JPMorgan believes that Alibaba's new investment strategy has achieved preliminary success, with its domestic e-commerce commodity trade volume (GMV) growth rate consistent with the industry growth rate. If this trend continues in the coming quarters, it may become the largest consumer stock in China. Goldman Sachs also stated that the introduction of WeChat Pay on Taobao is beneficial for developing the lower-tier markets and promoting further cooperation between Alibaba and Tencent.

Both Goldman Sachs and JPMorgan are bullish.$BABA-W (09988.HK)$they believe that the introduction of WeChat Pay by Taobao will pave the way for further cooperation between Alibaba and Tencent.$PDD Holdings (PDD.US)$The new monetization strategy proposed a week ago has little impact on Alibaba. Alibaba's new investment strategy has achieved initial success and may evolve into China's largest consumer stocks in the future.

Goldman Sachs believes that Taobao's announcement of the addition of WeChat Pay is beneficial for TaoTian to further develop the sinking market and provide more convenience for existing users, thereby promoting user penetration rate and total transaction volume of goods.

JPMorgan said that the new monetization strategy of PDD Holdings has limited impact on Alibaba, because PDD Holdings' new strategy mainly focuses on the merchant ecosystem rather than the consumer end; coupled with the significant difference in monetization rates between Alibaba and PDD Holdings, even if Taobao's monetization rate improves, it may still be the lowest-cost channel for merchants. $Alibaba (BABA.US)$And the monetization rate difference between Taobao and PDD Holdings is quite large, so even if Taobao's monetization rate improves, it may still be the lowest-cost channel for merchants.

JPMorgan is also bullish on the growth trend of Alibaba's domestic e-commerce gross merchandise value (GMV), believing that Alibaba's narrative in the next 6-12 months will change from being a market share relinquisher to a stable e-commerce growth stock. The inclusion of the "Hong Kong Stock Connect" and the acceleration of customer management revenue (CMR) growth will serve as short-term catalysts.

Taobao and Tmall introduce WeChat Pay.

In November 2013, Taobao and WeChat blocked each other, which has been nearly 11 years now.

On September 4th, Alibaba announced the first introduction of WeChat Pay on the Taobao and Tmall platforms. Goldman Sachs stated that this change is in line with its expectations, as starting from September 1st, Tmall began to levy software service fees (covering payment processing costs), which created conditions for the platform to expand online payment options.

Goldman Sachs believes that adding WeChat Pay can help Taobao and Tmall attract new user groups, especially benefiting the development of low-tier city users, and provide more convenience to existing users, thereby promoting user penetration rate and total trade volume growth.

In addition, the Taobao and Tmall Group has already collaborated with Tencent in WeChat advertising campaigns for several quarters. Goldman Sachs believes that the introduction of WeChat Pay by Taobao and Tmall can pave the way for further cooperation between Alibaba and Tencent. For example, Taobao-Tmall may have mini-programs within the WeChat ecosystem in the future.

This is significant for Alibaba because Tencent dominates China's social applications, with over 1 billion monthly active users, while Alibaba is the only e-commerce platform that does not yet have a shopping mini-program within the WeChat ecosystem. According to Quest Mobile data, there are approximately 247 million WeChat users in China who have not installed the Taobao app.

At the same time, Goldman Sachs also noted that Alipay recently launched mini-programs for Meituan Takeaway and Meituan Hotels, whereas previously users could only order on Ele.me through Alipay. Goldman Sachs believes that after the conclusion of the Alibaba anti-monopoly review, announced by Chinese regulators on August 30, 2024, as a milestone for Internet giants cooperation. There will be an increase in cooperation between Internet giants, and the ecosystem will no longer be relatively closed as before.

The new strategy of PDD has limited impact on Alibaba monetization.

On August 29, during the PDD conference call, a new investment strategy was proposed, including allocating 10 billion yuan to support high-quality merchants, improving platform ecosystem construction, and refunding commissions and advertising fees for directly refunded orders.

JPMorgan said:

"The new monetization strategy of PDD has limited impact on Alibaba, as PDD's new strategy mainly focuses on the merchant ecosystem rather than the consumer end. PDD's investment in the merchant ecosystem aims to improve the supply ecosystem for long-term sustainable growth, rather than seeking maximum market share growth in the short term."

In the current retail environment, increasing the profitability of high-quality merchants has a relatively small impact on consumer spending and therefore will not have a significant impact on the total transaction volume of Alibaba's domestic e-commerce business.

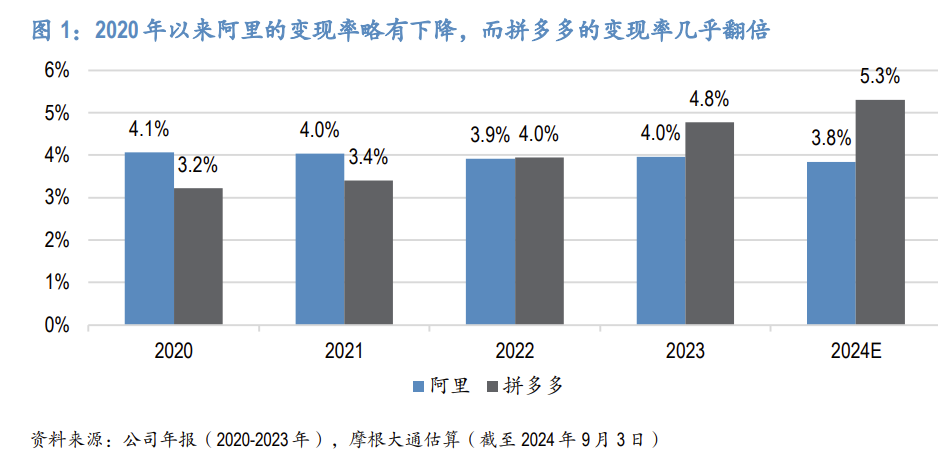

The slight increase in Taobao's monetization rate has little impact.

JPMorgan stated that in the past three years, Alibaba has been relatively restrained in monetizing its e-commerce business, while its peers have significantly improved their monetization of e-commerce. JPMorgan believes that the difference in monetization rates between Alibaba and PDD may be greater than it seems, as Alibaba's investment strategy has led to faster growth in lower-priced channels than higher-priced channels.

For example, JPMorgan estimates the monetization rate of Tmall to be 6%, Taobao to be 2%, and PDD to be over 5%. Therefore, even if Taobao's monetization rate increases, it may still be the lowest cost channel for merchants, and Alibaba's moderate increase in monetization rate will not change its relative value proposition to merchants.

Editor/ping