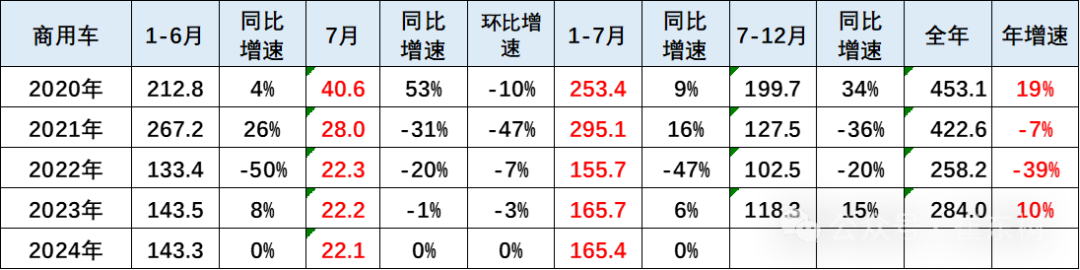

According to the data from the National Financial Supervisory Agency, the domestic insurance for commercial vehicles achieved 1.65 million units in the first seven months, a year-on-year decrease of 0.1%. In July, the domestic insurance for commercial vehicles achieved 0.22 million units, the same as the previous year, and remained steady.

According to the data from the National Financial Supervisory Agency, the domestic insurance for commercial vehicles achieved 1.65 million units in the first seven months, a year-on-year decrease of 0.1%. In July, the domestic insurance for commercial vehicles achieved 0.22 million units, the same as the previous year, and remained steady, on par with June. In July 2024, the penetration rate of new energy commercial vehicles reached 17% in the commercial vehicle market, with a penetration rate of 21% in July, an increase of 8 percentage points compared to the 13% in July of the previous year. The performance of new energy light commercial vehicles and other markets driven by policies was relatively strong. From January to July 2024, the sales volume of new energy commercial vehicles reached 0.275 million units, a year-on-year increase of 107%; in July 2024, it reached 0.047 million units, a year-on-year increase of 65%.

1. Analysis of national compulsory insurance data for the commercial vehicle market.

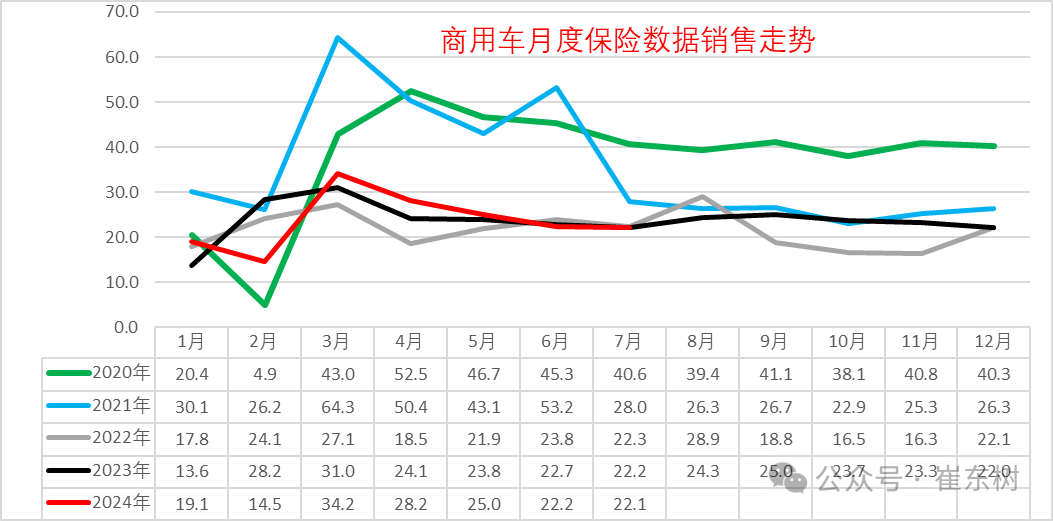

In recent years, the domestic commercial vehicle market has shown a rapid decline in demand. From the peak sales volume in 2020 to the period of policy adjustment in 2021, it entered a low point in 2022-2023. In the first seven months of this year, the domestic insurance for commercial vehicles achieved 1.65 million units, a year-on-year decrease of 0.1%; in July, the domestic sales volume of commercial vehicles reached 0.22 million units, the same as the previous year, and remained steady, on par with June. The year-on-year growth in the first seven months of this year was due to the recovery of the market.

The commercial vehicle market this year has shown a relatively stable trend, similar to the trend in 2021, with greater fluctuations from January to March. Due to abnormal insurance data, the sales volume of commercial vehicles in July this year was 0.22 million units, the same as in June, and the recovery of demand after March was less obvious.

The comprehensive inventory increase from January to December 2023 should reach 0.42 million units, which is a historical high. The remaining inventory of manufacturer sales volume, insurance volume, and export volume from January to July 2024 is 0.223 million units, which has decreased. The inventory increased significantly by 0.0412 million units in June 2024 and decreased by 0.0211 million units in July, indicating sufficient inventory.

2. Analysis of national new energy commercial vehicle market sales.

From January to July 2024, the sales volume of new energy commercial vehicles reached 0.275 million units, a year-on-year increase of 107%; in July 2024, it reached 0.047 million units, a year-on-year increase of 65%, showing a relatively strong performance and a good market growth after continuous subsidy withdrawal.

In 2023, the overall performance of new energy commercial vehicles showed a low position in the first four months due to the impact of subsidy withdrawal, and then demonstrated strong growth from May to December. In January and February 2024, it returned to the normal monthly trend, and the post-holiday opening from March to July also showed a rapid recovery and good growth momentum.

3. Penetration rate of new energy commercial vehicles.

In January to July 2024, the penetration rate of new energy commercial vehicles reached 17%, achieving a good improvement compared to last year.

In July, the penetration rate of new energy reached 21%, an increase of 8 percentage points compared to the 13% in July last year, showing a relatively strong performance.

From 2019 to 2021, the penetration rate of the entire new energy commercial vehicle was around 3%. It reached 9% in 2022, 11% in 2023, and reached a good level of 17% in January to July this year, reflecting the strong growth trend of new energy commercial vehicles.

In 2024, the penetration rate of new energy in trucks was 14%, and 55% in buses, both showing a slight increase compared to the same period. The penetration rate of electric trucks and buses increased significantly, particularly in light trucks and buses.

4. Analysis of changes in the commercial vehicle market.

The truck and bus structure of commercial vehicles is relatively stable. Light trucks performed well, while heavy-duty trucks showed a stronger trend this year after a deep adjustment last year.

The trend of light commercial vehicles in passenger cars is strong, while medium and large-sized commercial vehicles continue to shrink and remain sluggish.

The overall penetration rate of new energy in commercial vehicles is low, and plug-in hybrids have basically no market, while pure electric vehicles perform well. This year, the demand for fuel vehicles in large and medium-sized buses has clearly rebounded and has taken a turn to the return of the fuel vehicle demand after subsidies. The commercial vehicle hydrogen energy relies on subsidies to drive sales. Only the subsidy for large buses is high, but the overall performance of hydrogen energy is average, and the electrification of commercial vehicles performs relatively well.

The overall penetration rate of new energy in commercial vehicles is relatively low, with virtually no market for plug-in hybrids, but pure electric vehicles perform well. This year, the demand for fuel vehicles in medium and large-sized commercial vehicles has obviously rebounded, achieving a return to the era of post-subsidy fuel vehicle.

The sales of commercial vehicles powered by hydrogen energy are driven by subsidies, with only high subsidies for large buses. However, the overall performance of hydrogen energy is average, while the electrification of commercial vehicles performs well.

Commercial vehicle companies are mainly supported by light truck companies. Foton and Wuling are the main force in the light truck and micro-car markets, respectively.

6. Analysis of changes in the commercial vehicle competitive structure.

The commercial vehicle enterprise is mainly supported by light truck enterprises, Foton and Wuling are the main force in the light truck and micro-car market sales, respectively.

Overall, medium and heavy-duty trucks have a higher market share in the central and northwestern regions of the Yellow River area. New energy heavy trucks have performed well in the south and northwest regions, with the penetration rate particularly high in the south, though it has improved somewhat more slowly in the east.

FAW Jiefang, Sinotruk, Dongfeng Automobile, and other companies have shown the best performance in the domestic medium and heavy-duty truck market overall. The performance of heavy-duty trucks overall has been relatively stable, while some second-tier heavy-duty vehicle companies such as XCMG, Sany Heavy Industry, and Yutong have improved their penetration rates for electric vehicles.

8. Regional Market Structure of Light Trucks

The light truck market is mainly strong in the eastern, northern and southwestern regions.

The main market for new energy light trucks is still relatively strong in the eastern and southern markets, with a relatively slight decrease in the market in Beijing-Tianjin-Hebei municipalities overall this year.

The main manufacturers of domestic light trucks are still Beiqi Foton, SAIC-GM Wuling, Jianghuai Automobile, Sinotruk and Dongfeng Automobile, especially recently, Wuling and Changan and other such small light trucks have gradually shown relatively good market performance.

The main companies for new energy light trucks are Geely Auto and Xinyuan Auto, especially Geely Auto has shown extremely outstanding performance in new energy light trucks in the past two years.

9. Regional Market Structure of Light-duty Buses

The main sales areas of the domestic light truck market are mainly the relatively developed southern region. Due to road access restrictions, the sales of fuel light trucks in Beijing-Tianjin-Hebei have decreased, especially in the southern market, where the market for fuel light trucks has rapidly shrunk.

The demand for new energy light commercial vehicles is mainly strong in developed regions, with new energy performance in the southern region being relatively strong.

The main manufacturers of light commercial vehicles are Jiangling Motors Corporation, SAIC-GM-Wuling, SAIC Maxus, Foton Motor, Chongqing Changan Autos, Geely Commercial Vehicle, among others. Among them, Jiangling Motors Corporation maintains an absolute leading position, but the new energy light commercial vehicles of emerging force Geely Commercial Vehicle have performed relatively well. The recent introduction of Wuling's electric light commercial vehicles should be impactful.

10. Regional Market Structure of Large Bus

The market for large and medium-sized commercial vehicles has shown strong performance recently, with overall good performance in the central and western markets.

The regions with high penetration rates of new energy large and medium-sized commercial vehicles are mainly Beijing-Tianjin-Hebei, the southern region, and the middle reaches of the Yangtze River, while performance in other regions is mediocre.

The main manufacturers of large and medium-sized commercial vehicles are still Yutong, King Long, and other enterprises showing relatively outstanding performance, especially in traditional fuel vehicles for Yutong and King Long. Companies like Golden Dragon also have relatively good performance.

The enterprises with high penetration rates of new energy large and medium-sized commercial vehicles are mainly second-tier companies. The main companies are comprehensively developing new energy vehicles while maintaining a good market for traditional fuel vehicles.