Berkshire recently disclosed its holdings for the second quarter, changes in the top ten heavy stocks, in addition to the well-known market cut 49.3% of Apple, also reduced its holdings of Moody's by 3.5%, added to StoneCo by 2.93%, and added to RH by 4.28%. After reducing its holdings in Apple, Buffett, who holds nearly $280 billion, opened positions in two new companies in the second quarter. One is the largest offline cosmetic store in the United States, with a holding amount of $0.266 billion. The other is HEICO Corporation, with a holding amount of $0.185 billion, mainly engaged in aviation repair, aviation materials and military materials. Both are typical US long-term bullish stocks, with a rise of more than 100 times since listing. $Apple (AAPL.US)$ Ulta Beauty, one representative of the 'lipstick economy', went public in 2007. It currently has approximately 1,400 stores in 50 states in the United States, with its membership growing from 6 million in 2007 to 44.2 million in 2023. Member consumption accounts for 95%. Ulta has achieved double-digit revenue growth in 17 of the past 18 years, except for a 16.8% drop in revenue in 2021. Last year's revenue was $11.2 billion, with net income of $1.29 billion. Categorized by revenue, the makeup category accounts for 42%, skincare for 23%, hair for 19%, perfume for 10%, and services for 4%. $Chevron (CVX.US)$ Please use your Futubull account to access the feature. $Occidental Petroleum (OXY.US)$ According to Whalewisdom's estimate, Buffett's cost for holding StoneCo is about $177.5, and his cost for holding Ulta Beauty is about $385. $Chubb Ltd (CB.US)$.

After reducing its holdings in Apple, Buffett, who holds nearly $280 billion, opened positions in two new companies in the second quarter.

One is the largest offline cosmetic store in the United States, with a holding amount of $0.266 billion. $Ulta Beauty (ULTA.US)$ The other is HEICO Corporation, with a holding amount of $0.185 billion, mainly engaged in aviation repair, aviation materials and military materials. $Heico-A (HEI.A.US)$ Both are typical US long-term bullish stocks, with a rise of more than 100 times since listing.

According to Whalewisdom's estimate, Buffett's cost for holding HEICO is about $160.2.$Heico (HEI.US)$According to Whalewisdom's estimate, Buffett's cost for holding StoneCo is about $177.5, and his cost for holding Ulta Beauty is about $385.

The market expressed confusion about the two new companies in which the 'Stock God' opened positions. On the one hand, Ulta Beauty fell 40% in the past six months, and the company's sales prospects are pessimistic, which is now a point of division. Aero repair and aviation materials have very high valuations, not like Buffett's style of investing. This is two different investment styles. What did the 'Stock God' see?

One representative of the 'lipstick economy': Ulta Beauty

Ulta Beauty, one representative of the 'lipstick economy', went public in 2007. It currently has approximately 1,400 stores in 50 states in the United States, with its membership growing from 6 million in 2007 to 44.2 million in 2023. Member consumption accounts for 95%.

Ulta has achieved double-digit revenue growth in 17 of the past 18 years, except for a 16.8% drop in revenue in 2021. Last year's revenue was $11.2 billion, with net income of $1.29 billion.

Categorized by revenue, the makeup category accounts for 42%, skincare for 23%, hair for 19%, perfume for 10%, and services for 4%.

Ulta's main competitor is Sephora. Sephora has approximately 34 million members worldwide, but Ulta has a greater advantage in the US market. The key to Ulta's success is its membership model. In the context of declining consumer spending, Ulta covers all price ranges and has stronger user stickiness than Sephora. Ulta provides members with a cash back mechanism. For example, if a member spends about $2,000, they can get a discount of about $125. The higher the membership level, the higher the amount of the discount. Unlike major brand counters, Ulta can offer members discounts of 40-50% on promotional days because it has acquired products cleared by major brands at a low price. These products generally have a validity period of about one year. Ulta then sells them at a discount to consumers, which increases user stickiness. Beauty products are products with a high repurchase rate, and a good membership system can become a moat.

Thanks to its long-term membership model, Ulta has very strong long-term cash flow capabilities, and its annual disposable cash flow is executing a repurchase plan, which has made Ulta a long-term lipstick economy stock that rose from $4 to a high of $570 in March this year, supported by large repurchases, meaning that it can increase even during economic downturns.

After recent declines in stocks related to the lipstick economy, such as luxury goods and cosmetics, Ulta has also fallen 40% from its highs. In this round of decline, Buffett chose to open positions, a very interesting move.

After reducing its holdings in Apple, Buffett, who holds nearly $280 billion, opened positions in two new companies in the second quarter. One representative of the 'lipstick economy': Ulta Beauty. Ulta's main competitor is Sephora. Sephora has approximately 34 million members worldwide, but Ulta has a greater advantage in the US market. The key to Ulta's success is its membership model. In the context of declining consumer spending, Ulta covers all price ranges and has stronger user stickiness than Sephora. Ulta provides members with a cash back mechanism. For example, if a member spends about $2,000, they can get a discount of about $125. The higher the membership level, the higher the amount of the discount. Unlike major brand counters, Ulta can offer members discounts of 40-50% on promotional days because it has acquired products cleared by major brands at a low price. These products generally have a validity period of about one year. Ulta then sells them at a discount to consumers, which increases user stickiness. Beauty products are products with a high repurchase rate, and a good membership system can become a moat.

After recent declines in stocks related to the lipstick economy, such as luxury goods and cosmetics, Ulta has also fallen 40% from its highs. In this round of decline, Buffett chose to open positions, a very interesting move.

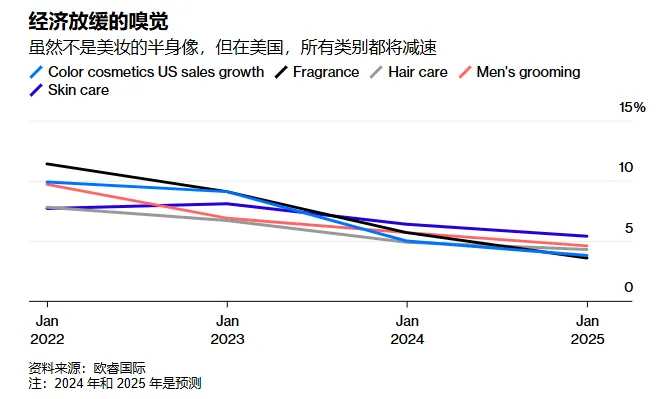

The reason is that in April, Ulta management stated that the global cosmetics and luxury goods market growth rates are slowing down and lowered Ulta's full-year revenue growth to 3-4%, with expected revenue of 11.5 billion USD for the year, which is even more pessimistic than the market expected.

As mentioned earlier, Ulta's revenue has grown at double-digit rates for 17 of the last 18 years, and this year is the second year of non-double-digit growth.

According to L'Oreal's guidance in June, the global beauty market's sales growth for this year was lowered from the previous 5% to 4.5%. Foreign views believe that L'Oreal's guidance is optimistic and that industry growth may only be 4%, or even some category growth may slow to the beginning of 3% next year.

The industry outlook is not optimistic; what did Buffett focus on?

Following this round of downturn, Ulta's valuation fell to around 12 times PE, the lowest level in nearly three years. Of course, at the time Buffett purchased the stock, the share price had not fallen that much, and the valuation was about 14 to 15 times PE.

We need to consider two points: one is whether Ulta's moat will be broken, and the other is whether industry demand is a short-term or medium-to-long-term effect.

Looking back at the past three years, at least Ulta's moat is still very solid. Although beauty has slowed down in the past three years, Ulta mainly operates in the U.S. market, which performs better than other markets. As for industry demand, the U.S. is mainly affected by high inflation, which has recently declined, and is expected to turn around with interest rate cuts.

It is worth noting that in March, Ulta announced a $2 billion share buyback plan, and recent management stated that there is still $1.8 billion remaining in the buyback amount as of May. They may pay dividends and buy back $1 billion within the year, which accounts for about 6% of the latest market value.

From this point of view, it is not difficult to understand the logic of buying Ulta at a low price.

Although industry growth has slowed down, the worst performance will still have a 5% growth rate in the future. In addition, the company has no interest-bearing debt, and its annual operating cash flow exceeds net income. The FY24 operating cash flow/revenue is 13%, and all available cash flow is used for buybacks and dividends. The moat has also been tested for more than ten years, and its valuation has fallen to a low of 12 times PE in nearly three years, which may be one of the reasons why the stock god established a new position. This is also more in line with Buffett's investment style, but it is completely different for Heico, another airline stock.

Second, Heico, a stock that is hundreds of times higher than the PE ratio.

Heico is an aviation parts manufacturer that was listed in 2002 and has performed excessively well since then, with a stock price that has been rising continuously and has never been affected by economic cycles except for the COVID-19 pandemic that caused a few weeks of stock price decline in 2020.

By 2023, revenue will be 2.97 billion USD and net profit will be 0.4 billion USD. The company's gross margin has remained at over 38% for many years, and its operating profit margin has remained above 20% for many years, which is related to the industry's special mode of operation.

According to the introduction by Snowball "Lightning Koala," big factories like General Electric and Pratt & Whitney need to spend huge sums of money on research and development of new equipment. Therefore, the products that are just launched into the market do not make money and can only earn money from subsequent replacement and service markets. This means that the profit margin of the aviation aftermarket is very high, and to reduce costs, airlines have an incentive to purchase some of the replaceable and unprotected spare parts from third-party suppliers.

Heico is responsible for the aviation aftermarket third-party spare parts. It uses imitation instead of original equipment for imitation, with lower development costs, cheaper prices, and qualified quality. It requires authorization from the U.S. Aviation Administration.

In the downward economic cycle, airlines need to further reduce costs, which gives Heico greater opportunities. For example, Heico's component prices are 20-30% cheaper than Boeing/Airbus's original parts, and most of its components are below USD 5,000. Therefore, many airlines are willing to purchase from Heico.

It is worth noting that industry demand is very stable because airplanes are not grounded or maintained less frequently due to fewer flights. These parts need to be regularly maintained and do not depend on how many times the plane has flown, so customer demand is very strong.

However, because these aviation parts do not have patent protection, they may face competition from peers, which requires speed and quality. According to Heico's disclosure, it has delivered 83.52 million parts without any quality accidents, saving clients USD 2 billion in purchasing costs.

The characteristics of this industry are that the barriers to entry are high because they are strictly regulated by aviation management. This makes the industry less concentrated and has many merger opportunities. According to statistics, there are more than 2,300 aviation parts manufacturers active in their respective sub-sectors in the United States.

In the past 34 years, Heico has carried out 98 M&A transactions with USD 5 billion and only divested 2 assets, with an annualized return rate of 22%.

In addition to after-sales service business for components, Heico's second business is defense military components, many of which are used in various high-tech weapons of the US Army, Navy, and Air Force, including missiles, drones, satellites, with high technical and political barriers.

In addition, due to the continuous increase in US defense spending in recent years, the military industry business has served as a hedge and protective effect for Heico. For example, in 2020, due to the large number of airplanes grounded due to the epidemic, affecting the after-sales parts business of airplanes, but fortunately, the defense components business maintained growth, offsetting the impact of the decline in airplane parts sales.

What's even more interesting is that Heico Aviation employees have made more money on their own stocks than they have in the company, with more than 400 employees' US 401K retirement accounts having company stock assets of over a million dollars.

Going back to why Buffett wanted to buy, it's actually hard to understand. You should know that Buffett never buys stocks with a super high PE ratio, or let's say buying Heico Aerospace and Defense was not his idea.

Looking at the P/E ratio, Heico Aerospace's market cap is $32.8 billion, and the company may earn $0.45 billion this year, corresponding to a P/E ratio of at least 70 times.

Due to the company's many M&A cases, the amortization expense reduces the accounting profit, and there is another valuation method on the market. The company's free cash flow has been higher than the accounting profit in recent years, and if the amortization expense is added back, the profit will be higher and the valuation will be relatively low.

If calculated based on the free cash flow of 600 million in 2024, the current dynamic valuation of the company's free cash flow is around 54 times. But even so, this is not cheap.

Conclusion

In addition to expensive valuation, Heico Aerospace's military industry business has also attracted considerable attention from the market.

In previous articles, we analyzed the significant increase in military spending by the United States, G7, and NATO countries in recent years, which is a signal worth noting. Meanwhile, Japanese military industry stocks have already risen significantly, or it is because they see the potential for future military industry?

Editor/Somer