indie Semiconductor, Inc. (NASDAQ:INDI) shares have had a horrible month, losing 32% after a relatively good period beforehand. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 41% in that time.

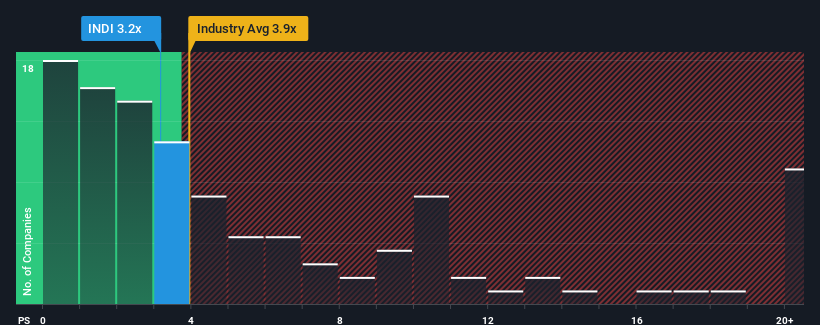

Even after such a large drop in price, there still wouldn't be many who think indie Semiconductor's price-to-sales (or "P/S") ratio of 3.2x is worth a mention when the median P/S in the United States' Semiconductor industry is similar at about 3.9x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

What Does indie Semiconductor's Recent Performance Look Like?

Recent times haven't been great for indie Semiconductor as its revenue has been rising slower than most other companies. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on indie Semiconductor will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For indie Semiconductor?

In order to justify its P/S ratio, indie Semiconductor would need to produce growth that's similar to the industry.

In order to justify its P/S ratio, indie Semiconductor would need to produce growth that's similar to the industry.

Taking a look back first, we see that the company grew revenue by an impressive 51% last year. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 30% as estimated by the eight analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 42%, which is noticeably more attractive.

In light of this, it's curious that indie Semiconductor's P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Bottom Line On indie Semiconductor's P/S

Following indie Semiconductor's share price tumble, its P/S is just clinging on to the industry median P/S. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

When you consider that indie Semiconductor's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for indie Semiconductor that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.