9月6日,美国劳工部公布8月非农企业和家庭调查数据。8月新增非农就业人口14.2万人,弱于市场预期的16万人,7月8.9万人(修正后)。8月失业率如期回落0.1个百分点至4.2%,前值4.3%。

9月6日,美国劳工部公布8月非农企业和家庭调查数据。8月新增非农就业人口14.2万人,弱于市场预期的16万人,7月8.9万人(修正后)。8月失业率如期回落0.1个百分点至4.2%,前值4.3%。The expected number of interest rate cuts for derivatives within the year is 4.5 times (25bp each time), and the number of interest rate cuts before June next year is 9 times. This radical interest rate expectation helps to achieve the effect of early interest rate cuts, which may be welcomed by the current Federal Reserve.

According to the Futu Securities research report, the team believes that the labor market has cooled significantly and may need to accelerate the pace of interest rate cuts. The faster wage growth is mainly due to structural factors, and the inflationary pressure is relatively controllable. In this case, the remaining three Federal Reserve meetings this year may cut interest rates by at least 25bp each time, with an overall interest rate cut of at least 75bp within the year. How quickly the Federal Reserve reaches the end of the interest rate cutting cycle may be more important.

The following is the summary of the research report:

On September 6th, the U.S. Department of Labor released the August non-farm household survey data. The number of new non-farm jobs in August was 0.142 million, weaker than the market's forecast of 0.16 million, and July was 0.089 million (revised). The unemployment rate in August fell as expected by 0.1 percentage point to 4.2%, down from the previous value of 4.3%.

On September 6th, the U.S. Department of Labor released the August non-farm household survey data. The number of new non-farm jobs in August was 0.142 million, weaker than the market's forecast of 0.16 million, and July was 0.089 million (revised). The unemployment rate in August fell as expected by 0.1 percentage point to 4.2%, down from the previous value of 4.3%.

After the data was released, the yield on 10-year U.S. Treasuries initially fell by about 10bp, then turned upwards and basically recovered the previous decline; U.S. stocks fell, with the Nasdaq index, S&P 500, and Dow Jones Industrial Average falling by 2.47%, 1.70%, and 0.95% respectively; the U.S. dollar index fell to a intraday low of 100.58 and rebounded to 101.27; COMEX gold initially rose by about 0.5% and then turned downwards, closing down 0.64%. Concerns about the cooling of the U.S. economy have overshadowed the interest rate cut trade. How should we look at the August non-farm data?

First, the unemployment rate slightly decreased. The U3 unemployment rate in August fell from 4.25% to 4.22%, which seems to be a decrease of 0.1 percentage point when rounded, but it actually decreased by only 0.03 percentage point, significantly higher than the unemployment rate of 4.05% in June. The number of unemployed persons in August was 7.115 million, slightly lower than the previous month's 7.163 million. The number of temporarily unemployed persons (seasonally adjusted) decreased from 1.062 million to 0.872 million, which may reflect the impact of adverse weather receding. The number of permanently unemployed persons increased slightly from 1.682 million to 1.688 million. The labor force participation rate remained at 62.7%, indicating a temporary slowdown in the transfer from the non-labor force population to the labor market.

The overall unemployment rate is higher than in 2018-2019. The U6 unemployment rate in August was 7.9% (up 0.1 percentage point from the previous month), which is between the average of 7.45% in 2019 and 8.1% in 2018. The U3 unemployment rate was 4.22%, significantly higher than 3.9% in 2018 and 3.7% in 2019.

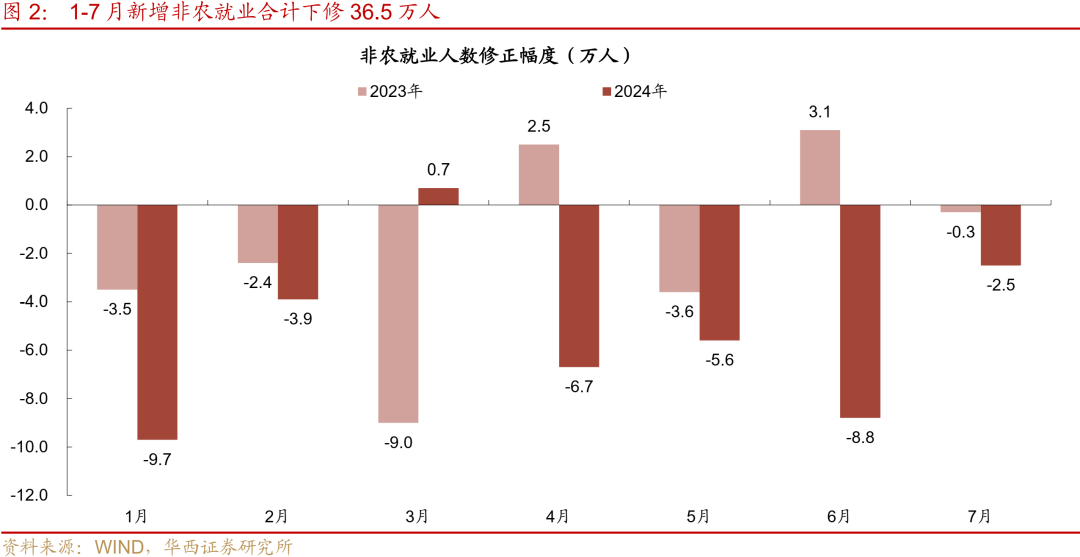

Secondly, the new employment growth remains weak and continues to be revised down. In August, new employment increased by 0.142 million people, down from 0.114 million people in July to 0.089 million people, and further down from 0.179 million people in June to 0.118 million people. A total downward revision of 0.086 million people in June and July. The downward revision of new non-farm employment from January to July this year reached 21.5%, totaling 0.365 million people, compared to a downward revision proportion and number of only 6.4% and 0.132 million people in the same period last year.

In August, the private sector added 0.118 million new jobs, with an average of 0.152 million from January to August this year, and a recent average of only 0.096 million in the last 3 months. Compared to 2018-2019, the annual average was 0.18 million and 0.148 million respectively. This reflects that the employment positions provided by the private sector have significantly slowed down, possibly struggling to meet the supply growth brought by immigrants, and may lead to a continuous increase in the unemployment rate in the future.

The non-farm response rate is low, also reflecting a cooling of the US labor market. Since the beginning of this year, the average response rate in the first month of non-farm employment is 59.9%, significantly lower than the average of 67.5% in the same period of the past three years, a decrease of 7.6 percentage points. The response rates for the second and third months are also lower by 3.7 and 6.1 percentage points respectively. Non-farm employment monthly data are frequently revised downwards. Generally speaking, in the second and third months, the proportion of response from small and medium-sized enterprises is higher, calculating non-farm employment based on the first month data gives more weight to large enterprises. Small and medium-sized enterprises are more susceptible to the negative impact of interest rate hikes, leading to a faster decrease in the number of new positions provided. Therefore, the frequent and significant downward revisions in new non-farm employment since the beginning of this year reflect that the labor market is relatively 'colder' than non-farm initial values.

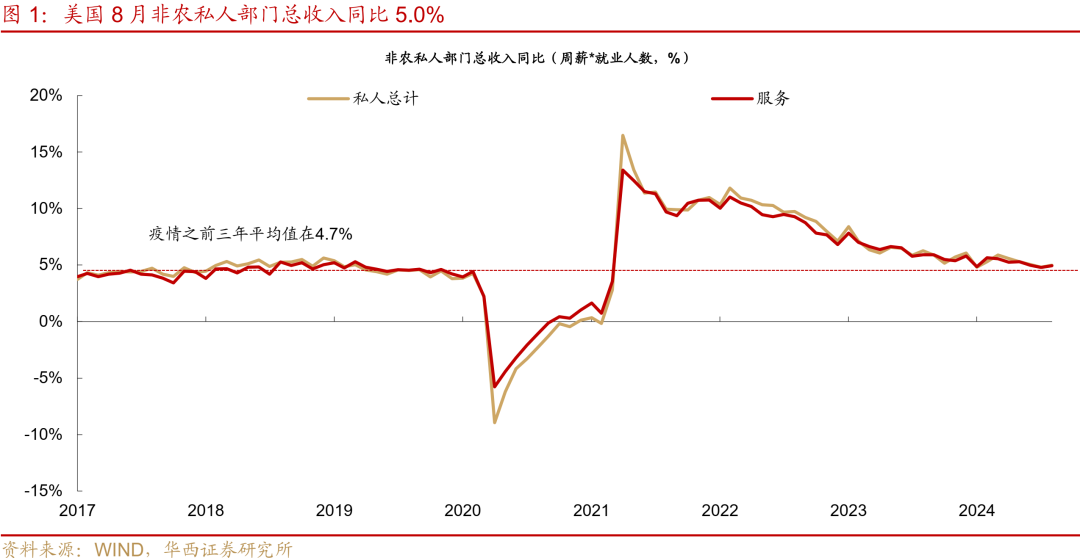

Thirdly, wage growth is accelerating. In August, non-farm wages increased by 0.40% on a seasonally adjusted basis, reaching a high point since February this year. The corresponding annualized growth rate is about 4.9%, although the growth rate is high, it is not yet significantly boosting inflation. Both goods and services saw an increase, rising by 0.06 and 0.20 percentage points to 0.33% and 0.43% respectively. Industries with a significant wage increase are mainly in information, utilities, retail, finance, etc., with growth rates ranging from 0.64% to 0.96%. These industries often require certain professional skills, making it difficult for immigrants to enter directly. Meanwhile, wages in leisure and hospitality, education, and medical services either slowed down or remained basically flat on a monthly basis. This wage distribution reflects a structural shortage in the labor market. The total income of the non-farm private sector (weekly wage * number of employees) increased slightly from 4.8% to 5.0% year-on-year, approaching the average of 4.7% in the pre-epidemic years of 2017-2019, indicating that the growth rate of non-farm total income is returning to pre-epidemic levels.

Fourthly, in terms of the pace of interest rate cuts, at the September, November, and December Federal Reserve meetings, there will be at least a 25 basis point cut each time. The August US employment data showed a scenario of weak new job creation, a slight decrease in the unemployment rate, and a structural rise in wages. Considering the 3-month moving average of only 0.096 million new jobs in the private sector, along with the significant downward revisions to non-farm employment since the beginning of this year, the labor market has cooled significantly, possibly necessitating an accelerated pace of interest rate cuts. However, the faster wage growth is mainly structural, which has a relatively controllable impact on inflation. In this scenario, the Federal Reserve may cut at least 25 basis points at each of the remaining three meetings this year, with an overall rate cut of at least 75 basis points by the end of the year.

In terms of market expectations, according to Bloomberg data, derivative products expect a rate cut 4.5 times (25 basis points each time) within the year, and 9 times before June next year. This more aggressive rate cut expectation is likely to bring forward the rate cut effect, which may be welcomed by the current Federal Reserve.

As for whether a single rate cut of 50 basis points is needed, the Federal Reserve may need more data to evaluate. Following the release of the August employment data, Federal Reserve officials emphasized the urgency of a rate cut in September. New York Fed President Williams stated, 'It is appropriate to lower the federal funds rate now,' but did not comment on the magnitude of the rate cut. Federal Reserve Governor Waller's stance remains slightly hawkish, as he believes the data remains relatively solid and that rate cuts should be prudent, but he also remains open to the possibility of a larger rate cut. Whether the Federal Reserve will cut by 50 basis points at the September meeting (to be released early on the 19th Beijing time) remains undecided, with the market expectation probability at only 30%. We anticipate a 25 basis point rate cut in September with a high probability.

Compared to a 25 basis point or a 50 basis point rate cut, we may need to pay more attention to the dot plot provided by the Federal Reserve at the September meeting, which represents the pace of rate cuts the Federal Reserve acknowledges going forward. The dot plot in June of this year projected a 25 basis point cut within the year, followed by 100 basis points in the next two years, leaning towards a 25 basis point cut each quarter. We need to observe the dot plot in September to see if the strategy switches from a 25 basis point cut each quarter to a 25 basis point cut at each meeting (8 meetings per year). The longer-run rate given by the Federal Reserve is 2.8%, which can be seen as the end point of rate cuts, corresponding to a total reduction of about 250 basis points in this rate cut cycle. If the switch is made to a 25 basis point cut at each meeting, the Federal Reserve will reach near the neutral rate by the fourth quarter of next year. The pace at which the Federal Reserve reaches the end point of the rate cut cycle may be more important.

The fifth is that the interest rate pricing has already been relatively sufficient, and the market is more concerned about the risk of the US economic slowdown. Market expectations are that the Federal Reserve will cut interest rates 9 times by June next year, totaling 225 basis points. This has already priced in a direction towards recession. The pace of interest rate cuts in recent cycles has only been this fast in 2001 and 2007, during the dot-com bubble and subprime crisis respectively. Therefore, there is relatively limited room for further expansion of interest rate cut expectations. Meanwhile, concerns about the US economic slowdown have been rising, reflected in increased volatility in the US stock market. Going forward, important data may continue to impact the sentiment of the US stock market.