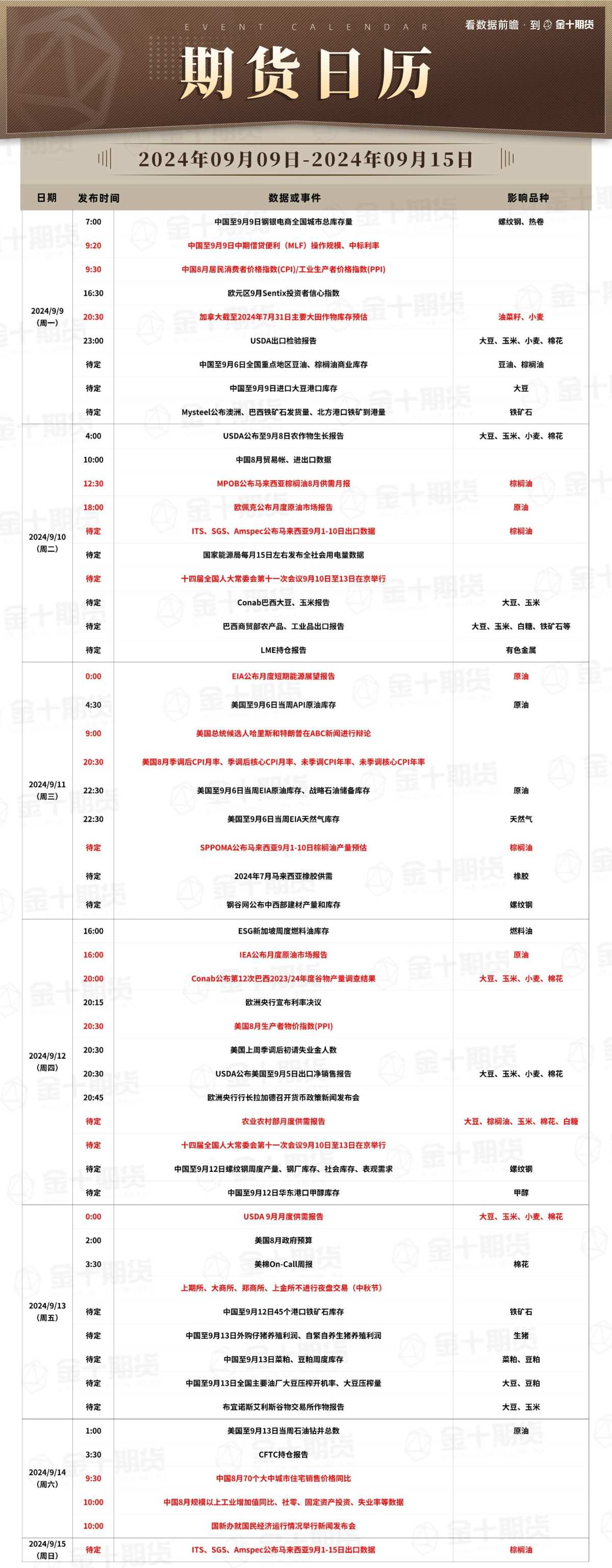

This week's important futures data and events at a glance

On September 9th at 9:30, China's CPI and PPI data for August will be released. Market analysts believe that due to factors such as weather, the year-on-year increase in CPI may further rise in August; domestic demand is stable, coupled with the high base effect of the same period last year, the year-on-year decline in PPI may widen again.

On September 10th at 12:00, MPOB will release the August monthly report on Malaysian palm oil. Reuters survey shows that due to weak export demand, Malaysian palm oil stocks are expected to rise to the highest level in six months in August. Darren Lim, a commodity strategist at Singapore broker PhillipNova, said that although stocks are expected to rise, they should still be at a manageable level, and production will largely depend on export demand and any potential changes in biodiesel regulations. Pay attention to the data in the monthly report and compare it with expectations.

On September 10th, ITS, SGS, and Amspec will announce the export volume of Malaysian palm oil from September 1st to 10th. ITS previously released data for September 1st to 5th, showing that Malaysian palm oil exports increased by 9.2% compared to the same period last month. Watch to see if this trend continues in the data this time.

On September 10th, OPEC will release its monthly oil market report. The July report projected a global crude oil demand growth rate of 2.11 million barrels per day in 2024, down from the previous expectation of 2.25 million barrels per day. The forecast for global crude oil demand growth in 2025 is 1.78 million barrels per day, down from the previous expectation of 1.85 million barrels per day. Pay attention to whether this month's report will further lower expectations for global crude oil demand growth.

On September 11th at 20:30, the US will release the August seasonally adjusted CPI annual rate and the seasonally adjusted CPI monthly rate. The seasonally adjusted CPI annual rate for July in the US was 2.9%, marking the fourth consecutive month of decline and returning to the "2 range" for the first time since March 2021. The market expectation is 3%. Pay attention to whether the consumer price index continues to decline in this period.

On September 12th at 16:00, the IEA released its monthly oil market report. The August report showed that global oil demand will increase by 0.97 million barrels per day this year and by 0.953 million barrels per day next year, slightly lower than the previous estimate of 0.974 million barrels per day and 0.979 million barrels per day. Pay attention to whether the demand forecast will be lowered this month.

On September 12th at 20:00, Conab released the results of its 12th survey on grain production for the 2023/24 crop year in Brazil. The previous survey projected Brazil's soybean production for the 2023/24 crop year to be 0.1474 billion tons, slightly lower than the expected 0.1481 billion tons and slightly higher than the previous value of 0.14734 billion tons, while yield per hectare remains unchanged at 3,202 kilograms. Pay attention to the adjustment of soybean production estimate in this report.

On September 12th at 20:15, the European Central Bank announced its interest rate decision. At the same time, at 20:45, ECB President Lagarde held a press conference on monetary policy. Citi believes that the ECB is highly likely to cut interest rates by 25 basis points next week, but it may gently remind people that unlike the Fed, the ECB does not have a dual mandate of employment and inflation.

On September 13th at 0:00, the USDA released its September monthly supply and demand report. The previous expectation for the soybean yield for the 2024/2025 crop year in the United States in August was 53.2 bushels per acre, and the market expectation was 52.5 bushels per acre. Recently, StoneX raised its estimate of the 2024 US yield from the previously estimated 52.6 bushels per acre to 53.0 bushels per acre. Pay attention to whether the USDA's monthly supply and demand report will raise the yield expectations.

On September 13th at 21:00, the Shanghai Futures Exchange, Dalian Commodity Exchange, Zhengzhou Commodity Exchange, and Shanghai Gold Exchange will not conduct night trading due to the Mid-Autumn Festival.

On September 14th at 10:00, the National Bureau of Statistics will release China's industrial added value, retail sales, real estate, fixed asset investment, and unemployment rate data for August, and hold a press conference on the operation of the national economy. The National Bureau of Statistics previously stated that the national economy has continued to show signs of improvement, with overall stable and steady progress. Pay attention to the industrial production data for August.