这些因素中,移民的影响尤其值得关注。短期内,移民流入可能会导致失业率上升,但这种原因引发的失业危害性相对较小。移民也部分解释了近期非农数据的下修,这表明就业市场的疲软程度可能被夸大。中期来看,移民有利于提高经济增长的潜力。CBO计算显示,移民可能使2024-2028年美国实际GDP增速提高0.3个百分点。

这些因素中,移民的影响尤其值得关注。短期内,移民流入可能会导致失业率上升,但这种原因引发的失业危害性相对较小。移民也部分解释了近期非农数据的下修,这表明就业市场的疲软程度可能被夸大。中期来看,移民有利于提高经济增长的潜力。CBO计算显示,移民可能使2024-2028年美国实际GDP增速提高0.3个百分点。Source: China International Capital Corporation Strategy. Author: Wang Hanfeng, Liu Gang et al. After a significant sell-off in the early part of last week, overseas Chinese capital stocks rebounded strongly in the middle of the week. At the beginning of the week, investors' sentiment deteriorated further due to multiple domestic and international factors. Under the pressure of external fund outflows, there was an impact on liquidity in the market and the market performance plummeted. Fortunately, this liquidity shock eased somewhat after policy stabilization signals on Wednesday, and the market subsequently showed an almost linear upward trend. After the roller coaster market last week, we tend to believe that the panic-style rapid sale in the early stage may be temporarily over, and the market may gradually enter a consolidation and bottoming period. However, the recovery of emotions still needs some time, mainly due to: 1) The outflow of overseas funds, especially the reduction of large-scale sovereign funds, is difficult to see a significant reversal in the short term; 2) The short selling ratio in the market is still high; 3) The geopolitical tensions, Sino-US relations, epidemic, domestic policies, and uncertainties in regulation have not yet completely weakened. Therefore, looking ahead, whether the market rebound can continue depends on: 1) Whether positive policy signals can be specifically implemented; 2) Whether external uncertainties will be alleviated.

Authors: Xiao Jie Wen, Zhang Wenlang, etc.

Summary

Since the second quarter of this year, inflation in the United States has slowed down while economic growth remains strong, increasing the possibility of a soft landing. Historically, soft landings have been rare because central banks usually raise interest rates to curb inflation, but raising interest rates often leads to excessive credit tightening and subsequently triggers an economic recession. However, we believe that this time may be different as improvements in the supply side help alleviate inflation without harming the economy, creating favorable conditions for achieving a soft landing.

We have noticed that there are four key supply factors working together: firstly, the recovery of supply chains has reduced the price pressures of tradable goods. Secondly, China has exported relatively inexpensive physical resources to the United States, reducing import costs. Thirdly, increased immigration has increased labor supply, easing labor shortages and wage pressures. Fourthly, improvements in labor productivity have reduced unit labor costs, alleviating the pressure on companies to raise prices due to rising production costs.

Among these factors, the impact of immigration is particularly noteworthy. In the short term, immigration inflows may lead to an increase in unemployment, but the harmful effects of this have been relatively small. Immigration also partially explains the recent downward revision of non-farm payroll data, indicating that the weakness in the job market may have been exaggerated. In the medium term, immigration contributes to improving the growth potential of the economy. According to CBO calculations, immigration may increase the actual GDP growth rate of the United States by 0.3 percentage points from 2024 to 2028.

Among these factors, the impact of immigration is particularly noteworthy. In the short term, immigration inflows may lead to an increase in unemployment, but the harmful effects of this have been relatively small. Immigration also partially explains the recent downward revision of non-farm payroll data, indicating that the weakness in the job market may have been exaggerated. In the medium term, immigration contributes to improving the growth potential of the economy. According to CBO calculations, immigration may increase the actual GDP growth rate of the United States by 0.3 percentage points from 2024 to 2028.

What kind of monetary policy is needed for a soft landing? Historically, a soft landing has usually been accompanied by a rate cut by the Federal Reserve, as timely policy adjustments help avoid excessive tightening. Federal Reserve Chairman Powell has already hinted at a rate cut in September, but the future path of rate cuts remains uncertain. One perspective is to determine the endpoint of rate cuts based on the level of the neutral real interest rate (r*), but the neutral rate cannot be directly observed and predictions vary widely, making it difficult to come to accurate conclusions. Another perspective is to look at Keynes' liquidity preference, where the low risk premium in stocks and credit markets suggests that monetary policy may not need to be significantly eased. Therefore, we expect the Federal Reserve to adopt a gradual rate cut, and there may even be pauses in the process. However, the Federal Reserve will also flexibly adjust based on economic data and may raise the pace of rate cuts if necessary.

Finally, a soft landing is not without risks. Reversals in supply improvements, energy price increases due to geopolitical conflicts, and the lagging effects of monetary tightening could all pose threats to a soft landing. Job losses and asset price increases caused by artificial intelligence could also present risks. We need to remain vigilant about these factors.

Main text

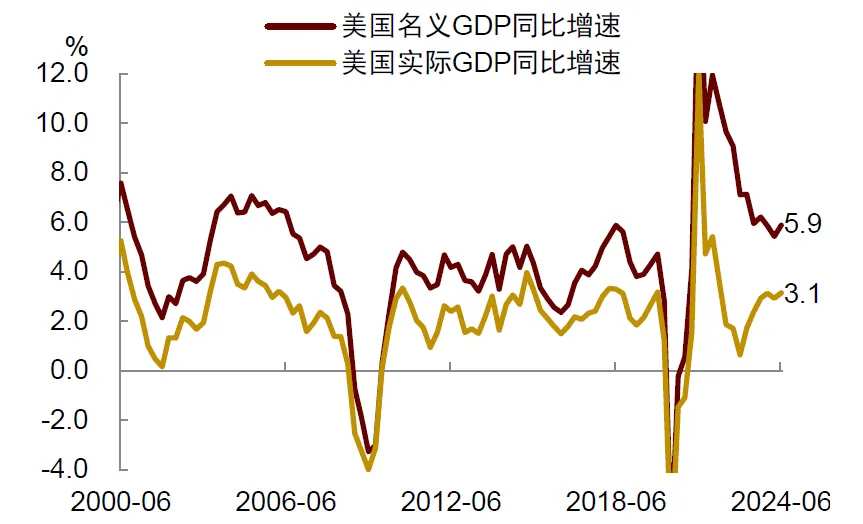

In August 2022, Federal Reserve Chairman Powell stated at the Jackson Hole meeting that high interest rates will reduce inflation, but they will also bring some pain [1]. This statement shows that at that time, the Federal Reserve was prepared for an economic downturn in order to contain inflation. However, two years have passed and the recession has not arrived. The U.S. economy is still strong, with a year-on-year growth rate of real GDP of 3.1% in the second quarter of 2024 (Chart 1). Meanwhile, inflation has continued to slow down, with CPI year-on-year growth rate dropping from a peak of 9.1% in 2022 to the current 2.9%, and core CPI excluding energy and food has decreased to around 3% (Chart 2).

The recent performance of the U.S. economy has raised expectations for a soft landing. A soft landing refers to the ability of the economy to maintain stable growth and successfully avoid a recession after a period of monetary policy tightening. In history, soft landings are not common because central banks often raise interest rates to contain inflation, but this often leads to excessive credit tightening, which in turn leads to a recession. From 1960 to 2020, the Federal Reserve has carried out a total of 11 interest rate hikes, of which only 3 have achieved a soft landing, while the other 8 have resulted in a recession. Will this time be an exception? Can the Federal Reserve achieve a soft landing? This may be one of the most concerned topics in the capital markets currently.

Improved supply is conducive to a soft landing.

History has shown that achieving a soft landing is not enough to rely solely on monetary policy, there must be external forces to assist. As former Chairman of the Federal Reserve Janet Yellen said, sometimes even luck is needed. Among these external factors, supply factors are particularly important because only supply expansion can reduce inflationary pressures and help maintain economic growth (supply creates demand). We believe that there are four supply factors currently helping the United States achieve a soft landing:

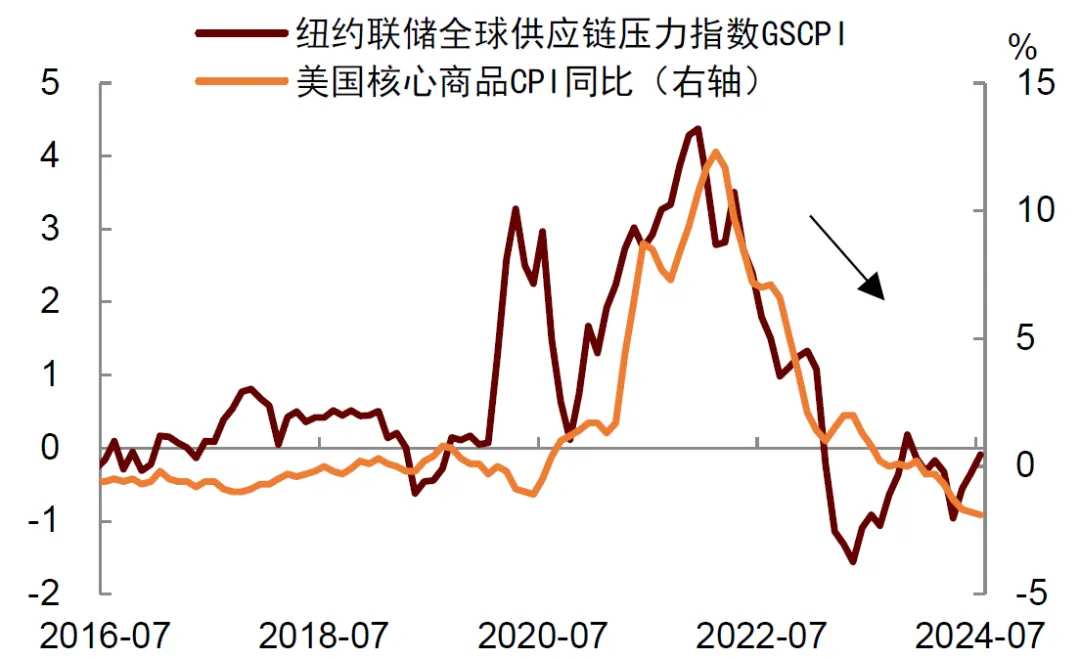

Firstly, the improvement of the supply chain has reduced price pressures on tradable goods. During the COVID-19 pandemic, the disruption of global supply chains had a significant impact on production and resulted in shortages of goods, leading to higher prices. As the pandemic is gradually brought under control, global supply chains are gradually returning to normal, which has a positive effect on reducing inflation. From U.S. inflation data, we can see that over the past two years, the price index of goods excluding energy and food (core commodity prices) has been declining. The decline in these prices lags behind the decline in supply chain pressures, indicating that they are the result of supply chain improvements (Chart 3).

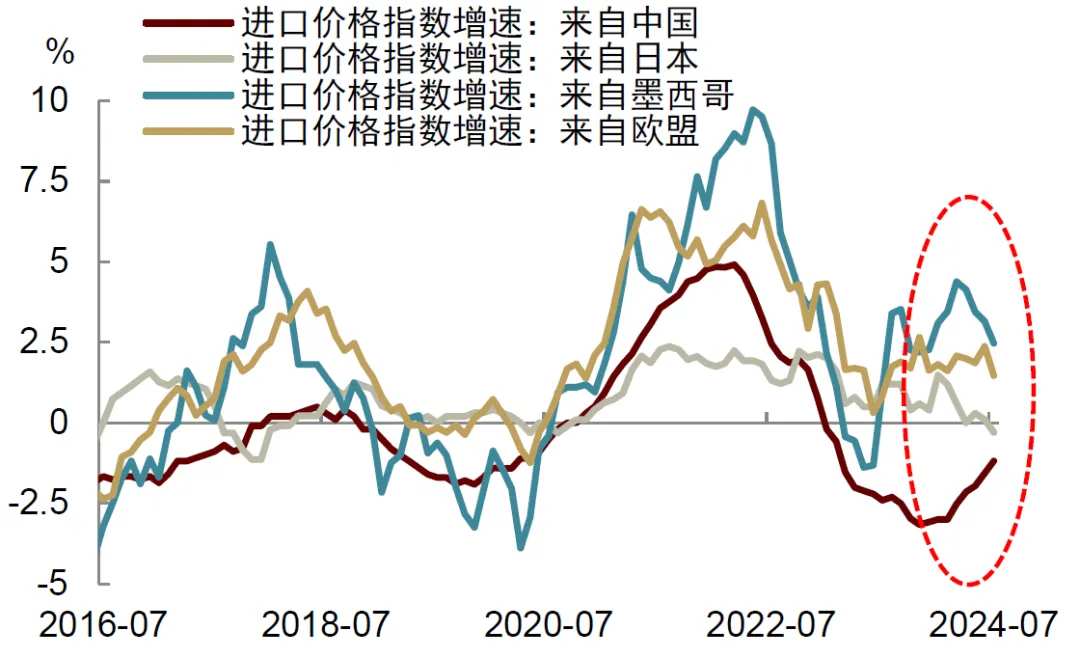

Secondly, China has exported relatively cheap tangible resources to the United States. The United States is the world's largest importer, and import prices have a significant impact on inflation. Among the goods imported by the United States, the price index of imports from China has declined year-on-year, while the prices of imports from other trading partners have risen (Chart 4). This contrast highlights the competitive advantage of Chinese products in terms of price (partly due to the scale effect of Chinese industries), and also indicates that low-cost exports from China have helped the United States control inflation.

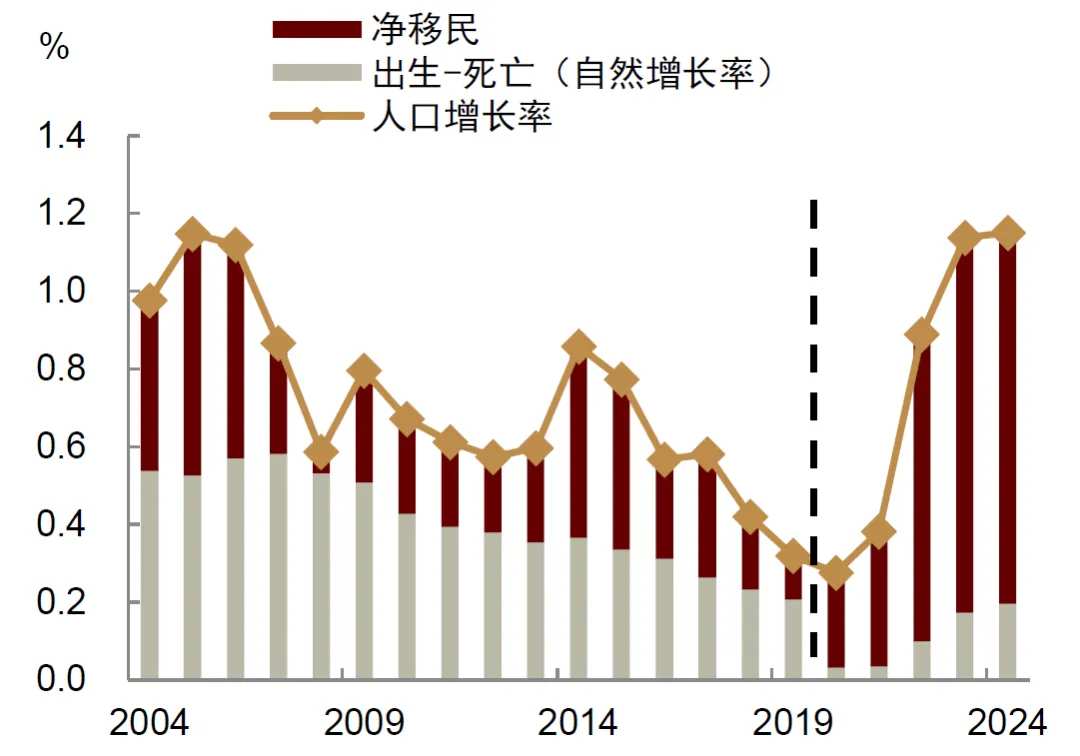

Thirdly, immigration inflows have eased labor shortages. In the early stages of the pandemic, a large number of labor forces exited the market, leading to recruitment difficulties for companies and increased wage pressures. With the recovery of the pandemic, workers began to return to the market, and at the same time, a large number of immigrants have entered the United States, further promoting the recovery of labor supply. According to the Congressional Budget Office (CBO) estimates, from 2022 to 2024, the net increase in immigrants to the United States will reach 2.2 million, 3.3 million, and 3.3 million, respectively, significantly higher than the pre-pandemic average of 0.9 million per year (Chart 5). Immigration inflows have eased labor pressure for companies and helped curb rapid wage increases, thereby alleviating inflationary pressures.

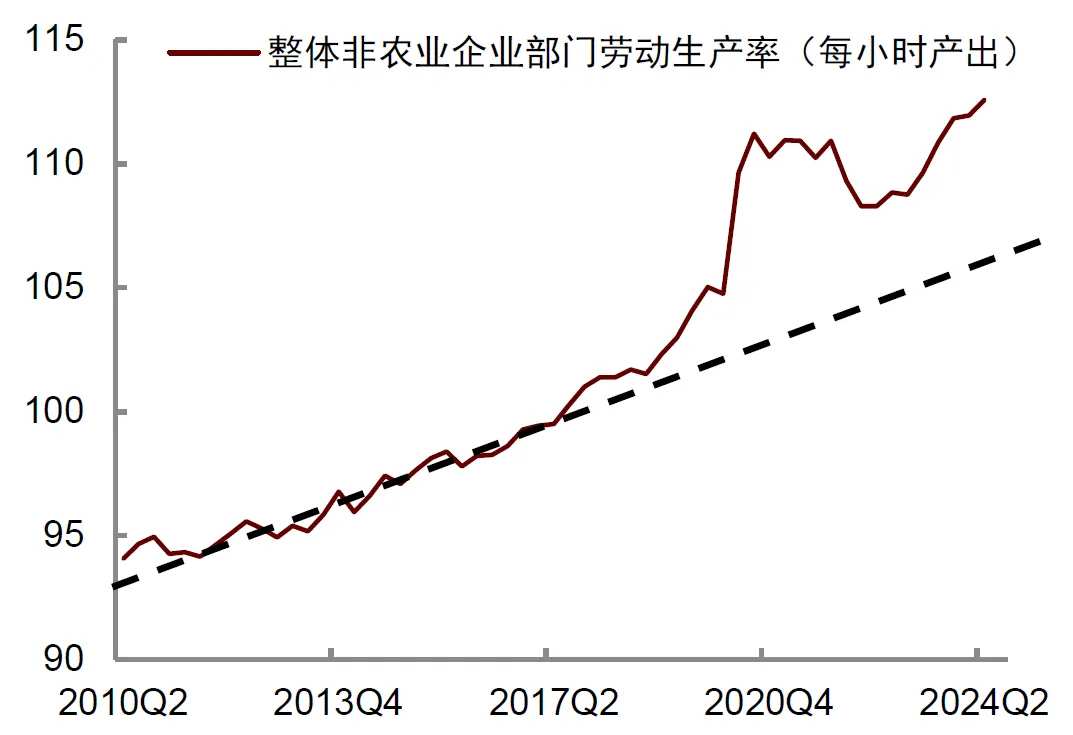

Fourthly, the improvement in productivity has reduced unit labor costs. There are signs that labor productivity in the United States has maintained a growth trend higher than before the pandemic (Chart 6). One explanation is that with the popularity of remote work, companies have increased investment in digitization and automation, thereby improving production efficiency. Another explanation is that the post-pandemic labor market has achieved optimization in labor matching and resource allocation efficiency. There is also a view that the rapid development of artificial intelligence has improved productivity, but this view is also controversial. In the long run, the improvement in productivity supports economic growth and can reduce unit labor costs, which is beneficial for a soft landing.

The impact of immigration may be underestimated

Among the four supply factors mentioned above, the impact of immigration inflows on the economy is particularly worth noting.

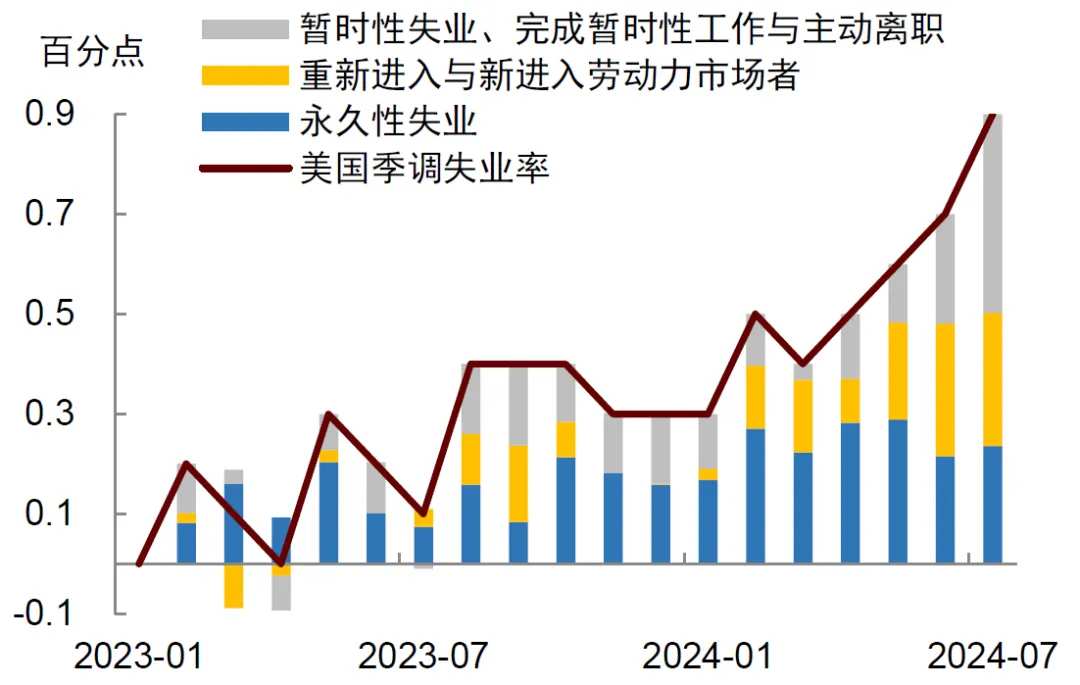

In the short term, immigration inflows may push up the unemployment rate, but the harm caused by this reason is relatively small. In the past year, the US unemployment rate has continued to rise, from a low of 3.4% in April 2023 to 4.3% in July 2024, an accumulated increase of nearly one percentage point. This change has raised concerns in the market, as historical experience suggests that when the three-month average unemployment rate rebounds by more than 0.5 percentage point from the bottom, the economy often faces the risk of recession (this experience is also known as the 'Samuelson rule').

After conducting in-depth research on the reasons for the rise in US unemployment rate, we found that the number of permanent unemployment caused by corporate layoffs did not increase significantly in the past year. The real cause of the higher unemployment rate is the re-entry of labor force and unemployment caused by temporary factors (Chart 7). This indicates that the increase in labor supply is an important factor causing unemployment. Compared to layoffs by companies, the harm caused by this kind of unemployment is relatively small, because it does not lead to a significant decrease in workers' income, resulting in a contraction in consumer spending and economic activity. On the contrary, immigration inflows may also promote consumption growth, support real estate demand, and bring support to total demand.

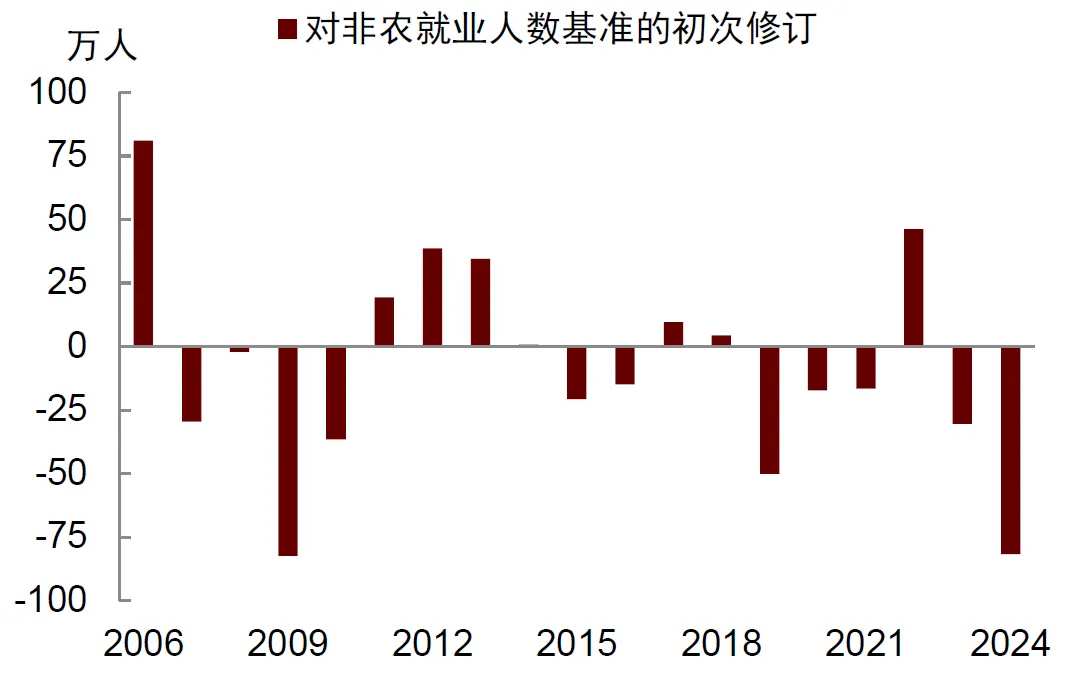

Immigration inflows may also result in an underestimation of non-farm employment. Two weeks ago, the US Department of Labor released the Quarterly Census of Employment and Wages (QCEW) report for the first quarter of 2024 and revised the non-farm employment figures from March 2023 to March 2024 based on this report. The revised data reduced the number of employment reported in the initial report by 0.818 million people, the largest downward revision since 2009 (Chart 8). However, the QCEW survey may underestimate the employment brought by illegal immigrants. This is because 90% of the data in the QCEW survey comes from state unemployment insurance databases, which are usually paid by employers and generally only cover legal employees and do not include illegal immigrants. This means that those illegally employed immigrants will not appear in the QCEW survey, which may result in the adjusted employment figures underestimating the actual employment.

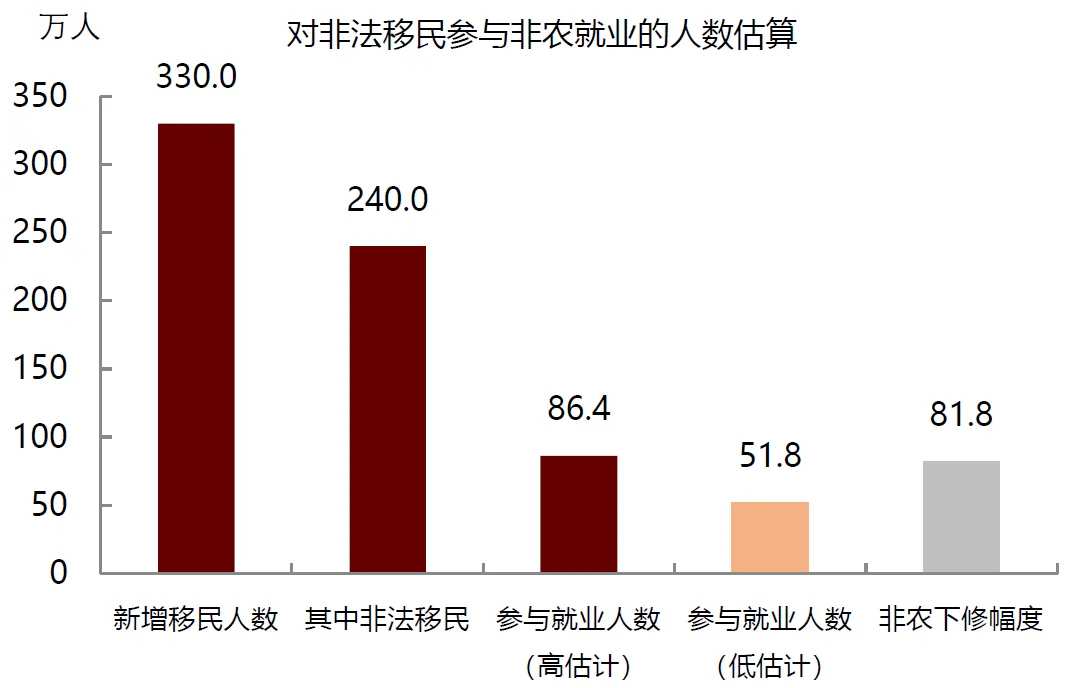

We can make a simple calculation based on CBO data. The net increase in immigration in the United States in 2023 is approximately 3.3 million, of which the number of illegal immigrants is approximately 2.4 million. Assuming that 80% of these people are labor force aged 16-65, and assuming that half of these people are employed (i.e. an employment rate of 50%), and among the employed population, 10% work in the agricultural sector and the remaining 90% work in the non-agricultural sector, it is estimated that the number of people participating in non-farm employment is approximately 0.864 million. If we assume an employment rate of only 30%, the corresponding number of non-farm employment would be approximately 0.518 million, which is roughly equivalent to the magnitude of the downward revision by the Department of Labor (Chart 9). However, it should be noted that under normal circumstances, the employment rate of the population aged 25-54 in the United States is as high as 80%, and the employment rate of the entire population aged 16 and above is 60%. Therefore, our assumption for the employment rate of illegal immigrants is relatively generous.

Of course, the downward revision of non-farm data by the Department of Labor is not entirely due to immigration. Normally, the Department of Labor adjusts the "birth-death model" of companies every year, which leads to the correction of employment figures. However, due to the larger number of immigrants entering since 2022, it is not ruled out that the magnitude of data revision may be greater than in the past, thereby exaggerating the degree of weak employment.

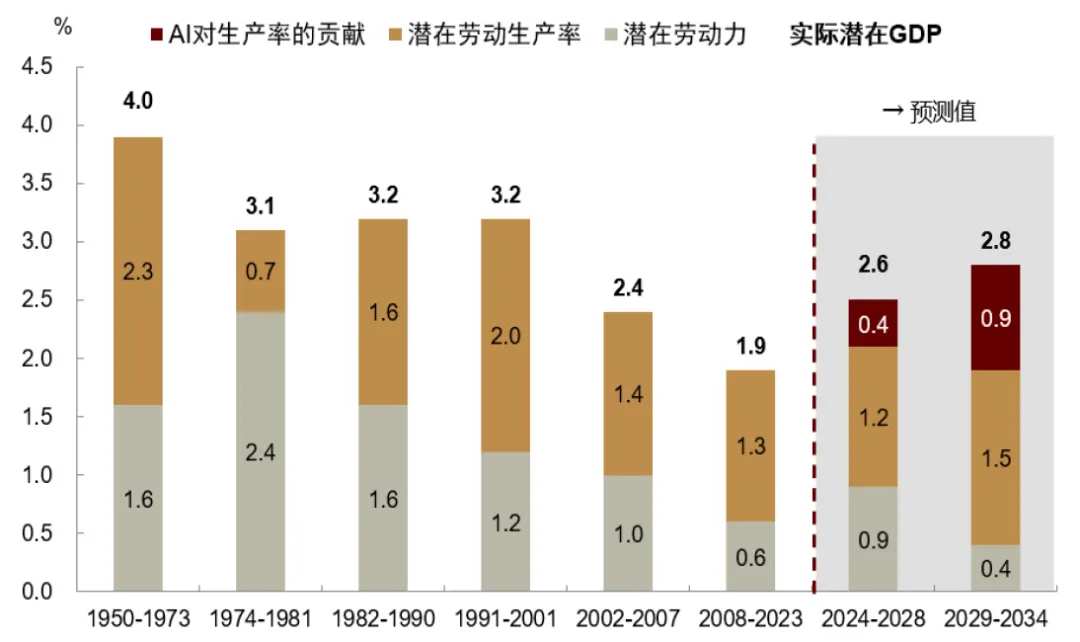

In the medium to long term, immigration is beneficial to population growth and helps to improve the potential economic growth rate. Population is a scarce resource in the future, and the population growth rates of major economies have been declining in the past decade. After 2010, with the retirement of the "baby boomer" generation, the growth rate of the US labor force population has slowed down. Inflows of immigrants can help change this trend and may boost the long-term potential economic growth rate of the United States. According to CBO estimates, immigration could push up actual GDP growth in the United States by 0.3 percentage points from 2024 to 2028. Under an optimistic scenario, considering the efficiency improvement brought by artificial intelligence, the potential GDP growth rate of the United States could increase from 1.9% during 2008-2023 to 2.6% during 2024-2028, and is expected to further increase to 2.8% during 2029-2034 (Chart 10).

Monetary policy under a soft landing

Historically, a soft landing is usually accompanied by a Fed interest rate cut, as timely adjustment of monetary policy helps avoid excessive tightening. With inflation easing and the job market slowing down, the Fed has also started preparing for interest rate cuts. At the Jackson Hole meeting in August 2024, Fed Chair Powell explicitly stated, 'The time has come for policy to adjust,' indicating that rate cuts would begin in September. However, the real question for the market is what the future rate-cutting path will be like? How big will the rate cuts be? Powell did not provide guidance in his speech, which adds to the uncertainty of US monetary policy.

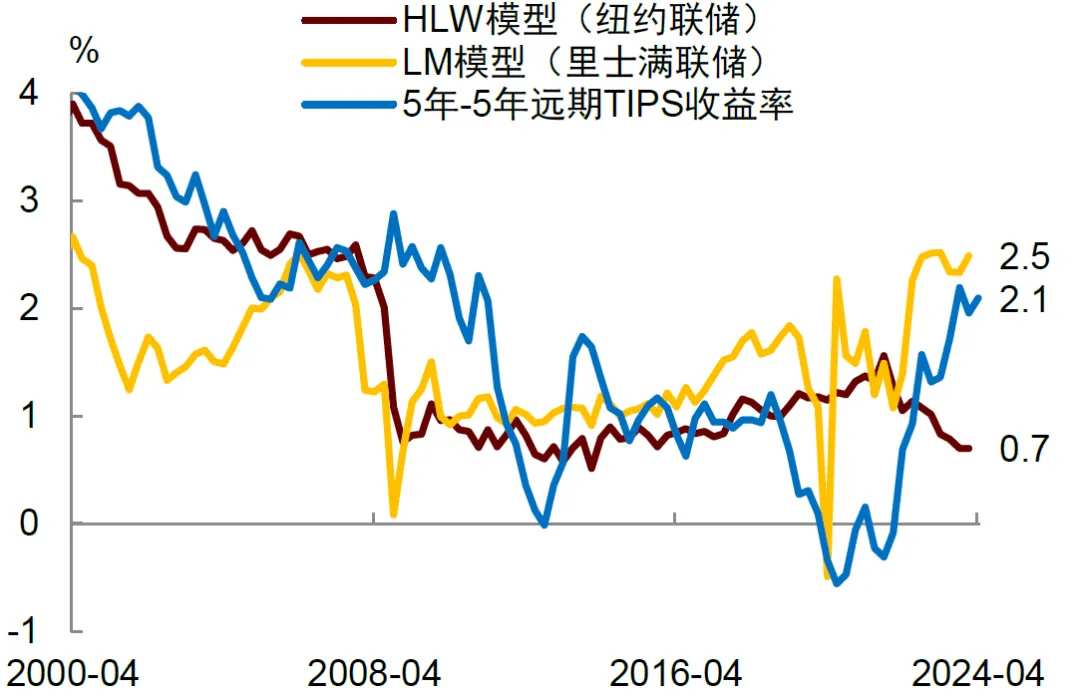

How to determine future monetary policy? We can look at it from two perspectives. One is from the perspective of neoclassical economics, which considers the real neutral interest rate (r*) as the 'reference system' for monetary policy. This perspective emphasizes the concept of equilibrium interest rate, where the real interest rate is determined by the forces of investment and savings. When investment is greater than savings, interest rates rise; conversely, interest rates fall. In the long run, after market adjustment, investment and savings tend to balance, and the corresponding equilibrium interest rate is the real neutral interest rate. Policymakers need to assess the level of the neutral interest rate, and then evaluate whether the current rate is higher (representing a tight monetary condition) or lower (representing an accommodative condition) than that level, and whether the policy rate needs to be reduced or increased.

However, the actual level of neutral interest rates cannot be observed, and policymakers often make judgments based on some statistical models and market price feedback. The two most commonly used models for estimating r* by the Fed are the HLW model of the New York Fed and the LM model of the Richmond Fed. In terms of market prices, a commonly used indicator is the 5-year-5-year forward TIPS yield. Currently, the actual neutral interest rates predicted by these models or prices differ greatly, ranging from 0.7% to 2.5% (Chart 11). On this basis, if it is assumed that long-term inflation expectations are around 2.7% [6], the corresponding nominal neutral interest rates range from 3.4% to 5.2% (Chart 12).

What does this mean for monetary policy? Since the current upper limit of the Fed's policy interest rate is 5.5%, this means that if the Fed wants to lower the interest rate to the neutral level, the conservative reduction is 30 basis points, and the aggressive reduction is 210 basis points, a significant difference. In other words, due to the unobservability of the neutral interest rate, policymakers now have great difficulty in determining the magnitude of future interest rate cuts based on it.

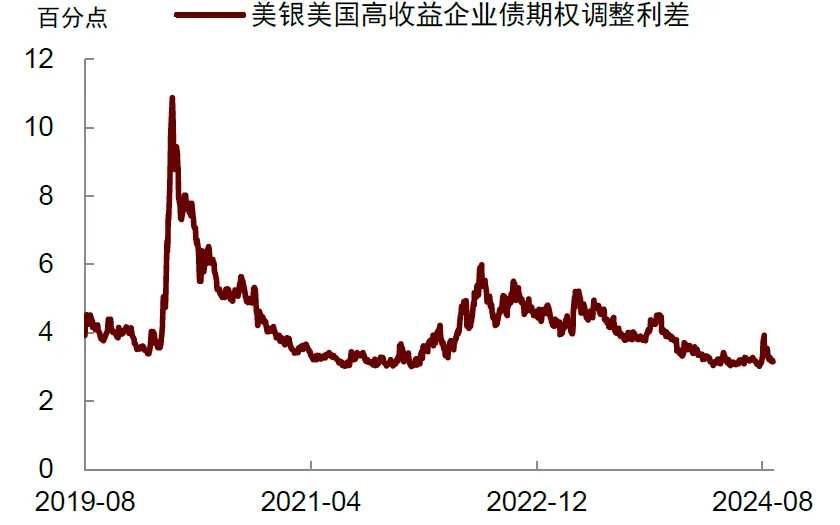

Another perspective is Keynes's liquidity preference theory. The theory emphasizes people's asset allocation behavior. When the money supply is sufficient and the interest rate level is low enough, people's demand for safe assets decreases, while their demand for risky assets increases. The latter includes stocks, real estate, physical investments, and even alternative investments like bitcoin. In other words, one criterion for judging whether monetary policy is tight is whether it has stirred people's speculative behavior and whether it has depressed the premium of risky assets relative to safe assets.

From this perspective, the risk premium on U.S. stocks is still very low (Chart 13), and the credit spread of U.S. corporate bonds (i.e. the corporate credit premium) is also at a low level (Chart 14), which indicates that people have not felt that monetary policy is very tight when allocating assets. In addition, with the rapid development of artificial intelligence, capital expenditures of the 'magnificent 7' tech giants in the USA have reached new heights [7]. Companies are increasing capital investment even at such high interest rates, indicating that the traditional transmission mechanism of monetary policy may be weaker than imagined.

Taking into account the two perspectives mentioned above, we tend to believe that the Federal Reserve will adopt a gradual approach when cutting interest rates. If the interest rate is cut too quickly and by too large an amount, it could lead to excessively loose monetary policy and the risk of inflation rising again. Our base case is that the Federal Reserve will cut interest rates by 25 basis points in September and another 25 basis points in December. If the economic data performs even worse, the Federal Reserve could take a larger cut during one of the rate cuts, such as a 50 basis point cut. However, if the economic data remains strong, the Federal Reserve could adopt a more cautious approach, pausing after cutting interest rates one or two times and observe before deciding on the next course of action.

Risks Facing a Soft Landing

The US economy is not without risks, and future risks can be roughly divided into three categories: supply-side, demand-side, and structural. From the supply-side perspective, if the supply improvement assumption mentioned earlier were to be reversed, a soft landing would face challenges. In fact, many US economic recessions in history have been accompanied by negative supply shocks, with the most typical being the "Great Stagflation" of the 1970s. Currently, there are also some supply factors with a high degree of uncertainty. For example, under the intensification of geopolitical conflicts, there may be upward risks to energy and commodity prices. The efficiency of global supply chains is declining in the era of deglobalization. Opposition to illegal immigration by the public and the approaching elections have prompted the Biden administration to restrict immigration. Excessive government intervention in the economy has led to a contraction in private sector supply. Most of these factors cannot be resolved through monetary policy adjustments and may pose a threat to a soft landing.

From the demand-side perspective, monetary tightening has a long and variable lag effect, which may put pressure on consumption and investment. Since the second quarter of this year, new housing starts and sales in the United States have slowed down, the delinquency rate on consumer credit cards has risen, and workers' expectations for future employment have weakened. At the same time, manufacturing PMI continues to weaken, and small and medium-sized enterprises lack confidence. These phenomena indicate that some interest rate-sensitive sectors have already been negatively affected by high interest rates. However, compared to supply-side shocks, a slowdown in demand seems more manageable because the Federal Reserve currently has ample policy space to deal with the downside risks to demand. The current policy rate of the Federal Reserve is over 5%, theoretically allowing for a cut of over 500 basis points. With the experience of 2008 and 2020, the Federal Reserve can also expand its balance sheet at any time to cope with any financial liquidity risks.

From the perspective of structural risks, it is necessary to pay attention to the impact of the development of artificial intelligence and asset prices on the short-term fluctuations of the economy. Technological progress often has a "creative destruction" function, which means that it brings impacts to traditional industries in the process of creating new value. Since the rapid development of artificial intelligence, some cognitive white-collar jobs have been at risk of being replaced, including entry-level translators, administrative clerks, programmers, and advertising models. This structural change can lead to job losses in some industries, wage declines for workers, and negative impacts on consumer confidence.

On the other hand, technological progress often accompanies asset price bubbles. Once the bubble bursts, it may lead to a shrinkage of residents' wealth effect, a weakening of corporate investment enthusiasm, and a decline in consumer spending and corporate investment. After the bursting of the technology internet bubble in 2000, the US stock market plummeted, and the economy subsequently entered a recession. Although the degree of that recession was relatively mild, it also resulted in an increase in the unemployment rate from 3.9% in 2000 to 6.3% in 2003. In response to the recession, the Federal Reserve lowered the policy interest rate from 6.5% to 1%.

In summary, with the slowdown in US inflation and strong economic growth, the possibility of a soft landing is increasing. However, supply-side, demand-side, and structural risks still exist, and these factors may disrupt the expectation of a soft landing. We need to keep an eye on these risks.

Editor/Rocky