2023年12月12日,

2023年12月12日,Source: MEGA WAVE

Author: Hou Tian

Since the end of last year, top sports brands have started to buy back their own stocks, and the scale is quite large.

On December 12, 2023,$LI NING (02331.HK)$the company announced a share buyback plan to repurchase 10% of the shares with a capital of no more than 3 billion Hong Kong dollars, expected to be completed within six months.

On December 12, 2023,$LI NING (02331.HK)$the company announced a share buyback plan to repurchase 10% of the shares with a capital of no more than 3 billion Hong Kong dollars, expected to be completed within six months.

In November of the same year, $Lululemon Athletica (LULU.US)$ The board of directors also approved a share buyback plan, planning to repurchase up to $1 billion of the company's common stock, and announced an additional $1 billion common stock buyback on May 29, 2024.

ANTA is the latest to take action. On August 27, 2024, ANTA announced a buyback on the Hong Kong Stock Exchange, with a planned use of not more than HKD 10 billion. According to the disclosure,$ANTA SPORTS (02020.HK)$The board of directors obtained authorization at the shareholders' annual meeting on May 8, 2024, allowing it to repurchase up to 10% of the total issued shares.

In recent years, the stock prices and performance of leading sports brands have been disappointing, while the management's performance has been generally strong - investing in cash reserves and carrying out large-scale share buybacks.

Large-scale share buybacks are not a random occurrence or impulsive decision. In addition to judging the fluctuations of the industry cycle, it is more about the firm belief in its brand barriers: top sports brands have maintained a high concentration and stable competitive pattern over the years with their strong R&D capabilities and brand barriers. This gives operators the confidence and courage to conduct 'countercyclical regulation' in the capital market.

Performance

Top sports brands have faced performance declines in recent years.

Compared with the previous peak, the stock prices of many leading sports brands have already dropped by nearly half. As of August 31, 2024, $LI NING (02331.HK)$ stock prices have fallen by 85% compared to their historical high in 2021. $ANTA SPORTS (02020.HK)$ has fallen by 58%, $Lululemon Athletica (LULU.US)$ has fallen by 52%.

The significant drop in stock prices is not only affected by market conditions, but also directly related to their performance.

From 2022 to the first half of 2024, the performance of sports brands has generally experienced varying degrees of decline. Li Ning's annual performance declined by 21.6% last year, and in the first half of 2024, its performance further declined by 8.0% compared to the previous year. Anta's performance in 2022 slightly declined by 1.7%, and although it has since recovered to positive growth, the growth rate is not as high as that of 2018 to 2019.

Starting from 2022, the North American brand Lululemon experienced a slowdown in revenue growth. In 2021, Lululemon's revenue growth reached 42%, but by 2022, this number dropped to 30%, and further dropped to 19% in 2023. In the first half of 2024, the revenue growth rate further declined to 8.6%. Especially in its headquarters in North America, the revenue growth rate is less than 1%.

In recent years, the performance of sports brands has been disappointing due to weak market demand. For example, Adidas and other well-known sports brands also experienced single-digit revenue growth in the first half of 2024. Except for Anta, the growth rates of most brands are lower than the GDP growth rate during the same period.$Nike (NKE.US)$and$adidas AG (ADDYY.US)$

The high inventory pressure of brand manufacturers is gradually being passed on to sales channels, and dealers are starting to offer more discounts and promotions to reduce inventory. This will also have an impact on the growth of brand manufacturers' channel sales.

Comparatively, Li Ning's inventory turnover days increased by 5 days to 63 days last year, and the inventory amount increased by 2.7% compared to 2022. 361's inventory turnover days increased by 2 days to 93 days, and the inventory amount increased by 14.4% compared to 2022.

The high inventory pressure of brand manufacturers is gradually being passed on to sales channels, and dealers are starting to offer more discounts and promotions to reduce inventory. This will also have an impact on the growth of brand manufacturers' channel sales.

In 2022, sports brands were confident in the future prospects of the sports industry and expanded against the trend, betting on post-epidemic recovery. However, from the current situation, the post-epidemic consumption recovery fell short of expectations, and domestic sports brands have also experienced weak performance growth. The aftermath of this situation has continued to the present and has had a profound impact on the industry.

Repair

Sports brands have basically passed the period of high inventory pressure.

In the first half of 2024, although most brands' revenue growth is still in single digits, the industry's fundamentals have likely started to improve based on inventory and discount conditions.

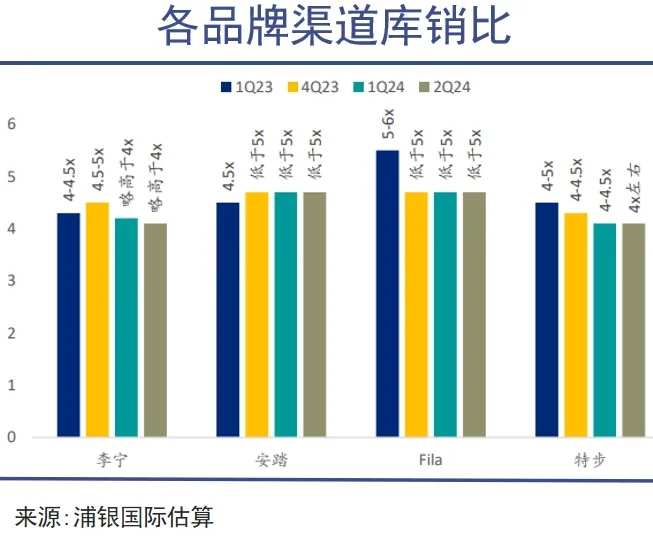

By the first half of 2024, the inventory-to-sales ratio of most Chinese sportswear players has remained stable or declined compared to the end of 2023. This means that the industry has basically passed the period of high inventory pressure. With the relief of inventory pressure, retail prices at the terminal have also stabilized.

In the first half of 2024, the terminal retail discounts of major players did not deepen significantly compared to the previous year but instead showed slight improvement.

In a weak demand environment, although the top sports brands have implemented certain discount strategies, most brands still pay more attention to the stability of discounts and the health of channel inventory. This has kept the profit margins of top brands relatively stable. For example, Anta's operating profit margin in the first half of 2024 was 21.8%.$XTEP INT'L (01368.HK)$ANTA Sports increased by 0.8%, Lululemon increased by 0.2%, and Nike increased by 0.6% compared to the same period last year, with growth rates of 10.4%, 15.6%, and 10.4%, respectively.

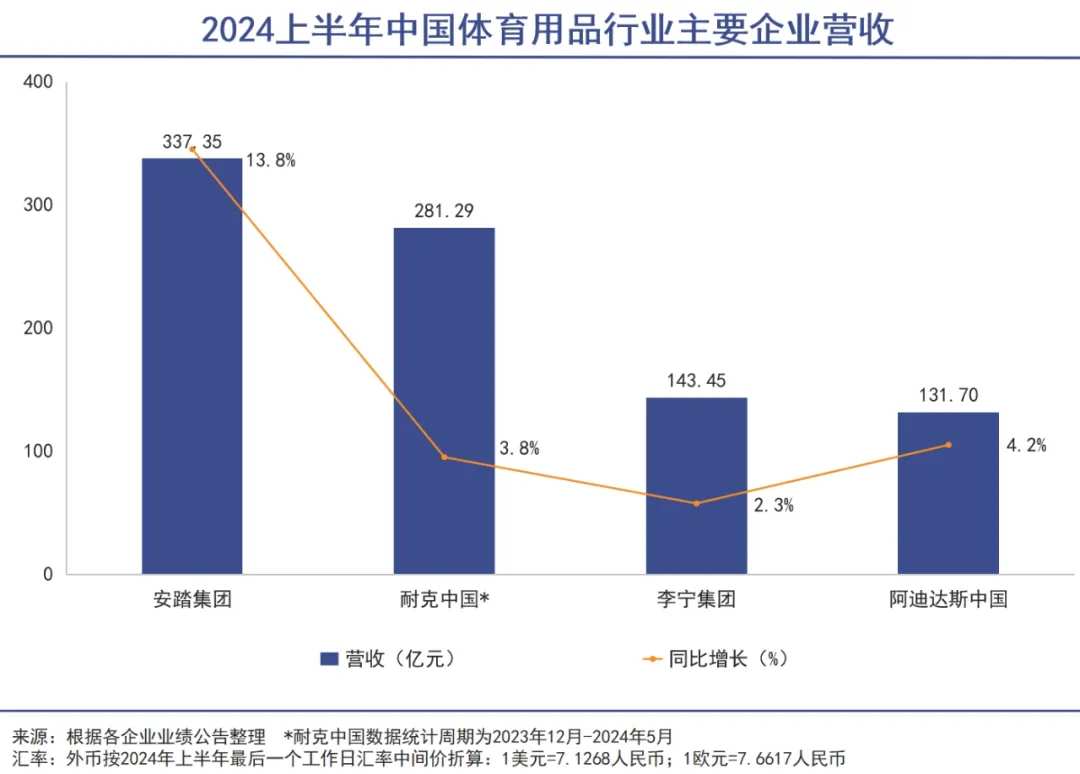

Among them, ANTA had the most obvious performance, with its revenue increasing by 13.8% to 33.74 billion yuan in the first half of the year, reaching a new half-year historical high, and its net income attributable to shareholders also achieved a high growth rate of 63%. At the same time, ANTA's profitability, operational efficiency, cash flow generation, and inventory management are all maintained at healthy levels.

On the other hand, although the sportswear market is facing temporary soft demand, it still has broad growth potential in the long run. Residents' health awareness continues to rise, and the participation in sports and outdoor activities is very high, and the corresponding willingness to consume is also growing.

Survey data shows that 82.76% of consumers have purchased sportswear in the past year, which is much higher than other sports-related products.

According to Euromonitor's forecast, China's sportswear market is expected to maintain a high compound growth rate of 7.7% during the period of 2023-2028, which exceeds most consumer industries such as personal accessories, beauty, and home appliances.

In addition, due to the high functional requirements of sportswear and the increasing ability of people to evaluate and determine functionality, leading companies with outstanding product capabilities will perform better in the market.

When sports brands such as ANTA, Li Ning, and Lululemon announced their share repurchase plans, their stock prices generally fell by more than 30% from their historical peak, and the price-to-earnings ratio (PE TTM) also dropped to a low level close to the historical 20th percentile. These companies obviously believe that the market valuation is already low enough and provides a higher margin of safety.

ANTA, Li Ning, and Lululemon's repurchase amounts reached 10 billion Hong Kong dollars, 3 billion Hong Kong dollars, and 2 billion US dollars, respectively. Among them, ANTA also increased its dividend payout ratio to 50.1% in the first half of 2024, an increase of 4.4% compared to the same period last year.

Barrier

Powerful supply chain system and deep brand moat.

Behind the large-scale buyback is the firm determination of sports brands on their own barriers.

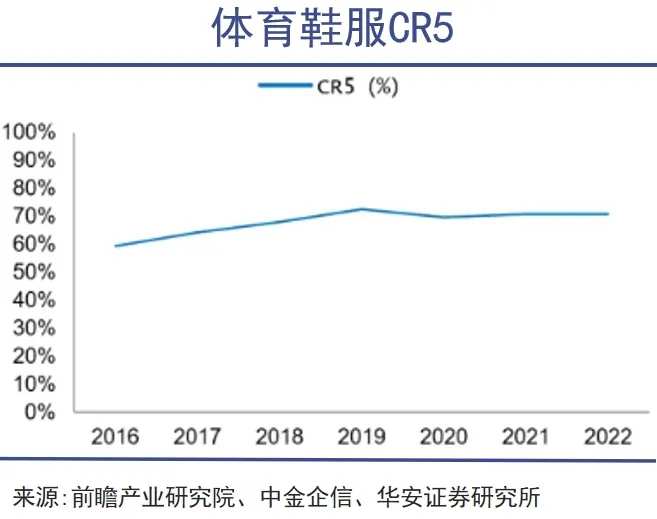

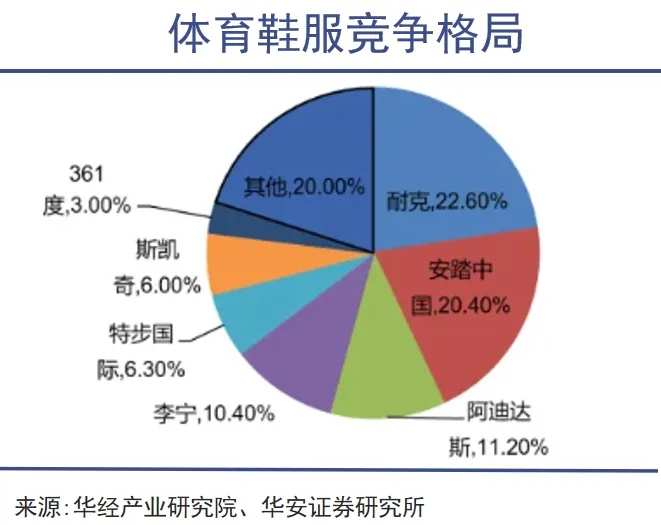

For a long time, the competitive pattern of sports brands has been relatively stable. Although there are constantly emerging competitors in the industry, the market still maintains a situation of double super and multiple strongs. In 2022, the CR5 of sports shoes and clothing is close to 70%, far higher than the 10.4% level of the traditional footwear and clothing industry, and the market share of Nike and Anta alone has reached 50%.

The reason why sports brands can maintain such a stable market position and high concentration is largely due to their strong brand moat.

Top sports brands have a long history of development. For example, Li Ning and Anta were established in 1990 and 1991 respectively, while Nike was established in 1972. Through long-term accumulation, these brands have built enough trust and reputation among consumers. Consumers believe that these brands represent high quality, reliability, and value, which is also an advantage that other competitors find difficult to replicate. $Nike (NKE.US)$

Headbrands continue to enhance their brand image through hiring spokespersons, product development, and channel reform. This is a significant and long-term investment cost that companies with insufficient capital strength find difficult to cope with.

For example, in 2023, Anta signed and appointed NBA star Kyrie Irving as the brand ambassador and chief creative officer for the company's basketball products, creating the Irving signature product line to enhance the brand's global recognition and gradually expand into the global market.

In addition, Anta has also collaborated with Donghua University to develop the "Anta Film" and create an outdoor product line, developed the "Tandeng" weightlifting shoes for the national weightlifting team, and developed the "PG7" shock-absorbing sole for entry-level shock-absorbing running shoes. These products generally emphasize technological content, which ultimately contributes to the enhancement of brand strength.

In terms of channels, headbrands are also constantly reforming. For example, Anta has broken the traditional "one-size-fits-all" model and, based on different segments of consumer groups, has divided its stores into five levels: Arena, Hall, Elite, Standard, and Basic. The goal is to enhance the store's image and enter higher-level commercial areas, which undoubtedly has a positive impact on brand image enhancement.

Overall, the strong capital of sports brands and the brand barriers formed by multiple investments make the stickiness between sports brands and consumers much stronger than that of ordinary footwear and apparel brands, and consumers are more willing to pay a premium for them.

In addition to brand moats, a strong supply chain system is also a barrier for sports brands. No matter how good the brand concept or design innovation is, it cannot be separated from the production process. High-quality and cost-effective suppliers and contract factories are important support for the long-term success of sports brands.

Top companies usually establish long-term cooperative relationships with core suppliers and contract factories. On the one hand, by cooperating with top companies, large suppliers and contract factories do not need to accept orders from other brands and can operate at full capacity to achieve high profits. On the other hand, some cooperative relationships are exclusive, meaning that the production lines and workshops of large suppliers and contract factories are specifically tailored for certain big brands.

For example, when Nike launched the Flyknit Racer knitted running shoes in 2012, Shenzhou International specifically purchased expensive new equipment for Nike and built new factories and design studios, making it difficult for small factories to make the same investment. Faced with the dominance of top companies over manufacturing resources, other second or third-tier brands, or new brands, have already fallen behind from the production and manufacturing process.

As core suppliers and outsourced factories in the top-tier enterprise supply chain system, they themselves have the characteristics of high barriers, high concentration, and high profit margins. These barriers are reflected in many aspects such as scale, research and development, quality control, production, and delivery time. Some factories also have strong technical capabilities and new product development capabilities, which can quickly respond to orders from top brands and provide innovative support at the production level, forming synergy with the brands, and more conducive to the development and expansion of the brands.

The above mentioned negative factors have collectively led to the low possibility of new brands achieving surpassing even in the face of industry downturn in the short term. The insurmountable industry barriers are exactly the confidence behind large-scale share buybacks by Anta, Li Ning, Lululemon, and Nike.

Editor/Rocky