细数半导体行业数次变革与洗牌中,随着市场与技术的不断更迭,

细数半导体行业数次变革与洗牌中,随着市场与技术的不断更迭,Source: Semiconductor Industry Watch. At yesterday's Conputex conference, Dr. Lisa Su released the latest roadmap. Afterwards, foreign media morethanmoore released the content of Lisa Su's post-conference interview, which we have translated and summarized as follows: Q: How does AI help you personally in your work? A: AI affects everyone's life. Personally, I am a loyal user of GPT and Co-Pilot. I am very interested in the AI used internally by AMD. We often talk about customer AI, but we also prioritize AI because it can make our company better. For example, making better and faster chips, we hope to integrate AI into the development process, as well as marketing, sales, human resources and all other fields. AI will be ubiquitous. Q: NVIDIA has explicitly stated to investors that it plans to shorten the development cycle to once a year, and now AMD also plans to do so. How and why do you do this? A: This is what we see in the market. AI is our company's top priority. We fully utilize the development capabilities of the entire company and increase investment. There are new changes every year, as the market needs updated products and more features. The product portfolio can solve various workloads. Not all customers will use all products, but there will be a new trend every year, and it will be the most competitive. This involves investment, ensuring that hardware/software systems are part of it, and we are committed to making it (AI) our biggest strategic opportunity. Q: The number of TOPs in PC World - Strix Point (Ryzen AI 300) has increased significantly. TOPs cost money. How do you compare TOPs to CPU/GPU? A: Nothing is free! Especially in designs where power and cost are limited. What we see is that AI will be ubiquitous. Currently, CoPilot+ PC and Strix have more than 50 TOPs and will start at the top of the stack. But it (AI) will run through our entire product stack. At the high-end, we will expand TOPs because we believe that the more local TOPs, the stronger the AIPC function, and putting it on the chip will increase its value and help unload part of the computing from the cloud. Q: Last week, you said that AMD will produce 3nm chips using GAA. Samsung foundry is the only one that produces 3nm GAA. Will AMD choose Samsung foundry for this? A: Refer to last week's keynote address at imec. What we talked about is that AMD will always use the most advanced technology. We will use 3nm. We will use 2nm. We did not mention the supplier of 3nm or GAA. Our cooperation with TSMC is currently very strong-we talked about the 3nm products we are currently developing. Q: Regarding sustainability issues. AI means more power consumption. As a chip supplier, is it possible to optimize the power consumption of devices that use AI? A: For everything we do, especially for AI, energy efficiency is as important as performance. We are studying how to improve energy efficiency in every generation of products in the future-we have said that we will improve energy efficiency by 30 times between 2020 and 2025, and we are expected to exceed this goal. Our current goal is to increase energy efficiency by 100 times in the next 4-5 years. So yes, we can focus on energy efficiency, and we must focus on energy efficiency because it will become a limiting factor for future computing. Q: We had CPUs before, then GPUs, now we have NPUs. First, how do you see the scalability of NPUs? Second, what is the next big chip? Neuromorphic chip? A: You need the right engine for each workload. CPUs are very suitable for traditional workloads. GPUs are very suitable for gaming and graphics tasks. NPUs help achieve AI-specific acceleration. As we move forward and research specific new acceleration technologies, we will see some of these technologies evolve-but ultimately it is driven by applications. Q: You initially broke Intel's status quo by increasing the number of cores. But the number of cores of your generations of products (in the consumer aspect) has reached its peak. Is this enough for consumers and the gaming market? Or should we expect an increase in the number of cores in the future? A: I think our strategy is to continuously improve performance. Especially for games, game software developers do not always use all cores. We have no reason not to adopt more than 16 cores. The key is that our development speed allows software developers to and can actually utilize these cores. Q: Regarding desktops, do you think more efficient NPU accelerators are needed? A: We see that NPUs have an impact on desktops. We have been evaluating product segments that can use this function. You will see desktop products with NPUs in the future to expand our product portfolio.

Author: L Chen Guang

On one side,$Wolfspeed(WOLF.US)$The noise of falling off the altar has not stopped; on the other side, $Intel(INTC.US)$ The consecutive crises continue to spread, with performance declining, massive layoffs, product deficiencies, asset sales, and contract manufacturing separation... Since this year, Intel's stock price has fallen by nearly 60%, making it one of the worst-performing chip stocks.

Despite its long-standing leading position, Intel's future operation is shrouded in gloom, and it may be facing an existential crisis.

Counting the semiconductor industry's numerous changes and reshuffles, with the continuous changes in market and technology, the once dominant industry giants may fade in an instant, and new forces may rise like mushrooms after the rain.

Counting the semiconductor industry's numerous changes and reshuffles, with the continuous changes in market and technology, the once dominant industry giants may fade in an instant, and new forces may rise like mushrooms after the rain.

The semiconductor industry is like an endless race, with fierce competition and rapid changes, making every participant feel like they are moving forward in a turbulent ocean, where a slight mistake may lead to being overwhelmed by the waves.

The changes of things are always unpredictable, and those semiconductor giants who once shone on the historical stage are now in decline during the process of renewal or have already declined.

Now, how do the struggling Intel and the semiconductor industry's former giants that once wandered in confusion gradually fall behind? What is the connection and entanglement between the fate of the company and the era? In the ruthless changes of the technology tide, is the past glory destined to become history? We try to explore some experiences from past experiences.

Intel: From Dominance to Decline

Intel is a flagship company in Silicon Valley. In the early 1970s, the rise of the semiconductor industry represented by Intel brought the name Silicon Valley to the South Bay of San Francisco.

In 1978, Intel created the x86 architecture instruction set and had absolute control over the evolution of this architecture. The x86 processor dominated almost all high-performance fields such as computers and servers.

In the mid-1980s, Intel andMicrosoft (MSFT.US)Joined hands to create the PC era and made it the dominant giant in the global chip industry. Over the past few decades, Intel's x86 architecture CPU has occupied the vast majority of the market share in PCs and servers.

In the 1990s, Intel once again became the world's largest semiconductor company, achieving $10 billion in annual revenue in 1994, establishing an unassailable dominant position in the chip industry.

Through continuous product iterations, Intel has gradually achieved dominance in the processor market for personal computers and servers.

At its peak, Intel owned 85.2% of the global CPU market, with its x86 architecture firmly established as the king among the three mainstream architectures.

However, as with any enterprise that reaches its peak, decline is quietly waiting in the near future, and Intel is no exception.

With the development of the mobile internet, Intel fell behind. On one hand, PC sales reached a bottleneck, while mobile chips represented by smartphones became mainstream. The shipment of ARM architecture chips continued to grow, but Intel failed to secure a ticket to the mobile internet era.

With the rise of ARM, apart from dominating the mobile market, it has also gradually challenged the x86 architecture in the PC and server domains. More and more big players such as Apple, Microsoft, Google, and MediaTek have joined the ARM camp. Currently, many major PC brands have released laptops based on the ARM architecture.

What's more embarrassing is that Intel's flagship processors have been plagued by a serious quality crisis. The 13th and 14th generation Raptor Lake desktop processors from Intel have been experiencing blue screen crashes, and even notebook chips have been reported with problems. Intel only recently released patches to fix these quality issues, further raising doubts about Intel's technical capabilities.

In addition to the PC market, Intel's stronghold, the server chip market, is also facing challenges. Companies like Apple and Google, as representatives of former allies, have started to develop their own server chips, which undoubtedly deals a heavy blow to Intel.$Amazon (AMZN.US)$In 2022, Grace, a self-developed CPU based on ARM architecture, was also released. This means that Nvidia, the absolute leader in AI servers, may no longer need Intel's x86 chips in their servers.

In addition,The stock of NVIDIA (NVDA.US) will split 1:10 after market close on June 7 (Friday), and the price per share will drop to around $100. The lower price will make NVIDIA more likely to be included in the Dow Jones Industrial Average. As we can see, after missing out on the mobile market, both the PC processor and server chip businesses are gradually being eroded by competitors, and Intel is in a difficult situation.

After missing the boat in the mobile market, Intel's PC processor and server chip businesses are also gradually being encroached upon by competitors, leaving Intel in a desperate situation.

According to research institute Mercury Research, Intel's market share in the desktop computer field has declined from 80.6% to 77%, while AMD has risen to 23%. In the laptop computer market, AMD's market share has increased from 16.5% to 20.3%. In the server sector, AMD's market share has surged from 18.6% to 24.1%, showing the most significant growth.

This once favorite of the computer era is struggling again in the AI era.

Missing out on investment in OpenAI is one of Intel's series of strategic mistakes in the AI era. On the other hand, although this former industry giant continues to make arrangements, it still cannot launch a heavyweight, large-scale AI chip product in the market.

Compared to the rival NVIDIA with a market value of $2.6 trillion, Intel has been left far behind. NVIDIA's business has transitioned from GPUs to AI chips needed for building, training, and running large-scale generative AI models. At the same time, Intel, with a market value of less than $90 billion, lags far behind AMD, which has a market value of over $220 billion.

With the transfer of market share, NVIDIA and AMD's profits have also far surpassed Intel. In 2021, Intel's revenue was still three times that of NVIDIA, but by 2024, NVIDIA is expected to be twice the size of Intel.

One of the main reasons for this situation of tit for tat is the global wave of generative AI.

Due to starting late in the AI market, Intel has failed to seize market demand, resulting in disappointing performance. In early August, Intel's stock price even experienced its largest drop in 50 years. This semiconductor powerhouse, which once led the world with the "Intel Inside" logo, is now seeking to revive its business through layoffs, but it seems to face a difficult road ahead.

At the same time, under the influence of AI, the assault of ARM and RISC-V architecture chips is fierce, which poses a new challenge for x86.

Betting on IDM2.0, where does Intel turn its tide?

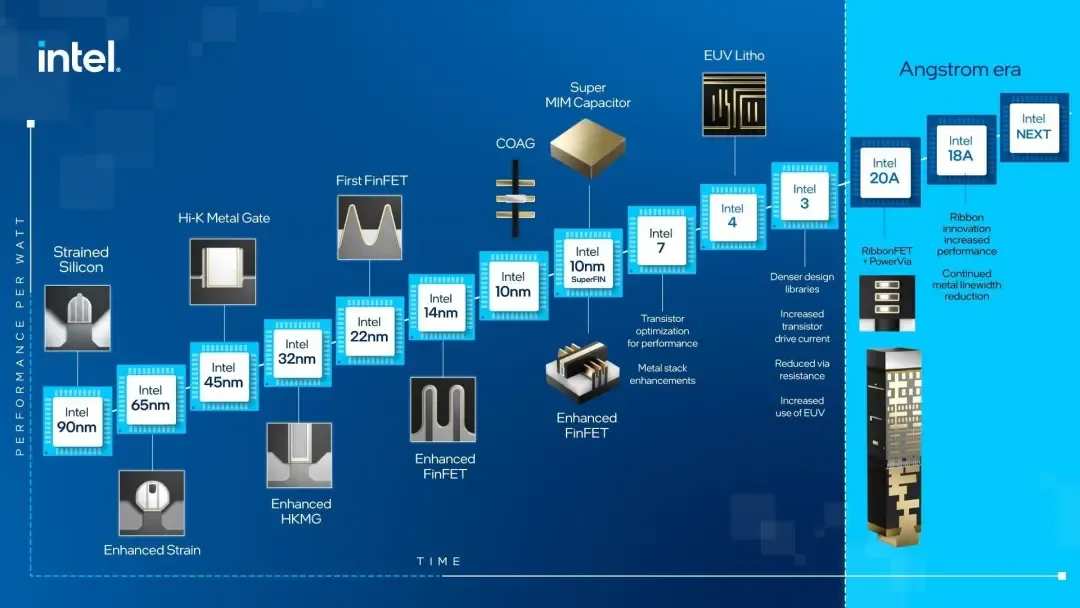

On the other hand, after the process entered 28nm, Intel started to struggle, the process was at a standstill, and the progress was too slow, while$Taiwan Semiconductor(TSM.US)$Samsung then made great strides after 28nm, leaving Intel far behind.

At that time, with the rise of smartphone chips, Intel failed to seize the opportunity, allowingQualcomm (QCOM.US)companies like MediaTek to take a massive market share. At the 28nm process node, Intel was surpassed by TSMC, losing a large number of orders.

At the same time, due to its outdated chip technology, in the PC processor market, AMD's Zen architecture, with the help of TSMC's advanced technology, emerged dominant, leaving Intel with almost no means to fight back.

Realizing the problem, Intel can no longer sit still and has started to focus on process technology. With the return of Kissinger, Intel has launched the IDM 2.0 transformation strategy, setting a goal to surpass five process nodes in four years. While rapidly improving the process technology, Intel also serves as a contract manufacturer for other companies' chips.

However, the IDM 2.0 strategy is not achieved overnight. After three and a half years in office, Kissinger has already invested nearly $60 billion in upgrading chip manufacturing equipment and building factories, but the contract manufacturing business still has little actual output, making insignificant contribution to Intel's financial reports. In the global chip contract manufacturing rankings for the fourth quarter of last year, Intel did not even make it into the top ten.

Industry insiders believe that Intel's expansion plan for wafer contract manufacturing may be too ambitious.

In this process, due to fierce competition in the PC and server chip market, Intel's revenue in 2023 has actually decreased by $24 billion compared to 2020, before Kissinger took office. Even for the chip giant Intel, it is difficult to bear such a heavy financial burden, leading to huge losses. Despite the sharp decline in revenue, Intel still needs to invest nearly $20 billion annually to promote Kissinger's transformation strategy.

According to financial data, after successfully launching products at the Intel 7 and Intel 4 key milestones, Intel incurred a net loss of $1.6 billion in the second quarter. At the end of the second quarter, Intel had $11.3 billion in cash and cash equivalents, but its debt was as high as $32 billion. In the eyes of Wall Street investors, Intel may already be yesterday's news in the chip industry, and major investment banks have quickly lowered their expectations for Intel.

In short, Intel's performance in the second quarter is not just a simple case of poor performance, but reflects the challenges that this chip giant faces in multiple business areas.

In order to continue the transformation strategy, Intel has announced a significant cost-saving measure to save $10 billion by 2025. In order to reduce costs, Intel has stopped dividends for the first time in 30 years and plans to lay off 15% of its workforce globally, resulting in at least 150,000 job losses.

In order to advance the transformation strategy, Intel has announced a quite aggressive cost-saving measure, announcing that it will save $10 billion in costs by 2025. In order to reduce costs, Intel has stopped paying dividends for the first time in 30 years and plans to lay off 15% of its workforce globally, resulting in at least 150,000 people losing their jobs.

It is not difficult to see that Intel has no way out and they need to reduce all unnecessary expenses and continue to invest precious operating capital into their core chip business in order to make Intel's chip factories truly competitive and win customers from competitors.

In this burning money war, Intel has already been deeply tied to the US government's chip security strategy. In other words, the US government will not sit idly by if Intel's IDM 2.0 strategy fails.

In 2022, the US government plans to invest over $39 billion through the Chip Act, encouraging chip companies to establish chip factories in the United States, rebuilding America's leading position in the chip industry, and considering it as one of the US national security strategies. Intel is the main promoter of this act and the biggest beneficiary.

Kissinger believes that the IDM 2.0 strategy is the only way for Intel to restore its former glory. This path will exhaust almost all of its resources, but it seems that Intel has no other choice.

Intel's current troubled situation is not created overnight, but the result of a series of strategic mistakes over the years.

The Intel management has to admit that after missing the mobile era, they did not fully benefit from the AI wave. Their core business is still declining and they need to continue investing in new chip manufacturing business, leading to huge losses.

In the face of financial difficulties and competitive crises, Intel is currently discussing various plans with investment banks, with the main goal of divesting non-core businesses and adjusting capital expenditures in order to revive its leadership position in the chip manufacturing field.

It is reported that Intel may split/suspend its wafer foundry division and sell the Altera FPGA division, as well as significantly reduce unnecessary capital expenditures.

The rumored Altera division, which was acquired by Intel for $16.7 billion in 2015 and became Intel's Programmable Solutions Group, was renamed Altera as a new company in March this year.

At the time, Intel envisioned maintaining absolute control over Altera while introducing new investments, with plans to push for the company's IPO in two to three years. However, this move may have already foreshadowed the tight financial resources situation for Intel.

At the same time, this plan has also exposed Intel's inadequacy in the ai field. Altera was once Intel's largest acquisition in history, seen as an important department in the FPGA field to boost the company's artificial intelligence development.

Looking at the FPGA market, Altera and Xilinx together accounted for 90% of the market share. The latter was acquired by AMD in 2020 and its valuation soared to $50 billion in 2022. However, Intel and AMD have not yet competed in the FPGA field, and Altera is facing the risk of changing ownership first.

On the other hand, the decision to split or divest from Intel's semiconductor foundry business unit is unlikely to happen for now. Before this significant option, Intel will first make some more moderate adjustments to reduce expenses. Because this business has always been considered critical by Kissinger as Intel's key business, it is crucial for Intel to regain its position in the chip manufacturing industry and eventually compete with companies like Taiwan Semiconductor.

During this turbulent period, Intel's semiconductor veteran Chen Liwu unexpectedly resigned, casting a shadow over Intel's future.

However, regardless of the various measures and rumors mentioned above, Intel may have to accept a thorough restructuring from architecture to concept.

Intel is unable to catch up with NVIDIA and AMD in the ai field, while facing new competitors in its traditional areas of strength. Currently, Intel is banking on regaining the market through a dual strategy of semiconductor foundry and ai chips. Apart from 'cutting corners' to buy time, it remains unclear whether it will seek more assistance or cooperation plans in the future.

In short, this old chip company in a huge transformation stage still has many challenges to face.

ADAS leader Mobileye: Woke up early and rushed to the late gathering.

Mobileye was established in Israel in 1999 and was listed on the New York Stock Exchange in 2014. It is undoubtedly the "elder" of the global autonomous driving chip industry.

In 2017, Intel made a sincere offer of $15.3 billion to acquire this autonomous driving company and subsequently triggered a global trend of "server on wheels".

In the past 20 years, Mobileye, based on visual perception technology, has launched a series of solutions composed of algorithms and EyeQ series chips. Undoubtedly, Mobileye can be regarded as a major pioneer and leader in the era of automotive ADAS. Data shows that around 2019, Mobileye's ADAS business accounted for up to 90% of the global market.

Expanding territories is easy, but defending the city is extremely difficult.

Waking up early did not give this "leader" an absolute advantage or absolute dominance. Instead, over time, it has become a replaceable entity.

In recent years, as the market shifted from assisted driving to autonomous driving, Mobileye gradually fell behind. Its original "chip + algorithm" solution cannot meet the needs of automakers and autonomous driving companies. Its computing power is inferior to competitors like Nvidia, and its closed algorithm cannot meet customers' requirements for differentiation. Issues such as slow algorithm iteration, long update cycles, and lagging single-chip computing power have pushed automakers into the arms of its competitors.

Many host manufacturers have changed and turned to suppliers such as Nvidia, Qualcomm, and Horizon, and the L2 systems equipped on mass-produced cars are becoming more and more aligned with the L4 autonomous driving technology architecture. The era belonging to Mobileye is coming to an end.$Nanfang Black Sesame Group (02533.HK)$ In summary, it is a story of a former ADAS leader who missed the first-mover advantage at the beginning of the intelligent driving trend and continuously lost customers, struggling to break through under the siege of new players. From the earliest days to later BMW and Weltmeister, the list of Mobileye's lost customers keeps growing with new names. Looking at it now, Mobileye's decline in both high-end Supervision and basic ADAS has not been truly halted.

Computing power, black box mode, product iteration cycle, and more have become the straws that broke Mobileye's back.$Tesla (TSLA.US)$Even now, realizing the problem, Mobileye, which is slow and slow step by step, will only find it increasingly difficult in the autonomous driving market. On the one hand, in terms of high-end products, Nvidia is becoming a common choice for domestic car companies with its hardware and open ecosystem advantages, and the development model based on Nvidia's underlying software and hardware is gradually solidifying. On the other hand, local players represented by Horizon are also gaining ground, squeezing Mobileye's survival space. In addition, there are strong manufacturers like Huawei expanding aggressively in a new way. There isn't much cake left for Mobileye.

Even though it is now aware of the problem, Mobileye, which is slow step by step, will only find it increasingly difficult in the autonomous driving market. On the one hand, in terms of high-end products, Nvidia is becoming a common choice for domestic car companies with its hardware and open ecosystem advantages, and the development model based on Nvidia's underlying software and hardware is gradually solidifying; on the other hand, local players represented by Horizon are also gaining ground and encroaching on Mobileye's survival space. In addition, strong manufacturers such as Huawei are expanding aggressively in a new way. There is not much cake left for Mobileye.

Although Mobileye has long been spun off from Intel and is independently listed. But its heyday is a thing of the past and is not enough to support the market's long-term confidence in it.

In the second quarter financial report of 2024, Mobileye disclosed a series of worrying data. Mobileye's revenue in the second quarter of 2024 was $0.439 billion, a 3% decrease year-on-year, with some growth compared to the first quarter, but the overall trend is not optimistic. The net loss reached $86 million, more than doubled from the same period last year, and the adjusted net income was $76 million, a 44% decrease year-on-year.

In the past few months, Mobileye's stock price has fallen by nearly 50%, and has dropped by nearly 65% since the beginning of this year.

As the former leader in automotive ADAS, Mobileye has not thrived in the market and has instead experienced a series of depreciations in the face of fierce competition, which is indeed regrettable.

Toshiba, a microcosm of the decline of the Japanese semiconductor industry.

Toshiba is not only a household appliance giant in Japan, but also one of Japan's largest semiconductor manufacturers.

Established in 1875, from the earliest incandescent lamps to later home appliances, Toshiba's business gradually expanded to include consumer products, information communication, semiconductors, etc., and was listed on the Tokyo Stock Exchange in 1949. Over the long term, it has been an important member of the world's chip manufacturers.

From an absolute giant with dominant position in industries such as home appliances, semiconductors, and computers, to being "dismembered" and sold, from being a giant to struggling in operation, what has Toshiba experienced in between?

东芝的衰落也可以说是日本制造业衰落的一个缩影。

二战结束以后,在美国的扶持下日本迅速崛起,美国将大量的科技订单交付给日本,以此扶持日本快速恢复经济水平。

恰逢半导体行业第一次热潮兴起,许多日系企业乘着时代的东风迅速崛起。

上世纪80年代初,日本超越美国成为全球最大半导体生产国,$日本电气(6701.JP)$(NEC)、东芝和In addition, the impact of the depreciation of the yen, the Japanese tourism industry has gradually recovered to the level of 2019 since the beginning of this year, which has also driven a surge in sales at Japanese department stores. The stock price of Mitsukoshi Isetan (3099.JP) has also risen sharply by more than 86% this year.3家企业垄断了全球半导体前三名。尤其是在DRAM存储器领域,日本占据全球80%市场份额。

In contrast, companies led by Intel in the United States have suffered losses for several years and have been forced to close many factories. The United States will not allow its technological leadership to be surpassed, so it has started anti-dumping lawsuits against major Japanese semiconductor manufacturers and has increased tariffs on these companies through a semiconductor cooperation agreement with Japan.

By the end of the 1980s, Japan entered a 30-year period of economic recession, exacerbated by multiple suppressions by the United States on the semiconductor industry. Eventually, in the 1990s, Japan handed over the global semiconductor sales throne to the United States, specifically to Intel.

Nevertheless, Toshiba maintained its position in the top five global semiconductor sales rankings even after the 1990s. In 2000, Toshiba's semiconductor sales were second only to Intel, ranking at the second position globally.

However, this also became Toshiba's last glory. Since the 21st century, with the transfer of the global semiconductor industry, manufacturing has gradually shifted to low-cost countries like China and South Korea, weakening the advantages of Japanese companies. Meanwhile, under the pressure from companies like TSMC and Samsung, Toshiba's market share continues to decline.

Due to poor management, Toshiba resorted to financial fraud in order to maintain the appearance of prosperity.

In 2015, Toshiba was exposed for eight years of financial fraud, which plunged the company into a deep crisis of public opinion and finance. It faced a damaged reputation, a plummeting stock market, and recorded a record annual loss of 8.8 billion yen. To recover from this loss, Toshiba had to sell off its businesses and the once-giant company collapsed.

In 2016, Toshiba sold its white goods business to $Midea Group Co., Ltd (000333.SZ)$In 2017, Toshiba transferred 95% of the equity of its imaging solution company (TVS) to Hisense Group.

In 2018, Toshiba, which was trapped in a predicament, turned its attention to the only profitable semiconductor business at that time. It sold 49.9% of the equity of its core business, storage, to a corporate alliance including Bain Capital of the United States for approximately 2 trillion yen. It was renamed KIOXIA in 2019 and is now one of the major producers of NAND Flash memory in the world.

However, due to the downturn in the global memory market, KIOXIA has incurred huge losses for three consecutive quarters in 2023, resulting in a financial deficit. The merger negotiations between KIOXIA and [missing translation].Company names in the text have already been specified how to translate.However, multiple merger negotiations between KIOXIA and [missing translation] have all ended in failure.

However, Toshiba, which has been selling assets for many years, still has not solved the problem.

As a giant of Japanese companies, Toshiba has always been a globally renowned electronics manufacturer, with significant influence in the fields of household appliances, electricals, energy, infrastructure, and semiconductors. It has once created many "Japanese first" and its products are even regarded as synonymous with high-quality products in the market.

However, after blindly running forward, it left behind endless sighs.

After a series of events such as the collapse of the Japanese electronics industry, intense market competition, financial fraud, nuclear power losses, and selling off core businesses, Toshiba's management became increasingly poor and long-term chaotic. In 2023, it accepted the acquisition invitation from JIP Consortium and finally embarked on the path of delisting 'redemption'.

Now, after going through a series of capital market shuffles and nearing the completion of privatization, Toshiba will adhere to the so-called 'doing the right thing' and shift its focus to the fields of infrastructure, electric machines, and semiconductors.

Qimonda: The rise and fall of the storage industry in Europe

When it comes to companies that have rapidly declined from their peak, there is a name that I believe everyone is familiar with, and that is Qimonda AG. It was a new memory company spun off from Infineon on May 1, 2006.

On the same day that it was spun off from its parent company Infineon, Qimonda went public on the New York Stock Exchange, becoming the memory product company that completed its IPO the fastest in the wave of spin-offs.

After going public, Qimonda embarked on a two-year sprint.

In 2006, Qimonda was a leading global DRAM company, a leader in 300mm wafer manufacturing, and one of the largest suppliers of PC and server DRAM products. At the same time, it had global partners and contract manufacturers such as Nanya Technology and Powerchip Technology.

In September 2006, Qimonda collaborated with Nanya Technology to launch the 75nm DRAM trench technology, further reducing chip size.

In 2007, as a global DRAM giant, Qimonda's business was focused on DRAM memory modules, memory particles of computer graphics cards, consumer-grade DRAM memory, and high-speed DRAM cache in mobile storage devices - these businesses once accounted for 90% of Qimonda's revenue. At that time, Qimonda had five 300mm wafer production bases in Europe, Asia, and North America, including five global research centers, including the Qimonda Xi'an research and development center, and was dominating the market.

In November 2007, Qimonda released the GDDR5 white paper, and its GDDR5 memory production equipment had been mass-produced - at a time when the mainstream memory chip was GDDR4 worldwide. For Qimonda, which was trying to skip GDDR4 and directly adopt GDDR5, this was undoubtedly a huge leap forward.

In February 2008, Qimonda was the first in the world to announce the breakthrough of the 30nm process memory, and announced embedded technology, which was also an important technological milestone in the history of DRAM development. Qimonda redefined DRAM technology as "embedded" and "stacked".

However, things change rapidly and unpredictably.

According to data, Qimonda's revenue in the first half of 2008 was 0.925 billion euros, a year-on-year decrease of 57%, and a net loss of as high as 1.058 billion euros. In the first half of the 2007 fiscal year, Qimonda still had a substantial net profit of 0.335 billion euros.

In other words, in just one year, Qimonda went from a company with a semi-annual profit of over 0.3 billion euros to a company with a net loss of over 1 billion euros, a profit decline of over 300%.

Looking back now, Qimonda's collapse began from "internal and external troubles".

From the perspective of the times, the 2008 U.S. financial crisis broke out, and its huge impact quickly spread from the U.S. stock market to European companies listed in the U.S., and Qimonda was a German company listed on the NYSE.

The drop in storage prices: The second reason is the underperformance of Windows Vista. In November 2006, Windows Vista was officially launched. In the financial report of Chimonda in 2006, it was expected that the launch of Vista would drive a 20% growth in DRAM. However, due to the vulnerability issues of the Vista operating system, sales fell short of expectations, resulting in an oversupply in the DRAM market and a significant price decline.

By the end of 2007, the price of DRAM had dropped to only one-fourth of the same period in 2006. In 2008, with the outbreak of the financial crisis, the price of DRAM plummeted even further. The price of DRAM chips dropped from $2.25 to $0.31, while the material cost for DRAM manufacturers during the same period was $0.6-0.7, and the cash cost was around $1.4. Coupled with Chimonda's relatively high cost, the market price was high, and Chimonda, which had higher production costs and higher market selling prices, was the first to be affected by the price drop.

Intensified market competition: South Korean memory manufacturers represented by Samsung have had three famous countercyclical investments in the process of memory development, with the most severe one in 2007.

In 2007, Samsung used 118% of its total profit for DRAM expansion, increasing the supply chain of the DRAM market and launching a price war by increasing production capacity intentionally to cause industry losses. The price of DRAM fell below cash cost in 2008 and even below material cost at the end of the year.

Samsung's countercyclical large-scale investment and expansion under the market downturn and the support from the South Korean government further worsened the situation for Chimonda, which was already in a state of supply-demand imbalance.

Comprehensive defeat: The final straw that crushed Chimonda came from the German government's abandonment. Compared to South Korea, Germany chose to abandon Chimonda in dealing with its difficulties.

According to publicly available information, in March 2008, Chimonda had negotiations with Macronix International Co., Ltd about their joint venture, Inotera Memories Inc., and Macronix International Co., Ltd hoped to take over 35% of Chimonda's equity. However, just a few days prior to this, Macronix International Co., Ltd reached an agreement with Micron, and the two parties established a joint venture, resulting in the termination of negotiations with Chimonda.

In October, Chimonda officially split from Macronix International Co., Ltd. Micron acquired Chimonda's entire stake in PowerChip Technology Corporation for $400 million, making PowerChip Technology Corporation a joint venture between Macronix and Micron.

After the breakup, Qimonda for the first time applied to the relevant German authorities for a loan to renovate its wafer fab in Dresden, so that it could produce chips with the latest process technology, as well as to pay off the debt to Huaya Science, etc. At this time, Qimonda had already been losing money for several months, but still claimed that the company's cash flow was good.

Immediately afterwards, Qimonda announced a plan to lay off 3,000 employees, which undoubtedly intensified investors' concerns about the company's market performance and further expanded concerns about the shrinking German job market.

On November 26, Qimonda, which could no longer sustain itself, once again applied to the German government, Infineon, and the Portuguese State Bank for a funding of 0.325 billion euros to get through this wave of economic crisis and the downturn of the DRAM industry.

Just when almost everyone believed that the German government would contribute to saving this last remaining storage company in Europe, Infineon, as the parent company and major shareholder, rejected the German government's funding plan. Subsequently, the German government chose to abandon Qimonda at the last minute.

On January 23, 2009, Qimonda, which did not receive the bailout funds, had to reluctantly declare bankruptcy. Qimonda, the light of European storage, came to an end in just three years.

At that time, the global monthly average shipment of DRAM was about 0.92 million wafers, and Qimonda's capacity in Germany and the United States' 12-inch wafer fabs was about 0.06-0.07 million wafers. Addition to the contract manufacturing capacity of Nanya, Qimonda's global monthly capacity was estimated to be about 0.08 million-0.09 million wafers, with a market share of nearly 10%, ranking fifth in the world.

On April 1, 2009, Qimonda officially entered bankruptcy liquidation proceedings.

The decline of Qimonda cannot be attributed solely to simple management and technological issues.

According to the information disclosed by United Microelectronics Corporation's contractor Huabang, United Microelectronics Corporation's 65nm process left to Huabang was competitive for 2-3 years at that time. This process could continue for two generations of process updates, and United Microelectronics Corporation also had a more advanced 46nm process. However, United Microelectronics Corporation did not wait for the construction and commissioning of the new process line.

The real reason for this is mainly due to financial constraints and the government's refusal to provide assistance.

In contrast, in 2008, with the support of the government, Samsung invested 118% of its total profit to expand production; Similarly, SK Hynix also repeated Samsung's counter-cyclical large investment, smashing 26 billion US dollars to build two new memory factories in South Korea. The source of funding is led by the South Korean government, with loans from the state-owned bank KEB bank for investment.

It can be seen that Samsung and SK Hynix's 'counter-cyclical investment' is the result of South Korea's national efforts to develop the memory industry, which has created a market share of over 70% for the two companies.

United Microelectronics Corporation's decline has left Europe without a major memory plant.

Recently, Infineon settled with United Microelectronics Corporation for 0.84 billion US dollars, ending a 14-year compensation dispute. With everything settled, there may be no more news of United Microelectronics Corporation in the future.

United Microelectronics Corporation/GlobalFoundries, the downfall of the semiconductor manufacturing giants

United Microelectronics Corporation and$GlobalFoundries(GFS.US)$(GlobalFoundries) is a fallen star in the wafer foundry field.

UMC is the second largest wafer foundry factory in Taiwan, while GlobalFoundries became the world's second largest pure wafer foundry factory when it was spun off from AMD's wafer manufacturing department in 2009. Both companies are in the second tier of global wafer manufacturing, second only to TSMC.

However, as Moore's Law approaches its limit, advanced processes have become a game that only the wealthy can afford to play. The investment in advanced processes is huge, and the risks are exceptionally large, leaving few players in the industry.

In August 2018, UMC announced that it would abandon R&D in advanced processes below 12nm, no longer pursuing the goal of becoming the market leader, but instead focusing on improving the company's return on investment. Around the same time, GlobalFoundries also announced the abandonment of 7nm LP process R&D, redirecting resources to 12nm and 14nm.

As a result, only TSMC, Samsung, and Intel remain as the global manufacturers developing and producing 10/7/5/3nm processes.

However, UMC and GlobalFoundries, which have abandoned advanced processes, are seeing continued erosion of market share. For example, AMD, which was once associated with GlobalFoundries, has fully switched to TSMC. Both UMC and GlobalFoundries have admitted that the speed at which customers are transitioning to processes below 10nm has exceeded expectations, leading to unfavorable business conditions and prospects.

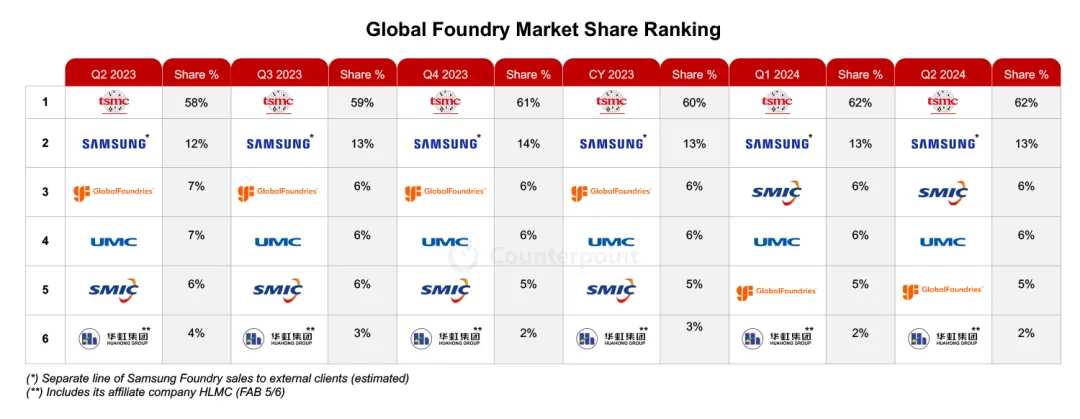

A recent report released by Counterpoint, a research firm, stated that global wafer foundry industry revenue is benefiting from strong growth in AI demand. According to Counterpoint Research's 'Wafer Foundry Quarterly Tracker' report, industry revenue in the second quarter of 2024 increased by about 9% quarter-on-quarter and 23% year-on-year due to strong AI demand.

According to the report, in the second quarter of this year, Taiwan Semiconductor ranked first in the global chip manufacturing industry with a market share of 62%, while Samsung's share was 13%.$ Semiconductor Manufacturing International Corporation (00981.HK) $United Microelectronics and GlobalFoundries both tied for third place with a market share of 6%, while GlobalFoundries' share was 5% and Huahong's share was 2%.

It is worth noting that the recovery speed of wafer foundry and semiconductor market in mainland China is faster than that of global counterparts. Counterpoint stated that SMIC and Huahong, among other mainland Chinese wafer foundry manufacturers, have released strong quarterly performance and positive guidance, as customers without wafer fabs in mainland China entered the inventory adjustment phase earlier than their global counterparts.

SMIC showed a strong performance in the quarterly results. For the third quarter performance, SMIC has given revenue guidance of a 13% to 15% increase compared to the previous quarter, mainly driven by the recovery of demand in the Chinese market, as well as the resurgence in demand for CIS, PMIC, IoT, TDDI, and LDDIC. The demand for 12-inch wafers at SMIC has also improved, leading to an increase in the average selling price (ASP) after semiconductor customers without wafer fabs replenished. SMIC remains cautiously optimistic about revenue growth for the entire year, with further increases in capacity utilization rates.

In comparison, United Microelectronics and GlobalFoundries both experienced a year-on-year decrease of 1 percentage point in their market share in the second quarter.

At that time, United Microelectronics and GlobalFoundries' decision to abandon advanced processes may have been correct. However, looking at the current market situation, they still miscalculated and are now experiencing the consequences of their decision.

In the future, as process technology continues to shrink, more and more customers will opt for more advanced processes to achieve higher performance, lower power consumption, reduce chip size, and lower costs. In the large-scale mature process market in China, it faces strong competition from domestic wafer foundry manufacturers.

In short, United Microelectronics Corp and GlobalFoundries have started to feel the loss of customers, and their market share has been gradually surpassed by Semiconductor Manufacturing International Corporation.

In conclusion,

Behind the decline of any giant, there are multiple reasons.

From the transition of these companies from prosperity to decline, we can vaguely sense that once the era changes, technological innovations occur, and industries undergo drastic transformations, some business giants will quickly decline.

Emerging markets are constantly developing, with endless industry demands, and the business world is ever-changing. The cycle of rise and fall repeats itself in the fate of these giants.

However, one thing is clear: whoever can firmly grasp the two key factors of technology and innovation is more likely to stand out in intense competition, establish a foothold in the tide of the era, and become a temporary winner.

But no one should think they are safe.

Editor/rice