The Beng Kuang Marine Limited (SGX:BEZ) share price has softened a substantial 25% over the previous 30 days, handing back much of the gains the stock has made lately. Of course, over the longer-term many would still wish they owned shares as the stock's price has soared 238% in the last twelve months.

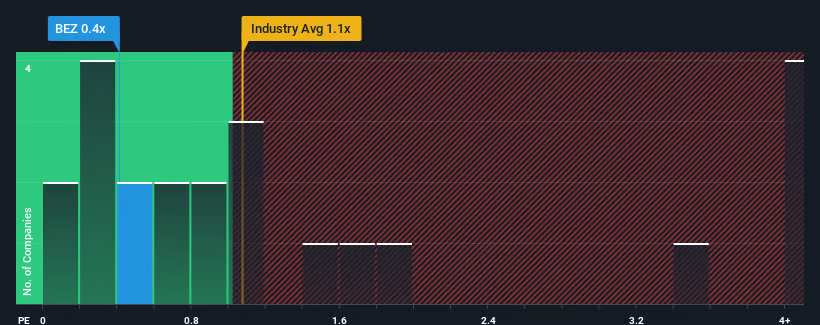

Even after such a large drop in price, it's still not a stretch to say that Beng Kuang Marine's price-to-sales (or "P/S") ratio of 0.4x right now seems quite "middle-of-the-road" compared to the Commercial Services industry in Singapore, where the median P/S ratio is around 0.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

How Beng Kuang Marine Has Been Performing

Recent times have been advantageous for Beng Kuang Marine as its revenues have been rising faster than most other companies. It might be that many expect the strong revenue performance to wane, which has kept the P/S ratio from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Want the full picture on analyst estimates for the company? Then our free report on Beng Kuang Marine will help you uncover what's on the horizon.How Is Beng Kuang Marine's Revenue Growth Trending?

In order to justify its P/S ratio, Beng Kuang Marine would need to produce growth that's similar to the industry.

In order to justify its P/S ratio, Beng Kuang Marine would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered an exceptional 73% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 119% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the lone analyst covering the company suggest revenue should grow by 14% over the next year. Meanwhile, the rest of the industry is forecast to expand by 13%, which is not materially different.

In light of this, it's understandable that Beng Kuang Marine's P/S sits in line with the majority of other companies. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Bottom Line On Beng Kuang Marine's P/S

Beng Kuang Marine's plummeting stock price has brought its P/S back to a similar region as the rest of the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

A Beng Kuang Marine's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Commercial Services industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Beng Kuang Marine (1 doesn't sit too well with us!) that you should be aware of before investing here.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.