Investors can still pay attention to the timing opportunities between the announcement date of Hang Seng Composite Index and the effective date of the Hong Kong Connect.

Hang Seng Index Company announced today that as of June 30, 2024, the quarterly review results of the Hang Seng Index Series show that there is no change in the constituent stocks and the number of constituent stocks remains at 82.

The number of constituent stocks in the Hang Seng Composite Index has increased from 509 to 518. All changes will be implemented after the close of trading on Friday, September 6, 2024, and will take effect from Monday, September 9, 2024.

Which symbols will be included in the Hong Kong Connect?

The new stocks included in the Hong Kong Connect can be judged based on the changes of the constituent stocks of the Hang Seng Composite Index.

As we all know, the first step of the Hong Kong Connect is to include stocks in the Hang Seng Composite Index. If the stock belongs to the large-cap or mid-cap index, it will be included. If the stock belongs to the small-cap index, it needs to be considered. If the average market capitalization at the end of the month for 12 months is greater than or equal to HKD 5 billion, it will be included; otherwise, it will not be included.

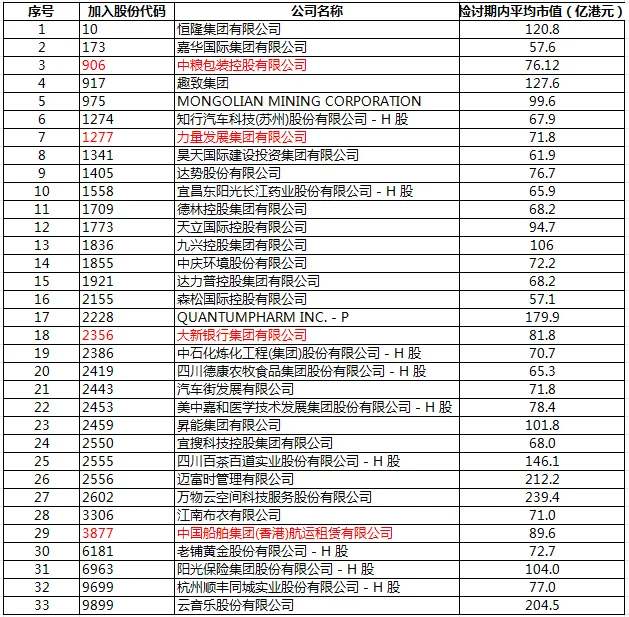

A total of 38 symbols were included in the Hang Seng Composite Index this time. 5 symbols that were already included in the Hong Kong Connect are deleted: CSSC Offshore & Marine Engineering (00317), China Merchants Group (00598), Huadian Power International Corporation (01071), China Zheshang Bank (02016), and China International Marine Containers (02039). There are still 33 symbols left after the deletions. The average market value at the end of the month during the inspection period (July 2023 to June 2024) of these symbols is as follows:

As shown in the above table, the lowest average market value during the inspection period is HKD 5.71 billion for SinoMab BioScience (02155). According to the inclusion rules of the Hong Kong Connect, all the 33 symbols above can be included in the Hong Kong Connect after this review.

It is worth noting that in some institution's predictions before the announcement of the review results, Great Eagle H, Cosunter, and Wasion Holdings, which have been highly anticipated to be included in the Hong Kong Connect, did not appear on the list of Hang Seng Composite Index this time. Four 'dark horses' that were not predicted but made it to the list are: COFCO Packaging, Kinetic Dev, Dah Sing Banking Group, and CSSC Shipping.

There is also a special stock that is expected to be included in the Hong Kong Connect in this adjustment, Alibaba-SW (09988).

Alibaba CFO Maggie Wu revealed in a recent earnings conference that Alibaba is actively seeking to make Hong Kong its primary listing venue. The shareholder meeting on August 22 will be another important moment in Alibaba's history. Once approved, Alibaba will complete dual primary listing in New York and Hong Kong at the end of August.

According to the regulations for the inclusion of weighted voting right stocks in the Hong Kong Connect, stocks that have been converted to a dual primary listing but have not yet met the criteria for the inclusion must be included as a constituent after 6 months and 20 trading days since the conversion date. The inspection date is the second Hong Kong trading day before the effective date of the regular adjustment of the constituent stocks of the Hang Seng Composite Index after the transition to the primary listing (September 5, 2024). Considering that Alibaba-SW's daily average market value and total turnover in the past 183 days have far exceeded the entry criteria for weighted voting right stocks, if Alibaba successfully completes the dual primary listing at the end of August, it is expected to be included in the Hong Kong Connect during this adjustment. Citic Securities has calculated the ETF situation currently linked to the Hong Kong Connect and Hong Kong Connect-related indices, which is expected to bring about HKD 4.03 billion of passive funds.

II. Trading excess returns opportunities before the effective date.

According to CITIC Securities' estimation, since 2019, during the interval between the announcement date of the Hang Seng Composite Index and the effective date of the Hong Kong Connect, the predicted relative average excess return of the included symbols to the Hang Seng Composite Index has reached 5.5%. After 30 days of the Hong Kong Connect taking effect, the average excess return of the symbols included in the Hong Kong Connect has declined significantly, with the excess return relative to the Hang Seng Composite Index since 2019 being only 0.2%.

During the time span from the announcement date of the Hang Seng Composite Index to the effective date of the Hong Kong Connect in 2023, the average excess returns of the included symbols dropped significantly to 0.8%. However, this is mainly due to the influence of the surge in long-term US Treasury yields on growth sector valuations in the 3rd quarter of 2023. The excess returns of the included symbols rose again in early 2024.

If the focus is on the newly listed stocks that are expected to be included, it can be found that the news of their inclusion has been priced in by the market beforehand, and the excess returns are not significant before the effective date.

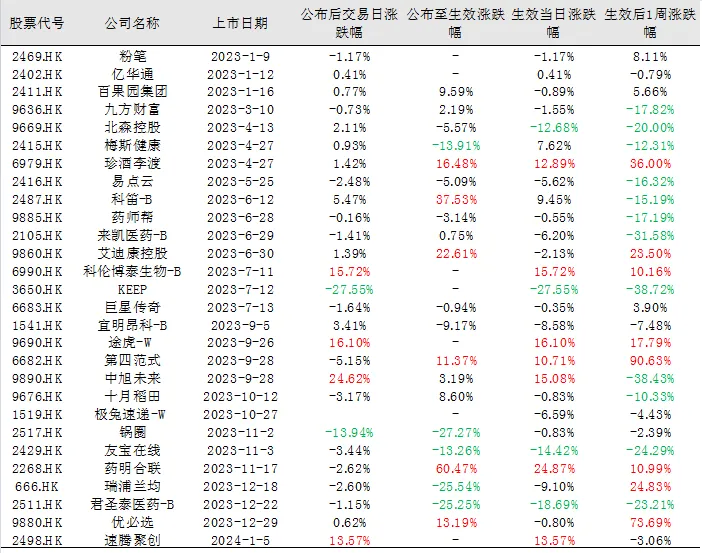

("-" represents the announcement date, which is also the effective date in this case.)

From the table above, we can see that, from the announcement to the effective date, the stocks that rose by more than 10% were Zhenjiu Lidu, Keda B, Eddie Kang Holdings, Fourth Paradigm, while those that fell by more than 10% on the day of the announcement were Meisi Health, Youbao Online, Ruipulan and Junshengtai Pharmaceutical.

There was a mix of gains and losses on the day the announcement took effect. Stocks that rose by more than 10% were Zhenjiu Lidu, Kebotai, Tu Tiger, Fourth Paradigm, Yiming Heli, and Suteng Juchuang. Stocks that fell by more than 10% included Beisen Holdings, Youbao Online, and Junshengtai Pharmaceutical.

As for the week after inclusion, the fluctuations were generally greater. There were many stocks that rose more than 10%, including Zhenjiu Lidu, Eddie Kang Holdings, Kebotai, Tu Tiger, Fourth Paradigm, Yiming Heli, Ruipulan, and Youbixuan, and so on.

Based on the above-mentioned historical performance, we can summarize that:

(1) Considering that the overall valuation of Hong Kong stocks is currently at a historical low point, the outflow of funds and the further downside of the market are limited, investors can still pay attention to the timing opportunities from the Hang Seng Index announcement day to the Hong Kong stock connect effective date.

(2) This time, newly and recently listed stocks included Lao Pu Huangjin (06181), QUANTUMPH-P (02228), and so on. The performance of these stocks is worth paying special attention to before the effective date.

(3) Of course, it is also worth noting that passive funds adjust their positions after the end of the trading day prior to the effective date (September 6). Stocks with relatively poor liquidity may be more affected by the adjustment of funds.

3. After including in Hong Kong Stock Connect, which symbols are more likely to be profitable?

After analyzing the market features and historical data after including Hong Kong Stock Connect, the research department of private institution Hengchang Investments found that:

1. Companies with a market cap less than HKD 10 billion. Companies with a lower market capitalization usually see a greater increase in liquidity and significant excess returns after including Hong Kong Stock Connect.

2. Companies with a PB less than 5x. Companies with a low PB ratio often exhibit better market returns during the Hong Kong Stock Connect adjustment period.

3. Sectors such as cyclicals, consumption, and technology. Companies in these sectors often perform better during market corrections, especially those with good fundamentals.

Based on these features, after considering market cap, PB, sectors, and fundamentals, Hengchang Investments recommends the following symbols:

Dongyangguang Changjiang Pharmaceutical (01558), a Chinese pharmaceutical company that specializes in product development, production and sales in the treatment fields of anti-virus, endocrine and metabolic diseases, cardiovascular diseases, and so on. The company currently produces, promotes, and sells a total of 33 pharmaceutical products in China, and produces 11 active pharmaceutical ingredients, most of which are for self-use. Currently, the company's three major treatment fields are anti-virus products, endocrine and metabolic disease treatment products, and cardiovascular disease treatment products. In the field of anti-virus treatment, especially for the treatment of influenza virus, the company has Keweite (oseltamivir phosphate) capsules and granules. In the endocrine and metabolic disease treatment field, Etongshu (benzbromarone tablets) is the company's main product. Etongshu is used to treat hyperuricemia. In the field of cardiovascular disease treatment, Oumeining (telmisartan tablets) and Xinhaining (amlodipine besylate and benazepril hydrochloride tablets) are the company's main products. In 2023, the company's net income reached 21.99 billion yuan, an increase of 2501.24% year-on-year.

Shunfeng Same Day (09699), backed by Shunfeng Group, is a leading third-party instant delivery provider. Shunfeng Same Day adopts a full-scenario business model, covering all types of products and services, such as same-city delivery service for businesses, same-city delivery service for consumers, and last-mile delivery service. In 2023, the net profit turned from loss to profit, and the company's revenue in 2023 was RMB 12.387 billion, a year-on-year increase of 21.1%. The total number of orders increased by more than 30% year-on-year, with same-city delivery service/last-mile delivery service revenue of RMB 7.387/5 billion respectively, a year-on-year increase of 12.8%/35.9%. The analyst of CITIC Securities predicts that the operating income in 2024-2026 will reach RMB 15.3/18.6/21 billion respectively, with year-on-year growth of 23.6%/21.8%/12.5%. Adjusted net profit is RMB 0.167/0.393/0.589 billion yuan, respectively, with a year-on-year change of +156.9%/+135.7%/+50.1%.

tianli int hldg (01773), tianli int is a leading K12 private education service provider in China, and has shifted its focus to the for-profit high school business. In the early days, the school mainly focused on K9 education. After going public in Hong Kong in 2018, the company relied on nearly 20 years of experience in operating schools and good reputation to expand to other provinces. As of now, the company has 50 schools in 16 provinces across the country. During this period, relying on its excellent record of promotion to higher education, the company has successfully transformed and focused on the for-profit high school market after the implementation of the Charity Law in 2021. The company achieved a revenue of 2.32 billion yuan in FY23, which is +161% year-on-year and exceeded the historical peak of 2020. The net income attributable to the parent company was 0.33 billion yuan, a year-on-year increase of 246%, which has recovered to 92% of the level in 2020. The enrollment of the company's high schools has been growing rapidly due to its excellent high school academic reputation, abundant sources of students from K9 education segment, as well as projected plans to open 3-5 new high schools every year. Meanwhile, the company will also accelerate its business expansion into entrusted management services based on its good reputation, having signed contracts with 14 schools and more than 20 education segments, which is comparable to the size of 190 schools managed by Hailiang Education. The future light-asset entrusted management business of the company also has broad development space. Analysts at Guoxin Securities predict that the net income attributable to the parent company in FY24-26 will be 0.55 billion, 0.81 billion, and 1.11 billion respectively, with a year-on-year increase of +49% / +34% / +29%.

Domino's representative in China, Hong Kong and Macau is Dashen (01405). By the end of 2023, Dashen already had 768 stores across more than 20 cities. From 2020 to 2023, Dashen has achieved rapid growth in revenue, with a CAGR of 40.3%. The gross margins for 2020-2023 were 71.9%, 73.6%, 72.8%, and 72.6%, respectively. For 2023, the company's profit has turned around from loss to profit. Backed by the world's largest pizza brand, Domino's strong brand background and powerful brand strength ensured strong performance of new store openings. Analysts at China Merchants Securities predict that in 2024/25/26, the newly added market will have a net increase of 210/270/300 stores.

JNBY (03306), as a leading Chinese designer brand, has a mature multi-brand matrix and excellent omni-channel operating capabilities. Its large number of high-stickiness members continue to contribute to sales and provide a steady driving force for the company's steady growth. From FY20 to FY23, the company's revenue achieved a CAGR of 12.9%, which is at a leading level in the middle-to-high-end women's wear market. It has created well-known designer brands such as JNBY, CROQUIS (Sketch), jnby by JNBY, and LESS, capturing the middle-to-high-income group with its strong brand recognition and brand values. On the profit side, the company's profitability has maintained a stable and positive trend, with an average net profit margin attributable to the parent company of 13.3% from FY14 to FY23, outstanding cost management, and profit margins ranking among the top in the industry. The company's operating efficiency is also relatively superior among comparable companies. In FY23, the company's inventory turnover days and accounts receivable turnover days were 188 and 9 days, respectively, both significantly better than the overall level of comparable companies. With excellent profitability and sufficient cash flow to support stable and high dividends, the company's FY20-FY23 operating cash flow net amount accounted for an average of 170% of net profit, and the average dividend payout ratio since its listing in FY17-23 was as high as 78.3%. Analysts at Zheshang Securities predict that net income attributable to the parent company will be 0.81/0.85/0.94 billion yuan in FY24-26, with a year-on-year increase of +30%/5%/10%.