The Silence Therapeutics plc (NASDAQ:SLN) share price has fared very poorly over the last month, falling by a substantial 26%. Looking at the bigger picture, even after this poor month the stock is up 87% in the last year.

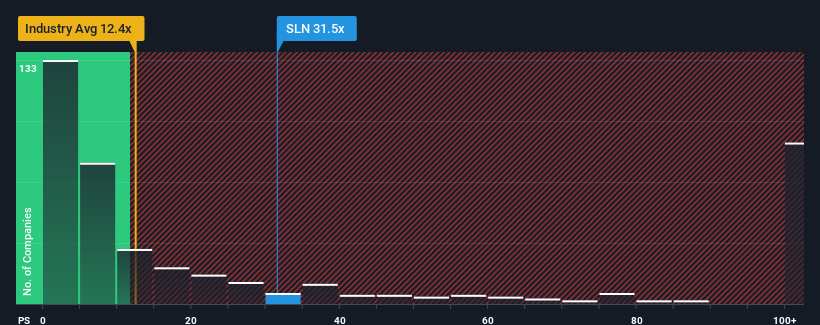

Even after such a large drop in price, Silence Therapeutics may still be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 31.5x, since almost half of all companies in the Biotechs industry in the United States have P/S ratios under 12.4x and even P/S lower than 5x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

What Does Silence Therapeutics' P/S Mean For Shareholders?

Silence Therapeutics could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Silence Therapeutics' future stacks up against the industry? In that case, our free report is a great place to start.How Is Silence Therapeutics' Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Silence Therapeutics' to be considered reasonable.

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Silence Therapeutics' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 37% decrease to the company's top line. Even so, admirably revenue has lifted 76% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 28% per annum as estimated by the five analysts watching the company. With the industry predicted to deliver 140% growth per annum, the company is positioned for a weaker revenue result.

With this in consideration, we believe it doesn't make sense that Silence Therapeutics' P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Bottom Line On Silence Therapeutics' P/S

Even after such a strong price drop, Silence Therapeutics' P/S still exceeds the industry median significantly. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've concluded that Silence Therapeutics currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You need to take note of risks, for example - Silence Therapeutics has 3 warning signs (and 1 which is significant) we think you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.