Before the non-farm data, there is new evidence of the cooling of the US job market, and economic concerns support a substantial rate cut bet. The yield curve of the 2-year/10-year US Treasury bonds, which briefly inverted for the third time in two years. The S&P 500 fell for the third consecutive day, with Broadcom falling more than 4% after hours, Tesla rising nearly 5%, and Nvidia and Chinese concept stocks rising nearly 1%. The yen reached a one-month high, and the offshore renminbi rose by 300 points to break 7.09 yuan. Gold rose briefly by 1%, and oil prices rose more than 2% before falling. US oil fell below $70 for the first time in 15 months over two days.

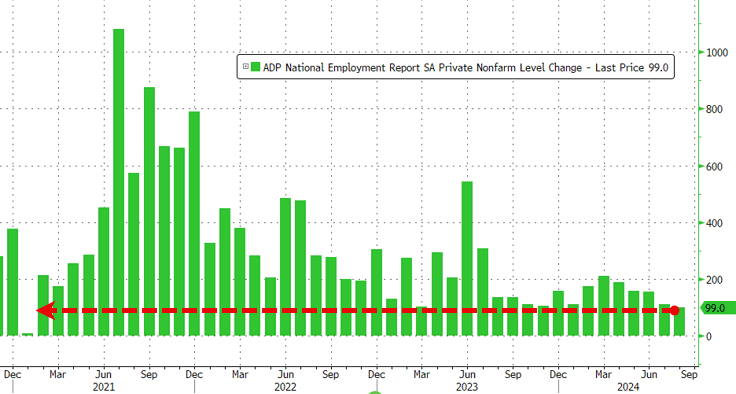

The labor market data is mixed. The unexpected decrease in the small non-farm payroll employment in the U.S. in August to 0.099 million is the lowest in three and a half years, and the July data was revised down, showing a sharp slowdown in the labor market. However, the initial jobless claims of 0.227 million people at the beginning of each week decreased compared to the previous week, and the continued unemployment benefit claims also fell to the lowest level in nearly three months.

However, the U.S. ISM non-manufacturing index expanded moderately for the second consecutive month in August, and the final value of the Markit services PMI announced earlier was the highest in nearly two and a half years, alleviating concerns about an economic hard landing. Mary Daly, a member of the Fed's policymaking committee and president of the Federal Reserve Bank of San Francisco, said that the Fed needs to lower its policy rates because inflation is declining and the economy is slowing down.

After the release of the two employment data, U.S. Treasury yields and the DXY index both temporarily declined and hit daily lows. After the release of the two services PMI data, U.S. Treasury yields and the DXY index rose temporarily, and then hit daily highs. The market's bet on a significant 50 basis point rate cut by the Fed in September fell slightly from 44% to 41%, while the probability of a 25 basis point rate cut rose to 59%.

The market is focused on the critical non-farm payroll data to further validate the extent of the rate cut. Economists generally expect an increase of 0.16 million non-farm jobs in August, higher than the 0.114 million in July. The unemployment rate is expected to drop slightly to 4.2%.

The major U.S. stock indices rose early in the morning, then fell back in the midday, and later only the Nasdaq successfully rebounded, but still significantly lower than the rise of over 1% in the early morning. Most of the stock indices closed at daily lows towards the end of trading, with the S&P and Russell 2000 index falling for three consecutive days, but the China concept stock index rose against the trend by nearly 1%. In terms of sectors, the consumer discretionary stocks led the gains, with Tesla rising by 4.9%.

Only the Nasdaq rose among the three major U.S. stock indices: the S&P 500 index fell 0.3% to 5,503.41 points. The Dow Jones Industrial Average, which is closely related to the economic cycle, fell 0.54% or 219 points to 40,755.75 points. The Nasdaq, which is dominated by technology stocks, rose 0.25% to 17,127.66 points. The Nasdaq 100 rose 0.05%. The Nasdaq Technology Market Value Weighted Index (NDXTMC), which measures the performance of Nasdaq 100 technology stocks, was almost flat. The Russell 2000 index, which is more sensitive to the economic cycle, fell 0.61%. The VIX fear index fell 6.66% to 19.90.

Most U.S. industry ETFs closed lower. The CSI Consumer Staples ETF and the Global Aviation Industry ETF rose more than 1%. The Medical Industry ETF and the Financial Industry ETF fell by more than 1%, while the Regional Banks ETF, the Banks ETF, and the Energy Industry ETF fell by nearly 1%. The Biotech Index ETF and the Daily Consumer ETF each fell by less than 0.5%.

Most of the 11 sectors of the S&P 500 index fell more than rose. The Health Care sector fell 1.39%, the Industrial and Financial sectors fell the most by 1.18%, the Materials and Energy sectors fell the most by 0.8%, and the Information Technology/Technology sector rose 0.05%, ranking third. The Telecommunications sector rose 0.52% and the Consumer Discretionary sector rose 1.41%.

Only Microsoft among the 'Big Tech Seven Sisters' fell. Tesla rose 4.9%, with the company expecting to offer Full Self-Driving (FSD) in China and Europe in the first quarter of 2025, pending regulatory approval. Nvidia rose 0.94%, Meta, the 'Metaverse', rose 0.8%, Amazon rose 2.63%, Google Class A rose 0.5%, Apple rose 0.69%, Bank of America expects the upcoming iPhone launch event to boost Apple's stock price, while Microsoft fell 0.12%.

Most chip stocks fell. The Philadelphia Semiconductor Index fell 0.6%; the SOXX industry ETF fell 0.54%; the Nvidia 2x Long ETF rose 1.71%. Intel fell 0.15%, as the company is considering selling part of its stake in Mobileye, an autonomous driving software company. ON Semiconductor fell 0.6%, ASML Holding ADR fell 1.96%, Applied Materials fell 1.17%, Qualcomm fell 0.47%, KLA Corp fell 2.29%, AMD fell 1.02%, Broadcom fell 0.84%, while Arm Holdings rose 1.77%, TSMC ADR rose 1.76%, and Micron Technology rose 0.11%.

Most AI concept stocks fell. C3.ai fell 8.21%, briefly falling 18% during trading, marking its biggest drop since September 2023. The company's subscription revenue in the latest quarter fell short of expectations, and the timing of profitability remains unknown. Super Micro Computer fell 2.09%, BigBear.ai fell 2.88%, Dell fell 1.74%, CrowdStrike fell 1.11%, SoundHound AI, an AI voice company in which Nvidia holds shares, fell 0.22%, Palantir fell 1.41%, Serve Robotics fell 7.61%, while BullFrog AI rose 5.96% and Oracle rose 1.32%.

China concept stocks index outperformed the US market. The Nasdaq Golden Dragon China Index rose 0.88%. Among the ETFs, the China Technology Index ETF (CQQQ) rose 0.63%. The China Internet Index ETF (KWEB) fell 0.04%.

Among the popular China concept stocks, NIO rose 14.39%, with Q2 revenue increasing by 99% year-on-year and Q3 delivery guidance exceeding market expectations. JPMorgan raised its rating for Xpeng Automotive ADR from Neutral to Overweight, with a target price raised from $8 to $11.5. JD.com rose 4.74%, Li Auto rose 0.48%. Citi downgraded its rating for Li Auto to Neutral, citing performance risks next year. Bilibili rose 2.26%, New Oriental rose 1.98%, Trip.com rose 0.74%, Baidu rose 0.52%, while Alibaba fell 0.05%, Pinduoduo fell 0.08%, Tencent ADR fell 0.08%, Meituan ADR fell 0.13%, Vipshop fell 0.16%, Netease fell 1.24%, and JD.com fell 1.68%.

In other key stocks: (1) Broadcom's AI-related revenue in Q3 fell short of expectations, with weak revenue guidance for Q4, causing the stock to drop more than 5% after hours. (2) Digital signature solution provider Docusign exceeded expectations for Q2 subscription revenue and raised its full-year revenue guidance, causing the stock price to drop more than 5% after hours. (3) Robotic process automation software company UiPath reported better-than-expected Q2 results and full-year guidance, causing the stock price to rise more than 8% after hours. (4) Applied Digital, which received $160 million financing from Nvidia, rose by approximately 66%, marking its largest single-day gain since May 2023.

The expectation of a US economic recession has intensified, and European stocks have fallen for the fourth day:

The pan-European Stoxx 600 index fell 0.54% to 512.05 points. Major sectors had mixed performance, with utilities stocks rising 1.66% while healthcare stocks declined 1.4%. Among the component stocks, Tiffany, a subsidiary of LVMH Group, will open three new stores in China by 2025.

The German stock index fell 0.08%. The French stock index fell 0.92%, the Italian stock index rose 0.01%, the Spanish stock index rose 0.53%, and the UK stock index fell 0.34%.

On the "mini non-farm payroll" release day, the yield on the 10-year US Treasury bond fell by 2.45 basis points, and the 2/10-year yield curve briefly ended its third inversion within a month. The 2-year yield hit a new low for over a year.

US bonds: At the end of the day, the yield on the 2-year US Treasury bond, which is more sensitive to monetary policy, fell by 0.62 basis points to 3.7476%. After the ADP "mini non-farm payroll" release, it dived and hit a daily low of 3.7106%, but rebounded after the ISM non-manufacturing data release, hitting a daily high of 3.7910%.

The yield on the 10-year benchmark US Treasury bond fell by 2.45 basis points to 3.7307%, significant dive after the ADP employment data release at 20:15 Beijing time, refreshing the daily low of 3.7194% near the release of the US ISM non-manufacturing index at 21:55. After the release of the ISM non-manufacturing data, it rebounded and approached the daily high of 3.7722% refreshed at 17:09. US stocks turned lower again during midday trading.

Eurozone bond yields fell by about 2 basis points: the yield on the 10-year German bond, the benchmark for the euro zone, fell by 1.6 basis points. It fell significantly after the release of the US ADP "small non-farm" employment data and hit a daily low before the release of the ISM non-manufacturing data. The yield on the 2-year German bond fell by 2.7 basis points. The yield on the 10-year French Treasury bond fell by 2.1 basis points, the yield on the 10-year Italian Treasury bond fell by 2.0 basis points, the yield on the 10-year Spanish Treasury bond fell by 2.1 basis points, and the yield on the 10-year Greek Treasury bond fell by 1.5 basis points. The yield on the 2-year UK bond fell by 2.5 basis points, and the yield on the 10-year UK Treasury bond fell by 2.0 basis points.

According to CCTV News, on September 5th local time, the IFO Institute for Economic Research in Germany pointed out that after a 0.3% economic contraction last year, Germany's economic growth will stagnate, with a downward revision of 0.4 percentage points for this year's growth expectation, and a downward revision of 0.6 percentage points for Germany's economic growth expectation in 2025.

"Small non-farm" data drove the DXY index to a one-week intra-day low. The release of the US ISM non-manufacturing data caused the DXY index to turn briefly higher before closing 0.3% lower. Non-US currencies rose across the board, with the Japanese yen breaking through 143 to a one-month high and rising for the third consecutive day. Offshore renminbi rose 235 pips to nearly a 16-month high at the close, breaking above 7.09 yuan:

US Dollar: The DXY index, which measures the US dollar against a basket of six major currencies, fell by 0.29% to 101.064 points. After the release of the US ADP employment data at 20:15 Beijing time, it plunged and hit a daily low of 100.964 points. After the release of the US ISM non-manufacturing index at 22:00, it rebounded briefly and turned higher. It spent most of the day in a downward trend, except for the volatility caused by the ISM data. It reached 100.514 points on August 27th.

The Bloomberg Dollar Index fell by 0.19% to 1230.74 points. During the Asia-Pacific midday session, it briefly hit a daily high of 1233.12 points. It remained in a volatile downward trend for the rest of the day, hitting a daily low of 1230.20 points after the midday session of US stocks, and approaching the bottom of 1221.94 points on August 26th.

Non-dollar currencies generally rose. The euro rose 0.26% against the dollar, the pound rose 0.24% against the dollar, and the dollar fell 0.27% against the Swiss franc; among commodity currencies, the Australian dollar rose 0.23% against the dollar, the New Zealand dollar rose 0.39% against the dollar, and the dollar fell 0.02% against the Canadian dollar.

Yen: The yen rose 0.21% against the dollar, to 143.44 yen. In pre-market trading, the yen reached a high of 142.852, and the U.S. ISM services PMI data caused a short-term decline in the yen and hit a daily low of 144.23 yen.

Offshore Renminbi: The offshore renminbi (CNH) rose 235 points against the dollar in the late trading session, to 7.0899 yuan, with overall trading in the range of 7.1144-7.0871 yuan during the day. On August 30, the offshore renminbi rose to 7.0710 yuan.

Cryptocurrencies showed more decline than rise. The largest market-cap leader, Bitcoin, fell 3.51% at the close to $56,305.00. The second largest, Ethereum, fell 3.51% at the close to $2,380.00, both hitting monthly lows.

Concerns about global economic recession have overshadowed the OPEC+ decision to postpone production increases by at least two months, as well as the good news of the U.S. oil inventory dropping to a new low for a year. Oil prices rose by more than 2.3% before falling back to lows of over 14 months, with U.S. oil rising over 2.3% but closing down 0.07% and Brent oil rising over 2% but closing down 0.01%:

U.S. Oil: WTI October crude oil futures closed down $0.05, or 0.07%, at $69.15 per barrel, marking a new low since June 2023.

Brent Oil: Brent November crude oil futures closed down $0.01, or over 0.01%, at $72.69 per barrel.

Intraday Performance: Reports suggest that OPEC+ has reached a consensus to postpone the planned increase in oil supply by two months. In addition, the EIA government edition of the weekly crude oil inventory report showed a decrease of approximately 6.9 million barrels last week, hitting a new low since September of last year. Influenced by both, U.S. and Brent oil prices continued to rise, with early U.S. oil hitting over 2.3% nearing the $71 per barrel mark and Brent oil rising over 2% surpassing the $74 per barrel mark. However, concerns about an economic recession triggered heightened risk aversion, resulting in a sharp drop for both oils. After hitting a daily low in the midday session, U.S. oil fell by nearly 0.7%, dropping below the $69 per barrel mark, and Brent oil dropped by nearly 0.5% near the $72 per barrel mark.

Natural gas: US natural gas futures rose by over 5.08% in October, to $2.2540 per million British thermal units. The increase in US natural gas inventories last week was lower than market expectations.

Although intraday ISM services PMI data narrowed the increase in gold prices, the significant decrease in the number of July JOLTS job vacancies on Wednesday, combined with ADP data, suggests a significant labor market slowdown. The weakening of the US dollar and Treasury yields boosted the prices of precious metals, driving gold prices to a near one-week high.

Gold: COMEX December gold futures rose 0.84% at the close, to $2547.20 per ounce. Spot gold maintained its upward trend throughout the day. Ahead of the pre-market "small non-farm payroll" and initial claims data, it reached a daily high, rising by over 1.1% to surpass the $2520 integer level. At the close, spot gold rose 0.86% to $2516.76 per ounce.

Silver: COMEX December silver futures rose 2.14% at the close, to $29.168 per ounce. Spot silver maintained its upward trend throughout the day, with the highest increase in the early session pushing above $29.10, and at the close, spot silver rose by 1.94% to $28.8229 per ounce.

Analysis points out that if the non-farm payroll report released on Friday in August shows an unemployment rate reaching the highest level since 2021 at 4.3%, and with the market placing large bets on a significant interest rate cut, gold prices are set to return to historic highs. It is possible to surge to $2700 by the end of the year.

London industrial base metals saw mixed movements. "Dr. Copper," the economic indicator, rose by over 1.47% to $9092 per ton, with zinc up by 272 dollars. However, aluminum fell by over 2.07%, closing down by 18 dollars, while lead and nickel dropped by 25 dollars and 136 dollars respectively.

COMEX copper futures rose 1.50%, to $4.1402 per pound.

Editor/Somer