The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Bio-Rad Laboratories, Inc. (NYSE:BIO) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Bio-Rad Laboratories Carry?

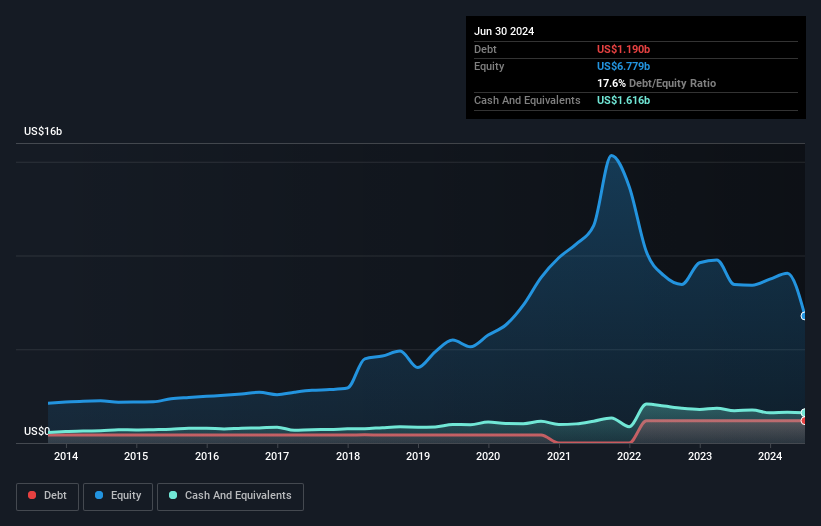

The chart below, which you can click on for greater detail, shows that Bio-Rad Laboratories had US$1.19b in debt in June 2024; about the same as the year before. But it also has US$1.62b in cash to offset that, meaning it has US$425.8m net cash.

A Look At Bio-Rad Laboratories' Liabilities

According to the last reported balance sheet, Bio-Rad Laboratories had liabilities of US$487.0m due within 12 months, and liabilities of US$2.42b due beyond 12 months. Offsetting these obligations, it had cash of US$1.62b as well as receivables valued at US$455.3m due within 12 months. So its liabilities total US$838.2m more than the combination of its cash and short-term receivables.

According to the last reported balance sheet, Bio-Rad Laboratories had liabilities of US$487.0m due within 12 months, and liabilities of US$2.42b due beyond 12 months. Offsetting these obligations, it had cash of US$1.62b as well as receivables valued at US$455.3m due within 12 months. So its liabilities total US$838.2m more than the combination of its cash and short-term receivables.

Given Bio-Rad Laboratories has a market capitalization of US$9.28b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Bio-Rad Laboratories also has more cash than debt, so we're pretty confident it can manage its debt safely.

While Bio-Rad Laboratories doesn't seem to have gained much on the EBIT line, at least earnings remain stable for now. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Bio-Rad Laboratories's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Bio-Rad Laboratories may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, Bio-Rad Laboratories recorded free cash flow worth 52% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing Up

We could understand if investors are concerned about Bio-Rad Laboratories's liabilities, but we can be reassured by the fact it has has net cash of US$425.8m. So we don't have any problem with Bio-Rad Laboratories's use of debt. Even though Bio-Rad Laboratories lost money on the bottom line, its positive EBIT suggests the business itself has potential. So you might want to check out how earnings have been trending over the last few years.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.