Shareholders in HeartCore Enterprises, Inc. (NASDAQ:HTCR) may be thrilled to learn that the covering analyst has just delivered a major upgrade to their near-term forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

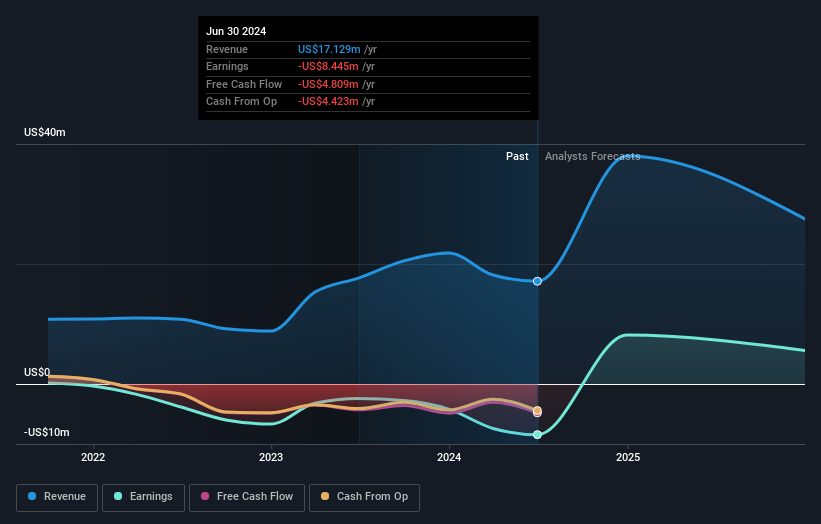

Following the upgrade, the most recent consensus for HeartCore Enterprises from its solo analyst is for revenues of US$38m in 2024 which, if met, would be a huge 122% increase on its sales over the past 12 months. Prior to the latest estimates, the analyst was forecasting revenues of US$29m in 2024. It looks like there's been a clear increase in optimism around HeartCore Enterprises, given the sizeable gain to revenue forecasts.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the HeartCore Enterprises' past performance and to peers in the same industry. It's clear from the latest estimates that HeartCore Enterprises' rate of growth is expected to accelerate meaningfully, with the forecast 4x annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 29% p.a. over the past three years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 12% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analyst also expect HeartCore Enterprises to grow faster than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that the analyst lifted their revenue estimates for this year. They're also forecasting more rapid revenue growth than the wider market. With a serious upgrade to expectations, it might be time to take another look at HeartCore Enterprises.

The most important thing to take away from this upgrade is that the analyst lifted their revenue estimates for this year. They're also forecasting more rapid revenue growth than the wider market. With a serious upgrade to expectations, it might be time to take another look at HeartCore Enterprises.

These earnings upgrades look like a sterling endorsement, but before diving in - you should know that we've spotted 4 potential risks with HeartCore Enterprises, including a short cash runway. For more information, you can click through to our platform to learn more about this and the 2 other risks we've identified .

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.