In recent years, the "institutional holding shares" of $CHINA MOBILE (00941.HK)$ / $China Mobile Limited (600941.SH)$Please use your Futubull account to access the feature.$CHINA TELECOM (00728.HK)$ / $China Telecom Corporation (601728.SH)$Please use your Futubull account to access the feature.$CHINA UNICOM (00762.HK)$ / $China United Network Communications (600050.SH)$ have been rising all the way since they met on the A-share market on January 5, 2022.

China Mobile A-share rose by more than 90%, while Telecom and Unicom performed relatively weaker, but the three major operators in Hong Kong all rose by more than 75%.

On this rising trend line, the institutions went from watching coldly to swarming in and using a lot of money to "favor" the operators.

But there are different "scenery" among them, with some people repeatedly "jumping", some people repeatedly "rebalancing" in AH shares, and some veterans who started to lay out 10 years ago.

On August 8th, China Mobile, one of the three major operators, announced the 2024 semi-annual report and the 2024 mid-term profit distribution plan ahead of others.

As shown in the mid-year report, China Mobile's operating income in the first half of 2024 was 546.7 billion yuan, a year-on-year increase of 3%, and net profit attributable to the parent was 80.201 billion yuan, a year-on-year increase of 5.3%; free cash flow was 67.4 billion yuan.

The mid-term dividend was HK$2.60 per share, a year-on-year increase of 7.0%. As of June 30, 2024, a total of HK$557.51 in mid-term dividends will be distributed (including tax), equivalent to approximately 51.3 billion yuan.

The quality of dividend assets is still good.

We have heard different asset managers talk about their early layout of the operators on different occasions.

Especially when talking about the recent outstanding performance of private equity managers, including Xinpu, Jingrui, Ruijun, Bisheng, etc., China Mobile is almost a must-talk target.

These institutions have been lurking in the market far earlier than the market, with different perspectives, but they have all benefited from a "reasonable account".

From the perspective of the most easily researched information, we have sorted out the situation in which the three major operators were held by public funds in the past three years and looked at the fund managers who are betting heavily on them.

01 Three major operators that have been continuously buying up by institutions in the rising stock market.

Since the establishment of our country, the telecommunications business has been under the management of the state. At that time, the Posts and Telecommunications Department was established, which also became the predecessor of China Telecom.

In the 1990s, in order to promote the market-oriented reform of the telecommunications business, China Telecom was officially established in 1994, and the company almost monopolized the fixed and mobile telecommunication network business during that period.

China Unicom, which was established at the same time, posed no "threat" to it.

In 1999, in order to break the monopoly of China Telecom, two split and reorganizations happened. The first time in 1999, the mobile network business (GMS network) was split into China Mobile. At the same time, the paging business was split into China Unicom Paging, the satellite communication business was split into China Satellite Communications, and China Telecom retained the original fixed network business. The second time in 2001, the split was made according to the northern and southern regions. The fixed network business of 10 provinces in the north was split up and added to Netcom and Jitong Company to form China Netcom. The fixed network business of the remaining 21 provinces was retained by China Telecom. So far, China's telecommunications industry is dominated by China Telecom, China Netcom, and China Tietong (established in 2004) in the fixed network field, while China Mobile and China Unicom mainly occupy the mobile network business. China Satcom is in the field of satellite communication.

In 1999, the mobile network business (GSM network) was split into China Mobile. At the same time, the paging business was split into China Unicom Paging, the satellite communication business was split into China Satellite Communications, and China Telecom retained the original fixed network business.

At the same time, the paging business was split into China Unicom Paging, the satellite communication business was split into China Satellite Communications, and China Telecom retained the original fixed network business.

The second split was made in 2001 according to the northern and southern regions.

The fixed network business of 10 provinces in the north was split and added to Netcom and Jitong Company to form China Netcom. The fixed network business of the remaining 21 provinces was retained by China Telecom.

So far, China's telecommunications industry is dominated by China Telecom, China Netcom, and China Tietong (established in 2004) in the fixed network field, while China Mobile and China Unicom mainly occupy the mobile network business. China Satcom is in the field of satellite communication.

Since the popularity of mobile internet began in 2003, China Mobile, which had a natural advantage in mobile network business, took the lead. By the end of 2005, it had more than 200 million mobile network customers. At that time, China Unicom had only over 30 million previous customers.

In 2008, in order to further balance the strength of the operators, China Tietong was merged into China Mobile (mobile network business obtained), China Unicom merged with China Netcom (fixed network business obtained), and China Unicom transferred its CDMA network to China Telecom (mobile network business obtained). Thus, the pattern of the three major operators was officially formed, and the Ministry of Industry and Information Technology also issued 3G licenses to the three companies at the end of the year.

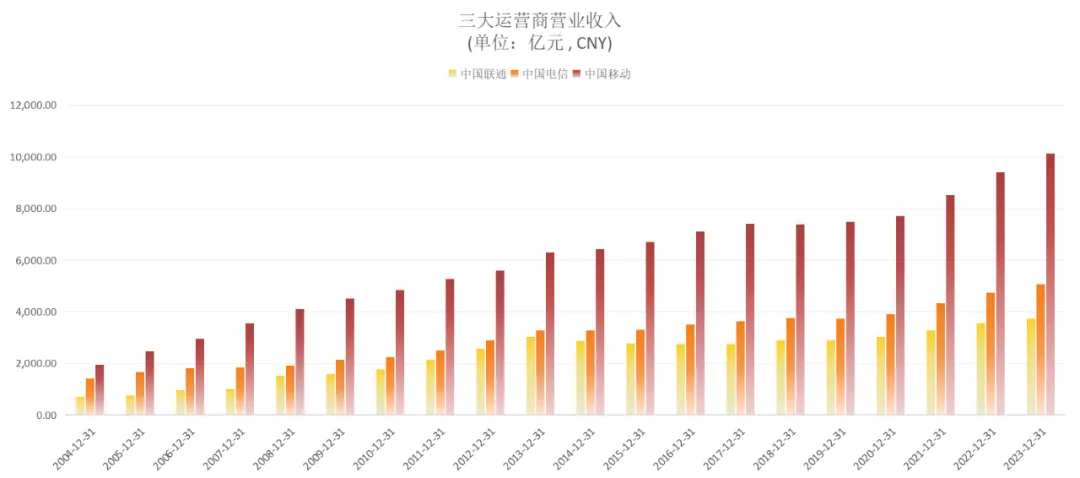

It can be said that China Mobile, as the largest operator, cannot be ignored in later efforts. However, since its establishment, it has had a natural advantage in mobile internet and still maintains a leading position. In terms of the quality of the company, the main financial data such as revenue and net profit of the three major operators are stable, especially China Mobile's operating income exceeded one trillion yuan for the first time in 2023.

Data source: Wind as of December 31, 2023

Data source: Wind as of December 31, 2023

Data source: Wind as of August 9, 2024

Data source: Wind as of August 9, 2024

China Unicom in 2023 was not a "big surprised", with Hong Kong stocks rising by more than 34% in 2022, and a big increase of 30% this year, with institutions increasing their holdings in the second quarter.

Since the three major operators have all been listed on A shares, although they were uniformly reduced by institutions in the second quarter of 2022 and the fourth quarter of 2023, the proportion of institutional holdings has always been on the rise.

In fact, even before the three major operators returned to A shares, they had already been favored by institutional investors.

On May 7th, 2021, the three major operators, China Mobile, China Unicom, and China Telecom, announced that they would delist from the United States. On January 5th, 2022, China Mobile returned to A shares.

Thus, the three major operators officially met on A shares.

It was also at this time that the trend of dividend assets slowly unfolded.

Bao Wuke had been holding positions on China Mobile for 22 quarters.

China Mobile, China Telecom, and China Unicom were all listed on US and Hong Kong stocks in the early 21st century.

Compared with China Mobile and China Telecom, which returned to A shares in the past two years, China Unicom was listed on A shares as early as 2002.

In 2003, the three major operators followed the "Five Golden Flowers" to make a breakthrough.

By the end of 2003, China Unicom's A-share stock was the heaviest in a single fund, which was Huaxia Growth Hybrid, a star product of Huaxia Fund at that time. The fund manager in charge was the well-known Wang Yawei.

The second and third heaviest stocks were Penghua Hongtai Hybrid and Harvest Fenghe Fund.

In 2006 and 2007, the Hang Seng Index continued to set new highs. At the end of 2007, QDII funds were officially established, and the Hong Kong stocks of the three major operators began to be heavily bought, but the positions were not many.

Until the end of 2014, after the Hong Kong Stock Connect was opened, we saw many familiar names in institutional holdings.

During this period, China Unicom's A-share stock has always been heavily held by institutions, but has rarely received attention from actively managed funds. Passive index products hold more positions on it.

Among them, Bao Wuke should occupy a place of affection for the operators the longest.

As of the second quarter of 2024, Bao Wuke held positions on China Mobile for 22 quarters.

At the end of the third quarter of 2016, Bao Wuke first heavily bought shares of China Mobile (listed in Hong Kong), which was a small bottom of China Mobile's share price volatility at that time. In the fourth quarter, Bao Wuke added a large amount of positions in China Mobile (listed in Hong Kong) while it dropped by 12%, and also bought China Unicom (listed in Hong Kong) which only fell by 3% in the quarter. In the first quarter of 2017, Bao Wuke bought China Telecom (listed in Hong Kong) again, while adding positions in China Mobile (listed in Hong Kong) and China Unicom (listed in Hong Kong), and then continuously reduced positions. By the end of 2017, its holdings in China Mobile and China Unicom listed in Hong Kong had all been liquidated. Since then, Bao Wuke has been slightly reducing its holdings in China Mobile (listed in Hong Kong) until the third quarter of 2018, and then liquidated them after a brief heavy position. Interestingly, the CSI Dividend Index outperformed the CSI 300 Index from March 2015 to May 2020. From the market of 2018, the Hang Seng Index hit a stage high of 33,484.08 points on January 29, 2018. Since then, the Hang Seng Index has been shaking and falling, and the stock prices of the three major operators (listed in Hong Kong) all fell by more than 10% in 2019. In hindsight, Bao Wuke's operation was quite accurate. In 2018, when the CSI 300 Index fell by 25.31%, the Invesco Great Wall Shanghai, Hong Kong, and Shenzhen Selection Fund managed by Bao Wuke had a yield of -12.42%. In the annual report of that year, Bao Wuke stated that he focused on buying and holding stocks with high business barriers and relatively cheap valuations, and that the Hong Kong stock market had a lower valuation and he discovered many investment opportunities in this market. Until the end of 2020, Bao Wuke once again increased its holdings of China Mobile (listed in Hong Kong), and has been heavily holding it since then. At that time, the stock price was almost the lowest since 2010. In the years 2019-2020 without heavy positions in the three major operators, Sichuan Chuantou Energy, China South Publishing & Media Group, and other undervalued and high dividend targets were the favorites of Bao Wuke. In the first quarter of 2022, China Mobile was listed on the A-share market, and Bao Wuke bought 2.07 million shares, with a market value of 0.138 billion yuan. In the second quarter of 2021, Bao Wuke also heavily bought shares of China Telecom (listed in Hong Kong), and increased positions in China Telecom (listed in A-share market) in the third quarter of 2022. In 2023, the stock prices of the operators skyrocketed, which was also one of the reasons for the net value of Bao Wuke's products to repeatedly hit new highs. Tasting the sweetness of nearly 30% rise in the past quarter, institutional investors began to heavily increase their positions. Bao Wuke began to take profits in the second quarter of 2023 and then reduced positions in the following two quarters. He said, 'For companies like Mobile and Telecom, their stock prices have risen sharply and their valuations are no longer as excessively undervalued as before. They are now at a reasonable valuation level, and their investment value will definitely decline significantly.' In the first quarter of 2024, Bao Wuke greatly reduced positions in China Mobile (listed in A-share market) and increased positions in China Mobile (listed in Hong Kong), but by the end of the second quarter, the three major operators had all exited the top ten heavy weight stocks in its managed funds.

In the fourth quarter, Bao Wuke added a large amount of positions in China Mobile (listed in Hong Kong) while it dropped by 12%, and also bought China Unicom (listed in Hong Kong) which only fell by 3% in the quarter.

In the first quarter of 2017, Bao Wuke bought China Telecom (listed in Hong Kong) again, while adding positions in China Mobile (listed in Hong Kong) and China Unicom (listed in Hong Kong), and then continuously reduced positions. By the end of 2017, its holdings in China Mobile and China Unicom listed in Hong Kong had all been liquidated.

Since then, Bao Wuke has been slightly reducing its holdings in China Mobile (listed in Hong Kong) until the third quarter of 2018, and then liquidated them after a brief heavy position.

Interestingly, the CSI Dividend Index outperformed the CSI 300 Index from March 2015 to May 2020.

From the market of 2018, the Hang Seng Index hit a stage high of 33,484.08 points on January 29, 2018. Since then, the Hang Seng Index has been shaking and falling, and the stock prices of the three major operators (listed in Hong Kong) all fell by more than 10% in 2019.

In hindsight, Bao Wuke's operation was quite accurate.

In 2018, when the CSI 300 Index fell by 25.31%, the Invesco Great Wall Shanghai, Hong Kong, and Shenzhen Selection Fund managed by Bao Wuke had a yield of -12.42%.

In the annual report of that year, Bao Wuke stated that he focused on buying and holding stocks with high business barriers and relatively cheap valuations, and that the Hong Kong stock market had a lower valuation and he discovered many investment opportunities in this market.

Until the end of 2020, Bao Wuke once again increased its holdings of China Mobile (listed in Hong Kong), and has been heavily holding it since then. At that time, the stock price was almost the lowest since 2010. In the years 2019-2020 without heavy positions in the three major operators, Sichuan Chuantou Energy, China South Publishing & Media Group, and other undervalued and high dividend targets were the favorites of Bao Wuke.

In the first quarter of 2022, China Mobile was listed on the A-share market, and Bao Wuke bought 2.07 million shares, with a market value of 0.138 billion yuan.

At that time, the stock price was almost the lowest since 2010.

In the years 2019-2020 without heavy positions in the three major operators, Sichuan Chuantou Energy, China South Publishing & Media Group, and other undervalued and high dividend targets were the favorites of Bao Wuke.

In the first quarter of 2022, China Mobile was listed on the A-share market, and Bao Wuke bought 2.07 million shares, with a market value of 0.138 billion yuan.

In the second quarter of 2021, Bao Wuke also heavily bought shares of China Telecom (listed in Hong Kong), and increased positions in China Telecom (listed in A-share market) in the third quarter of 2022.

In 2023, the stock prices of the operators skyrocketed, which was also one of the reasons for the net value of Bao Wuke's products to repeatedly hit new highs.

Tasting the sweetness of nearly 30% rise in the past quarter, institutional investors began to heavily increase their positions.

Bao Wuke began to take profits in the second quarter of 2023 and then reduced positions in the following two quarters.

He said, 'For companies like Mobile and Telecom, their stock prices have risen sharply and their valuations are no longer as excessively undervalued as before. They are now at a reasonable valuation level, and their investment value will definitely decline significantly.'

In the first quarter of 2024, Bao Wuke greatly reduced positions in China Mobile (listed in A-share market) and increased positions in China Mobile (listed in Hong Kong), but by the end of the second quarter, the three major operators had all exited the top ten heavy weight stocks in its managed funds.

Looking at it in detail, most of Bao Wuke's purchases in China Mobile were at the low points during the volatility.

Moreover, from his past positions combined with quarterly reports, he actually chose the same types of companies, including the three major telecom operators.

In 2022, Liu Xu and Wang Pei were heavily positioned at the same time for "Walking to the Left and Walking to the Right".

On the morning of January 5, 2022, after a 24-year hiatus, China Mobile returned to the A-share market and broke the record for the largest fund-raising by A-shares in nearly a decade set by China Telecom in August 2021.

In the first quarter of 2022, China Mobile's AH shares were both increased.

The top three institutions that heavily bought into it at that time were Zhong Ou, Dacheng, and well-known private equity firm Ningquan Asset Management.

The fund manager for Dacheng's heavy position was Liu Xu, the fund manager for Zhong Ou's heavy position was Wang Pei, and the heavy position for Ningquan Asset Management was Yang Dong.

Liu Xu not only participated in the subscription, but also increased his position and purchased after China Mobile was officially listed.

As of the fourth quarter of 2022, Liu Xu's Dacheng high-tech industry fund was heavily positioned in China Mobile's AH shares at the same time.

Until the third quarter of 2023, China Mobile (A-shares) dropped out of the top ten heavy positions, while China Mobile (H-shares) was heavily positioned.

Liu Xu said: "Its (telecommunications stocks) valuation has already presented a very cheap state, and the company has a lot of money in its accounts, strong profitability, and a high industry status. In particular, companies in the communications sector are relatively defensive, with no significant fluctuations, and are a To C type."

Especially, communications companies are relatively defensive, with no significant fluctuations, and are a To C type.

Mainly heavily positioned in Hong Kong stocks, in his view, if the return rate, competitiveness and market capitalization of Hong Kong stocks and A-shares are compared, Hong Kong stocks still have competitiveness.

At the same time, Liu Xu said that he didn't make any significant adjustments, but rather shifted large amounts of A-shares to Hong Kong stocks.

In the second quarter of 2024, Liu Xu increased his position in China Mobile's (H-shares) again, while reducing his shareholding in China Mobile's (A-shares).

Looking at Liu Xu's overall position, he has almost eaten up China Mobile's growth in the past three years.

But the situation is different for Wang Pei of Zhong Ou Fund.

In the first quarter of 2022, he not only heavily positioned himself in China Mobile (A-shares), but also in China Mobile (H-shares), with a total market value of holdings reaching 1.192 billion.

Based on Wang Pei's past holdings, this move is inconsistent with his style.

Therefore, as of the end of the second quarter, Wang Pei directly cleared China Mobile (H-shares) and continued to significantly reduce his holdings of China Mobile (A-shares).

In the interim report, he wrote: 'The industrial opportunities brought by new technologies may be more in line with China's development direction and future industrial structure. In this context, investors need to have a deeper understanding of investment opportunities.'

However, it can be seen from Wang Pei's subsequent quarterly reports that his investment style and strategy have begun to change.

In the 2023 annual report, Wang Pei stated: 'The phenomenon of undervalued dominance has continued for two years, and whether in large-cap or small-cap value, it outperforms growth industries.'

At this time, Wang Pei quietly added some dividend assets.

In Q4 of 2023, Wang Pei heavily invested in China Telecom (A-shares), China Shenhua Energy, and made a small purchase of China Unicom (A-shares).

In the first quarter of this year, he further increased his holdings of China Telecom (A-shares) by 28 million stocks and reduced his holdings of China Mobile (A-shares).

By the second quarter, both China Telecom (A-shares) and China Mobile (A-shares) were reduced, but China National Offshore Oil and China National Offshore Oil were added to holdings.

He wrote in the quarterly report, 'The market's main line continues to revolve around high dividends, upstream resources, and technological innovation. We will focus on resource industries, low-priced consumer goods, aging, and technological innovation. At the stock level, we will actively seek out a group of companies that represent China's competitiveness to deploy.'

From the change in holdings, it is indeed changing according to the quarterly report description.

However, this time it crossed over from growth stocks, and compared to 2022, it was not as cost-effective in terms of buying prices. Looking at past performance, it ended with negative growth for two consecutive years.

From the adjustments made by mutual funds in the second quarter of 2024, they slightly increased their holdings of China Mobile's Hong Kong stocks and reduced their holdings of China Mobile's A-shares.

Data source: Wind as of August 9, 2024.

Jiao Wei, who always holds Baijiu (Chinese liquor), bought into China Mobile (A-shares) in the hidden core holding of Yin Hua Wealth Theme in the 2022 annual report, and continued to increase his holdings to nearly 9.7 million shares by the end of 2023.

Since the beginning of this year, Jiao Wei has reduced his holdings of China Mobile (A-shares) for two consecutive quarters.

China National Offshore Oil, which is also a dividend asset, was purchased by Jiao Wei in Q2 of 2022, when it rose all the way through 2023 and was bought in.

However, the rare thing is that he candidly admitted in the 2022 annual report: "The timing of the execution discount of shifting to high-dividend asset allocation is not good. This discount on execution should come from emotional interference."

Looking back, Ruifeng Fund has been a loyal holder of China Mobile (listed in Hong Kong) over the past three years.

Fu Pengbo's managed Ruiyuan Growth Value Fund started buying China Mobile (listed in Hong Kong) at the end of 2020, while Zhao Feng directly bought it as the second-largest holding in the first quarter of 2021.

In the first quarter of 2021, Fu Pengbo and Zhao Feng's two public funds collectively increased their holdings by nearly 70 million shares, with an increase amount of as high as RMB 2.806 billion (approximately HKD 3.351 billion), having a total market cap of China Mobile (listed in Hong Kong) worth over RMB 3.5 billion by the end of the first quarter.

In the quarterly report, Fu Pengbo wrote: "Public utilities, steel, leisure services and other sectors have relatively prominent relative returns. When selecting companies, we evaluate their valuation levels and growth potential more strictly."

At the time, China Mobile (listed in Hong Kong) also had a historically low valuation.

After China Mobile (listed in A-share market) was listed in 2022 and its stock price increased, Fu Pengbo continuously reduced his holdings of China Mobile (listed in Hong Kong).

In the first quarter report of 2023, Fu Pengbo significantly reduced his holdings of China Mobile (listed in Hong Kong) by 2.122 million shares.

In the quarterly report, Fu Pengbo mentioned that the attractiveness of China Mobile (listed in Hong Kong) decreased because of the choice of companies with reasonable valuation, growth certainty, and continuity.

After reducing his holdings for several consecutive quarters, Fu Pengbo and Zhao Feng also gained a lot of excess returns with the increase of China Mobile stock price.

Looking at the heavy holdings of China Telecom AH shares in the second quarter of 2024, Qu Yang's multiple funds under management significantly increased their holdings.

At the same time, Qu Yang's Qianhai Kaiyuan China Scarce Assets Fund, of which he is in charge, heavily increased its holdings of China Mobile (listed in A-share market), but from the quarterly report, we did not see much explanation.

In 2019 and 2020, Qu Yang enjoyed a great reputation in the market.

His management scale reached nearly 10 billion in early 2020 and 60 billion yuan by the end of the second quarter of 2021, but he only had 18.79 billion yuan left by the second quarter of 2024.

Qu Yang is good at timing investment and is known for trend investment. Looking at his operations since 2023, it can be said that he has been sprinting all the way on the road of pursuing high dividend assets.

During the China Mobile's surge in the first quarter of 2023, Qu Yang continuously chased the increase and bought a large number of China Mobile AH shares, holding a total market cap of over 1 billion, with Hong Kong stocks more than A shares.

In the third quarter, Qu Yang did AH stock rebalancing on China Mobile. Significantly increased A shares and reduced H shares, and in the fourth quarter, slightly increased position in China Mobile (A shares) and reduced position in China Mobile (AH shares) with large amounts.

Interestingly, in the first quarter of this year, after Qu Yang again increased positions in China Mobile AH shares, he heavily bought China Telecom (A shares), and in the second quarter, he heavily bought China Telecom (H shares).

At the same time, Qu Yang also heavily bought China Oil and China National Offshore Oil.

However, these 'bull stocks' did not contribute much to the performance of the products. Over the past two years, Qu Yang's performance has fallen behind. Among the 8 products he manages this year, 5 maintain a yield of around 3%, and 3 products have negative returns.

From the second quarter of 2024, the quarterly report holdings of the three major A-share heavyweight funds of the three major operators show that Da Cheng Internet Thinking Hybrid Fund has a high exposure rate.

In the second quarter of this year, Wang Shuai's Da Cheng Internet Thinking Hybrid fund increased its positions in China Mobile (A shares) by 1.02 million shares and in China Telecom (A shares) by 10.64 million shares, but reduced its position in China Unicom (A shares) by 15.12 million shares.

Wang Shuai's three major operators followed them all the way up.

From his past holdings, Wang Shuai now mostly allocates to those popular stocks in early 2023 in terms of AI computing power.

But because of his short tenure, it remains to be seen whether he can form his own investment philosophy in the future.

In summary.

CNOOC and China Mobile are increasingly becoming the standard for public and private equity funds. As representatives of current dividend assets, they are indeed the best option for risk aversion and stable returns.

Only by looking at it over a longer period of time and within the scope of the whole market, will investment ideas and choices differ.

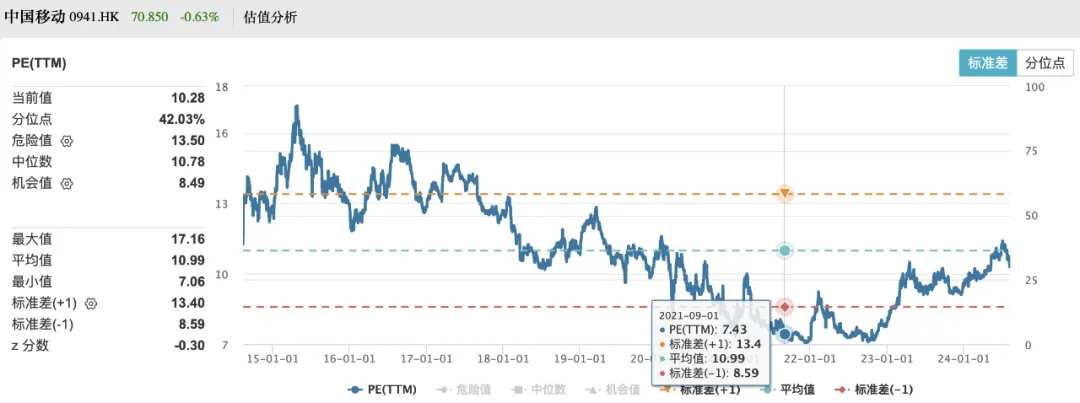

It should be known that China Mobile was once cold-shouldered by the market for many years. In early 2021, a small number of sensitive investors who were heavily invested in it found that 'there were no sell-side reports on operators in the market.'

Now, the investors who calculated the accounts and bought these assets think that 'the price-to-performance ratio has decreased a lot.' This is normal, and the market is constantly re-evaluating excellent stocks.

Doing 'rebalancing' between operators and between A shares and H shares is also a process of seeking 'relative value'.

But it has not yet reached the real watershed.

It's just that many companies are now at the 'operator moment' in the market.

Editor/Somer