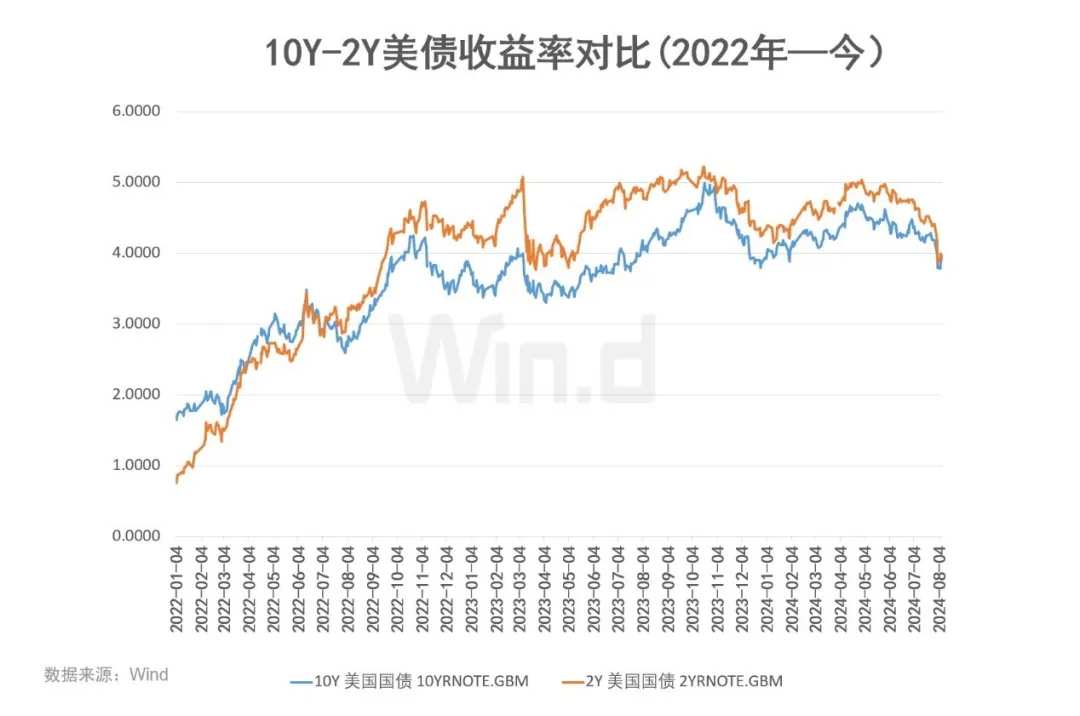

这反映出市场对美联储将在9月18日降息至少25个基点的预期升高,还有人预测最高会降息50基点。导致这一情况发生的原因是,最新数据显示7月份美国职位空缺创2021年初以来最低水平,且裁员人数也有所增加,这个消息导致收益率曲线出现剧烈变动。

这反映出市场对美联储将在9月18日降息至少25个基点的预期升高,还有人预测最高会降息50基点。导致这一情况发生的原因是,最新数据显示7月份美国职位空缺创2021年初以来最低水平,且裁员人数也有所增加,这个消息导致收益率曲线出现剧烈变动。Source: Wind

On September 5, there was another major change in the overnight U.S. Treasury market, and the phenomenon of inverted yield curve was temporarily relieved. Historical experience has shown that there has been a clear record of inverted yield curve resolution in the face of economic recession. However, some economists also point out that the predictability of the yield curve for the economy is not ideal.

Temporary relief from inversion.

On September 4, US time, $U.S. 2-Year Treasury Notes Yield (US2Y.BD)$ it fell 9 basis points to 3.7683%, $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ only fell 6 basis points to 3.7684%.

This reflects the market's increased expectation that the Federal Reserve will cut interest rates by at least 25 basis points on September 18, and some predict a maximum cut of 50 basis points. The reason for this situation is that the latest data shows that the number of job vacancies in the United States in July reached the lowest level since early 2021, and the number of layoffs has also increased, leading to a sharp movement in yield curve.

This reflects the market's increased expectation that the Federal Reserve will cut interest rates by at least 25 basis points on September 18, and some predict a maximum cut of 50 basis points. The reason for this situation is that the latest data shows that the number of job vacancies in the United States in July reached the lowest level since early 2021, and the number of layoffs has also increased, leading to a sharp movement in yield curve.

"The labor market is no longer cooling down to the temperature before the epidemic, but has already cooled down to the temperature before the epidemic," said Nick Bunker, Director of Economic Research at Indeed Hiring Lab. "No one, certainly not the policy makers of the Federal Reserve, should hope that the labor market becomes cooler at this point.

Along with the sharp movement of U.S. bond yields, the U.S. stock market also shows signs of lack of confidence. On that day, the three major U.S. stock indexes all showed a tendency to rise and then fall. As of the close, $S&P 500 Index (.SPX.US)$ fell 0.16% to close.

Is it the curse of the U.S. economy?

The yield spread between 10-year and 2-year U.S. Treasury notes has been inverted since early 2022, for a full two and a half years, which is a long enough time and ranks second in U.S. history. Therefore, it has also attracted considerable attention from all sides.

In the history of the United States, there have been five instances where the bond yield curve inverted was resolved, and four of them experienced severe economic recessions. It is worth noting that during the inversion period, the U.S. economy still performed well in the above four instances, and the real severe recession occurred after the inversion was resolved. Therefore, the return to normal of the inversion instead implies a curse of economic recession in the U.S.

However, there are also authoritative figures among the optimists. For example, the chief global interest rate strategist at Goldman Sachs has stated that the yield curve may steepen a bit because concerns about tail risks have at least diminished and economic growth momentum is strong.

Zhou Hao, an overseas macroeconomic researcher at GTJA, also believes that from the perspective of monetary policy response, inflation is starting to rise, and the market is concerned that the economy may experience a hard landing, so the yield curve will invert. However, as inflation stabilizes, the yield curve will gradually smooth out and the inversion will gradually disappear, indicating that market concerns about economic recession are significantly reduced.

Zhou Hao further pointed out that what the market may be more concerned about is whether the yield curve can predict the economy. Based on past experience, the yield curve's predictability of the economy is not ideal. If investor confidence in the yield curve is to be rebuilt, a new validation process will surely be needed.

It will take time for the yield curve inversion to truly be resolved.

With the looming rate cuts by the Federal Reserve, the spread between 2-year and 10-year Treasury yields has continued to narrow and recently approached disappearance. However, it should be noted that a complete normalization and maintenance of Treasury yields may still take time.

The Federal Reserve's interest rate decision at the meeting on September 17-18 is the most critical determining factor. Interest rate swap prices indicate that traders expect a 100% probability of a 25 basis point rate cut this month, with a probability of more than 30% for a 50 basis point rate cut.

In addition, market safe-haven demand and factors related to government bond supply also affect the changes in short-term and long-term bond yields.

Michael Brown, Senior Research Strategist at Pepperstone, said in a report that US bonds may continue their rally on Tuesday. He said that the increase on Tuesday was led by long-term bonds but may be somewhat restrained by a large number of new corporate bond issuances. "Although the demand for safe-haven may continue this rally, if this demand persists in the coming trading days, then when the market begins to reprice the prospects of the Federal Reserve towards the hawkish direction, the sell-off of short-term government bonds and a new round of steepening of the yield curve should become a reality." He said that the current market expectations for the Federal Reserve to cut interest rates by 100 basis points before the end of the year are still too optimistic.

Editor/Rocky