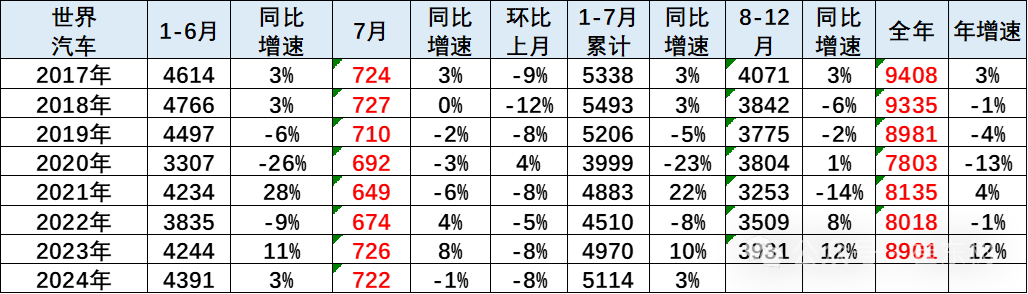

In July 2024, global car sales reached 7.22 million units, a year-on-year decrease of 1%, a decrease of 8% from June.

According to the 36kr app, Cui Dongshu, the secretary general of the China Passenger Car Association, stated that the global automotive sales in July 2024 reached 7.22 million units, a 1% year-on-year decrease, and an 8% decrease from June. In July 2024, it was still slightly lower than the peak in July 2018, at the median level of previous years. Sales from January to July 2024 reached 51.14 million units, a 3% year-on-year increase. In July 2024, Chinese car companies accounted for 31% of the global market.

From a global perspective, the Chinese automotive market showed strong recovery in 2024. Chinese car companies such as BYD (01211), Chery Automobile, Geely Auto (00175), and Chongqing Changan Automobile (000625.SZ) had the most prominent rebound, while the performance of the Asian group represented by Toyota and Kia remained relatively poor. The international chip shortage in the past two years has had a relatively small impact on the Chinese car market and instead has driven strong performance in Chinese car exports, seizing a huge international market supply and demand gap and gaining rare development opportunities. As a highly monopolized industry such as automotive chips, the recent supply-side tightening will bring significant opportunities for the rise of the Chinese supply chain, and the rapid development of new energy in the near term has strengthened the trend of Chinese independent car companies, leading to the gradual decline of some international car companies.

1. Trends in global automotive sales for the month

1. Trends in global automotive sales for the month

In July 2024, global automotive sales reached 7.22 million units, a 1% year-on-year decrease, and an 8% decrease from June. It was still slightly lower than the peak in July 2018, at the median level of previous years. Sales from January to July 2024 reached 51.14 million units, a 3% year-on-year increase.

After declining continuously from 2018 to 2020, the global main auto-producing countries' sales in 2021 were 81.35 million units, a year-on-year increase of 4%, demonstrating good post-pandemic recovery. However, the sales in 2022 were only 80.18 million units, a year-on-year decrease of 1%, barely above the 2020 sales level.

In 2023, the global car sales reached 89.01 million units, a 12% year-on-year increase, still 5% away from the peak level in recent years, and the level of production and sales gap has narrowed. At present, in 2024, the number is 51.14 million, close to 2019, and it is expected to exceed 90 million according to the pace of 2023.

In the first seven months of 2024, the global car market was relatively stable. The increase in sales before the Chinese Spring Festival in January contributed to the global increment. The trend of the global car market was stable from March to May, but weak in June and July.

2. Historical trends in global auto sales

The world auto sales in the above table primarily includes the sales of 70 countries, with sales of around 90 million units, which can generally be tracked monthly. Due to frequent wars, the global data has been slow in recent months.

There are also 100 other countries whose sales data can only be tracked annually, with a total of approximately 3 million units in 2022. Compared to the 80 million units from the 70 major countries, these smaller countries account for only about 3% of the total and have little impact.

Looking at the world sales represented by major countries, the global car sales in 2018 decreased by 1%, the first annual negative growth since 2010. In 2019, car sales were 89.81 million units, a 4% decrease compared to the previous year, slightly better than the decline in 2008; sales declined by 13% in 2020; car sales rebounded by 4% in 2021 compared to the previous year; performance of 1% decline in global sales in 2022 was poor; performance of 11% increase in global sales in 2023 was good; performance of 3% increase in global sales in the first seven months of 2024 was good. In January of this year, the Chinese car market was temporarily strong due to the Spring Festival factor, but there was little growth afterwards, with an overall growth rate of 3%. Therefore, the comprehensive performance of the Chinese car market in the first seven months is still stable with a slight increase.

3. Chinese sales remain in the lead in 2024 The Chinese auto market has an extremely significant impact on the world auto market. From 2016 to 2018, China's auto market accounted for about 30% of the world market, and in 2019, it fell to 29%, still having an absolute advantage. The market share rose to 32% in 2020-2021. In 2022, China's share rose to 33%. In 2023, China's share remained at 34%, and the low at the beginning of the year was a normal reflection of the Spring Festival factor and the withdrawal of the car purchase tax incentive policy. The main reason for the increase in China's share in May 2024 to 32% was the low level in February due to the Spring Festival factor. The North American and European markets have fully rebounded this year, and the trend in the southern hemisphere market is strong.

The Chinese auto market has an enormous influence on the global auto market. From 2016 to 2018, China accounted for around 30% of the world's cars, which dropped to 29% in 2019 but still had an absolute advantage. From 2020 to 2021, the market share rose to 32%. In 2022, China's market share increased to 33%.

In 2023, China's market share remained at 34%, with the lower share at the beginning of the year being a normal reflection of the Spring Festival factor and the withdrawal of the car purchase tax incentive policy. Subsequently, China's market share reached 32% from January to July 2024, mainly due to the low factor of the Spring Festival in February. This year, the market share in Northern Europe has fully recovered, and the trend in the Southern Hemisphere market is strong.

4. Developing countries' markets are significantly strengthening.

Looking at sales volumes from various countries globally, currently the developed markets of Europe and the USA are performing relatively well, with China's automotive market overall showing good trends. Domestic sales in Russia are close to China's export volume, with Chinese automakers holding a high market share in Russia. The Russian market is gradually recovering, leading to high sales volume and profits for Chinese independent automakers.

5. Trends in markets around the world

Since 2020, China's global market share has continued to increase, reaching 33.8% in 2023. In 2024, the Chinese automobile market will experience a low and then high trend, currently around 31.9%.

6. Trends in China's global market share.

In 2023, the global market further differentiated, with China's share gradually recovering. At the beginning of 2023, the withdrawal of preferential policies led to a sharp drop in Chinese car sales, with a share of 29% in January. From February to April, it rebounded to a good level of 32%. From May to July, it rose to 33%, and from August to December, China's share of the world's cars increased to a high of 38%. Therefore, the characteristics of high growth brought by the low base of the early 2024 are evident, and the growth pressure from May to July gradually emerges.

In 2024, China's car market gradually returns to normal, coupled with strong exports, so China's sales share continues to strengthen. In March and April 2024, the Chinese market warmed up, and in May and June, China accounted for 33% of the global market share, which was consistent with previous years. In July, China's car market sales share was 31%, weaker than the global market trend.

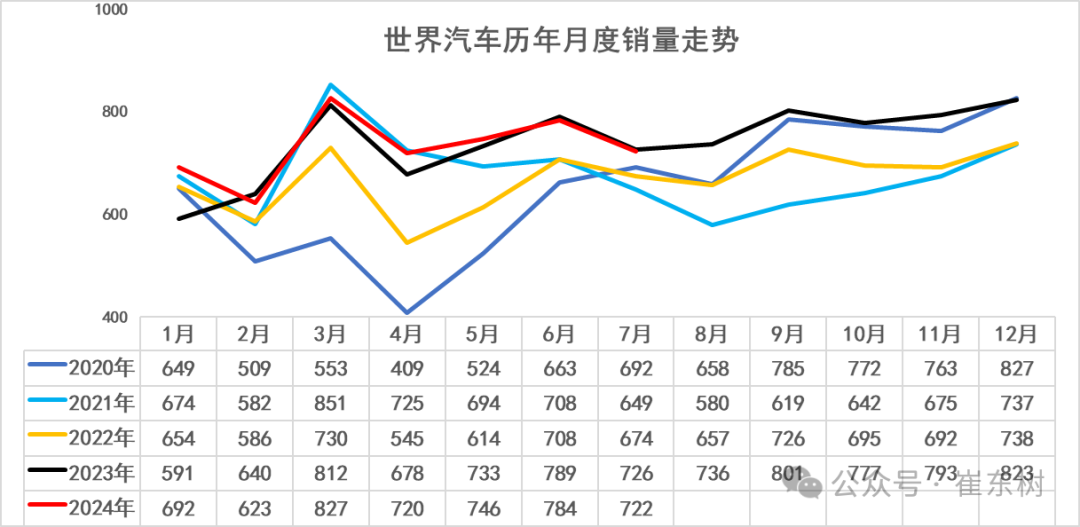

7. Monthly trends in car sales in various countries.

From the monthly sales growth trends of various countries around the world, the trend between months is basically balanced. However, due to seasonal and annual factors, there are still significant differences in trends among countries.

Due to China's automotive market still being in the stage of popularization, it shows relatively strong performance at the beginning and end of the year, with a relatively soft trend in the summer. In contrast, the US automotive market shows relatively weak performance at the beginning of the year and relatively stable characteristics in the middle of the year. However, the spring boost characteristic of the Chinese automotive market this year is not obvious, therefore the market share increase is not significant. With the Federal Reserve raising interest rates, the automotive markets in Europe and the United States are declining, resulting in a more stable trend. The trend of the Japanese automotive market in July of this year is not strong, while the Chinese automotive market at the beginning of 2024 remains relatively strong.

This chart shows the world market share performance of international automotive groups. From the current overall performance of the groups, the market share of top international automotive companies has significantly decreased, while Chinese automotive companies have generally shown strong performance. As the international market positions of China, Russia, and India improve, coupled with the strong market performance of Asian automotive companies such as Geely, BYD, Chery, Changan, and Suzuki, the production and sales trends of Asian automotive companies are positive. European automotive companies generally have poor performance.

This chart shows the world sales share trends of various major automotive groups. From the current overall performance of the groups, the market share of top international automotive companies has significantly decreased, while Chinese automotive companies have generally shown strong performance. As the international market positions of China, Russia, and India improve, coupled with the strong market performance of Asian automotive companies such as Geely, BYD, Chery, Changan, and Suzuki, the production and sales trends of Asian automotive companies are positive. European automotive companies generally have poor performance.

The world market share of Chinese domestic brands has been significantly increasing. BYD, Chery, Changan, Geely, and other domestic brands have shown relatively strong performance.

The world share of international automotive groups is comprehensive. The market share of top international automotive companies has significantly decreased, while Chinese automotive companies have generally shown strong performance. As the international market positions of China, Russia, and India improve, coupled with the strong market performance of Asian automotive companies such as Geely, BYD, Chery, Changan, and Suzuki, the production and sales trends of Asian automotive companies are positive. European automotive companies generally have poor performance.

In addition to the Indian factors such as Hyundai, Suzuki, and Tata, the market share of other international brands has declined across the board. Toyota Group has performed relatively well, with a decrease of 0.2 percentage points compared to 2019. By 2024, its global market share has reached around 11%, but the North American market has performed strongly overall.

Volkswagen's performance is relatively weak, with a decrease of 1.9% in market share compared to 2019. It faces significant pressure in the Chinese market. The overall improvement in Volkswagen Group's other global markets is significant, with a noticeable recovery in the Southern Hemisphere market.

Hyundai Motor's trend is relatively stable, remaining unchanged compared to 2019. By 2024, its global market share will be around 7.6%. It performs well in other markets in Asia, but its performance in China has been consistently weak due to its weak product competitiveness.

Suzuki's market performance is strong, mainly due to its strong performance in markets such as Japan. Honda Group has also performed poorly this year, with a decline of 1.6% compared to 2019, and its performance in the Chinese market is relatively weak.

Mercedes-Benz and BMW Group from Germany have performed steadily. The pressure in the traditional luxury car market in China has increased, and luxury car demand has shifted towards domestically produced high-end vehicles due to changes in consumer demand.