After the highly anticipated release of US CPI data in July, Wall Street traders increased their bets that Fed officials would cut interest rates by 25 basis points in September, while expectations for a direct 50 basis point cut cooled slightly.

On August 15th, Caixin learned that after the highly anticipated release of US CPI data in July, investors in the US bond market increased their bets that Fed officials would cut interest rates by 25 basis points in September, while expectations for a direct 50 basis point cut cooled slightly.

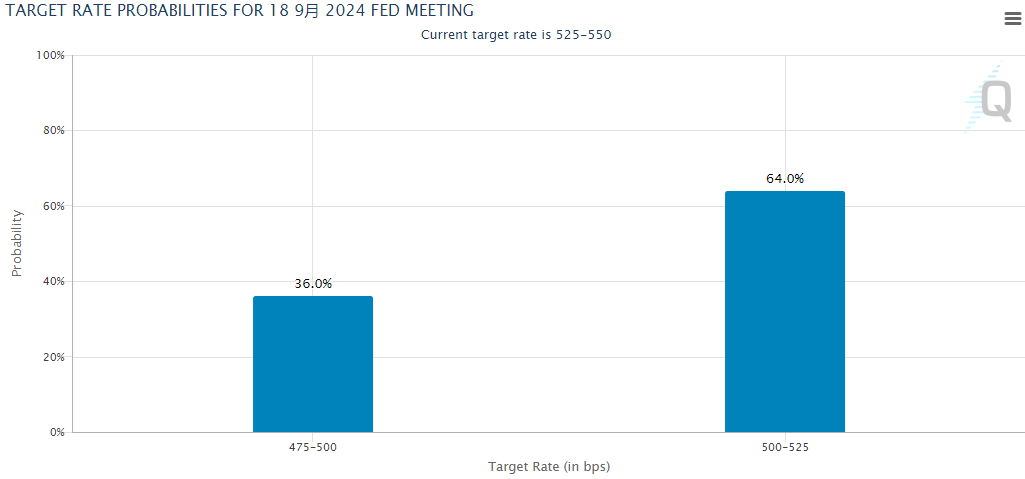

The pricing of the interest rate swap market shows that traders have priced in the latest interest rate cut on the Fed's September meeting for 32 basis points (leaning towards 25 basis points) overnight. CME Group's Fed Watch Tool also shows that the probability of a 25 basis point cut in the Fed's interest rate at the meeting has risen to 64%, while the probability of a 50 basis point cut is only 36%.

Earlier this week, the probability of a 25 and 50 basis point interest rate cut in September was almost 50/50.

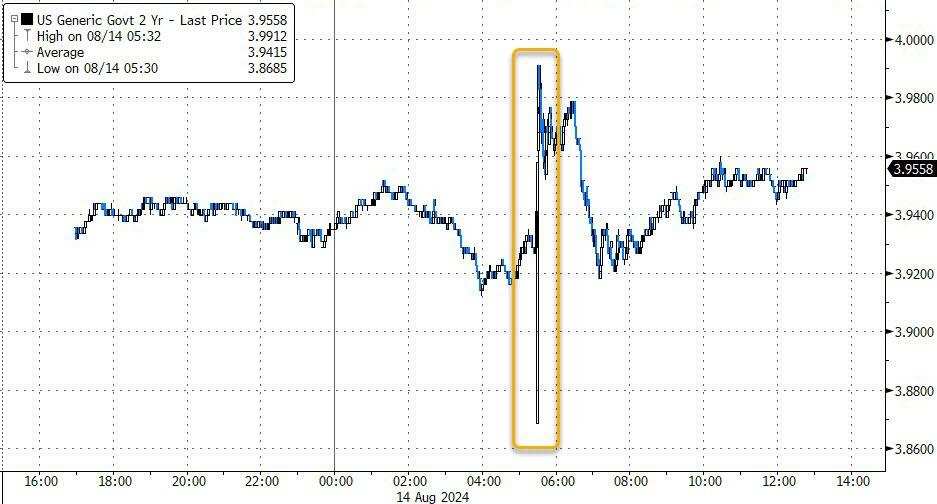

Looking back at the performance of the overnight US bond market, the market fluctuated greatly after the release of CPI data. The two-year Treasury yield experienced a "elevator" situation with fluctuations of more than ten basis points in a short period of time, but ultimately failed to break through the 4% threshold.

By the end of the New York session, yields on US bonds of various maturities rose or fell. Among them, the two-year Treasury yield rose 2.8 basis points to 3.97%, the five-year Treasury yield rose 0.6 basis points to 3.684%, the ten-year Treasury yield fell 0.9 basis points to 3.84%, and the thirty-year Treasury yield fell 3.4 basis points to 4.129%.

David Kelly, the Chief Global Strategist at J.P. Morgan Asset Management, said in an interview that the CPI data confirms that inflation concerns are fading because the data is close to expectations, so investors are starting to sell based on the fact that bond markets are now in this situation.

In Wednesday's trading, the options flow data pegged to the overnight secured financing rate (which closely tracks the central bank's policy path) showed that many traders closed positions of bets for a 50 basis point interest rate cut. Since the pricing of the swap market tended towards a 25 basis point cut instead of a direct 50 basis point cut, other related traders appeared to have adjusted their dovish bets.

Data released by the US Bureau of Labor Statistics on Wednesday showed that US CPI was up 2.9% year-on-year in July, falling below 3% for the first time since 2021. The core CPI, which excludes volatile food and energy prices, rose 3.2% year-on-year and 0.2% month-on-month.

This report may give the Fed sufficient reason to start cutting interest rates at its next meeting on September 17th-18th. The PCE price index, the Fed's favorite inflation indicator, which will be released later this month, has been moving closer to the Fed's target of 2%, and Fed Chairman Powell has hinted that the Fed is likely to cut interest rates in September.

Of course, in the latest CPI report, inflation in certain core service categories, including housing rent and car insurance, remains high. This is also why many industry insiders are more inclined to support a 25 basis point interest rate cut overnight. However, it can be foreseen that although people's expectations for a 25 basis point interest rate cut are higher, the CPI data itself may not be enough to put this issue to rest. The data performance of the current employment market may be more indicative of how much interest rates will be cut.

Lindsay Rosner, multiple department fixed income director at Goldman Sachs Asset Management, said that the inflation data "clears the way for a 25 basis point interest rate cut in September, but also does not completely eliminate the possibility of a 50 basis point cut."

Neil Sutherland, investment portfolio manager at Schroeder Investment Management, pointed out, "We are indeed seeing a weaker labor market. When the market discusses the scale of the Fed's interest rate cut in September, labor market data may make us clearer."

Nick Timiraos, a well-known reporter known as the "New Fed Communication Agency," said after the CPI data was released on Wednesday that the July CPI had paved the way for the Fed to lower interest rates at its September meeting. He expects the discussion focus of the September Fed meeting to be on the scale of the interest rate cut, either a traditional 25 basis point cut or a larger 50 basis point cut. The reason why the scale of the interest rate cut may become the focus of the discussion is that the US labor market has recently shown potential signs of weakness, but the inflation data released on Wednesday did not resolve this debate.

Timiraos also believes that this debate may ultimately be decided by labor market reports, including the weekly initial jobless claims and the August non-farm payroll report to be released on September 6th. If a 50 basis point interest rate cut is to be made, it depends on whether there are poor conditions in the labor market.

Austan Goolsbee, Chicago Fed President, said on Wednesday that he is increasingly concerned about the labor market rather than inflation, given recent progress on pricing pressure and disappointing employment data. He declined to comment on the likelihood and scale of the Fed's interest rate cut at its September meeting.

Editor/Somer