Looking at August, the demand for deep processing still maintains above 4.4 million tons, but there is limited imported-to-domestic arbitrage space, and currently high import costs will constrain the trend of import volume growth to the port.

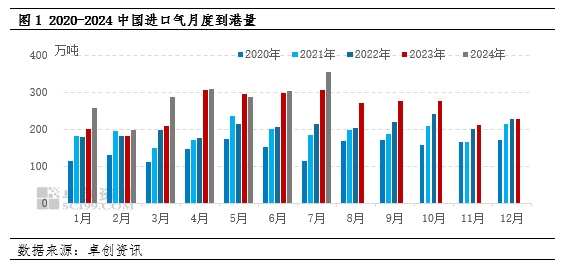

In July 2024, the arrival volume of VLGC was 3.557 million tons, an increase of 17.20% month-on-month, mainly affected by factors such as import costs and start-up of deep processing facilities. Looking at August, industrial demand is expected to remain at a high level, and it is expected that the arrival volume in August will remain high.

In July, the arrival volume increased by 17.20% month-on-month.

According to the ship scheduling data of Zhuochuang Information, in July 2024, China's frozen cargo arrived at a volume of 3.557 million tons, an increase of 0.522 million tons from June 2023, a year-on-year increase of 17.20%; from the perspective of July 2024 data, the arrival volume increased by 0.487 million tons, a month-on-month increase of 15.86%.

Production load has increased, but inventory still needs to be digested.

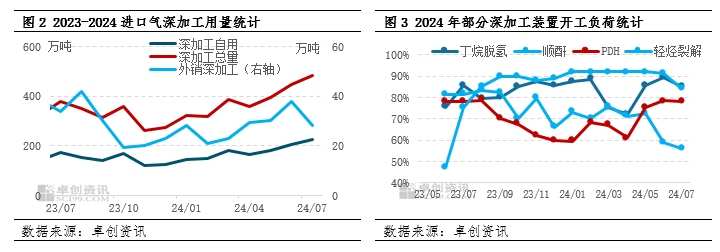

According to the statistics of Zhuochuang Information, from the perspective of the load of the hydrocarbon deep processing unit, the load of butene dehydrogenation in July was 85.53%. The load of PDH unit was 78.1%. The load of adipic acid unit was 55.92%. Light hydrocarbon cracking still maintained 84.03%. The deep processing start-up load in July maintained a high level of operation, and with the addition of new production capacity, the demand for deep processing increased significantly compared with the previous period.

Deep processing profitability is poor, and sales arbitrage performance is average.

As of July 29th, the average gross profit per ton of China's PDH unit this month was -268 yuan/ton, and the theoretical gross profit increased compared with June, with a narrowing of negative levels. In July, the international CP price remained the same as in June, but due to a slightly lower discount, the propane import landed price was also slightly lower than in June. In addition, in July, the domestic propylene price performed strongly, with an average slightly higher than in June. The theoretical profit of PDH plant also received certain repair and improvement. As of July 29th, the theoretical calculation of import arbitrage for this period by Zhuochuang Information was an average of 10 yuan/ton. The average national import gas external sales price for this period was 5071 yuan/ton, an increase of 9 yuan/ton from the previous period, and an increase of 0.18%. Internationally, Saudi Aramco announced its July CP, with propane and butane unchanged from June. Propane was $580/ton and butane was $565/ton, equivalent to an import landing cost (excluding wharf operation fees) of around 4900 yuan/ton. The import landing cost remained at a high level. Domestically, this month's domestic import volume is expected to exceed 3.5 million tons, a new high for the year, but the main refinery civilian gas external output is low, and the international market trend is strong, so there is no strong willingness to sell at a low price. This month's domestic import gas prices have been consolidating mainly horizontally, and the price is close to the import cost line, and the import arbitrage space has shown a slight opening state.

Import costs have not changed much, and port inventories have increased.

In July, Saudi Aramco announced that propane and butane were unchanged from the previous month. Propane was $580/ton, unchanged from the previous month; butane was $565/ton, unchanged from the previous month. Propane is estimated to be around 4998 yuan/ton, and butane is estimated to be around 4740 yuan/ton. The CP is finally the same as the previous month, slightly lower than the paper market level on Friday. At the end of June, due to the strong overall performance of crude oil in June, the paper market prices have risen somewhat, but the overall market is still low in terms of negative levels, indicating that the market is not very tight, and the absolute values of price increase are mostly due to the strong performance of crude oil driving the price of liquefied gas. Of course, the market also has certain demand, mainly the continuous maintenance of PDH start-up above 75% and the demand for far-east ethylene to support the international market price of LPG. However, the combustion market is in the off-season of demand, and the demand is weak. This is also an important reason for the obvious, low price of butane. From the perspective of port inventory, due to the optimistic view of the future market by some industry participants, purchasing enthusiasm was good in July, and some industry participants had a hoarding mentality, leading to an increase in port inventories.

The expected arrival volume in August is slightly reduced.

The expected arrival volume in August is slightly reduced compared with July, and deep processing demand is still maintained above 4.4 million tons in August, but the arbitrage space for import to domestic trade is limited, and the current import cost is high, which will constrain the growth trend of import volume. It is expected that the import volume in August will decrease slightly compared to July, with an expected volume of around 3.3 million tons.