The Star Market is about to welcome a new stock listing.

According to Gelonghui, Yinosi (688710.SH) completed its subscription on August 23 and will be listed on the Star Market in the near future, with Haitong Securities as the sponsor.

Yinosi is a biomedical CRO (Contract Research Organization) enterprise, ranking third in the market share of non-clinical safety evaluation in China, following Wuxi Apptec and Joinn Laboratories.

When it comes to CXO, many investors first think of Gelong. In recent years, the ups and downs of the CXO industry have made many people sigh. Everyone involved in it cannot escape the industry cycle. Under the industry wave, Yinosi has experienced high growth and will face a test period in 2024.

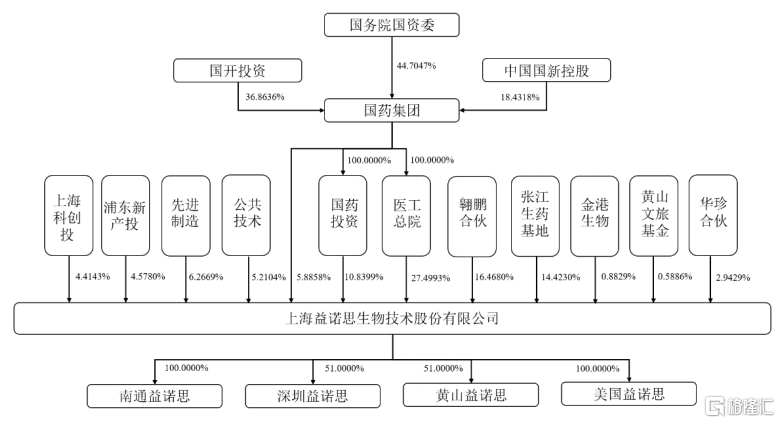

It is worth noting that Yinosi is one of the few national teams in the CRO field, with China National Pharmaceutical Group, under the State Council State-owned Assets Supervision and Administration Commission, holding actual control over 30% of the voting rights, and the actual controlling shareholder of the company.

In addition, Yinosi introduced two experimental monkey suppliers (Huazhen Partnership and Jingang Biological) as shareholders before the IPO, and this rushed shareholding behavior once raised market concerns about interest transmission.

Pre-issuance equity structure of the company, sourced from the prospectus.

The issue price of Yinos is 19.06 yuan per share, and the number of new shares issued is 35.2449 million shares, accounting for 25% of the total share capital after the issuance; the total amount of funds raised is estimated to be 0.672 billion yuan, which is significantly different from the intended fundraising amount of 1.6 billion yuan in the previous prospectus.

The price-earnings ratio of this issuance is 15.40 times, slightly lower than the industry's average price-earnings ratio (18.37 times). Considering the good market atmosphere for new listings recently, the company is highly likely to rise on the first day of listing.

01

There is sufficient reserve of experimental monkeys and the gross margin is increasing.

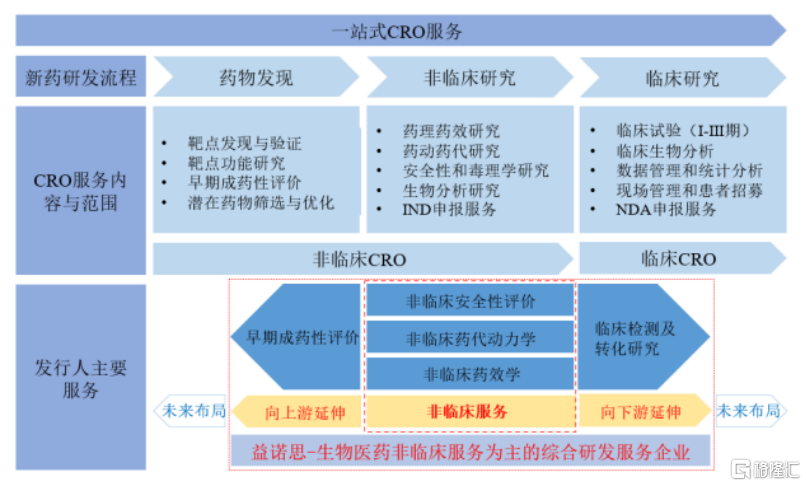

Yinos is a comprehensive research and development service (CRO) company specializing in providing non-clinical research services in the field of biomedical. The services cover three major sectors: early-stage evaluation of biomedical drugs, non-clinical research, and clinical testing and translation research.

The specific content of the non-clinical research sector includes non-clinical safety evaluation, non-clinical pharmacokinetic research, and non-clinical pharmacological research.

The company's business areas are listed in the prospectus.

Specifically, more than 90% of the company's annual revenue comes from non-clinical research services, mainly serving Class I innovative drug development. As of the end of 2023, the company has assisted in the research services for over 100 international and domestic first-in-class innovative drugs.

Non-clinical CRO business is the foundation of the company's business development, accounting for over 90% of the revenue; among which, non-clinical safety evaluation accounts for over 80%.

Company's business structure, sourced from the prospectus

Benefiting from the rapid development of China's CRO market in recent years and the continuous improvement of the company's service capabilities, the company's operating income during the reporting period has shown a good growth trend.

In 2021, 2022 and 2023 (referred to as the 'reporting period'), the company achieved operating income of 0.582 billion yuan, 0.863 billion yuan, and 1.038 billion yuan, respectively, with a compound annual growth rate of 33.60% over the three years. During the same period, the net income was 84.5201 million yuan, 0.118 billion yuan, and 0.182 billion yuan, respectively.

Main financial data and financial indicators during the reporting period, sourced from the prospectus

During the reporting period, the gross margin of Yinuosi's main business was 38.40%, 40.35%, and 43.63% respectively, steadily improving. The change in the company's gross margin is mainly influenced by factors such as sales prices, raw material purchase prices, labor costs, and market competition, with the fluctuation of the price of laboratory monkeys being the most critical factor.

Laboratory monkeys are the company's main raw materials, and the proportion of income generated from business involving the use of laboratory monkeys during the reporting period ranges from 44% to 53% of the total revenue.

From 2021 to 2022, there was a tight supply of laboratory monkeys (upstream raw materials), and prices continued to rise. Since the second quarter of 2023, the tight supply of domestic laboratory monkeys has eased due to factors such as the decreased demand for COVID-related drugs.

Regarding the increase in the company's gross margin due to the rise in raw material prices, the explanation in Yinuosi's prospectus is that the company has reserved laboratory monkeys early and at a low cost, which has to some extent smoothed the overall cost of laboratory monkeys, resulting in a slower increase in the company's laboratory monkey costs compared to the increase in order prices, thereby leading to an increase in gross margin.

When comparing gross margins with industry peers, the source is the prospectus.

Overall, due to differences in the reserve levels of laboratory monkeys and the valuation methods used for cost allocation, there are significant differences in gross margins among companies in the same industry.

However, if the prices of laboratory monkeys and other raw materials fluctuate significantly in the future, or if there is a shortage of laboratory monkeys due to special events, it may have an adverse impact on the company's production and operation.

It is worth noting that at the end of 2023, the company's inventory book value reached 0.511 billion yuan, accounting for 25.71% of the current assets; the majority of the inventory is the company's contract fulfillment cost, and if there is a cost overrun in scientific experiments in the future, it will face the risk of inventory write-down.

In addition, by the end of 2023, the company's accounts receivable book value exceeded 0.2 billion yuan, although the vast majority are within 1 year, it still needs to be alert to the risk of bad debt losses due to unrecoverable accounts.

02

The financing end of the pharmaceutical industry is declining, and a chill is beginning to sweep over the CRO.

Although the company's performance growth has been fast before 2023, the subsequent industry risks cannot be ignored.

In 2023, due to the weakening of investment and financing enthusiasm in the CRO industry, the slower-than-expected growth of the pharmaceutical market, and other factors, the demand growth rate has slowed down. In addition, factors such as intensified industry competition and the decrease in the price of experimental monkeys have caused the new signed orders' prices at Yisheng to decline since the second half of 2023, resulting in a year-on-year decrease in gross margin of 8.23 percentage points in the first half of 2024, causing a year-on-year decrease in non-GAAP net profit attributable to the parent of 14.79%.

The company expects the decline in the first 9 months of 2024 to further expand, with a non-GAAP net profit attributable to the parent of approximately 0.119 billion yuan to 0.13 billion yuan, a year-on-year decrease of 21.93% to 28.53%, exceeding the expected decline.

The company's performance fluctuations are closely related to the investment and financing cycle in the biomedical field.

In the past few years, the high financing in the global biomedical field has injected sufficient funds for Biotech to conduct new drug research and development.

According to iqvia holdings, the global biomedical enterprise financing amount (including IPO, follow-up financing, and venture capital) increased significantly to over 100 billion US dollars in 2020 and 2021, reaching a historical high, which has also brought about a high prosperity in the CRO industry.

However, since 2022, with the fading of excessive disturbance factors, global biomedical financing has fallen back to about 61 billion US dollars from a high level.

Affected by this, the research and development input of Biotech companies may decline, thereby affecting the demand for CRO.

Global biomedical financing situation, source prospectus

In addition, CRO services belong to a market with relatively full competition.

In recent years, the emphasis on cost control of unit project research and development by pharmaceutical companies and the mismatch between supply-side capacity planning and the slowdown in demand growth have led to more options for downstream customers to find partners, and the competition among CRO companies has become increasingly fierce.

On the one hand, multinational CRO companies such as IQVIA and LabCorp have successively established branches in China to accelerate the development of the domestic market, and the company will compete in the domestic market with multinational CRO companies in pharmaceutical R&D business.

On the other hand, domestic CRO companies such as WuXi AppTec, Pharmaron, Joinn Laboratories, and Shanghai Medicilon Inc. are gradually growing, further intensifying the competition in the domestic CRO industry.

After many years of development, the global safety assessment market in 2022 has presented an oligopoly monopoly situation. The two oligarchs, Charles River and LabCorp, hold approximately 27.2% and 14.8% of the market share, respectively, giving them a relatively absolute competitive advantage in the market.

From a domestic perspective, the company ranks in the top three in the domestic non-clinical safety assessment sub-field market with a market share of 6.8% in 2022, with WuXi AppTec and Joinn Laboratories ranking ahead.

Competition in the non-clinical safety assessment service industry, source: prospectus

In addition, YiNuoSi's current business is mainly focused on domestic customers, with over 95% of its revenue coming from the domestic market during the reporting period. There is currently no geopolitical risk, but if domestic peer companies are hindered overseas in the future, it will inevitably lead to intensified competition in the domestic market, adding further pressure to the industry competition.

In the scenario where multiple negative factors are combined, the company's adjusted net income attributable to the parent may experience a decline in 2024 that exceeds the expected drop, or there may be a risk of further decline in the future.