From August 1st to August 18th, the new energy vehicle market retailed 0.49 million vehicles, a 58% year-on-year increase over the same period last August, and a 27% increase over the same period last month. The cumulative retail sales this year have reached 5.478 million vehicles, a 36% year-on-year increase.

According to the data released by the China Association of Automobile Manufacturers, from August 1st to August 18th, the new energy vehicle market retailed 0.49 million vehicles, a 58% year-on-year increase over the same period last August, and a 27% increase over the same period last month. The cumulative retail sales this year have reached 5.478 million vehicles, a 36% year-on-year increase; the national passenger vehicle manufacturers' wholesale of new energy vehicles reached 0.431 million vehicles, a 33% year-on-year increase over the same period last August, and a 21% increase over the same period last month. The cumulative wholesale this year has reached 5.993 million vehicles, a 30% year-on-year increase.

From August 1st to August 18th, the passenger vehicle market retailed 0.907 million vehicles, an 8% increase over the same period last August, and a 16% increase over the same period last month. The cumulative retail sales this year have reached 12.474 million vehicles, a 3% year-on-year increase; the national passenger vehicle manufacturers' wholesale reached 0.757 million vehicles, a 9% year-on-year decrease over the same period last August, and a 12% increase over the same period last month. The cumulative wholesale this year has reached 14.477 million vehicles, a 4% year-on-year increase.

In August 2024, the national passenger vehicle market had a stable start in retail.

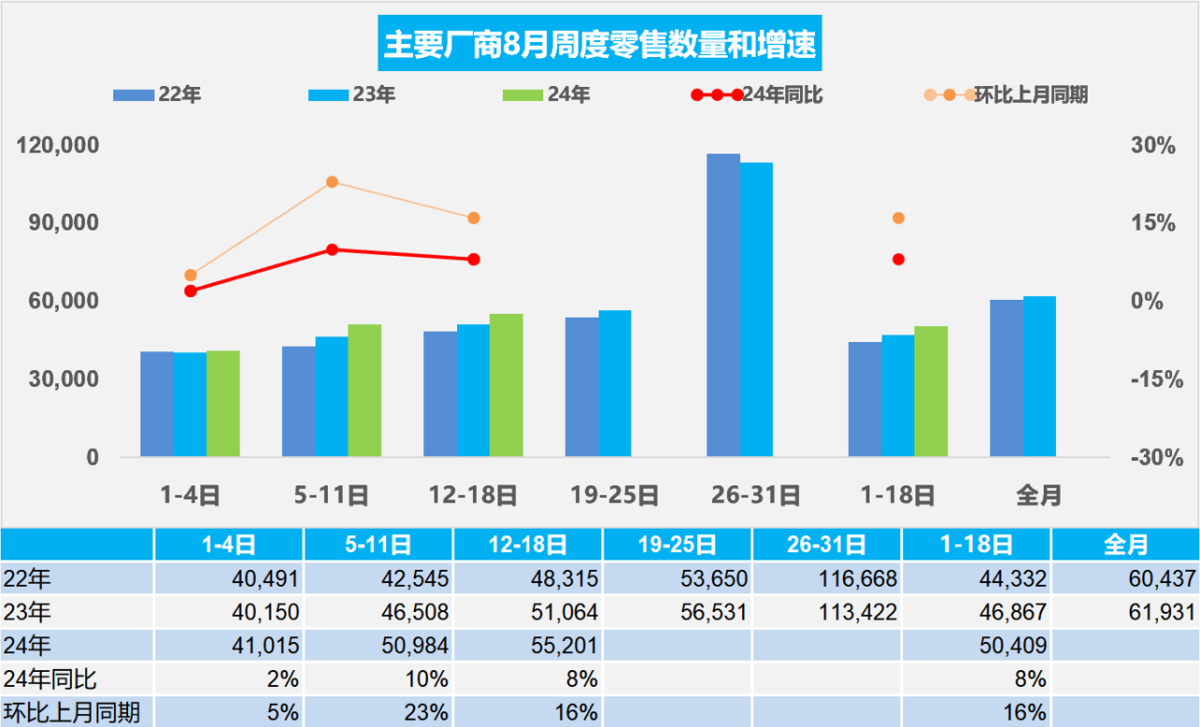

In the first week of August, the average daily retail sales of passenger vehicles reached 0.041 million vehicles, a 2% year-on-year increase over the same period last August, and a 5% increase over the same period last month.

In the second week of August, the average daily retail sales of passenger vehicles reached 0.051 million vehicles, a 10% year-on-year increase over the same period last August, and a 23% increase over the same period last month.

In the third week of August, the average daily retail sales of passenger vehicles reached 0.055 million vehicles, an 8% year-on-year increase over the same period last August, and a 16% increase over the same period last month.

From August 1st to 18th, the passenger vehicle market retailed 0.907 million vehicles, an 8% increase over the same period last August, and a 16% increase over the same period last month; the cumulative retail sales this year have reached 12.474 million vehicles, a 3% year-on-year increase.

Compared to July, the demand for a second family car for transporting children to and from school is stronger before the start of the school season in August. In the first half of this year, there were 3.43 million marriages registered nationwide, a decrease of 0.498 million compared to the same period last year, which puts some pressure on the wedding car market in the autumn.

Since the middle and late July, manufacturers and dealers, with a mindset of recuperation, combined with seasonal personnel and equipment rest under the high-temperature summer environment, have focused on promotion recovery and price stability strategies on the premise of maintaining a good production and sales rhythm, in order to maintain channel stability.

The current complex and changeable external environment has a significant impact on consumer confidence. Some consumers have weak consumption confidence, and the demand for first-time purchases is far less than that of replacement purchases. Although the subsidies for stimulating car consumption at the local level this year are generally much lower than last year in terms of subsidy amount and the scale of benefiting users, the delay in initiation has brought about a doubling of the national scrapping and renewal subsidy policy, which has become an important driving force for the growth of the car market. The demand for replacement and additional purchases has driven the continuous strength of the new car and used car markets, and will continue to serve as the cornerstone of maintaining the existing scale of the automotive market.

In August 2024, the sales volume of passenger vehicle manufacturers nationwide started off weak.

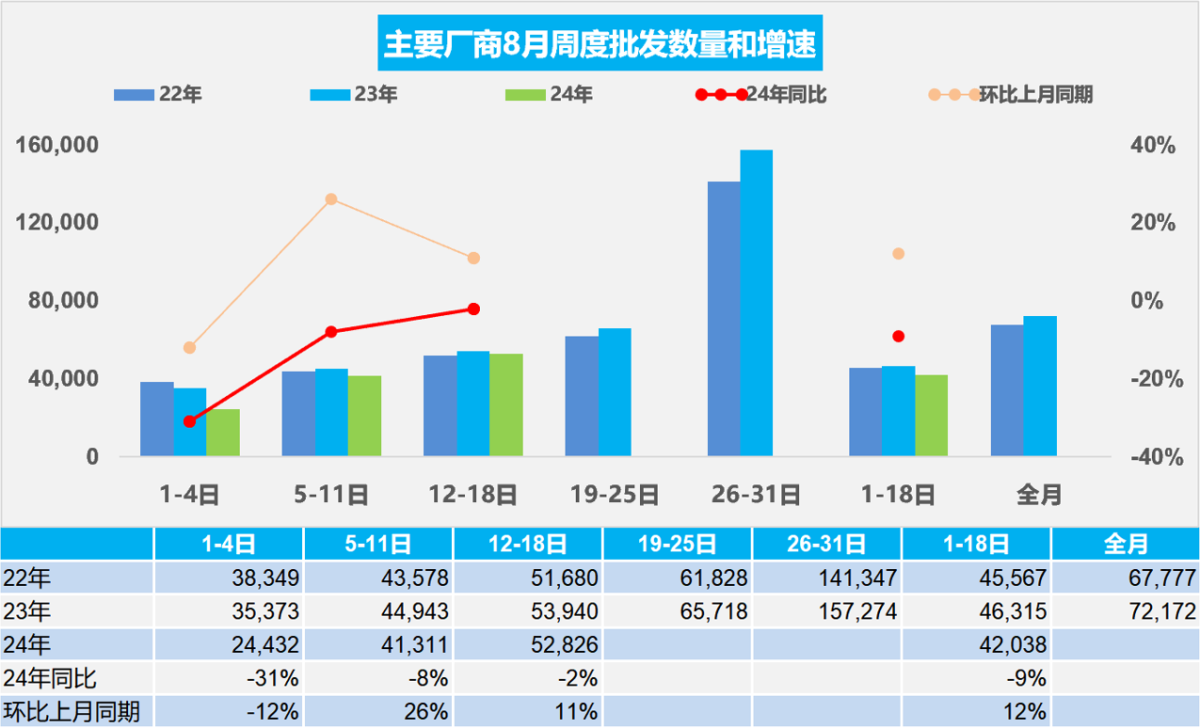

In the first week of August, the average daily wholesale volume of passenger vehicle manufacturers was 0.024 million, a decrease of 31% compared to the same period in August last year, and a decrease of 12% compared to the same period last month.

In the second week of August, the average daily wholesale volume was 0.041 million, a decrease of 8% compared to the same period in August last year, and an increase of 26% compared to the same period last month.

In the third week of August, the average daily wholesale volume was 0.053 million, a decrease of 2% compared to the same period in August last year, and an increase of 11% compared to the same period last month.

From August 1st to 18th, passenger vehicle manufacturers nationwide wholesale 0.757 million vehicles, a decrease of 9% compared to the same period in August last year, and an increase of 12% compared to the same period last month. The cumulative wholesale volume this year has reached 14.477 million vehicles, a year-on-year increase of 4%.

In August, there were 22 working days, one day less than last year. With the structural differentiation of the car market growth, most companies have sufficient traditional car production capacity, and a longer period of high-temperature leave, the car market is in a period of rest. In August, there are peak holidays at the beginning of the month and mini peak holidays in the middle of the month, so the sales trend of manufacturers fluctuates greatly. Recently, manufacturers have reduced the pressure of production and sales at the beginning of the month, in order to consider the survival pressure of dealers and changes in market prices, and achieve more pragmatic sales management. Therefore, sales in late August should rebound to some extent.

With the promotion of the scrap update subsidy policy in the retail market in August and the gradual introduction of replacement update policies in various regions, manufacturers' production and sales will gradually recover well.

In July 2024, car production decreased by 2%, consumption decreased by 5%, and the penetration rate of new energy vehicles was 0.99 million, accounting for 43%.

According to data from the National Bureau of Statistics, in July, the total retail sales of consumer goods reached 3,775.7 billion yuan, a year-on-year increase of 2.7%. Among them, the consumption of automobiles was 379.8 billion yuan, a decrease of 4.9%, and the retail sales of consumer goods other than automobiles reached 3,395.9 billion yuan, an increase of 3.6%. From January to July, the total retail sales of consumer goods reached 27,372.6 billion yuan, a year-on-year increase of 3.5%. Among them, the consumption of automobiles was 2,673.6 billion yuan, a decrease of 1.7%, and the retail sales of consumer goods other than automobiles reached 24,699 billion yuan, an increase of 4.0%.

In 2024, the demand for car production will steadily increase, the expectations for social consumption will continue to improve, and the high-quality development of the automobile industry will continue to rebound. In 2023, the relationship between car sales and real estate sales is 37 square meters of housing per car, and it will continue to decrease to 33 square meters of housing per car in 2024. The comparison between housing and car sales has slightly improved, which is more reasonable than the peak in 2020 when it was 70 square meters per car. Due to debt pressure, the demand for the car market is relatively low. As the only consumer goods not yet popularized in urban and rural families in China, the overall trend of the national passenger car market has been improving in recent years, and passenger car consumption has gradually improved.

With the decrease in the impact of the low base of the Spring Festival factor in 2024, there is still considerable pressure for the growth of car consumption. Therefore, promoting car market consumption and implementing vehicle scrapping and update subsidies, especially doubling the subsidies for scrapping and updating, will have a good market promotion effect. The car market expects that the impact of scrapping and updating of owners must be owners before the policy is implemented. It is hoped that in the future, there will be more improvement measures such as promoting new energy vehicles to rural areas, reducing personal income tax for car buyers, exempting vehicle purchase taxes for compliant pure electric vehicles with a range below 200 kilometers, and encouraging marriage and car purchases, which will stimulate car consumption and promote economic growth.

As of the end of July, the national passenger car market had a stock of 3.33 million vehicles, with an inventory turnover of 52 days.

In July, the trend of new energy vehicles is good, but due to the deep adjustment of the production and sales of fuel vehicles, the inventory of passenger cars in the country was 3.33 million vehicles at the end of July 2024, a decrease of 0.11 million vehicles from the previous month. The proportion of manufacturer's inventory is 26.8%. The total inventory of passenger vehicles nationwide decreased by 0.15 million vehicles compared to July 2023, but increased by 0.09 million vehicles compared to July 2022.

Due to the relatively slow recovery of the market after the price reduction during the Spring Festival this year, the competition pressure in the fuel vehicle market is greater. Under the combined influence of expectations brought by stimulus policies, further promotion of wait-and-see sentiment, and other factors, manufacturers have significantly reduced production to cope with the sluggish market. At the end of July, the total manufacturer inventory of 3.33 million vehicles supports 52 days of future sales, compared to 53 days of inventory in July last year, the structural pressure is relatively stable.

We evaluate the monthly market performance according to the setting method and evaluation results of the PMI index. According to the summary calculation of forecasts by internal personnel of the manufacturers, the forecast index PFI for passenger vehicles in July is 27%, and the satisfaction index PSI is 67%. Currently, the forecast index PFI for passenger vehicles in August is 63%. The satisfaction rating of the market in July is similar to the reversal perception of the market at the previous extremely low point.

In July 2024, the demand for lithium iron phosphate batteries continued to strengthen.

In July 2024, the installed capacity of lithium batteries was 42GWh, a year-on-year increase of 29%. The installed capacity of ternary batteries was 11.4GWh, accounting for 27%, lower than the same period; while the installed capacity of lithium iron phosphate batteries was 30GWh, accounting for 72%, showing a slight slowdown in the growth of ternary batteries. From January to July, the installed capacity of lithium batteries was 245GWh, a year-on-year increase of 29%.

In recent years, the market for pure electric passenger vehicles has declined sharply, while the demand for batteries in pure electric special vehicles has continued to rise rapidly. Currently, the market share of pure electric passenger vehicles has dropped from 18.5% in 2020 to 1% in 2024, a decrease of 17 percentage points. The battery usage in plug-in hybrid passenger vehicles has grown relatively rapidly, currently rising from 7% in 2021 to 22% this year, an increase of 15%. Meanwhile, the proportion of pure electric vehicles has dropped to 67%, and plug-in hybrids and pure electric vehicles together account for about 90% of the core battery demand in the passenger vehicle segment.

According to the calculation of battery volume based on the certification, the production volume of certified products in July 2024 is 0.895 million units. From January to July, the production volume is strong with 5.22 million units, including 2.85 million units of pure electric passenger vehicles, 2.08 million units of plug-in hybrid passenger vehicles, and 0.26 million units of pure electric special vehicles. These production data are still good.

The energy density range of the mainstream batteries for pure electric vehicles is currently between 125 and 160. Particularly in July 2024, the battery proportion in the range of 125 to 140 reached 50%, an increase of 8 percentage points year-on-year.

In January to July 2024, the proportion of vehicle models with an energy density of 160 or higher is 14%, which shows a significant decrease compared to 18% in 2023. This is mainly due to the decrease in energy density caused by the substitution of lithium iron phosphate batteries for ternary batteries. The proportion of products with an energy density below 125 has decreased from 9% in 2023 to the current 4% in 2024, and is expected to decrease to 1% in the third quarter.