除了区域差异,企业盈利也出现分化。浙商证券发布的《餐饮行业2024年半年度业绩综述报告》也提到,2024年1-6月餐饮企业注册量始终高于注销吊销量,门店供给持续上升,行业竞争持续白热化进一步促进形成了上半年餐饮整体行业的弱复苏,但优质品牌仍能脱颖而出。

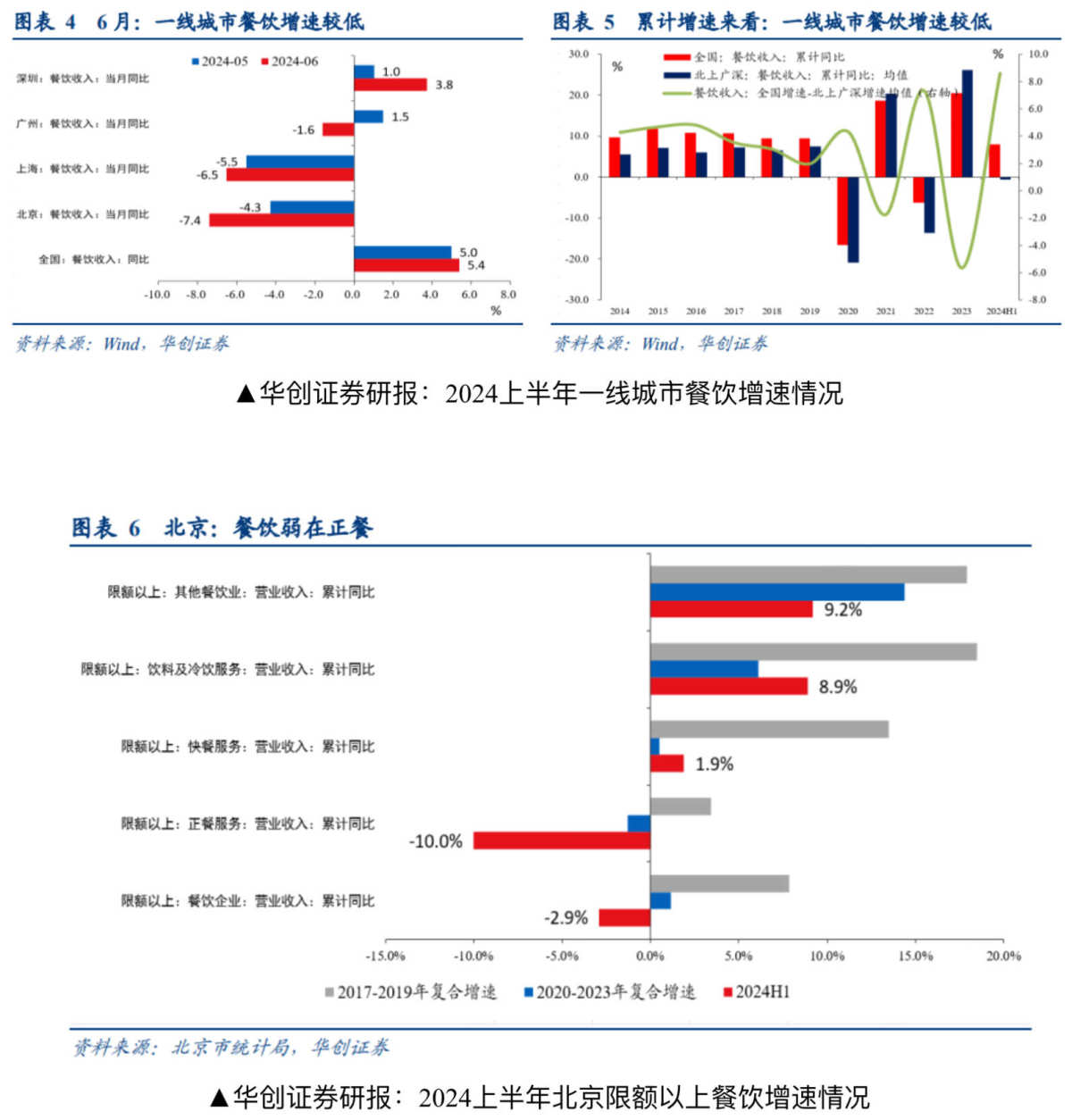

除了区域差异,企业盈利也出现分化。浙商证券发布的《餐饮行业2024年半年度业绩综述报告》也提到,2024年1-6月餐饮企业注册量始终高于注销吊销量,门店供给持续上升,行业竞争持续白热化进一步促进形成了上半年餐饮整体行业的弱复苏,但优质品牌仍能脱颖而出。Recently, the dining situation in first-tier cities such as Beijing and Shanghai has sparked heated discussions.

According to the recent consumer observation report released by Huachun Securities, the dining consumption in first-tier cities is performing worse than the national average. The national dining revenue growth rate in the first half of the year was 7.9%, while Beijing was -3.5%, Shanghai was -3.6%, Guangzhou was 3.0%, and Shenzhen was 1.3%. The national growth rate is higher than that of first-tier cities.

From the category perspective, dining in first-tier cities may be affected by the decline in regular meal consumption. The report from Huachun Securities shows that in the first half of the year in Beijing, the growth rate of above-quota dining services was -10.0%, with significant losses in regular meal services, while fast food, beverages and delivery, and catering delivery were still profitable. This means that there is significant pressure on the operation of regular meal services in Beijing.

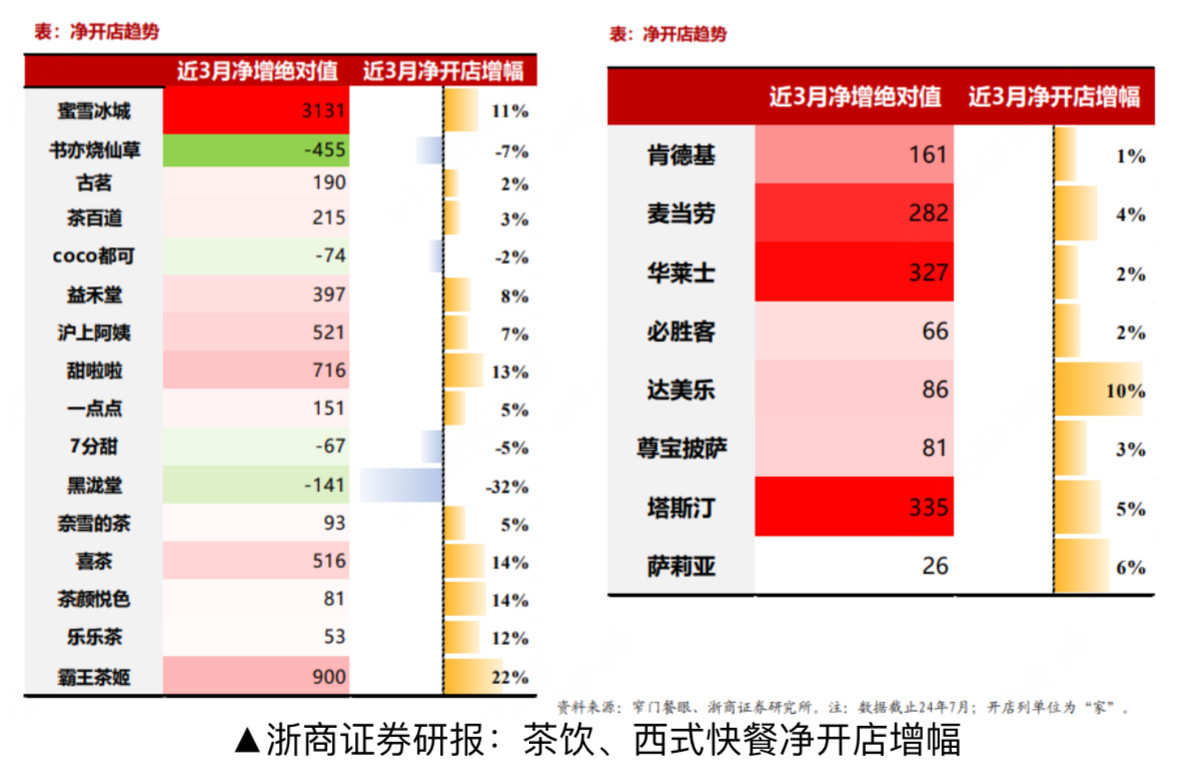

In addition to regional differences, there is also a differentiation in business profitability. The "Summary Report of the Performance of the Dining Industry in the First Half of 2024" released by Zheshang Securities mentioned that the number of dining companies registered in the first half of 2024 has consistently been higher than the number of deregistrations, indicating a continuous increase in store supply and intense competition in the industry. This has further driven the weak recovery of the dining industry in the first half of the year, but quality brands can still stand out.

In addition to regional differences, there is also a differentiation in business profitability. The "Summary Report of the Performance of the Dining Industry in the First Half of 2024" released by Zheshang Securities mentioned that the number of dining companies registered in the first half of 2024 has consistently been higher than the number of deregistrations, indicating a continuous increase in store supply and intense competition in the industry. This has further driven the weak recovery of the dining industry in the first half of the year, but quality brands can still stand out.

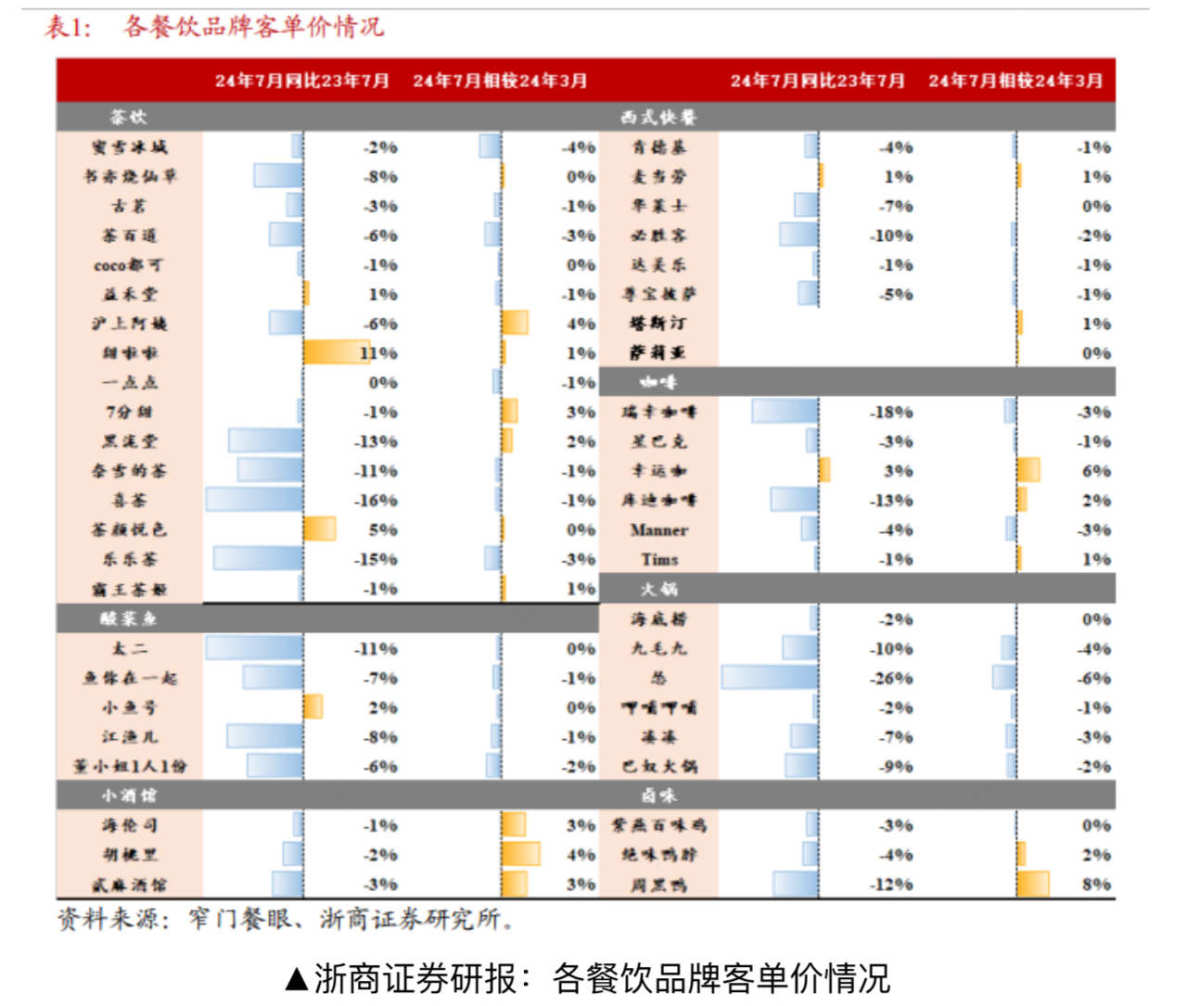

According to the aforementioned report, companies with strong brand strength and management capabilities such as Haidilao and Yum China are expected to stabilize their average customer spending, which is mainly due to their own brand strength and management capabilities.

Furthermore, from a comprehensive industry perspective, intensified competition has also led to a continued decline in average customer spending in the dining industry. Another monthly dining report published by Zheshang Securities states that brands in various dining sectors such as tea and coffee, Western-style fast food, and hot pot are still expanding, but they are experiencing a downward trend in average customer spending. Some brands in certain sectors even have double-digit declines. It is expected that the pressure on average customer spending will continue, mainly due to intensified industry competition.

According to media reports, since 2023, the opening and closing of dining establishments have remained high, indicating accelerated industry restructuring and continued market vitality. The monthly dining report shows that Western-style fast food, tea and coffee, and some hot pot brands are still actively opening new stores. According to data from Tianyancha, in the first half of this year, the number of newly registered domestic dining-related companies reached 1.347 million, while the number of deregistrations and revocations reached 1.056 million, nearly equaling the total for the entire year of 2023.