历史规律而言,港股通调整落地前后,往往伴随着股票价格的剧烈波动,特别是那些此前曾围绕“入通”进行过市值管理的股票。入通之后,利好落地,有可能出现回调。此外,前期因媒体或市场关注不足的股票,却有可能因入通调整出现正向预期差,入通之后反而开启一波行情。

历史规律而言,港股通调整落地前后,往往伴随着股票价格的剧烈波动,特别是那些此前曾围绕“入通”进行过市值管理的股票。入通之后,利好落地,有可能出现回调。此外,前期因媒体或市场关注不足的股票,却有可能因入通调整出现正向预期差,入通之后反而开启一波行情。According to the announcement of Hang Seng Index Company and Hong Kong Stock Exchange on August 16th, this time, a total of 33 stocks including Universal Cloud, Maifushi, Chabaida, SF Express, Netease Cloud Music, Sunshine Insurance, Jingtai Technology, Lao Pu Gold, and Hang Lung Group will be included in the scope of the Hong Kong Stock Connect constituents.

The highly anticipated adjustment of the Hang Seng Index and the constituent stocks of the Hong Kong Stock Connect will be implemented after the market close tomorrow (September 6th). Due to the impact of bad weather, the Hong Kong stock market is closed today, so the adjustment of the Hang Seng Index and the Hong Kong Stock Connect will take effect after the market close on September 9th (next Monday).

According to the announcement of the Hang Seng Index Company and the Hong Kong Stock Exchange on August 16, this time will include a total of 33 stocks, such as All-Wise Cloud, Mai Fushi, TeaBaiDao, SF SameCity, Netease Cloud Music, Sunshine Insurance, Crystal Tech, Lao Pu Gold, Hang Lung Group, etc., into the scope of the Hong Kong Stock Connect symbol.

Historically, the adjustment of the Hong Kong Stock Connect is often accompanied by significant fluctuations in stock prices, especially for those stocks that have previously been managed in terms of market cap around "inclusion in the Connect". After inclusion, the positive impact may lead to a pullback. In addition, stocks that were previously not well-covered by the media or the market may have a positive expectation gap due to the inclusion adjustment, and may even start a new wave of market activities after inclusion.

Historically, the adjustment of the Hong Kong Stock Connect is often accompanied by significant fluctuations in stock prices, especially for those stocks that have previously been managed in terms of market cap around "inclusion in the Connect". After inclusion, the positive impact may lead to a pullback. In addition, stocks that were previously not well-covered by the media or the market may have a positive expectation gap due to the inclusion adjustment, and may even start a new wave of market activities after inclusion.

Regardless, both of the above situations exist, and investors need to analyze specific problems rather than making generalizations.

1. The Carnival of Inclusion

A stock being included in the Hong Kong Stock Connect means that it will receive incremental funds for buying, which is a major bullish factor. Therefore, intuitively, before the implementation of the "through train", the stocks should show a "carnival" attitude.

Among the 33 stocks that will be included in the Hong Kong Stock Connect, the stock prices of companies such as Jingtai Technology, Dah Sing Banking Group, and Dekang Agriculture have all surged today. Jingtai Technology, for example, has been rising since August 29th, and as of the close on September 5th, its stock price has increased by a cumulative 149%. Dah Sing Banking Group surged by 9% in a single day on August 30th, while Dekang Agriculture has accumulated a 28% increase since August 30th.

Jingtai Technology, for example, is a new stock listed in June this year, with a market cap of approximately 18 billion Hong Kong dollars at the time of listing, meeting the market cap requirements for inclusion in the Hang Seng Index. As a result, it was quickly included in the Hong Kong Stock Connect. After its recent continuous rise, its market cap has now reached 51.9 billion Hong Kong dollars.

In addition, stocks such as Kinetic Development, Stella Holdings, China Ship Leasing, and Lao Pu Gold are at high prices. However, shares of Songsheng International, Dalipal Holdings, and others are in a continuous decline. Shengneng Group, after plunging 98% on September 3rd, is already in a very weak position.

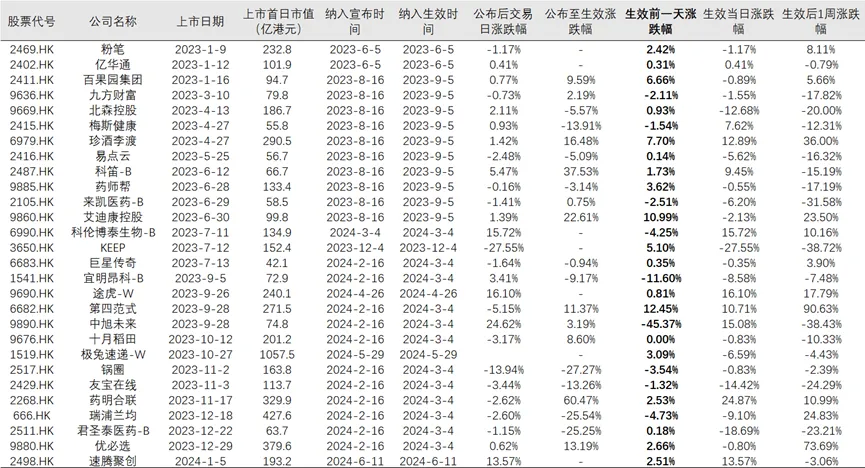

Reviewing historical data, we have compiled statistics on the announcement time, implementation time, announcement day price changes, trends between the announcement and implementation, as well as the price changes around the implementation day and the week after the implementation for the 28 new stocks listed since early 2023 that have been included in the Hong Kong Stock Connect.

Table: Statistics of price changes for important dates before and after the implementation of Hong Kong Stock Connect for stocks included since early 2023

The data shows that overall, the trend from announcement to implementation or the day before implementation is generally upward. For example, out of the 28 stocks included, the average increase from announcement to implementation is 2.7%, and the average increase on the day before implementation is 1.2%. Although the numbers may not seem exaggerated, considering that many stocks have accumulated a significant increase in anticipation of the inclusion, and the time span from announcement to implementation is not long, such price changes are still statistically significant.

In addition, it is interesting to note that the trend of some stocks fluctuates drastically before the announcement, between the announcement and implementation, on the day of implementation, and in the week following implementation. The main representative is Zhongxu Future. On the day of the announcement, Zhongxu Future rose by 24%, and during the period between the announcement and implementation, the increase narrowed to 3%. The day before implementation, there was a sharp drop of 45%, and on the day of implementation, there was a sharp rise of 15%. In the week following implementation, there was a significant decline of 38%.

From this, it can be seen that although being included in the Hong Kong stock market connection is theoretically bullish, the specific situation still needs to be analyzed based on the individual circumstances of different stocks. As the implementation of the "connection" approaches, some stocks have already started to fluctuate.

In my opinion, for investors participating in the game of the "connection", the most prudent strategy is to properly manage their positions from the announcement to the implementation, so as to stand firm. This will prevent being caught off guard when stock prices fluctuate dramatically in the period leading up to implementation.

2. Which stocks are favored by the Hong Kong stock market connection?

There is no doubt that in recent years, southbound funds have become the most important source of incremental capital for the Hong Kong stock market. The stocks that are focused on and traded by Hong Kong stock market connection investors often become market hotspots. So, what are the characteristics of the stocks favored by Hong Kong stock market connection investors?

As of today's closing, we have compiled the Hong Kong stock market holdings of all Hong Kong stocks and listed the stocks with a Hong Kong stock market connection holding ratio exceeding 20% in the table below.

Table: Statistics of the performance of stocks with a Hong Kong stock market connection holding ratio exceeding 20% since listing.

Based on the analysis of the listing date, sector, peak price occurrence time of these stocks, and recent trends, we have identified the characteristics of stocks with high holdings of the Stock Connect in terms of market cap, sector, and historical market performance:

(1) First, in terms of market cap. According to the latest data, the market cap of these stocks is generally below 50 billion, except for semiconductor manufacturing international corporation, china res power, innovent bio, and cnooc, among other large blue chip stocks. If the holdings of Stock Connect are expanded to over 10%, the number of large-cap stocks increases significantly, including companies like Xiaomi, Meituan, Xpeng, Li Auto, China Unicom, and even China Mobile and Tencent, which are among the top three in terms of market cap.

Therefore, we can draw the first conclusion that stocks with the highest holdings of Stock Connect are generally small and medium-sized companies, while stocks with moderate holdings of Stock Connect are more likely to be mid to large-cap companies.

(2) Secondly, in terms of sector characteristics, clustering is observed. Broadly classified into three categories, the first category consists of old stocks listed in 2007, many of which are value investment stocks such as Datang Energy, China Res Power, CNOOC, CGN Power, picc p&c, cnbm, cosco ship engy, etc.

The second category includes concept stocks formed during the bull market driven by the southbound funds in 2015. Examples include eb environment, dynagreen env, Meitu, etc. When talking about these stocks, there is a sense of outdated hot topics and short-lived hype.

The third category includes concept stocks formed during the bull market from 2019 to 2021, covering various sectors such as biomedical (18A), semiconductor semiconductors, 5G, cloud computing, internet of things, new energy, new economy, new consumption, etc. There are also many stocks involved, such as Poly PPT Ser, Akeso, JXR, Wuxi Bio, Kingdee Int'l, XD Inc, Kingsway, Yonyou, Li Ning, semiconductor manufacturing international corporation, Innovent Bio, xiabuxiabu, Bilibili, etc.

(3) Stock Price Trends

Stocks with holdings of Stock Connect above 20%, except for a very small number hitting recent highs, like CNOOC, the vast majority have experienced significant declines in the past one or two years. Their peak stock prices mostly coincide with the hottest periods of their respective sectors.

For example, A-share sectors such as Akeso, JXR, and Wuxi Bio, generally reached their peak in late 2020 and early 2021. New consumer concept stocks such as Xiabuxiabu, Bilibili, and Li Ning had their peak in the first half of 2021. As for the previous hotspots, the stocks formed during the crazy bull market of southbound funds in 2015, companies such as EB Environment and Ali Pictures reached their highest prices in the summer of 2015.

In addition, there are also many stocks listed after 2020 in the statistical results, many of which reached their peak right after listing, or experienced a decline in share price after half a month of listing or after the lifting of the lock-up period, such as Poly PPT Ser and many others.

One sad and undeniable fact is that for shares with a holding proportion of more than 20% by the Hong Kong Stock Connect, except for CNOOC and China Gold, whose historical highest prices appear in 2024, the rest of the shares have been declining this year. Some of them have not only been declining this year but have been continuously declining for two to three years.

This raises a painful question: is the Hong Kong Stock Connect really a bottom-fisher?

3 Is the Hong Kong Stock Connect really a bottom-fisher?

Let's not rush to a conclusion and first look at the statistical data.

Assuming we don't consider the latest adjustments that have not taken effect yet, since the Shanghai-Hong Kong Stock Connect opened in November 2014 and the Shenzhen-Hong Kong Stock Connect opened in December 2016, up to now, there are a total of 525 stocks in the Hong Kong stock market that are included in the Hong Kong Stock Connect. Among these stocks, there are 69 stocks with a Hong Kong Stock Connect holding proportion higher than 20% and 205 stocks with a Hong Kong Stock Connect proportion higher than 10%.

Out of these 525 stocks, only 22 stocks reached their historical highest prices in 2024. Among them, 9 are new stocks listed in the second half of 2023 or the first half of this year, which coincided with the end of the lock-up period and the moment of entry into the Stock Connect.

In other words, the majority of these 525 H shares have experienced at least a year of decline. We have analyzed the time when these stocks reached their historical highs, which mostly concentrated in the periods of 2007-2008, 2015-2018, and 2020-2021, which happened to be three decent bull markets in the history of Hong Kong stocks.

If we do precise calculations, the average decline of these 525 stocks from their respective historical highs is 72.13%, while the average decline from the historical highest price for the 205 stocks in which the shareholding ratio is over 10% in the Hong Kong stock connect program is 74.63%. For the 69 stocks with a shareholding ratio over 20%, the average decline from the historical highest price is 78.37%. From this, it can be seen preliminarily that the higher the shareholding ratio of the Hong Kong stock connect, the deeper the decline from the historical highest price.

In addition, based on the recent 1-year data, the average decline of the 525 H shares in the Hong Kong stock connect program in the past year is 15.54%. The average decline of the 205 stocks with a shareholding ratio over 10% is 20.17%, while the average decline of the "high Hong Kong stock connect stocks" with a shareholding ratio over 20% is as high as 25.42%. This shows a distribution pattern similar to the decline from the historical highest price.

As for the five stocks with a shareholding ratio over 40% in the Hong Kong stock connect program, their cumulative average decline from the respective historical highest points is as high as 80%. The average decline in the past year also reaches 42.67%. These stocks include Mog Digitech, Poly Ppt Ser, Dongfeng Group, Xinte Energy, and Zhejiangexpress.

Therefore, in general, it can be considered that the higher the shareholding ratio in the Hong Kong stock connect program, the more prone the stocks are to decline.

Of course, this cannot be generalized. For example, China National Offshore Oil Corporation, with a shareholding ratio of 20.03% in the Hong Kong stock connect program, has only a 16% decline from the historical highest price and has not only not fallen over the past year but also has a 54% increase. However, this situation only occurs in a few individual stocks.

As for why stocks with a higher shareholding ratio in the Hong Kong stock connect program are more likely to decline, a reasonable inference is that Hong Kong stock connect investors, whether they are institutions or individuals, tend to buy more as prices fall under certain investment concepts. Due to the opposing positions of foreign/Hong Kong funds and Hong Kong stock connect funds in the game of the Hong Kong stock market, the two operate in opposite directions. Foreign funds continue to sell, while Hong Kong stock connect funds continue to buy. As a result, stock prices fall deeper and the shareholding ratio in the Hong Kong stock connect program continues to rise.

In this sense, it is not an exaggeration to say that the Hong Kong stock connect is a "clean-up buyer".

How does the Hong Kong stock connect cut leek?

Currently, the liquidity of the Hong Kong stock market is declining, and the Hong Kong stock connect, as almost the only way for incremental funds, has been used by some stocks and has become a new tool for cutting leeks, especially in the IPO market.

Once a new stock is included in the Hong Kong stock connect, there will be passive funds building positions based on the corresponding tracking index. At the same time, within half a year to one year after the new stock is listed, it will face pressure. As a result, the passive funds in the Hong Kong stock connect are forced to absorb the lifting of the ban. Therefore, the effective date of inclusion in the Hong Kong stock connect has become another important time point for market fluctuations, apart from the lifting of the ban.

In addition, if the inclusion in the stock connect fails, it is more likely to cause a steep drop. For example, Evergrande Group, whose stock price plummeted by 98% in a single day, is a classic case. According to our previous analysis, Evergrande Group speculated on "inclusion in the stock connect" after its listing. It was speculated once in January this year, but started speculating again after April, and its stock price nearly multiplied tenfold in three months. And at the end of June when the Hang Seng Index conducted its semi-annual review, Evergrande Group's market value met the requirements for inclusion in the stock connect.

However, in early August, due to the Hong Kong Securities and Futures Commission naming four stocks with highly concentrated equity, also known as "high control", the company's final last-minute effort before inclusion in the stock connect was shattered.

Of course, due to the high concentration of equity, even major negative news is difficult to cause a sharp drop. But ultimately, on September 3rd (Tuesday), due to the bursting of margin calls, the stock price collapsed completely, plummeting 98% in a single day.

Overall, the market overview of the day when the inclusion in the stock connect took effect and the week after is relatively balanced. For example, stocks such as Tuho, Wuxi Biologics, and Zhenjiu Lidu soared on the day when the inclusion took effect, while stocks such as Beisen Holdings plunged. Stocks that soared during the week after the inclusion included UBTECH, Fourth Paradigm, and Rui Pulin, among others. Stocks that plummeted during the week after the inclusion included Zhongxu Future, Youbao Online, and Junshengtai Pharmaceutical, among others.

Investors need to have a certain amount of insight and not fall into traps of stocks that use 'inflow' as a tool to cut profits.

5 New Rules and Their Impact on 'Inflow'

On August 27th, Hang Seng Index Company announced the optimized method for calculating the '12-month average market value' as a condition for 'inflow' in Hong Kong stocks, as well as the handling method for long-term trading halts. This caused quite a stir.

The method now calculates the '12-month average market value' by taking into account the market value on all trading days during the 12 months, instead of averaging the market value at the end of each month. This means that the calculation period has been increased from 12 to at least 252. This change has shocked the industry.

This undoubtedly makes the conditions for 'inflow' more stringent and at the same time reduces the possibility of manipulation. Under the previous rules, if a company wanted to engage in 'market value management', it only needed to manipulate the market value to meet the requirements on the last trading day of each month, a total of 12 times. However, under the new rules, market value management needs to be performed every day. This undoubtedly poses a huge challenge for companies.

Of course, it is undeniable that this optimization is intended to compress the space for listed companies to speculate using loopholes in the rules, but it may also further exclude more companies from the 'inflow' target group. It should be noted that 'inflow' funds are currently the only source of liquidity for many shares in the Hong Kong stock market. Without the 'inflow', many companies, even if listed, would struggle.

Perhaps this is the reason why 19 listed companies jointly called for an expansion of the 'inflow' just a day or two before the announcement of this optimization plan. From the perspective of enterprises, if domestic IPOs are not restarted, the only option is to list in Hong Kong. However, if there is no 'inflow' support after listing in Hong Kong, the liquidity will also dry up. Many innovative enterprises and PE/VC funds established in recent years will face the threat of drying up. If they cannot list, where will the company or management find the money to buy back the shares?

This expands the Hong Kong stock connect, which seems to be just a stock market and capital market issue, but it affects a broader social and livelihood landscape.

Of course, from the perspective of listed companies, since they have already gone public, they should stay on the right path and focus their efforts on operating the business and creating value, rather than completely ruining the Hong Kong stock connect, which is almost the most important source of incremental funds for the Hong Kong stock market.