After a turbulent week, global bond markets calmed down as concerns about a potential downturn in the US economy subsided.

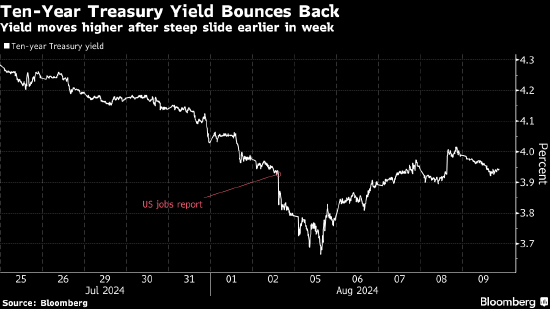

The benchmark 10-year US Treasury yield has returned to the level before the US labor market report was released last week, recovering most of the decline at the beginning of this week. Traders' expectations that the Federal Reserve will cut interest rates by an aggressive and unconventional margin have also weakened.

Globally, risk appetite gradually picked up as this week progressed, curtailing investors' interest in bonds across Europe, similar to the performance of the US Treasury bond market.

This week's sharp fluctuations highlight the nervousness of the market as investors try to determine the timing and pace of the Fed's interest rate cut. Economic data has once again become a key factor affecting market expectations. The July employment data triggered a sharp rise in treasury bonds last week, while the number of weekly unemployment claims this Thursday triggered a sell-off.

According to Coalition Greenwich data, in the seven trading days up to August 8, the volume of US Treasury bonds traded more than 1 trillion dollars on each trading day, setting a historical record of such a large number of consecutive transactions.

The inflation data will be the next test for the treasury bond market. Traders will be watching producer and consumer price indices on Tuesday and Wednesday to confirm that inflation is still falling, thereby supporting the Federal Reserve to cut interest rates as early as next month.

The 10-year Treasury yield fell to 3.67% at the beginning of the week and was close to 3.94% on Friday. The yield on 2-year Treasury bonds, which are sensitive to interest rate policies, rose 15 basis points to 4.03% this week. Short-term yields in the US bond market rose slightly on Friday, and the yield curve flattened out.

The three treasury tenders this week showed that investors are more interested in shorter term bonds. The $58 billion 3-year treasury tender received good demand, while the demand indicators for the 10-year and 30-year treasury tenders were weak.

The timing of interest rate cuts

The swap market shows that traders think September is the most likely month for the Federal Reserve to cut interest rates for the first time. The swap contract shows that month's interest rate cut was about 38 basis points.

Although this indicates that there are still some expectations that interest rates will be cut by 50 basis points in September, there has been a big correction compared to Monday's fixed price. At the time, market pricing showed that interest rates would be cut more than 25 basis points this year, and even one time during an unregular meeting. Traders now expect a policy easing margin of around 100 basis points during the year.

“The market will still worry about the risk of cutting interest rates by 50 basis points in September and the possibility of interest rate cuts between sessions, but both of these possibilities reflected in the market have declined sharply from recent highs,” Gennadiy Goldberg, an interest rate strategist at TD Securities, and others wrote in the report. “It is also still a concern that the Federal Reserve is speeding up the pace of interest rate cuts.”

TD Securities anticipates that the Federal Reserve will cut interest rates by 25 basis points per meeting starting in September until interest rates reach the so-called neutral level of 3% around the end of 2025. The bank believes this should cause the 10-year Treasury yield to fall to 3.4% by the end of the year and reach 3% by 2025.

The vast majority of economists surveyed expect interest rates to be cut by only 25 basis points in September.