After the last CPI release caused a significant market turning point, will there be another big trend this time? What preparations do investors need to make? Without further ado, we inform you through an illustrated and condensed version of the US CPI data preview.

Before we start looking ahead to tonight's US CPI data, let's take a look at two charts.

The first chart shows the trend of the Nasdaq, which shows that the US stock market, especially tech stocks, experienced the biggest turning point of the year on July 11th after reaching its peak.

The second chart shows the trend of the USD/JPY, which shows that the source of the recent rally of the Japanese yen or the global arbitrage trading purge storm actually happened on July 11th.

As for what happened on July 11th, I believe that everyone is no stranger to it: the last US CPI release day.

What happened on that day? And what triggered a series of cross-asset price reactions from the stock market to the foreign exchange market, we have repeatedly reported in previous articles and will not go into details here. The focus tonight is that after the last CPI release caused a significant market turning point, will there be another big trend this time? What preparations do investors need to make?

Without further ado, we'll let you know these through an illustrated and condensed version of the US CPI data preview:

How is the market expectation for tonight's CPI data?

Let's take a look at Wall Street's expectations for tonight's CPI data:

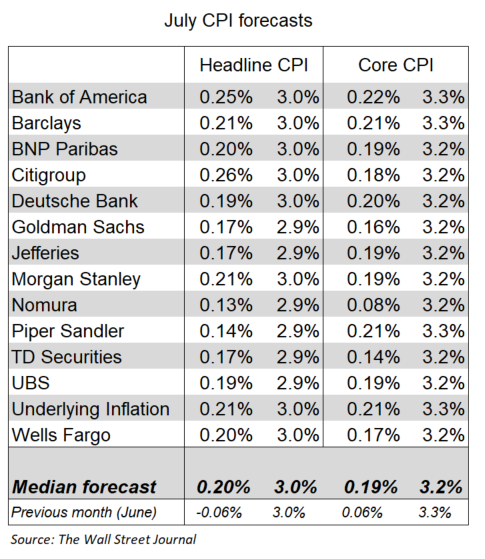

After June’s unexpected decline in CPI, the economic analysts of institutions surveyed by the media currently predict that the overall CPI in July is expected to rise by 0.2% from the previous month (higher than the decline of -0.1% in the previous month), and the year-on-year rate is expected to increase by 2.9% (lower than that of June, which was 3.0%).

Excluding the easily-volatile energy and food prices, the core CPI in July is expected to rise by 0.2% from the previous month (higher than the previous increase of 0.1%), and the year-on-year rate is expected to increase by 3.2% (lower than the previous increase of 3.3%).

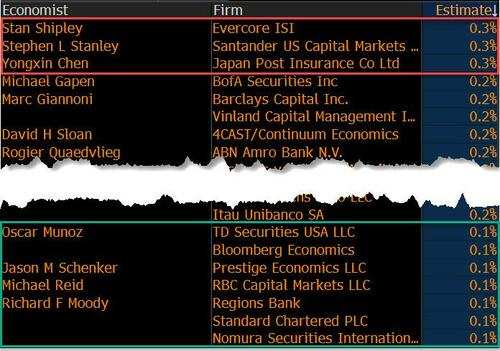

Among the four data sets, the core CPI month-on-month rate is the most concerned about, and the distribution of the current institution survey is as follows:

Among the 66 analysts interviewed by the media, only three analysts expect the core CPI in July to increase by 0.3% compared to the previous month. Seven analysts expect a month-on-month increase of 0.1%, while the remaining analysts expect a month-on-month increase of 0.2%.

It is worth noting that before tonight, the US core CPI month-on-month data has appeared for three consecutive times with actual published values lower than the market's estimated value-this is the longest such experience since the outbreak of the COVID-19 crisis. Whether this scene will continue tonight is worth paying attention to.

In addition, another highlight of tonight’s data is whether the year-on-year CPI increase in July can be slightly lower than expected, and re-enter the "2 era" (2.9%) after more than three years. If this scene really appears, it may become a "spot" in the market.

According to the bank forecasts compiled by "New Fed Communications" Nick Timiraos, major Wall Street institutions predict a CPI year-on-year rate of either 3.0% or 2.9%, so the probability of the data finally falling to 2.9% is not small.

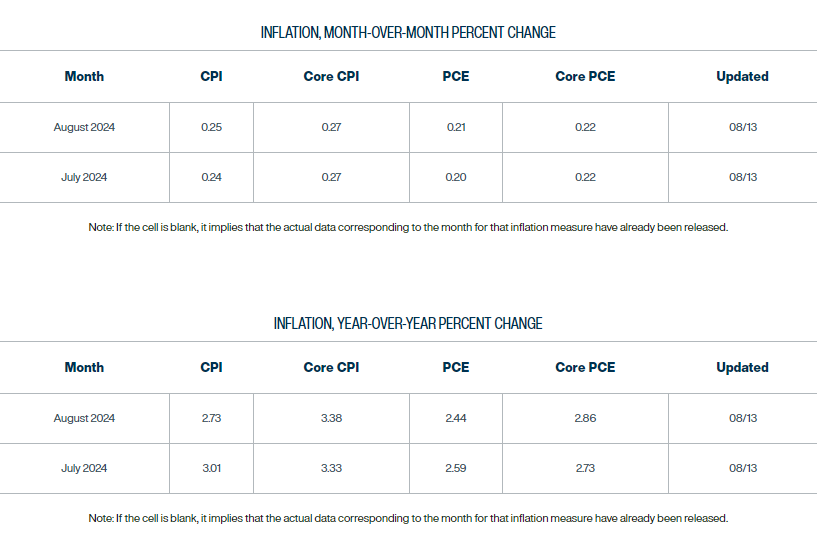

However, as another reference, the inflation prediction model of the Cleveland Fed shows that the overall inflation rate in July may rise by 0.24% from the previous month, and the year-on-year rate may rise by 3.01%; the core CPI may rise by 0.27% month-on-month and 3.33% year-on-year. This indicates that the Cleveland Fed's model believes that tonight's data may have upward risks compared to the market's general expectations.

How will investment banks specifically analyze tonight's data?

Let's quickly take a look at the specific analysis of tonight's data by major investment banks.

First of all, Bank of America believes that due to the rebound in core service inflation and energy prices, the overall CPI in July is expected to rise by 0.25% (unrounded), and the year-on-year rate is expected to remain unchanged at 3.0%; the bank also expects that the month-on-month core CPI will rise by 0.22% (unrounded). The bank believes that although this inflation data is not as low as the June report, it is generally consistent with the previous trend of inflation decline and should be able to trigger the Fed's interest rate cut starting in September.

In terms of core service inflation, Bank of America pointed out that due to the decline in air ticket prices, core service inflation in June, which does not include rent and owner-equivalent rent (OER), fell slightly, but the bank expects the decrease in air ticket prices in July to decrease. In addition, housing prices should rebound, but the deceleration of rent and owner-equivalent rent (OER) is expected to remain unchanged.

Goldman Sachs' view is more dovish. It is expected that core CPI will rise by 0.16% month-on-month and 3.20% year-on-year. The bank also expects CPI to rise by 0.17% month-on-month and 2.93% year-on-year in July. The bank emphasized the trends of the four key components expected to appear in this month's report:

First, the bank expects prices of used cars (-1.5%) and new cars (-0.1%) to further decrease in July. Currently, the auction price of used cars has dropped by 26% from its peak, while the price of used cars in the CPI composition has only dropped by 18%, indicating that there is still room for further decline in the classified indicators of the CPI report.

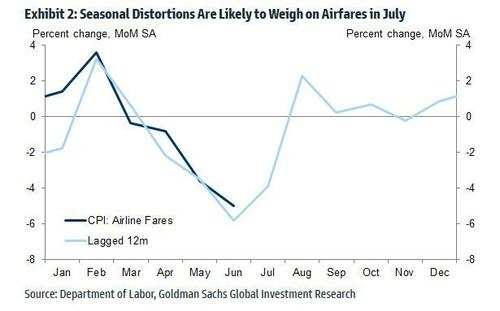

Secondly, the bank expects air ticket prices to drop by 2.5% in July, following a substantial decline in June, reflecting the sustained adverse factors brought by seasonal distortions.

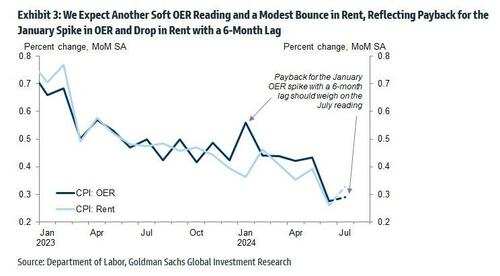

Thirdly, Goldman Sachs expects the equivalent rent OER (+0.29%) of the owner to grow again moderately, and the main rent will rebound slightly (+0.33%), reflecting the impact of the surge in OER and the decline in rent (6 months) lagging behind. However, looking ahead, Goldman Sachs believes that the strong growth of single-family home rents is likely to lead to a rise in OER beyond rent.

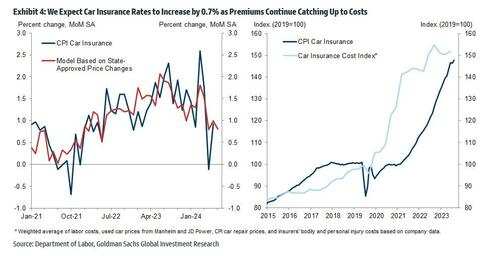

Fourthly, the bank expects car insurance prices to rise, but the rate of increase will not be as quick as it was at the beginning of the year: the expected increase in car insurance is 0.7%, while the average increase so far in 2024 is 1.2%. Rising car prices, maintenance costs, and rising medical and litigation costs have all brought price pressure to insurance companies, but the transfer of premiums to consumers has a long lag period, partly because insurance companies must negotiate price increases with state regulatory agencies.

How will data affect financial markets tonight?

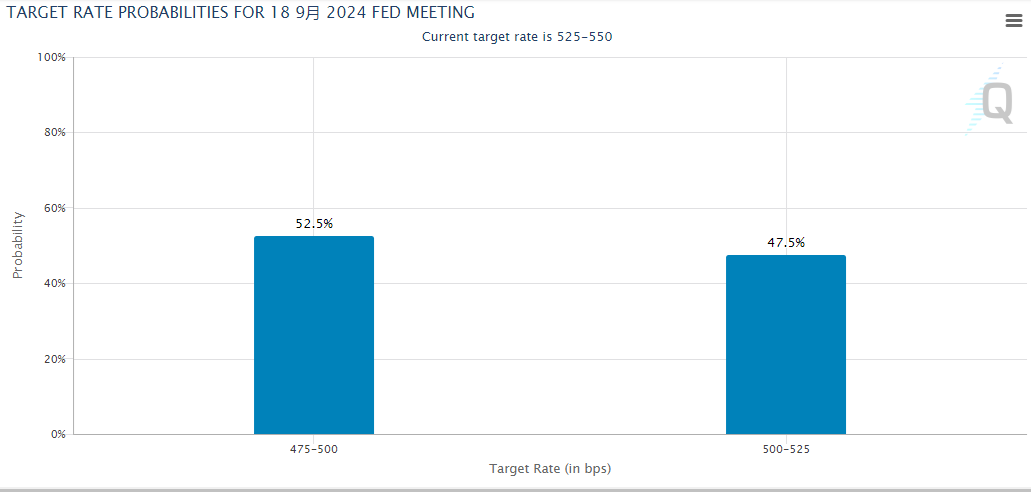

According to CME Group's FedWatch tool, the probability of traders predicting that the Fed will cut rates by 50 basis points in September is about 52%, and the probability of cutting rates by 25 basis points is 48%.

Given that it is almost 50-50 whether the Fed will cut rates by 25 or 50 basis points in September, the good or bad of tonight's CPI data will obviously affect the change of this "balance".

As for the foreign exchange, bond, and precious metal markets, the impact of tonight's CPI data on market trends is undoubtedly easier to judge. If the data is higher than expected, it will obviously be good for the dollar, push up US Treasury yields, and be bearish for gold. Otherwise, if data is lower than expected, it may be bearish for the dollar, push down US Treasury yields, and then be bullish for gold.

What is relatively difficult to judge is actually the trend of US stocks. Last time, when CPI data was lower than expected, it should have been beneficial to US stocks, but on that day, a wave of rotation swept the market after a brief surge, and the largest tech giants by market value suffered a major decline, dragging down the performance of the stock index.

And tonight, whether similar rotation will occur is actually a question mark. This is because the intensification of the risks of economic recession in the United States has undermined the foundation of rotation to a large extent. Originally, it was expected that interest rate cuts under the background of economic stability would benefit a series of small-cap stocks and value stocks that benefit from the economic growth cycle, but if interest rate cuts are due to a sudden turn for the worse in the economic outlook, then this underlying logic cannot stand.

From the current judgment of investment banks, tonight's judgment will be mainly based on the traditional logic that 'lower-than-expected inflation data will be beneficial to US stocks.' The following figure shows the potential rise and fall of the S&P 500 index under different core CPI month-on-month performances expected by Goldman Sachs tonight:

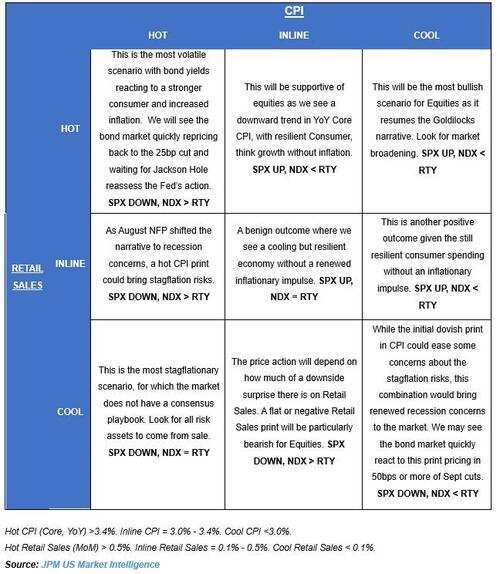

Morgan Stanley, which has predicted the impact of CPI on the market almost every time, ‘creatively’ combines the performance of tonight's CPI data and Thursday's retail sales data for analysis. The following figure shows all the scenarios predicted by the bank:

CPI YoY>3.4%, retail sales MoM>0.5%: This is the most unstable situation, and bond yields will respond to stronger consumers and higher inflation rates. We will see the bond market quickly re-pricing, returning to betting on a 25 basis point rate cut in September, and waiting for the Jackson Hole global central bank annual meeting to re-evaluate the Fed's actions. In this scenario, the S&P 500 index will fall, NDX>RTY (the Nasdaq 100 outperforms the Russell 2000);

CPI YoY>3.4%, retail sales MoM falls between 0.1% and 0.5%: the hot CPI data may bring stagflation risks due to the market's shift to concerns about economic recession after the non-farm employment data at the beginning of this month. In this scenario, the S&P 500 index will fall, NDX>RTY;

CPI YoY>3.4%, retail sales MoM<0.1%: This is the most "stagflationary" situation, and the market has no consensus on this. If this happens, all risk assets will be sold. In this scenario, the S&P 500 index will fall, and NDX=RTY (both perform equally).

If CPI YoY falls between 3.0%-3.4% and retail MoM is greater than 0.5%, it will support the stock market. As we can see core CPI MoM is trending downwards, consumer confidence is recovering, and economic growth is expected to occur without inflationary pressures. In this context, the S&P 500 index will rise, and NDX will follow suit.

If CPI YoY falls between 3.0%-3.4% and retail MoM falls between 0.1%-0.5%, it will be a benign result and we will see a resilient economy. There won't be another inflationary impulse. In this context, the S&P 500 index will rise, and NDX=RTY.

If CPI YoY falls between 3.0%-3.4% and retail MoM is less than 0.1%, the movement of stock prices will depend on the degree of unexpected retail sales decline. Flat or negative growth in retail sales will be particularly unfavorable for the stock market. In this context, the S&P 500 index will fall, and NDX>RTY.

If CPI YoY is less than 3.0% and retail MoM is greater than 0.5%, it will be the most bullish scenario for the stock market, as it will resemble the story of Cash Girll. Market gains are expected to expand. In this context, the S&P 500 index will rise, and NDX will follow suit.

If CPI YoY is less than 3.0% and retail MoM falls between 0.1%-0.5%, it will be another positive outcome as consumer spending still has elasticity and there won't be any inflationary impulse. In this context, the S&P 500 index will rise, and NDX will follow suit.

Although the initial fall of CPI may ease some concerns about stagflation risk, this combination will bring new recession worries to the market. We may see the bond market react quickly to this data, betting on a 50 basis point or more rate cut in September. In this context, the S&P 500 index will fall, and NDX will follow suit in this context.

Editor/Lambor