In the first half of the year, the macroeconomy continued to recover, but the business operations of enterprises have not fully recovered yet due to the low prosperity of coal and oil & gas equipment. As a leading company in the domestic mining equipment and logistics equipment industry, sany int'l has shown a relatively stable operating side by actively strengthening its business capabilities and exploring new market opportunities.

On August 28, sany int'l released the mid-year performance for 2024. The financial report shows that the revenue reached 10.8 billion yuan in the first half of the year, with a net income attributable to shareholders of 1.03 billion yuan.

Through this financial report, the author will analyze the underlying logic that drives the future growth of sany int'l.

1) The mining equipment sector is still on the left side of the industry cycle bottom.

1) The mining equipment sector is still on the left side of the industry cycle bottom.

From the financial data, it can be seen that the mining equipment revenue is slightly lower compared to the same period last year, mainly due to the decrease in coal production in the first half of the year and insufficient demand for new equipment investments.

In the first half of the year, the total industrial raw coal output was 2.27 billion tons, a year-on-year decrease of 1.7%. The clean and efficient utilization of coal-fired power and ultra-low emission levels have significantly improved. However, the impact of the coal price drop in the first half of the year and the consequent decline in performance has become a common phenomenon in the coal industry, with demand being suppressed. From January to June, the cumulative total profits of the national-scale coal mining and washing industry decreased by 24.8% year-on-year.

From a long-term perspective, coal, as the main energy source in China, plays a visible role as a "ballast" and "stabilizer" in ensuring long-term energy supply. In policy terms, it is necessary to maintain the "upward elastic production" of coal, proposing to form around 0.3 billion tons/year of adjustable production capacity reserves by 2030 to meet the peak coal demand. This will drive technological innovation and promote industrial upgrading, leading to new demands for next-generation equipment such as intelligent tunneling complete sets of equipment and fully mechanized mining systems. As a leader in the coal machinery industry, sany int'l is expected to enjoy more development opportunities in the industry, thereby improving its competitiveness and profitability in the industry.

This will drive technological innovation and promote industrial upgrading, leading to new demands for next-generation equipment such as intelligent tunneling complete sets of equipment and fully mechanized mining systems. As a leader in the coal machinery industry, sany int'l is expected to enjoy more development opportunities in the industry, thereby improving its competitiveness and profitability in the industry.

The financial report shows that the gross margin of Sany Int'l's mining equipment business increased by 2.4 percentage points year-on-year to 28.6%, with different levels of growth in product market share, such as tunneling machines, which increased by 1.4 percentage points to 63.6%. Combining with industry trends, it can be speculated that gross margin and market share are expected to continue to remain stable.

The latest research report from Minmetals Securities points out that in the current mining enterprise capital expenditure cycle from 2017 to present, due to inadequate exploitable projects, it is difficult to have substantial growth in the future, but sustainability is expected to exceed expectations.

Another research report indicates that mining machinery sales are closely aligned with capital expenditures. Thirteen years ago, rapid expansion of mining enterprise capital expenditures led to an overdrawn subsequent demand phenomenon, resulting in a downturn in mining machinery sales from 2014 to 2016. Considering the typical 8-10 year lifespan of mining machinery, the previously purchased machinery during the rapid expansion phase of mining enterprises has reached its lifespan, initiating a new cycle of equipment updates.

It is not difficult to speculate that in the long term, the mining equipment business will be a solid foundation for Sany Int'l.

2) The logistics equipment sector maintains strong growth momentum.

The financial report for the first half of 2024 shows that the revenue of the logistics equipment business reached 3.6 billion yuan, a year-on-year increase of 17%, with a net income attributable to shareholders of 0.53 billion yuan, a 24% increase year-on-year. The growth of the logistics equipment sector is strong, with profit growth outpacing revenue growth, reflecting the economies of scale and leading product advantages of Sany Int'l's logistics equipment business, further improving the quality of earnings.

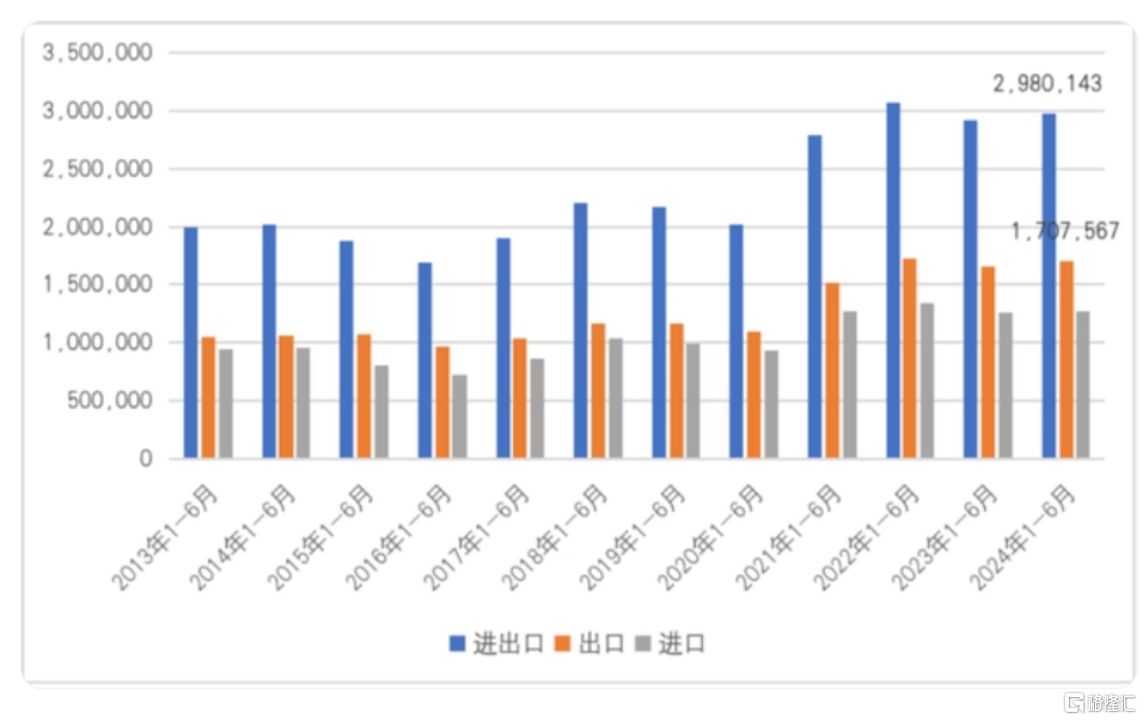

Currently, the future growth trend of the logistics equipment business appears to be quite clear. This year, global economic moderate recovery has driven trade growth, with China's foreign trade situation exceeding expectations. In the first half of the year, national ports completed a cargo throughput of 8.56 billion tons, a 4.6% increase year-on-year. As an embodiment of new quality production capacity, the digitalization, intelligence, and green transformation of port shipping industry have become the general trend. The prosperity of port logistics equipment supports the rising prosperity and solid growth foundation of Sany Int'l's logistics equipment sector.

(Image: China's foreign trade growth from January to June 2013 to January to June 2024, unit: million US dollars)

At present, Sany International is leading the industry in the positive crane/stacker market share, both exceeding 70%, and has formed a dual-driven strategy of large stackers and small stackers. In the first half of the year, the overseas income included 1.7 billion yuan from small stackers, a year-on-year increase of 25.2%; and 0.55 billion yuan from large stackers, a year-on-year increase of 54.4%.

Based on its leading layout time and intensity in the small stacker field, Sany International has a complete research, development, manufacturing, and production system, with high competitive barriers. In the future, Sany International is expected to maintain its position as a leader in the small stacker sector. In the large stacker field, with continued efforts in smartization, electrification, and internationalization, performance is expected to maintain high growth.

According to Sany International, the large stacker has orders in hand exceeding 5 billion yuan, and with the improvement of delivery capacity in the second half of the year, it strives to deliver 2.5 billion yuan for the whole year. In addition, it aims to deliver more than 3.5 billion yuan in 2025.

4) China's high-tech manufacturing going global, focusing on the broad growth space of its main business.

Since the beginning of this year, the global demand for high-tech products and applications has continued to grow, and China's high-end 'smart' manufacturing, representing high-tech and high value-added products, is steadily integrating into the global value chain, with great growth potential.

Sany International has developed strong market competitiveness and, with its flagship products, cost advantages, and technological innovation, has continuously achieved success in multiple regions such as Asia-Pacific, North Asia, and Africa, opening up the overseas market.

In the first half of the year, Sany International's overseas income from the mining equipment business was 1.56 billion yuan, a year-on-year increase of 5.8%; and the overseas income from the logistics equipment business was 2.25 billion yuan, a year-on-year increase of 27.3%, maintaining steady growth and continuously leading the industry's development direction with popular products.

Through the output of advanced technology and the high-profit assistance of overseas products, Sany International is fully enjoying the development opportunities of the overseas market and obtaining more new increments. Under the trend of electrification, Sany International is now accelerating its transformation into a provider of intelligent green equipment and solutions, with broad space for imagination.

It is worth noting that this year Sany International is more focused on its core business and has disposed of the loss-making robot business, realizing a disposal income of 22.74 million yuan, thus optimizing the company's business structure and resource allocation, demonstrating its determination to improve its operational capability and quality and ensure returns for shareholders and investors.

In addition, in the second half of the year, Sany International acquired Sany Lithium, completing the puzzle of the source, network, load, and storage industry. It is expected that the entire market size will reach 800 billion yuan in 2024, and in the next three years, it will reach 1.5 trillion yuan. At present, Sany Lithium has already achieved profitability and its potential is beginning to emerge. With the full listing of the entire series of mature products by the end of this year, the performance of Sany Lithium is expected to reach a higher level.

In the context of global acceleration of carbon neutrality, Sany International, with its perfect "source, network, load, and storage" solution, will be able to serve global companies in exploring new energy businesses and establish more technological and industrial cooperation. Therefore, Sany International's globalization and low-carbon process will be further accelerated, and after expanding its influence globally, it will also usher in better development.

Summary

From the perspective of value investors, we may continue to have higher expectations for Sany International. Looking back from 2019 to 2023, Sany International's revenue increased from 5.656 billion yuan to 20.278 billion yuan, with a compound annual growth rate (CAGR) as high as 37.6%. The return on equity (ROE), which measures the profitability of the enterprise, increased from 13.42% in 2019 to 17.04% in 2023, achieving a year-on-year improvement.

Nowadays, Sany International has a solid performance foundation and its market position is further consolidated. It focuses on its core business to expand its business boundaries, thereby achieving sustained revenue growth in the future. Therefore, regardless of external fluctuations, Sany International has the ability to grow and withstand risks. At present, the trends of electrification, intelligence, and internationalization in the industry are clear, and the development prospects of Sany International are considerable.