Metals Focus released its latest Precious Metals Weekly Report, stating that it is expected that the net gold purchases by global official sectors will slightly slow down in the second half of 2024, with a total net purchase of about 800 tons for the year. Although the pace of gold purchases is slowing down, the total net purchase for 2024 is still expected to be 57% higher than the annual average value during the period of 2010-2019, an increase of about 300 tons. More importantly, it should not be forgotten that the gold market has been in a structurally oversupplied state in recent years, so the large-scale gold purchases by official sectors to some extent helps alleviate the burden on investors who have already absorbed the oversupply in the gold market.

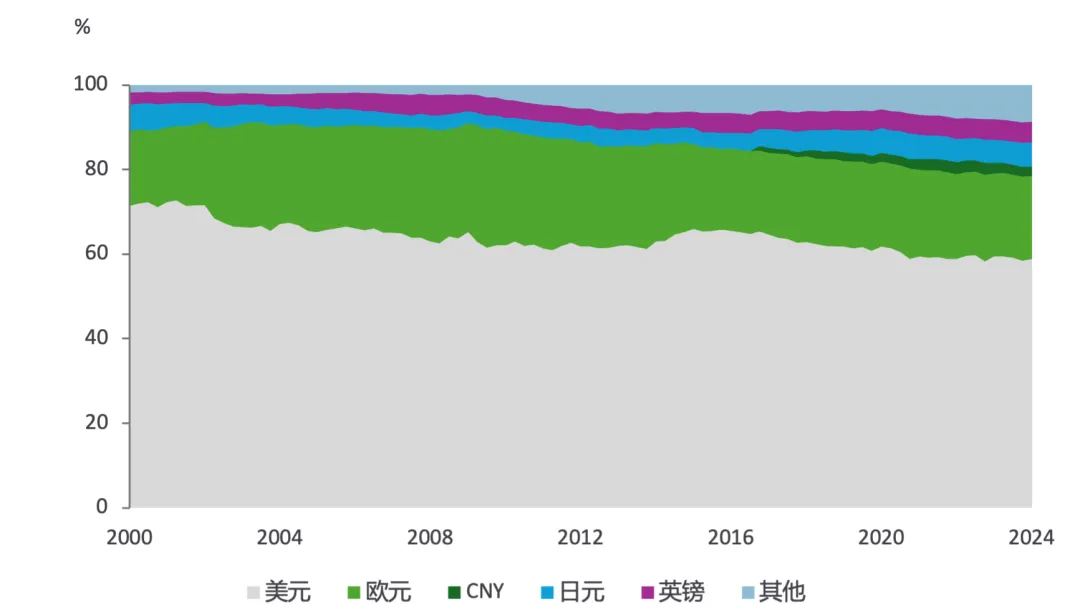

Currency composition of official forex reserves

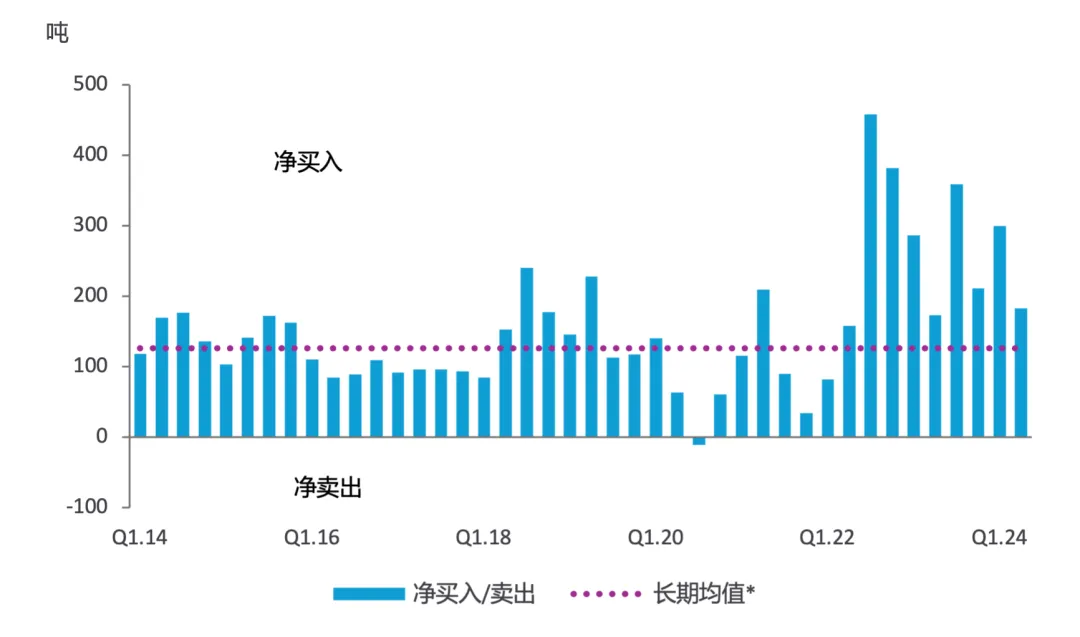

Metals Focus pointed out that the aggressive interest rate hikes during the period of 2022-2023 led to a decline in professional investors' interest in gold, but the gold purchases by global official sectors surged, providing necessary support for the gold price from time to time. After reaching a new high of 1,082 tons in 2022, the net gold purchases by global official sectors remained strong in 2023, exceeding 1,000 tons for the second consecutive year. The demand from global central banks in 2022 and 2023 accounted for more than 20% of the global annual gold demand, a significant increase compared to the approximately 10% during the period of 2010-2019.

Although official sectors remain the main buyers of gold this year, their buying pace has slowed in recent months. According to Metals Focus estimation, the net gold purchases by global official sectors in the second quarter of this year was 183 tons, a 39% decrease compared to the first quarter. Although the pace of buying has slowed down, the net gold purchases in the second quarter is still at a historical high in absolute quantity (44% higher than the quarterly average during the period of 2010-2019). In fact, due to a significant increase in net purchases in the first quarter, the net gold purchases by global official sectors in the first half of 2024 exceeded 480 tons, setting a new record for net purchases in the first half of the year, and ranking as the third highest value in Metals Focus data series starting from 2010 (only surpassed by the second half of 2022 and the second half of 2023).

Among the countries that have reported buying gold this year, the countries that have been active buyers in the past few years remain the main buyers. Among these, the two largest buying countries, Turkey and India, increased their gold holdings by 44 tons and 38 tons respectively in the first half of this year, making them the only two countries with a significant increase in net purchases. Among other countries that reported buying gold, China and Poland increased their gold holdings by 29 tons and 19 tons respectively, and a slowdown in the pace of increase has become a common phenomenon.

Metals Focus believes that the slowdown in gold purchases by official sectors is somewhat related to the sharp rise in gold prices since March this year. Although generally the gold buying decisions of reserve management institutions are less affected by gold price fluctuations, the record high gold price and its rapid rise may have had an impact on the decision of how much gold to buy in the short term. Despite the slowdown in buying pace (or unchanged gold holdings), due to the continuous rise in gold prices, the proportion of gold reserves in most countries' international reserves in the first half of 2024 has increased. This also helps explain why the gold buying activity by global official sectors has slowed down in recent months.

Just as in the period between 2022 and 2023, the de-dollarization is still the main driving factor behind the strong interest in gold by many central banks this year. This largely reflects the heightened geopolitical tensions over the past two years, especially after the US decided to weaponize the dollar through sanctions against Russia. Although its use in transactions is limited, gold is recognized as a safe asset that can be stored domestically, free from the impact of sanctions or seizures.

Concerns about the long-term sustainability of US debt have also been growing this year. Regardless of the outcome of the November presidential election, it is unlikely that the US government's budget deficit will be significantly reduced in the coming years. With the bleak economic prospects and worsening sovereign debt issues, the scope for shifting towards holding other major reserve currencies such as the euro and the yen is also limited. Considering the impressive performance of gold prices, it may not be surprising that some central banks have decided to increase their gold exposure.

Official sector quarterly net purchases/sales value

In addition to robust buying, the lack of significant selling has also helped maintain the global central banks' net gold purchases at a high level. In fact, in the first half of 2024, the total gold sales by official sectors worldwide decreased by two-thirds year-on-year, although the high base in the first half of 2023 is an important reason behind it. At that time, the Central Bank of Turkey injected a huge liquidity into the domestic gold market temporarily, driving up the selling volume, ahead of the presidential election. Almost all the countries that sold gold this year were countries that had bought a significant amount of gold in the past decade. Some countries (such as the Philippines and several CIS countries) have abandoned the strategy of "buying and passively holding" and adopted a more active gold reserve management strategy by maintaining the proportion of gold reserves in their international reserves at a set level. With the recent increase in gold prices, it is understandable that these countries have chosen to reduce their gold holdings (although in limited quantities).

Looking ahead, the aforementioned favorable factors are expected to continue to exist in the foreseeable future, so there are still sufficient reasons for official sectors to increase their gold reserves. In terms of the political situation, the outcome of the US presidential election in November may lead to further instability in the geopolitical situation, especially if a Republican president is elected. Of course, the impact of the continuously rising gold prices should not be ignored. Metals Focus still believes that gold prices will reach new highs in the later part of this year. However, some reserve management institutions may consider the current gold price to be too high as an entry point, which could limit the scale of official sector purchases.

Editor/new